| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| UK Construction Aggregates Market Size 2024 |

USD 17,546.13 Million |

| UK Construction Aggregates Market, CAGR |

4.74% |

| UK Construction Aggregates Market Size 2032 |

USD 25,415.80 Million |

Market Overview

UK Construction Aggregates Market size was valued at USD 17,546.13 million in 2024 and is anticipated to reach USD 25,415.80 million by 2032, at a CAGR of 4.74% during the forecast period (2024-2032).

The UK Construction Aggregates Market is driven by increasing infrastructure development, rapid urbanization, and government investments in sustainable construction projects. The rising demand for aggregates in residential, commercial, and industrial construction fuels market expansion. Additionally, the shift toward recycled and sustainable aggregates, driven by stringent environmental regulations and a focus on reducing carbon footprints, is reshaping industry dynamics. Advancements in aggregate processing technologies enhance production efficiency and quality, further supporting market growth. Furthermore, the growing emphasis on smart cities and green building initiatives boosts the demand for eco-friendly aggregates. Supply chain optimization and strategic collaborations among key players enhance market competitiveness. However, fluctuating raw material costs and regulatory compliance challenges may impact growth. Overall, the market exhibits steady expansion, supported by infrastructure modernization and increasing adoption of recycled materials to meet sustainability goals while ensuring cost-effectiveness and long-term environmental benefits.

The UK construction aggregates market is geographically diverse, with significant demand driven by urbanization, infrastructure development, and sustainability initiatives across key regions such as London, Manchester, Birmingham, and Scotland. Each region experiences varying levels of aggregate consumption, influenced by large-scale residential, commercial, and public infrastructure projects. The market is highly competitive, with major players such as CRH plc, Colas Group, CEMEX S.A.B. de C.V., Heidelberg Materials AG, EUROVIA Kamenolomy AS, Sika AG, Tarmac, Buzzi S.p.A., Boral Limited, Carmeuse, CEMROS, and Holcim Group leading in aggregate production and distribution. These companies focus on innovation, sustainable material sourcing, and strategic partnerships to enhance market presence. The growing emphasis on recycled aggregates and eco-friendly construction materials further drives competition, compelling key players to invest in advanced technologies and sustainable solutions. With continuous urban expansion and infrastructure modernization, the UK construction aggregates market remains a dynamic and evolving sector.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The UK construction aggregates market was valued at USD 17,546.13 million in 2024 and is expected to reach USD 25,415.80 million by 2032, growing at a CAGR of 4.74% from 2024 to 2032.

- Increasing demand for sustainable and recycled aggregates is driving market growth, supported by stringent environmental regulations and circular economy initiatives.

- Infrastructure modernization projects, including smart city developments and transportation expansions, are fueling aggregate consumption across the UK.

- The market is highly competitive, with key players focusing on innovation, sustainable material sourcing, and strategic partnerships to strengthen their market position.

- Fluctuating raw material costs and stringent environmental regulations present challenges, impacting operational costs and production efficiency.

- London, Manchester, Birmingham, and Scotland are the key regions contributing to market growth, driven by urbanization and public infrastructure investments.

- Rising adoption of digital technologies in aggregate processing and supply chain management is enhancing efficiency and cost-effectiveness for industry players.

Report Scope

This report segments the UK Construction Aggregates Market as follows:

Market Drivers

Rising Infrastructure Development and Urbanization

The expansion of infrastructure projects across the UK is a key driver of the construction aggregates market. For instance, the UK government’s National Infrastructure and Construction Pipeline outlines over 660 projects and programs aimed at enhancing transportation networks, including roads, bridges, and railways. Government initiatives to enhance transportation networks, including roads, bridges, and railways, significantly increase the demand for aggregates. Additionally, large-scale urban development projects, such as housing schemes and commercial complexes, further contribute to market growth. With the UK’s population rising and urban centers expanding, the need for high-quality construction materials remains steady. The demand for aggregates is also fueled by ongoing renovation and modernization projects aimed at improving aging infrastructure. As a result, construction firms are increasingly sourcing aggregates to support sustainable and durable construction practices.

