Market Overview

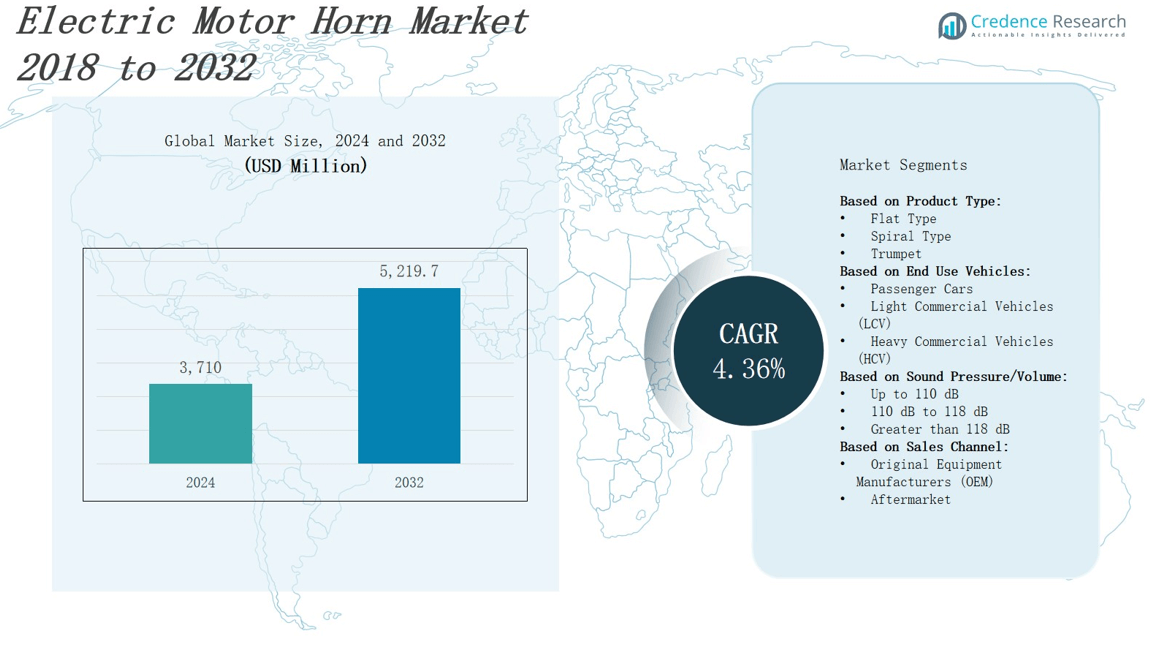

The electric motor horn market is projected to expand from in 2024 to USD 5,219.7 million by 2032, reflecting a CAGR of 4.36%.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Electric Motor Horn Market Size 2024 |

USD 3,710 million |

| Electric Motor Horn Market, CAGR |

4.36% |

| Electric Motor Horn Market Size 2032 |

USD 5,219.7 million |

Manufacturers are accelerating innovation in the electric motor horn market as regulatory mandates tighten vehicle safety standards and OEMs adopt advanced horn technologies to enhance auditory warnings. Rising electric vehicle production and urbanization drive demand for energy‑efficient, compact horns that integrate seamlessly with modern powertrains and ADAS platforms. Market participants are investing in IoT‑enabled, customizable‑tone systems to improve situational awareness and user experience. They also leverage durable, corrosion‑resistant materials to extend service life in harsh environments. Meanwhile, the shift toward sustainable designs fuels development of eco‑friendly components and recyclable materials, reflecting broader automotive industry commitments to environmental responsibility and optimization.

