CHAPTER NO. 1 : INTRODUCTION 21

1.1. Report Description 21

Purpose of the Report 21

USP & Key Offerings 21

1.2. Key Benefits for Stakeholders 22

1.3. Target Audience 22

CHAPTER NO. 2 : EXECUTIVE SUMMARY 23

CHAPTER NO. 3 : GUM GRAFTING MARKET FORCES & INDUSTRY PULSE 25

3.1. Foundations of Change – Market Overview 25

3.2. Catalysts of Expansion – Key Market Drivers 27

3.3. Momentum Boosters – Growth Triggers 28

3.4. Innovation Fuel – Disruptive Technologies 28

3.5. Headwinds & Crosswinds – Market Restraints 29

3.6. Regulatory Tides – Compliance Challenges 30

3.7. Economic Frictions – Inflationary Pressures 30

3.8. Untapped Horizons – Growth Potential & Opportunities and Strategic Navigation – Industry Frameworks 31

3.9. Market Equilibrium – Porter’s Five Forces 32

3.10. Ecosystem Dynamics – Value Chain Analysis 34

3.11. Macro Forces – PESTEL Breakdown 36

CHAPTER NO. 4 : COMPETITION ANALYSIS 38

4.1. Company Market Share Analysis 38

4.1.1. Asia Pacific Gum Grafting Market Company Revenue Market Share 38

4.2. Strategic Developments 40

4.2.1. Acquisitions & Mergers 40

4.2.2. New End-User Launch 41

4.2.3. Agreements & Collaborations 42

4.3. Competitive Dashboard 43

4.4. Company Assessment Metrics, 2024 44

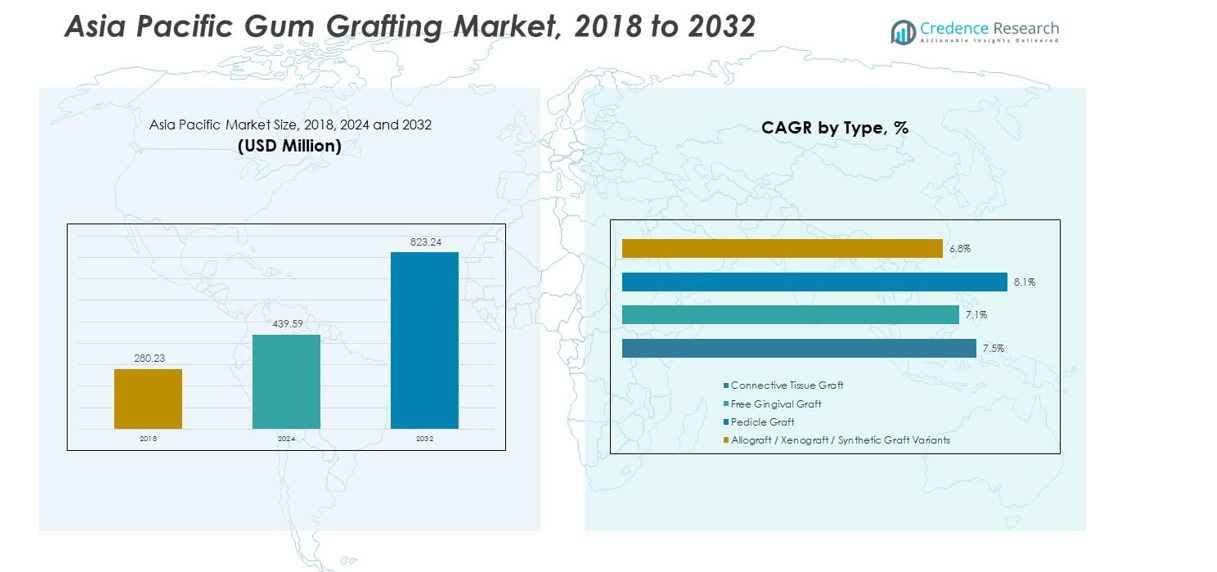

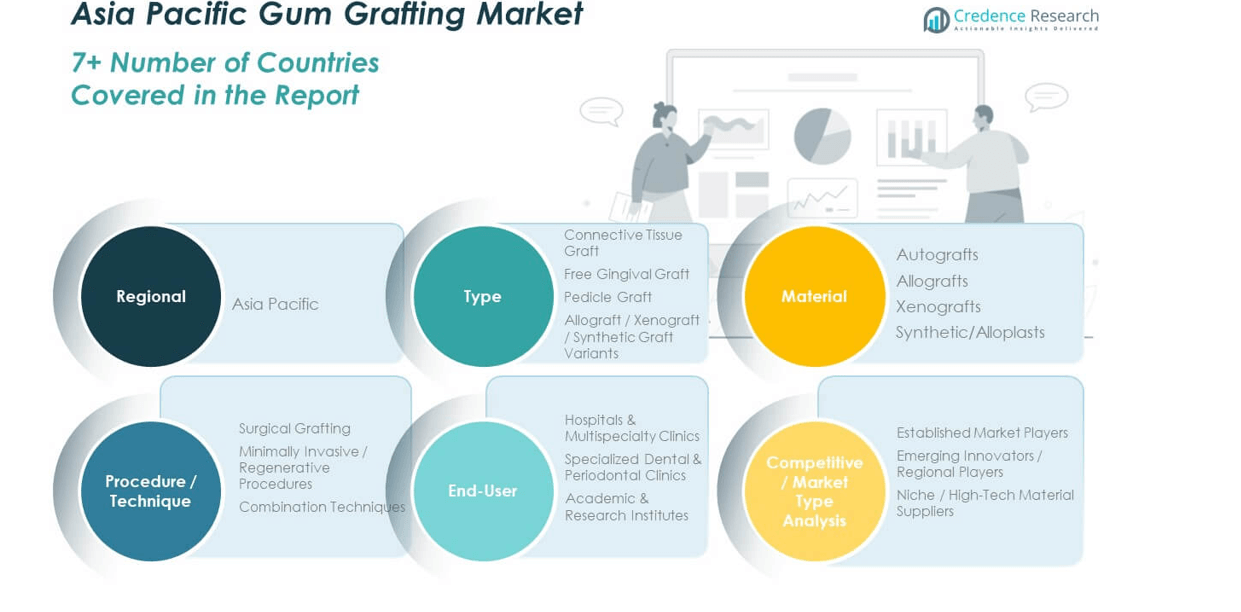

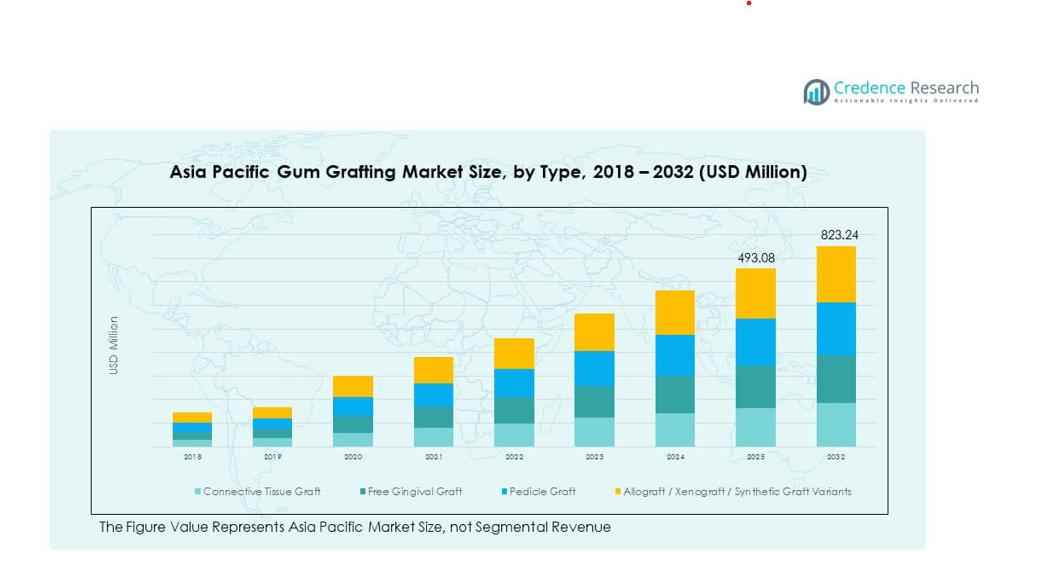

CHAPTER NO. 5 : ASIA PACIFIC MARKET ANALYSIS, INSIGHTS & FORECAST, BY TYPE 45

CHAPTER NO. 6 : ASIA PACIFIC MARKET ANALYSIS, INSIGHTS & FORECAST, BY MATERIAL 49

CHAPTER NO. 7 : ASIA PACIFIC MARKET ANALYSIS, INSIGHTS & FORECAST, BY PROCEDURE / TECHNIQUE 53