Growing Adoption of Recycled and Sustainable Aggregates

Environmental concerns and stringent regulations are driving the shift toward recycled and sustainable aggregates in the UK. For instance, the Mineral Products Association estimates that recycled and secondary aggregates accounted for 30% of the total aggregates supply in Great Britain in 2022. These materials not only help in waste management but also reduce dependency on virgin aggregates, contributing to a more sustainable construction ecosystem. Additionally, advancements in recycling technology have improved the quality and efficiency of recycled aggregates, making them a viable alternative to traditional materials. As sustainability becomes a key priority for the construction industry, the adoption of eco-friendly aggregates is expected to rise steadily.

Technological Advancements in Aggregate Production

Innovations in aggregate processing and production technologies are enhancing the efficiency and quality of materials used in construction. Modern crushing and screening equipment improve aggregate consistency, reducing waste and increasing production capacity. Automated processes and digital solutions, such as real-time monitoring systems, optimize supply chain operations and minimize downtime. Additionally, advancements in material testing and quality assurance ensure compliance with stringent regulatory standards. These technological improvements not only enhance productivity but also enable cost-effective production, making high-quality aggregates more accessible to the construction industry. As companies invest in advanced equipment and digital solutions, the UK construction aggregates market continues to evolve with greater efficiency and sustainability.

Government Regulations and Strategic Infrastructure Investments

The UK government plays a crucial role in shaping the construction aggregates market through regulatory policies and strategic investments. Stringent regulations regarding mining activities and environmental sustainability encourage the adoption of best practices in aggregate extraction and production. Furthermore, government funding for large-scale infrastructure projects, including high-speed rail, smart city initiatives, and energy-efficient buildings, boosts demand for high-quality aggregates. Public-private partnerships (PPPs) also drive market growth, ensuring steady investment in construction and infrastructure development. While regulatory compliance poses challenges for some companies, it also creates opportunities for innovation and sustainability-driven growth. As the government continues to focus on infrastructure modernization, the demand for construction aggregates remains strong, fostering long-term market expansion.

Market Trends

Rising Demand for Recycled and Secondary Aggregates

The UK construction aggregates market is witnessing a growing shift toward recycled and secondary aggregates due to increasing environmental concerns and stringent government regulations. For instance, the Mineral Products Association highlights that recycled and secondary aggregates, such as crushed concrete and reclaimed asphalt, accounted for a significant portion of the total aggregates supply in Great Britain. The adoption of crushed concrete, reclaimed asphalt, and industrial by-products like slag is increasing as they offer cost-effective and environmentally friendly alternatives to virgin aggregates. Additionally, government policies promoting circular economy practices and waste reduction are accelerating this trend. As recycling technologies advance, the quality and performance of secondary aggregates continue to improve, making them a preferred choice for sustainable construction projects.

Integration of Digital Technologies in Aggregate Processing

Technological advancements in aggregate production are enhancing efficiency, quality, and sustainability. The integration of digital solutions such as automation, AI-powered monitoring systems, and real-time data analytics is optimizing aggregate processing and supply chain operations. Smart crushing and screening equipment are improving material consistency and reducing energy consumption. Additionally, GPS tracking and automated logistics solutions are streamlining aggregate transportation, minimizing delays and costs. These innovations not only enhance operational efficiency but also contribute to lower carbon emissions by optimizing resource utilization. As construction firms embrace digital transformation, the aggregate market is expected to benefit from improved productivity and cost-effectiveness.

Expansion of Sustainable Infrastructure and Green Building Projects

The rising focus on sustainable infrastructure and green building initiatives is significantly influencing the UK construction aggregates market. For instance, the UK government’s Greening Government Commitments and the National Infrastructure and Construction Pipeline emphasize investments in eco-friendly projects, such as energy-efficient buildings and low-carbon transport infrastructure. Builders are incorporating aggregates that contribute to improved thermal insulation, reduced energy consumption, and enhanced structural durability. Additionally, green certification programs, such as BREEAM and LEED, are promoting the use of sustainable aggregates, compelling construction companies to prioritize environmentally responsible material sourcing.