The electric motor horn market exhibits diverse demand across Asia Pacific, North America, Europe, Latin America, and the Middle East & Africa. Asia Pacific leads with EV adoption and urban fleets. North America drives through stringent safety regulations. Europe emphasizes regulatory compliance and advanced acoustic standards. Latin America growth stems from commercial vehicle upgrade. Middle East & Africa sees steady uptake. Key players such as Denso, FIAMM Technologies, HELLA, Johnson Electric, Robert Bosch, Nidec, Panasonic, MITSUBA, Imasen Electric Industrial, and UNO Minda compete through innovation, regional production, and OEM partnerships.

Market Insights

- The market will grow from USD 3,710 million in 2024 to USD 5,219.7 million by 2032 at a CAGR of 4.36%.

- Regulatory mandates tighten safety standards and OEMs adopt advanced horn technologies to boost auditory warnings

- Electric vehicle production and urbanization increase demand for compact, energy‑efficient horns integrated with modern powertrains and ADAS.

- IoT‑enabled, customizable‑tone systems improve situational awareness and user experience.

- Use of durable, corrosion‑resistant materials extends service life in harsh environments

- Shift toward eco‑friendly designs fuels development of recyclable horn components.

- Key players—including Denso, FIAMM Technologies, HELLA, Johnson Electric, Robert Bosch, Nidec, Panasonic, MITSUBA, Imasen Electric Industrial, and UNO Minda—compete through innovation and OEM partnerships.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Technological Advancements Enhance Performance

Automotive manufacturers integrate advanced materials and compact designs to boost horn clarity and volume. It improves auditory warnings in congested urban settings. The electric motor horn market benefits from innovations in piezoelectric and electromagnetic systems. Engineers test prototypes under extreme temperatures to ensure reliability. Regulatory bodies endorse horns that meet stringent decibel thresholds. This progress drives faster adoption of high‑performance horns across passenger and commercial vehicles.

- For instance, Valeo introduced a compact electric horn system designed to meet European regulatory limits while delivering clearer acoustic signals for passenger cars.

Regulatory Pressure Elevates Safety Standards

Governments enforce noise and performance regulations to safeguard road users. The electric motor horn market responds to new mandates that require consistent decibel levels and sound patterns. It aligns production with UNECE SAE guidelines. Manufacturers collaborate with testing labs for certification and compliance. Meeting these benchmarks improves market credibility. Companies invest in quality management systems to maintain regulatory adherence and reduce recall risks. Suppliers adopt digital tracking to ensure traceability.

- For instance, Hella partnered with TÜV Rheinland for third-party noise emission testing, validating performance against regulatory standards.

Electric Vehicle Adoption Spurs Demand

Growth in electric vehicle production increases demand for low‑power horns. OEMs integrate horns into compact EV architectures, battery management systems. It reduces power draw and aligns with sustainability goals. The electric motor horn market gains traction through strategic partnerships between horn suppliers and EV manufacturers. Engineers optimize circuitry to conserve battery life and prevent voltage fluctuations. Industry players scale manufacturing capacity to meet surging EV orders. Stakeholders forecast sustained global demand.

Integration with Advanced Driver Assistance Systems

Innovations in ADAS drive integration of intelligent acoustic alerts with vehicle safety systems. It enables directional sound emission linked to collision warning sensors. The electric motor horn market capitalizes on demand for synchronized audio‑visual alerts. Suppliers embed microcontrollers, variable tone modules to adapt horn patterns based on driving conditions. Engineers validate performance through road tests. Manufacturers upgrade software firmware for remote diagnostics. Consumers gain enhanced safety awareness through horn technologies.

Market Trends

Compact Designs and Integration with Vehicle Architectures

Manufacturers develop smaller, lightweight horns to fit modern vehicle layouts. The electric motor horn market gathers momentum through demand for unobtrusive components. Engineers optimize housing shapes to improve acoustic efficiency without sacrificing space. OEMs embed horns within bumper modules and crash structures. It aligns with trends in electric and hybrid powertrain packaging. Suppliers use precision stamping and molding techniques for consistent quality. Certification tests verify performance under tight installation constraints.