CHAPTER NO. 8 : ASIA PACIFIC MARKET ANALYSIS, INSIGHTS & FORECAST, BY END-USER 57

CHAPTER NO. 9 : ASIA PACIFIC MARKET ANALYSIS, INSIGHTS & FORECAST, BY COMPETITIVE / MARKET TYPE ANALYSIS 61

CHAPTER NO. 10 : ASIA PACIFIC MARKET ANALYSIS, INSIGHTS & FORECAST, BY COUNTRY 65

CHAPTER NO. 11 : COMPANY PROFILE 68

11.1. Straumann Holding AG 68

11.2. Dentsply Sirona 71

11.3. Zimmer Biomet 71

11.4. 3M 71

11.5. Company 5 71

11.6. Company 6 71

11.7. Company 7 71

11.8. Company 8 71

11.9. Company 9 71

11.10. Company 10 71

11.11. Company 11 71

11.12. Company 12 71

11.13. Company 13 71

11.14. Company 14 71

List of Figures

FIG NO. 1. Gum Grafting Market Revenue Share, By Type, 2024 & 2032 45

FIG NO. 2. Market Attractiveness Analysis, By Type 46

FIG NO. 3. Incremental Revenue Growth Opportunity by Type, 2024 – 2032 47

FIG NO. 4. Gum Grafting Market Revenue Share, By Material, 2024 & 2032 49

FIG NO. 5. Incremental Revenue Growth Opportunity by Material, 2024 – 2032 50

FIG NO. 6. Incremental Revenue Growth Opportunity by Material, 2024 – 2032 51

FIG NO. 7. Gum Grafting Market Revenue Share, By Procedure / Technique, 2024 & 2032 53

FIG NO. 8. Market Attractiveness Analysis, By Procedure / Technique 54

FIG NO. 9. Incremental Revenue Growth Opportunity by Procedure / Technique, 2024 – 2032 55

FIG NO. 10. Gum Grafting Market Revenue Share, By End-User, 2024 & 2032 57

FIG NO. 11. Market Attractiveness Analysis, By End-User 58

FIG NO. 12. Incremental Revenue Growth Opportunity by End-User, 2024 – 2032 59

FIG NO. 13. Gum Grafting Market Revenue Share, By Competitive / Market Type Analysis, 2024 & 2032 61