Growth in Public-Private Partnerships for Infrastructure Development

Public-private partnerships (PPPs) are playing a crucial role in the expansion of the UK construction aggregates market. Government-backed infrastructure projects, including road expansions, railway modernization, and urban redevelopment, are being developed in collaboration with private firms, ensuring steady aggregate demand. These partnerships facilitate large-scale construction investments while promoting innovation in material usage and sustainable practices. Additionally, infrastructure resilience projects, aimed at mitigating the impact of climate change, are increasing the demand for durable aggregates capable of withstanding extreme weather conditions. As PPPs continue to drive infrastructure growth, the need for high-quality construction aggregates remains strong, fostering long-term market stability.

Market Challenges Analysis

Fluctuating Raw Material Costs and Supply Chain Disruptions

The UK construction aggregates market faces significant challenges due to fluctuating raw material costs and supply chain disruptions. For instance, the Office for National Statistics (ONS) highlights that global events such as the COVID-19 pandemic, Brexit, and the Suez Canal blockage have significantly disrupted supply chains, leading to material shortages and increased costs. Additionally, disruptions in the supply chain, caused by labor shortages, regulatory restrictions, and geopolitical uncertainties, further exacerbate market instability. The reliance on imported aggregates in certain regions adds to cost volatility, as global economic conditions influence material availability and pricing. To mitigate these challenges, industry players are increasingly investing in localized production facilities and exploring alternative raw material sources. However, maintaining a stable supply chain amidst economic uncertainties remains a persistent concern for the market.

Stringent Environmental Regulations and Land Use Restrictions

Stringent environmental regulations and land use restrictions present another significant challenge for the UK construction aggregates market. Regulatory bodies impose strict guidelines on quarrying and mining activities to minimize environmental impact, limiting the availability of extraction sites. Obtaining permits for new quarry developments is a time-consuming process, often delayed by environmental assessments and community opposition. Additionally, sustainability policies encourage reduced reliance on virgin aggregates, pushing companies to invest in recycling infrastructure and alternative materials. While these regulations support long-term environmental goals, they increase operational costs and compliance burdens for aggregate producers. Companies must adopt innovative and sustainable extraction methods to align with regulatory requirements while ensuring consistent aggregate supply for the construction industry.

Market Opportunities

The UK construction aggregates market presents significant growth opportunities driven by the increasing demand for sustainable and recycled materials. As environmental regulations become more stringent, there is a rising emphasis on using secondary aggregates such as crushed concrete, reclaimed asphalt, and industrial by-products. This shift not only supports sustainability goals but also helps construction firms reduce costs associated with raw material procurement. Advancements in recycling technologies further enhance the quality and usability of secondary aggregates, making them a viable alternative to traditional materials. Additionally, government incentives and policies promoting the circular economy encourage greater adoption of eco-friendly aggregates, providing a lucrative opportunity for companies investing in sustainable production and waste management solutions.

Infrastructure modernization projects and smart city initiatives offer another avenue for market expansion. The UK government’s commitment to upgrading transportation networks, energy-efficient buildings, and urban redevelopment drives the demand for high-quality aggregates. Public-private partnerships (PPPs) facilitate large-scale infrastructure investments, ensuring a steady requirement for durable and high-performance aggregates. Moreover, innovations in aggregate processing, such as automation and digital monitoring, improve efficiency and cost-effectiveness, making production more sustainable. Companies that leverage advanced technologies and strategic collaborations can capitalize on the growing infrastructure sector while aligning with sustainability objectives. As urbanization and green building initiatives gain momentum, the demand for premium construction aggregates is expected to rise, creating long-term growth prospects for industry players.