- For instance, FIAMM has engineered electric horns embedded within crash structures of hybrid vehicles, aligning with trends in electric and hybrid powertrain packaging and supporting compact vehicle design requirements.

Smart Horn Systems Enabled by Connectivity and Software

Developers integrate sensors and microcontrollers to enable adaptive warning signals. The electric motor horn market embraces software updates for tone modulation. Engineers link horns to vehicle networks for monitoring. It enhances safety through targeted alerts in critical scenarios. Manufacturers deploy over‑the‑air update capabilities to refine sound profiles. Certification bodies assess cyber resilience in connected horn modules. Companies test interfaces with ECU for seamless integration. Tier‑1 suppliers invest heavily in R&D.

- For instance, Bosch’s electric horn units incorporate adaptive sound control via sensor feedback that adjusts horn loudness and tone based on ambient noise levels, improving safety without exceeding noise pollution limits.

Sustainable Materials and Eco‑friendly Manufacturing Processes

Suppliers adopt biodegradable plastics and recyclable metals to meet environmental goals. The electric motor horn market shifts toward low‑emission production techniques. It reduces waste through closed‑loop recycling systems at manufacturing plants. Engineers source bio‑derived polymers to replace conventional resins. OEMs implement energy‑efficient stamping and injection molding lines. Certification bodies set emission targets for horn production. Tier‑2 vendors partner with recyclers to complete material recovery cycles. Industry groups publish sustainability standards.

Emerging Market Expansion and Aftermarket Growth Opportunities

Distributors target rising vehicle fleets in Asia‑Pacific and Latin America. The electric motor horn market experiences robust aftermarket sales in developing regions. It benefits from fleet modernization programs and parts refurbishment initiatives. Local workshops adopt OEM‑grade horns to meet quality standards. Suppliers launch training programs to support installation and maintenance. Market research firms project double‑digit growth in aftermarket demand. Companies negotiate distribution partnerships to strengthen regional presence. Exports grow rapidly.

Market Challenges Analysis

Complex Regulatory Compliance Across Regions

Regulatory bodies impose diverse noise and safety requirements across major markets. The electric motor horn market faces constant updates to UNECE and FMVSS standards. It must align product specifications with regional mandates before shipment. Manufacturers conduct extensive validation tests to ensure decibel levels and sound patterns meet local thresholds. Certification delays can hinder time‑to‑market and increase development costs. Suppliers collaborate with accredited labs to streamline approval processes. Companies maintain detailed documentation to support audits and reduce non‑compliance risks.

Supply Chain Disruptions and Cost Pressures

Global material shortages and tariff fluctuations challenge consistent horn production. It affects procurement of copper coils, magnets and housing components. Manufacturers absorb rising logistics expenses or negotiate long‑term contracts with vendors to secure supply. Lead time variability can force production schedule changes and inflate inventory carrying costs. Tier‑1 suppliers invest in regional sourcing to limit exposure to export restrictions. OEM partnerships require transparent cost reporting to justify price adjustments. Companies explore dual‑sourcing strategies to enhance resilience and maintain profitability under market volatility.

Market Opportunities

Integration into Autonomous and Electric Vehicle Platforms

OEMs pursue integration into emerging EV and autonomous vehicle architectures. The [electric motor horn market ] gains traction through demand for low‑power, compact acoustic devices. It benefits from partnerships between horn suppliers and vehicle OEMs. Compliance with electric drive system voltage requirements drives new designs. Tier‑1 vendors develop modular horns that work with ADAS sensor networks. Regulatory bodies support horns that deliver precise directional alerts. Consumer interest in advanced safety features boosts horn replacement and upgrade cycles.

Deployment of Smart and Adaptive Audio Warning Systems

Manufacturers develop horns with programmable tone patterns linked to onboard sensors. The [electric motor horn market ] finds opportunity in software‑enabled modules for variable alerts. It integrates microcontrollers that adjust sound based on speed and obstacle proximity. Tier‑2 vendors offer remote firmware update capabilities. OEMs test these systems in real‑world traffic scenarios. Partnerships with electronics firms accelerate innovation in networked warning solutions. Fleet operators plan retrofits to improve safety records.

