Ambulatory EHR Market Overview:

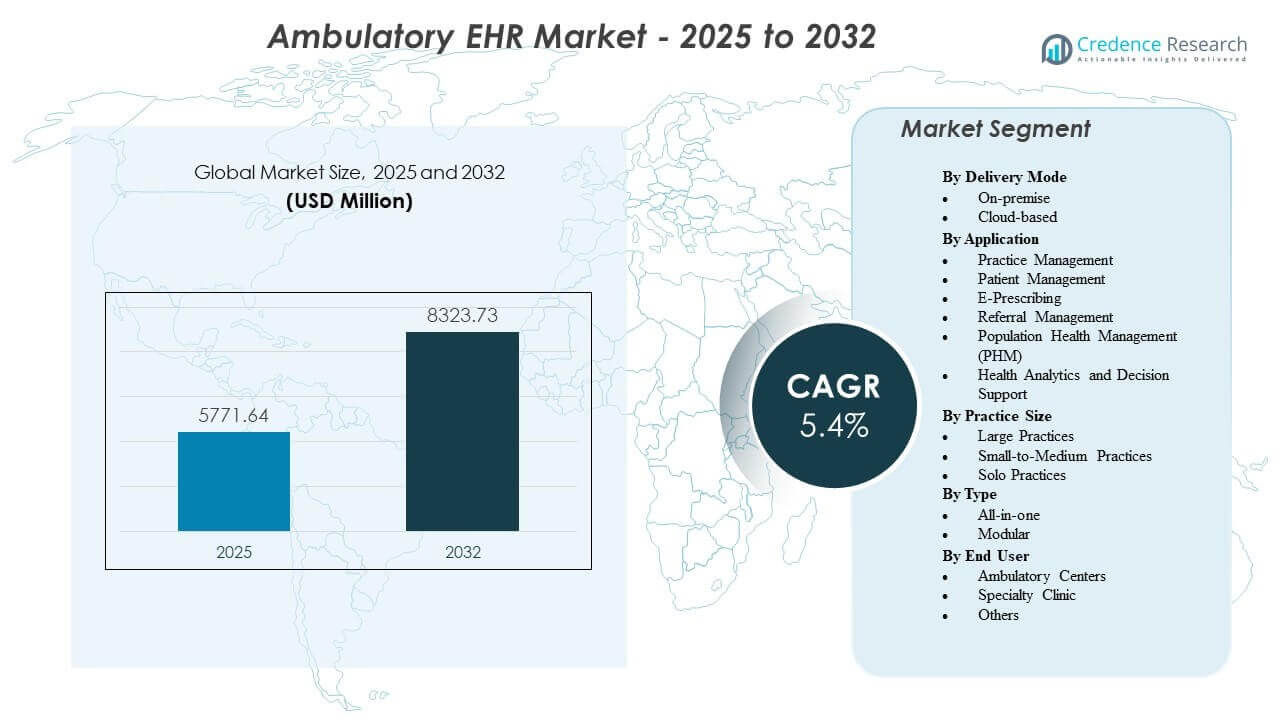

The Ambulatory EHR Market is projected to grow from USD 5,771.64 million in 2025 to an estimated USD 8,323.73 million by 2032, with a compound annual growth rate (CAGR) of 5.4% from 2025 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Ambulatory EHR Market Size 2025 |

USD 5,771.64 Million |

| Ambulatory EHR Market, CAGR |

5.4% |

| Ambulatory EHR Market Size 2032 |

USD 8,323.73 Million |

Ambulatory EHR Market Insights:

- Growing outpatient volumes, regulatory compliance needs, and demand for interoperable digital systems continue to push clinics toward advanced EHR platforms that improve workflow accuracy and care coordination.

- High implementation costs, workflow disruption during transitions, and data privacy risks create restraints that slow adoption among smaller practices with limited IT and financial resources.

- North America leads due to established digital health infrastructure, while Europe follows with strong national e-health programs supporting coordinated outpatient care.

- Asia Pacific remains the fastest-growing region, driven by expanding private healthcare networks and rising investments in cloud-based EHR platforms across developing markets.

Ambulatory EHR Market Drivers

Rising Outpatient Volumes And Expansion Of Specialty Care Networks Across Urban And Semi-Urban Regions

Outpatient visits continue to increase across primary and specialty care clinics. Healthcare systems shift non-critical services from hospitals to ambulatory centers. This transition raises demand for structured digital record systems. Clinics require centralized data access across multiple locations. Physicians depend on real-time patient history for accurate decisions. Administrative teams seek tools that reduce paperwork and manual errors. Digital scheduling and billing improve patient throughput. The Ambulatory EHR Market benefits from this steady shift toward organized outpatient care delivery.