Market Segmentation Analysis:

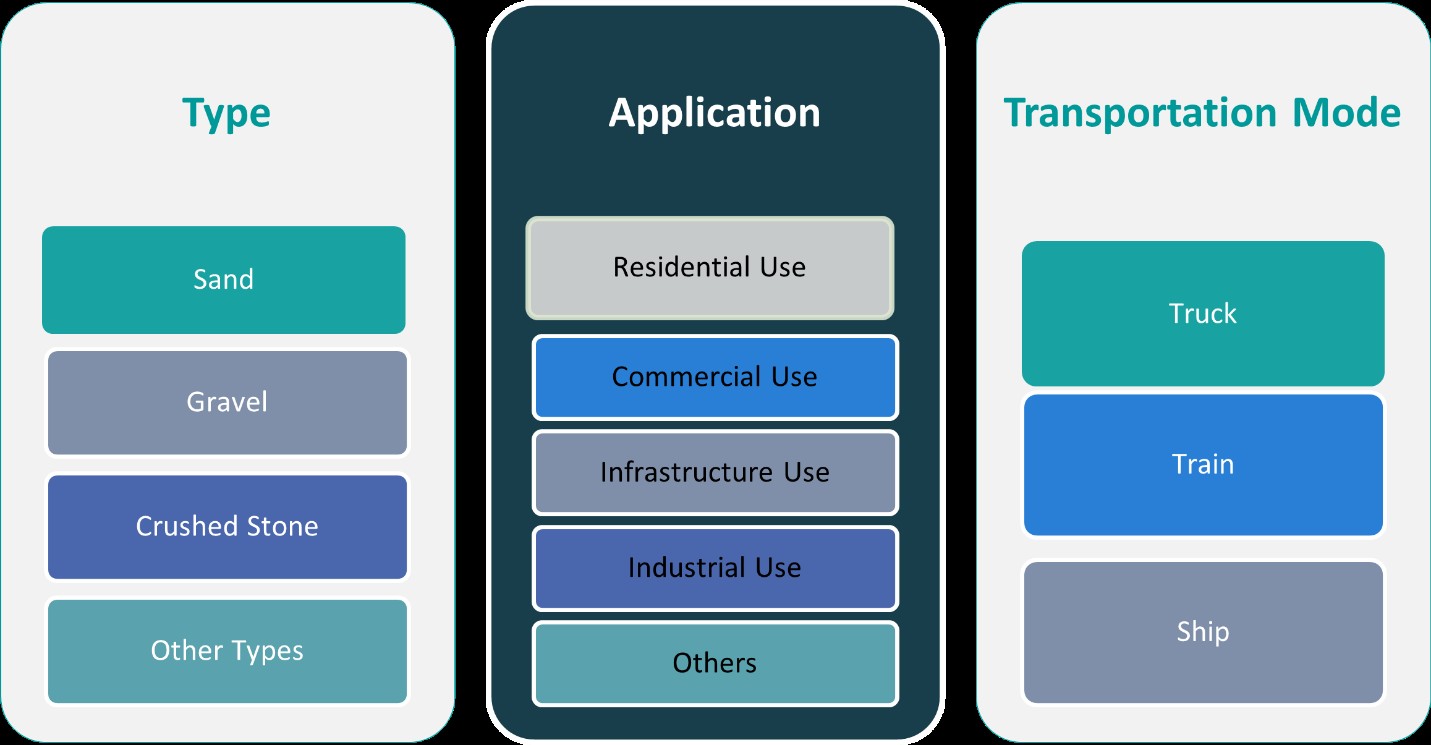

By Type:

The UK construction aggregates market is categorized into sand, gravel, crushed stone, and other types, each playing a crucial role in construction activities. Sand is a fundamental material used in concrete production, plastering, and masonry work, making it a vital component in both residential and commercial projects. The increasing demand for sustainable and fine aggregates in modern construction supports its market expansion. Gravel is widely used in road construction, drainage systems, and foundation work due to its durability and load-bearing capacity. With rising infrastructure development, including highways and rail networks, the demand for high-quality gravel continues to grow. Crushed stone serves as a key aggregate in concrete, asphalt production, and railway ballast, offering superior strength and versatility. Its increasing use in large-scale infrastructure projects drives its market demand. Other types of aggregates, including recycled materials and lightweight aggregates, are gaining traction as sustainable alternatives, further contributing to market diversification and environmental conservation efforts.