FIG NO. 14. Market Attractiveness Analysis, By Competitive / Market Type Analysis 62

FIG NO. 15. Incremental Revenue Growth Opportunity by Competitive / Market Type Analysis, 2024 – 2032 63

FIG NO. 16. Analytical Instrumentation Market Revenue Share, By Country, 2024 & 2032 65

List of Tables

TABLE NO. 1. : Asia Pacific Gum Grafting Market Revenue, By Type, 2018 – 2024 (USD Million) 48

TABLE NO. 2. : Asia Pacific Gum Grafting Market Revenue, By Type, 2025 – 2032 (USD Million) 48

TABLE NO. 3. : Asia Pacific Gum Grafting Market Revenue, By Material, 2018 – 2024 (USD Million) 52

TABLE NO. 4. : Asia Pacific Gum Grafting Market Revenue, By Material, 2025 – 2032 (USD Million) 52

TABLE NO. 5. : Asia Pacific Gum Grafting Market Revenue, By Procedure / Technique, 2018 – 2024 (USD Million) 56

TABLE NO. 6. : Asia Pacific Gum Grafting Market Revenue, By Procedure / Technique, 2025 – 2032 (USD Million) 56

TABLE NO. 7. : Asia Pacific Gum Grafting Market Revenue, By End-User, 2018 – 2024 (USD Million) 60

TABLE NO. 8. : Asia Pacific Gum Grafting Market Revenue, By End-User, 2025 – 2032 (USD Million) 60

TABLE NO. 9. : Asia Pacific Gum Grafting Market Revenue, By Competitive / Market Type Analysis, 2018 – 2024 (USD Million) 64

TABLE NO. 10. : Asia Pacific Gum Grafting Market Revenue, By Competitive / Market Type Analysis, 2025 – 2032 (USD Million) 64

TABLE NO. 11. : Asia Pacific Gum Grafting Market Revenue, By Country, 2018 – 2024 (USD Million) 66

TABLE NO. 12. : Asia Pacific Gum Grafting Market Revenue, By Country, 2025– 2032 (USD Million) 67