Market Segmentation Analysis:

By Product Type:

Flat Type horns deliver crisp, focused audio signals in tight vehicle spaces. The electric motor horn market shows strong uptake of Spiral Type horns, which offer robust sound projection and compact installation. It favors Trumpet horns for heavy‑duty applications, where depth and volume meet stringent safety requirements. Manufacturers adjust diaphragm materials and coil specifications to match each horn style. OEMs select product types based on vehicle design constraints and acoustic performance targets. Tier‑1 suppliers maintain versatile production lines to address diverse format needs.

- For example, Hella’s Spiral horn installed in Audi models produces 110 dB, fitting easily into limited mounting areas.

By End Use Vehicles:

Passenger Cars drive volume growth through demand for stylish, low‑power horns. The electric motor horn market aligns product specifications with compact car architectures and urban safety norms. It supports Light Commercial Vehicles with horns calibrated for broader sound dispersion and higher durability. Engineers tailor heavy gauge windings to suit Heavy Commercial Vehicles, ensuring audible warnings under high engine noise. OEMs integrate horns within modular bumper assemblies. Suppliers collaborate with fleet operators to refine horn selection based on operational environments.

- For instance, Hella GmbH & Co. KGaA engineered multi-tone electric horns for light commercial vehicles to ensure broad sound dispersion and penetration in urban and industrial environments, enhancing driver and pedestrian safety.

By Sound Pressure/Volume:

Up to 110 dB horns cater to urban passenger vehicles where noise regulations demand moderate levels. The electric motor horn market grows through horns rated 110 dB to 118 dB, which balance compliance and driver awareness. It pushes development of Greater than 118 dB horns for commercial and industrial fleets that require maximum audibility. Manufacturers test prototypes under varying ambient noise conditions to validate performance. Tier‑2 vendors certify horns against international decibel standards. OEMs adjust amplifier circuits to optimize energy draw and sound output.

Segments:

Based on Product Type:

- Flat Type

- Spiral Type

- Trumpet

Based on End Use Vehicles:

- Passenger Cars

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

Based on Sound Pressure/Volume:

- Up to 110 dB

- 110 dB to 118 dB

- Greater than 118 dB

Based on Sales Channel:

- Original Equipment Manufacturers (OEM)

- Aftermarket

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America commands 25% of the electric motor horn market, ranking second behind Asia Pacific’s 40%. It benefits from a mature automotive industry and robust demand for advanced safety features. OEMs integrate energy‑efficient horns into passenger cars and light commercial vehicles to meet stringent FMVSS requirements. Suppliers leverage local content rules and electric vehicle incentives to streamline production. It supports aftermarket growth through structured replacement and upgrade programs. Partnerships between horn manufacturers and major automakers reinforce regional stability.

Europe

Europe holds 20% of the electric motor horn market, placing third after Asia Pacific and North America. It focuses on compliance with UNECE noise and performance standards. Manufacturers develop horns that deliver precise decibel levels while minimizing power draw. It sees steady uptake across passenger and commercial vehicle segments driven by environmental and safety regulations. OEMs work with Tier‑1 suppliers to embed horns into modular vehicle architectures. Investment in R&D strengthens product differentiation and market resilience.