By Application:

Based on application, the UK construction aggregates market is segmented into residential, commercial, infrastructure, and industrial uses. Residential construction drives significant aggregate consumption, with growing housing projects increasing the demand for concrete, sand, and gravel in foundation work, flooring, and structural elements. Commercial construction, including office buildings, retail spaces, and mixed-use developments, fuels aggregate demand for durable and aesthetically appealing structures. The rise of urban commercial hubs continues to support this segment’s growth. Infrastructure development, such as roads, bridges, and transportation networks, remains a dominant consumer of aggregates. Government investments in smart cities, railway expansion, and energy-efficient infrastructure boost this segment’s market share. Industrial applications, including manufacturing facilities, warehouses, and heavy-duty flooring, require specialized aggregates with high compressive strength. The increasing focus on sustainable and cost-effective material sourcing in industrial construction further propels demand. With the UK’s emphasis on modernization and sustainability, all application segments contribute to the overall growth of the construction aggregates market.

Segments:

Based on Type:

- Sand

- Gravel

- Crushed Stone

- Other Types

Based on Application:

- Residential Use

- Commercial Use

- Infrastructure Use

- Industrial Use

Based on End- User:

Based on the Geography:

- London

- Manchester

- Birmingham

- Scotland

Regional Analysis

London

London dominates the UK construction aggregates market, accounting for approximately 35% of the total market share, driven by extensive urban development and infrastructure projects. As the country’s economic hub, London experiences high demand for aggregates in residential, commercial, and public sector construction. Major projects, such as high-rise buildings, transportation expansions like the Crossrail project, and smart city initiatives, fuel aggregate consumption. The city’s emphasis on sustainable construction and the adoption of recycled aggregates also contribute to market growth. With increasing housing demands and government policies supporting urban regeneration, London remains a key contributor to the overall expansion of the construction aggregates sector.

Manchester

Manchester holds around 25% of the UK construction aggregates market, supported by its growing real estate sector and infrastructure investments. As a major commercial and industrial center in northern England, the city witnesses significant demand for aggregates in residential and commercial construction. Urban redevelopment projects, including mixed-use spaces and transport infrastructure enhancements, drive market expansion. Additionally, the city’s commitment to sustainability encourages the use of eco-friendly aggregates, further propelling market growth. Ongoing developments in the Manchester Airport expansion, new housing initiatives, and road network improvements contribute to the rising demand for high-quality aggregates in the region.

Birmingham

Birmingham accounts for approximately 20% of the UK construction aggregates market, fueled by industrial and infrastructure advancements. As a key manufacturing and logistics hub, the city sees substantial aggregate consumption in warehouse construction, commercial buildings, and transport infrastructure. The High-Speed Rail 2 (HS2) project, connecting Birmingham to London, is a major driver of aggregate demand. Additionally, residential development projects aimed at addressing housing shortages further boost market activity. The city’s increasing focus on sustainable urban planning and smart construction solutions promotes the use of recycled aggregates, contributing to long-term market growth and environmental sustainability.

Scotland

Scotland represents 20% of the UK construction aggregates market, driven by large-scale infrastructure projects and government investments in sustainable development. The demand for aggregates is primarily influenced by public sector projects, including road expansions, renewable energy infrastructure, and urban regeneration initiatives. The Scottish government’s focus on net-zero construction and circular economy principles encourages the use of secondary and recycled aggregates, enhancing market sustainability. Additionally, Scotland’s rich natural reserves provide easy access to high-quality aggregates, reducing reliance on imports. As investments in green infrastructure and energy-efficient building projects increase, Scotland continues to be a significant player in the UK construction aggregates market.

Key Player Analysis

- CRH plc

- Colas Group

- CEMEX S.A.B. de C.V.

- Heidelberg Materials AG

- EUROVIA Kamenolomy AS

- Sika AG

- Tarmac

- Buzzi S.p.A.