- For instance, Epic confirmed that more than 165 million patients actively use its MyChart portal, supporting large ambulatory networks with unified access to clinical records.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Regulatory Compliance Requirements And Quality Reporting Mandates Across Healthcare Systems

Governments enforce strict documentation and reporting standards. Clinics must adopt certified EHR platforms to meet compliance rules. Quality-based reimbursement models depend on accurate data capture. Digital audit trails support transparency in patient care. Interoperability mandates push providers to share records securely. Standardized coding systems improve claim accuracy. Secure storage reduces legal and operational risks. These regulatory factors drive consistent demand for advanced ambulatory EHR solutions.

- For instance, athenahealth publicly reports that its cloud network supports over 160,000 providers, enabling large-scale electronic quality reporting aligned with federal compliance programs.

Need For Operational Efficiency And Cost Optimization In Independent And Group Practices

Independent clinics face pressure to control operating expenses. Manual record systems create delays and billing gaps. Automated workflows streamline appointment scheduling and claims processing. Clinical templates reduce documentation time per visit. Integrated revenue cycle modules enhance payment tracking. Cloud deployment reduces hardware and maintenance costs. Central dashboards help practice managers monitor performance. Efficiency-focused investments strengthen adoption across small and mid-sized practices.

Growing Emphasis On Patient-Centered Care And Coordinated Treatment Pathways

Patients expect seamless communication and digital access to records. Secure portals allow online appointment booking and prescription requests. Shared records improve coordination between specialists and primary physicians. Care teams use structured data to track chronic conditions. Preventive care reminders support better outcomes. Digital alerts reduce duplication of tests and procedures. Mobile access enhances physician flexibility. These factors reinforce long-term demand for modern ambulatory systems.

Ambulatory EHR Market Trends

Integration Of Artificial Intelligence Tools For Clinical Decision Support And Workflow Automation

Healthcare providers adopt AI-driven modules within ambulatory systems. Predictive analytics assist physicians with diagnosis support. Automated coding tools improve billing accuracy. Natural language processing converts voice notes into structured records. Risk scoring models identify high-risk patients. Data dashboards provide actionable insights in real time. AI enhances productivity across outpatient settings. The Ambulatory EHR Market reflects steady integration of intelligent automation features.

Expansion Of Cloud-Native Platforms With Subscription-Based Pricing Models

Vendors move toward fully cloud-based infrastructure. Subscription models reduce upfront capital costs for clinics. Remote access supports multi-location practice networks. Automatic updates improve system performance and security. Cloud hosting enables faster deployment cycles. Scalable storage supports long-term data growth. Smaller clinics prefer flexible pricing structures. This transition reshapes competitive dynamics among EHR vendors.

Adoption Of Interoperability Standards And Health Information Exchange Connectivity

Healthcare systems prioritize seamless data exchange. Standard protocols enable secure sharing across providers. National health networks promote connected care ecosystems. Ambulatory platforms integrate with labs, pharmacies, and imaging centers. Real-time data flow improves treatment continuity. Structured APIs support third-party app integration. Health information exchanges expand across regions. Interconnected systems strengthen coordinated outpatient care delivery.

- For instance, Epic Systems verifies that its interoperability framework, Care Everywhere, supports over 21 million patient record exchanges per day, reinforcing large-scale connected care.

Growth Of Mobile-First Interfaces And Remote Access Capabilities For Physicians

Mobile devices play a larger role in clinical workflows. Physicians access patient records through tablets and smartphones. Secure authentication protects sensitive health data. Remote chart review supports flexible work models. Mobile alerts notify providers about urgent updates. User-friendly dashboards improve adoption among older practitioners. Digital signature tools speed up documentation tasks. Mobile-enabled platforms increase overall system usability in ambulatory care.

- For instance, DrChrono publicly states that its EHR mobile app has been downloaded over 1 million times, confirming strong adoption of mobile-first tools among outpatient providers.

Ambulatory EHR Market Challenges Analysis

High Implementation Costs And Workflow Disruption During System Transition Phases

EHR deployment requires significant upfront investment. Clinics must allocate funds for software licenses and training. Data migration from legacy systems creates operational complexity. Staff resistance slows adoption in some practices. Temporary workflow disruption affects patient scheduling. Customization demands increase vendor service costs. Technical downtime can reduce clinic productivity. The Ambulatory EHR Market faces barriers when smaller providers hesitate to upgrade systems.