Asia Pacific

Asia Pacific leads the electric motor horn market with 40% share, outpacing all other regions. It thrives on China’s vast vehicle production and rapid electric vehicle adoption. Local manufacturers innovate compact, low‑power horns suited to dense urban environments. It sees strong demand in India and Southeast Asia driven by expanding two‑wheeler and light commercial vehicle fleets. OEMs source horns locally to reduce lead times and logistics costs. Dealers and retrofit workshops further extend market penetration.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Johnson Electric

- HELLA

- UNO Minda

- Panasonic

- Robert Bosch

- FIAMM Technologies

- Denso

- Nidec

- MITSUBA

- Imasen Electric Industrial

Competitive Analysis

Denso and FIAMM Technologies lead competitive dynamics with broad portfolios and global reach. HELLA differentiates through advanced acoustic research and OEM collaborations. Johnson Electric focuses on cost efficient modules tailored to emerging markets. Bosch leverages sensor integration to deliver intelligent horn systems compatible with ADAS platforms. Panasonic invests in compact designs for electric vehicles to reduce power consumption and installation space. MITSUBA exploits regional production facilities to accelerate delivery and support local certification. Nidec emphasizes reliability through rigorous testing under extreme conditions and extended warranties. Imasen Electric Industrial competes through customizable tone profiles tailored for luxury segments. UNO Minda expands presence through aftermarket networks in Asia and Latin America. It fuels innovation by forging strategic alliances and file patents for novel diaphragm materials. Market participants pursue vertical integration to secure key raw materials and control costs. Sustained R&D investment remains critical to maintain competitive edge in performance and durability.

Recent Developments

- On October 3, 2024, Nidec Motor Corporation partnered with Ashok Leyland to supply its E‑Drive electric motor‑controller systems for commercial vehicles in India.

- In 2024, Uno Minda introduced the D‑90 horn range in India, delivering 105–110 dB output and OEM‑spec compatibility for Maruti Suzuki and Tata vehicles.

- In November 2023, Robert Bosch unveiled a prototype self‑adjusting horn system that automatically adapts volume based on ambient noise levels.

- On October 3, 2024, Nidec Motor Corporation partnered with Ashok Leyland to supply E‑Drive electric motor‑controller systems for commercial vehicles in India.

Market Concentration & Characteristics

The electric motor horn market exhibits high concentration with a handful of global players controlling majority revenue share. Tier‑1 companies like Denso, FIAMM Technologies, HELLA, and Robert Bosch command leading positions through extensive OEM partnerships and robust R&D investments. It features differentiated product portfolios spanning flat, spiral, and trumpet types that enable high‑precision applications across passenger cars, LCVs, and HCVs. Regional leaders in Asia Pacific leverage cost advantages and large vehicle volumes to outperform competitors. North American and European firms compete on compliance with stringent noise and safety standards that drive product innovation. The market’s moderate to high entry barriers include capital‑intensive manufacturing and complex certification processes. Procurement of high‑quality raw materials and precision tooling further limits new entrants. Market participants pursue global vertical integration to secure supply chains and strengthen aftermarket service networks. Continuous innovation in power‑efficient, adaptive‑tone horn systems keeps competition intense and sustains concentration among top vendors globally.

Report Coverage

The research report offers an in-depth analysis based on Produt Type, End-User Vehicle, Sound Pressure/Volume, Sales Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- OEMs will integrate horns with ADAS for directional acoustic alerts improving pedestrian and driver safety.

- Manufacturers will adopt eco-friendly materials to reduce environmental impact and comply with emerging sustainability regulations.

- Suppliers will develop low-power horn modules optimized for electric, hybrid vehicle platforms to improve efficiency.

- Companies will deploy over-the-air firmware updates enabling real-time refinement of horn sound profiles and performance.

- Tier‑1 vendors will expand regional manufacturing facilities to reduce logistics costs and meet local demand.

- Aftermarket channels will offer retrofit kits featuring smart, customizable-tone horn systems for improved vehicle safety.

- Engineers will optimize horn acoustics through simulation tools to ensure reliable performance under environmental conditions.

- Regulatory bodies will update noise standards to encourage adoption of precise horn systems in vehicles.

- Partnerships between horn suppliers and technology firms will drive IoT-enabled warning solutions for connected vehicles.

- Manufacturers will pursue vertical integration to secure critical raw materials and ensure stable supply chains.