Ambulatory Infusion Centers Market Overview:

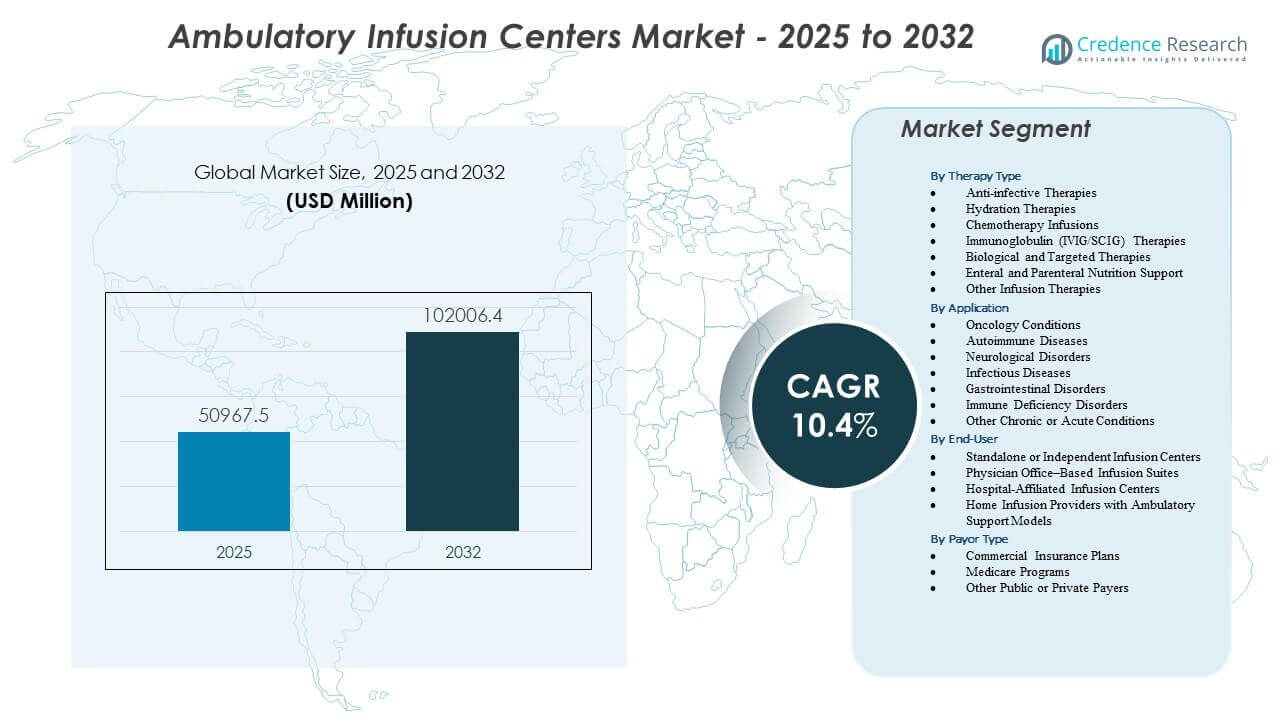

The Ambulatory Infusion Centers Market is projected to grow from USD 50,967.5 million in 2025 to an estimated USD 102,006.4 million by 2032, with a compound annual growth rate (CAGR) of 10.4% from 2025 to 2032. Growing demand for outpatient-based infusion services drives steady expansion across the Ambulatory Infusion Centers Market.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Ambulatory Infusion Centers Market Size 2025 |

USD 50,967.5 million |

| Ambulatory Infusion Centers Market, CAGR |

10.4% |

| Ambulatory Infusion Centers Market Size 2032 |

USD 102,006.4 million |

Ambulatory Infusion Centers Market Insights:

- Expanding use of biologics, immunoglobulin therapies, and chronic disease treatments strengthens patient flow into outpatient infusion centers, supported by flexible scheduling and lower care costs.

- Operational challenges such as workforce shortages, complex reimbursement rules, and high therapy management requirements continue to limit service scaling across several regions.

- North America leads the market due to strong infrastructure and payer alignment, while Europe maintains growth through structured day-care infusion pathways for chronic conditions.

- Asia Pacific emerges as the fastest-growing region, driven by expanding private healthcare systems and broader adoption of specialty therapies within outpatient infusion models.

Ambulatory Infusion Centers Market Drivers

Rising Shift Toward Cost-Efficient Outpatient Infusion Delivery

Healthcare systems move infusion therapy from hospital settings to outpatient centers to reduce overall costs and improve patient flow. This shift strengthens the Ambulatory Infusion Centers Market and supports wider adoption of chronic care management plans. Providers use outpatient centers to ease pressure on inpatient units and redirect routine therapies to controlled, low-cost environments. Patients prefer these centers for shorter wait times and flexible scheduling. Payers support this transition due to lower reimbursement burdens. It benefits from strong demand for biologic therapies that require recurring sessions. Growing insurance participation strengthens patient access. Expanding provider networks raise service availability in many regions.

- For instance, Option Care Health reported delivering more than 3 million annual infusion treatments across its national outpatient network, demonstrating the scale of shifting infusion care to ambulatory sites.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Increasing Burden of Chronic and Autoimmune Diseases

Growing cases of autoimmune, neurological, and metabolic disorders create high demand for long-term infusion support. The Ambulatory Infusion Centers Market benefits from the need for scheduled biologic and specialty drug administration. Patients seek centers that maintain safety standards while offering predictable treatment cycles. Healthcare teams rely on these centers to manage complex conditions with consistent oversight. Rising awareness of biologic effectiveness improves therapy uptake. It gains support from better diagnostic coverage and earlier treatment initiation. Demand grows in both urban and semi-urban settings. Strong clinical protocols make these centers preferred channels for disease-modifying therapies.