Cybersecurity Risks And Data Privacy Concerns Across Connected Healthcare Networks

Digital records attract cyber threats and data breaches. Clinics must comply with strict data protection laws. Security upgrades require continuous monitoring and updates. Weak access controls expose sensitive patient information. Phishing attacks target healthcare staff frequently. Cloud platforms demand strong encryption standards. Incident response plans add operational burden. Privacy concerns remain a persistent challenge for outpatient digital systems.

Ambulatory EHR Market Opportunities

Expansion Into Emerging Economies With Growing Private Healthcare Infrastructure Development

Emerging markets invest heavily in outpatient clinic networks. Governments promote digital health reforms in urban centers. Private hospital chains expand specialty clinics rapidly. Local providers seek scalable and affordable EHR platforms. Cloud deployment reduces infrastructure barriers. Training programs improve digital literacy among medical staff. International vendors form partnerships with regional IT firms. These developments create new revenue streams for ambulatory EHR providers.

Integration With Value-Based Care Models And Population Health Management Programs

Healthcare systems adopt performance-based reimbursement frameworks. Providers require structured data to track patient outcomes. Population health modules support chronic disease monitoring. Risk stratification tools enhance preventive care planning. Analytics dashboards improve cost transparency. Coordinated care pathways depend on shared digital records. Telehealth integration broadens service reach. Strong alignment with value-based strategies presents long-term growth opportunities.

Ambulatory EHR Market Segmentation Analysis:

By Delivery Mode

On-premise systems remain relevant in environments that require strict data control and customized workflows. These deployments suit organizations with strong IT teams and legacy infrastructure. Security-focused clinics value local data storage and dedicated server setups. Upgrades demand higher investment but provide deeper configuration options. Cloud-based platforms lead growth due to flexible access and lower upfront costs. Clinics prefer automatic updates and scalable storage offered through subscription models. Remote access supports multi-site networks. The Ambulatory EHR Market reflects a steady shift toward cloud-native systems across diverse practice settings.

By Application

Practice management tools support appointment scheduling, claim workflows, and billing operations. Patient management modules streamline charting, care histories, and clinical documentation. E-prescribing improves medication accuracy and reduces administrative delays. Referral management strengthens communication between primary and specialty providers. Population health management (PHM) helps clinics monitor chronic diseases and coordinate preventive care. Health analytics and decision support provide insights that guide clinical performance. Clinics rely on integrated applications to support digital transformation. These functions raise efficiency in outpatient workflows.

By Practice Size

Large practices adopt advanced systems to support high patient volume and complex workflows. These setups integrate multiple specialties and depend on strong interoperability. Small-to-medium practices seek cost-effective tools that balance functionality and ease of use. Cloud deployment appeals to clinics with limited IT staffing. Solo practices require intuitive platforms with simplified dashboards and minimal training needs. Vendor support plays a key role in adoption across practice sizes. Each group selects digital tools that match operational intensity. This variation shapes product demand across the segment.

By Type

All-in-one platforms provide integrated tools within a unified system. Clinics choose these solutions to simplify vendor management and improve workflow cohesion. These platforms combine scheduling, charting, billing, and analytics. Modular systems offer flexibility for clinics that want tailored features. Specialty providers often add components based on clinical needs. Modular tools support gradual upgrades without major disruptions. Interoperability shapes system selection across many clinics. The structure of each type influences digital strategy across outpatient settings.

- For instance, NextGen Healthcare publicly confirms widespread adoption of its specialty-driven modular EHR solutions, used by thousands of ambulatory practices across diverse clinical domains.

By End User

Ambulatory centers adopt EHR platforms to streamline outpatient care and improve patient flow. These centers depend on digital tools to manage multi-specialty coordination. Specialty clinics require advanced clinical templates and diagnostic data integration. Their workflows benefit from customized modules. Other users include urgent care centers and community health practices that need scalable systems. These groups invest in EHR tools to support accurate records and faster care delivery. Each user category selects platforms aligned with operational focus and service complexity.

- For instance, DrChrono reports over 1 million downloads of its mobile EHR app, showing strong adoption among ambulatory and urgent care settings seeking mobile-first workflows.