- Boral Limited

- Carmeuse

- CEMROS

- Holcim Group

Competitive Analysis

The UK construction aggregates market is highly competitive, with leading players focusing on innovation, sustainability, and strategic expansion to maintain their market presence. Key players include CRH plc, Colas Group, CEMEX S.A.B. de C.V., Heidelberg Materials AG, EUROVIA Kamenolomy AS, Sika AG, Tarmac, Buzzi S.p.A., Boral Limited, Carmeuse, CEMROS, and Holcim Group. These companies leverage advanced technologies in aggregate processing, digital monitoring, and automation to enhance operational efficiency and cost-effectiveness. Sustainability is a key differentiator, with major players investing in recycled aggregates and eco-friendly production methods to comply with stringent environmental regulations. Strategic acquisitions, mergers, and collaborations play a crucial role in market expansion, allowing companies to strengthen their supply chains and broaden their geographical reach. Additionally, the rising demand for premium-quality aggregates in infrastructure projects and urban development drives competition. As government policies promote sustainable construction, industry leaders are focusing on innovation and environmentally responsible solutions to gain a competitive edge.

Recent Developments

- In September 2024, Holcim started the Holcim Sustainable Construction Academy. This is a free online training program that teaches about eco-friendly building methods. It helps people who work in construction learn new skills. The program offers both online classes and face-to-face training.

- In October 2024, CRH Ventures launched the Sustainable Building Materials accelerator to scale up creative climate and build technology firms that specialize in CO2-mineralized materials and sustainable binder solutions.

- In July 2024, Heidelberg Materials launched a recycling plant in Katowice, Poland, using a patented ReConcrete process to recycle demolition concrete and replace virgin material.

- In July 2024, Cemex USA formed a joint venture with Couch Aggregates and Premier Holdings for the production and distribution of aggregates in the Mid-South region. Cemex USA already had a strategic partnership with Couch Aggregates. The company stated that this vertical integration, combined with Premier Holdings’ Gulf Coast marine terminals, would accelerate its regional growth.

- In April 2024, Rogers Group joined The Road Forward initiative to advance sustainable asphalt production and paving practices.

- In January 2024, Heidelberg Materials launched Evo Build, its new global brand for low-carbon and circular products. This initiative aims to provide sustainable solutions for the construction industry, focusing on reducing carbon emissions and promoting circular economy principles.

Market Concentration & Characteristics

The UK construction aggregates market exhibits a moderate to high market concentration, with a mix of multinational corporations and regional players competing for market share. Leading companies such as CRH plc, Colas Group, CEMEX S.A.B. de C.V., Heidelberg Materials AG, and Holcim Group dominate the market through extensive production capacities, advanced processing technologies, and strong distribution networks. The market is characterized by a strong emphasis on sustainability, regulatory compliance, and resource efficiency, with growing demand for recycled and secondary aggregates. Stringent environmental regulations and land use restrictions create barriers to entry, favoring established players with the financial capacity to invest in eco-friendly production and innovation. Additionally, the industry relies on long-term infrastructure projects, ensuring stable demand but requiring high capital investment. Competition is driven by pricing strategies, quality differentiation, and technological advancements, with companies focusing on digitalization and automation to optimize aggregate processing and supply chain efficiency.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Type, Application, Transportation Mode and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The UK construction aggregates market is expected to witness steady growth, driven by increasing infrastructure development and urbanization.

- Sustainable and recycled aggregates will gain more traction as environmental regulations become stricter.

- Advancements in digital technologies and automation will enhance aggregate production efficiency and supply chain management.

- Rising investments in smart cities and green building projects will create new opportunities for market expansion.

- Leading companies will focus on mergers, acquisitions, and partnerships to strengthen their market presence and expand geographical reach.

- Government policies promoting circular economy initiatives will encourage greater adoption of secondary aggregates.

- Fluctuations in raw material costs and energy prices may pose challenges to profitability and production stability.

- Increased demand for high-performance aggregates in large-scale infrastructure projects will drive innovation and product development.

- Strategic investments in sustainable mining and quarrying practices will play a crucial role in long-term market growth.

- Regional market dynamics will be influenced by public infrastructure funding, private sector investments, and regulatory changes.