Segmentation:

By Delivery Mode

By Application

- Practice Management

- Patient Management

- E-Prescribing

- Referral Management

- Population Health Management (PHM)

- Health Analytics and Decision Support

By Practice Size

- Large Practices

- Small-to-Medium Practices

- Solo Practices

By Type

By End User

- Ambulatory Centers

- Specialty Clinic

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America holds the largest share of the Ambulatory EHR Market at around 45%, supported by strong digital health infrastructure and long-standing EHR incentive programs. The United States leads adoption due to mature interoperability frameworks and widespread use of cloud-based systems in outpatient clinics. Canada strengthens growth with federal support for digital patient records. Regional providers invest in integrated platforms to enhance coordinated care. Vendor presence remains strong across hospital-owned and independent clinics. The region maintains leadership through continuous innovation and regulatory alignment.

Europe accounts for nearly 28% of the global share, driven by national e-health mandates and EHR modernization programs. Countries such as Germany and the United Kingdom show faster adoption due to structured digital transformation funding. Clinics invest in standardized data systems to improve quality reporting and patient engagement. The region prioritizes interoperability across public and private networks. Local vendors compete with global companies through specialty-focused solutions. The Ambulatory EHR Market benefits from steady investment across primary and specialty care environments.

Asia Pacific holds close to 20% of the market share and remains the fastest-growing region with rising digital adoption across China, India, Japan, and Australia. Governments promote electronic records to support outpatient workflow modernization. Private healthcare chains introduce cloud-based systems to scale operations across multiple clinics. Interoperability initiatives expand gradually across national networks. Rural digitization programs increase demand for low-cost and mobile-enabled platforms. The region strengthens its presence through strong economic growth and expanding care delivery networks.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Epic Systems Corporation

- eClinicalWorks

- Athenahealth

- NextGen Healthcare

- Oracle Health (formerly Cerner)

- Kareo Clinical / Tebra

- Allscripts / Veradigm

- PrognoCIS (Bizmatics)

- AdvancedMD

- DrChrono

Competitive Analysis:

The Ambulatory EHR Market features strong competition among global vendors and regional specialists that target outpatient workflows. Leading companies focus on developing cloud-based platforms that reduce operational complexity for clinics. Many providers prioritize interoperability tools that link ambulatory centers with hospitals, labs, and pharmacies. Vendors compete by adding AI-driven decision support, voice-enabled documentation, and advanced analytics modules. Pricing flexibility plays a major role in adoption among small and medium practices. Large practices prefer integrated suites with practice management, billing, and population health tools. The competitive landscape shifts as companies form partnerships with telehealth platforms and health information exchanges. Product differentiation depends on usability, specialty templates, and regulatory compliance features. Regional vendors gain traction by offering localized solutions and multilingual interfaces.

Recent Developments:

- In June 2025, MEDITECH expanded its Expanse EHR system across 132 clinics with Willis Knighton Health System. The rollout consolidated three prior EHRs, enhancing care coordination between ambulatory and acute settings while supporting specialized workflows like oncology.

- In February 2025, athenahealth partnered with Abridge to integrate generative AI capabilities into its Ambient Notes solution for ambulatory care practices. This collaboration embeds real-time ambient listening and AI-generated documentation directly into athenaOne EHR, reducing clinician administrative burdens and improving efficiency for over 160,000 users.

- In November 2024, Veradigm released Ambient Scribe, an AI-powered tool that captures patient conversations and generates structured notes within its ambulatory EHR platform. This innovation uses standards-based APIs to integrate with various systems, aiming to streamline documentation and boost interoperability.

Report Coverage:

The research report offers an in-depth analysis based on Delivery Mode, Application, Practice Size, Type, End User and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Rising adoption of cloud-based platforms will strengthen system scalability and enable wider deployment across small and mid-sized clinics in the Ambulatory EHR Market.

- AI-driven automation will enhance clinical documentation speed and improve decision support accuracy for outpatient providers.

- Interoperability frameworks will expand, creating stronger data exchange between ambulatory centers, hospitals, labs, and pharmacies.

- Demand for mobile-enabled EHR interfaces will grow as physicians rely on remote access and flexible charting tools.

- Population health features will gain traction, supporting chronic disease management and preventive care strategies in outpatient settings.

- Specialty clinics will adopt advanced modules tailored to unique workflows and diagnostic requirements.

- Practice analytics will become a core feature as clinics seek insights to improve revenue performance and operational efficiency.

- Regulatory reforms will continue to promote structured reporting, ensuring consistent digital adoption across diverse practices.

- Emerging markets will accelerate adoption due to rapid clinic expansion and increasing investment in digital health ecosystems.

- Vendor competition will intensify as platforms integrate telehealth, billing automation, and patient engagement tools into unified systems.