- For instance, Accredo (Cigna Group) reports supporting over 30,000 patients on specialty infusion therapies annually, reflecting nationwide growth in biologic and autoimmune-related infusion needs.

Advancements in Infusion Devices and Therapy Management

New infusion pumps, remote monitoring tools, and automated drug management systems improve safety and workflow efficiency. Providers use advanced equipment to minimize errors and enhance patient comfort. The Ambulatory Infusion Centers Market benefits from device upgrades that support long infusion durations with greater stability. It helps teams monitor therapy response more accurately. Improved drug compatibility expands the range of treatments these centers can deliver. Automation reduces manual steps during dosing and documentation. Enhanced chair-side tools support better patient experiences. Wider adoption of digital workflows improves operational consistency.

Growing Preference for Convenient and Patient-Centric Care Models

Patients prefer outpatient infusion care for its convenience and predictable scheduling. The Ambulatory Infusion Centers Market grows as flexible appointment models replace rigid hospital timelines. It offers streamlined registration, shorter waiting periods, and more comfortable treatment environments. Providers design centers around patient needs to improve adherence. Demand rises among working adults who seek reliable care without hospital visits. Improved staff-to-patient ratios strengthen clinical attention. Insurance coverage expands access for repeat therapies. Growth in chronic disease populations amplifies the need for these patient-friendly settings.

Ambulatory Infusion Centers Market Trends

Expansion of Specialty Drug Administration in Outpatient Settings

Specialty drugs require structured supervision, and outpatient centers expand capacity to meet rising needs. The Ambulatory Infusion Centers Market reflects this growth through broadened clinical protocols. It supports administration of oncology, neurology, and immunology therapies. Providers integrate advanced drug handling workflows to improve treatment accuracy. Training programs expand to support staff competency. Centers invest in controlled environments to handle sensitive biologics. Growth in specialty pharmacies strengthens referral patterns. Collaboration between drug manufacturers and outpatient networks increases access.

Integration of Digital Tools for Workflow and Patient Management

Digital platforms improve scheduling, dosing oversight, and patient tracking. Outpatient centers adopt tools that streamline administrative tasks and reduce delays. The Ambulatory Infusion Centers Market gains value from integrated EMR systems that support quick clinical decisions. It benefits providers who adopt automated reminders and remote check-ins. Digital dashboards help teams manage high-volume infusion traffic. Clinical documentation improves with structured digital inputs. Real-time communication tools enhance coordination. Rising data visibility supports more efficient care planning.

- For instance, Epic Systems is installed in over 305 health systems across the U.S., with more than 250 million patients having active EMR records, making it one of the most widely used clinical platforms supporting outpatient infusion workflows.

Rising Expansion of Independent Infusion Center Chains

Independent operators expand nationwide to address rising patient demand. These centers offer flexible appointments and high service availability. The Ambulatory Infusion Centers Market experiences strong competition as chains invest in new locations. It motivates providers to improve clinical consistency and patient experiences. Investors see outpatient infusion care as a scalable growth model. Expansion strategies focus on underserved suburban and semi-urban regions. Contract opportunities strengthen ties with specialty clinics. Multi-site models enable standardized service delivery.

- For instance, Vivo Infusion expanded to nearly 80 ambulatory infusion centers across 15 states following its acquisition of Infusion Associates, marking one of the largest independent operator footprints in the U.S.

Growing Collaboration Between Payers and Outpatient Infusion Providers

Payers promote outpatient infusion care due to its lower cost profile. Partnerships between insurers and infusion centers expand patient access. The Ambulatory Infusion Centers Market benefits from structured reimbursement agreements. It encourages patients to shift from hospital outpatient departments to freestanding centers. Contracting supports predictable treatment costs. Providers align their care pathways with payer guidelines to maintain coverage. Collaboration supports better chronic care continuity. Data-sharing agreements help improve patient outcomes.

Ambulatory Infusion Centers Market Challenges Analysis

Complex Reimbursement Landscape and Cost Pressures

Reimbursement rules vary across regions and create uncertainty for providers. The Ambulatory Infusion Centers Market faces challenges when insurers adjust coverage criteria. It deals with delays in claims approval that affect financial stability. Providers must navigate variations in reimbursement between biologics and specialty drugs. Rising operational costs pressure profit margins for independent centers. Staff training and equipment upgrades require steady investment. Limited coverage for new therapies restricts patient access. Regulatory differences across states increase administrative complexity. Slow reimbursement cycles strain cash flow.

Shortage of Skilled Clinical Staff and Compliance Requirements

Trained infusion nurses and technicians remain difficult to recruit in many regions. The Ambulatory Infusion Centers Market struggles to expand capacity without adequate staffing. It must maintain strict compliance with safety protocols. Complex drugs demand precise handling skills. Providers face challenges when adapting workflows to evolving regulations. Training needs require continuous investment. Staff burnout increases turnover risks. Compliance audits create heavy operational workload. Maintaining consistent quality across multiple sites becomes difficult.

Ambulatory Infusion Centers Market Opportunities

Expansion of Services Into Emerging Disease Areas and Advanced Therapies

Growing pipelines in oncology, rare diseases, and autoimmune disorders create new service opportunities. The Ambulatory Infusion Centers Market benefits from centers that diversify therapy portfolios. It can broaden treatment scope as more biologics and specialty drugs gain approval. Providers who invest in advanced handling capabilities position themselves for stronger growth. Demand rises for centers that specialize in rare disease infusion support. Partnerships with specialty clinics open new referral channels. Expansion into complex infusion types attracts higher patient volume. Training enhancement creates stronger operational capacity. Early adoption of new therapy areas builds competitive advantage.

Growth Potential in Underserved Regions and Technology-Enabled Models

Emerging markets present strong potential for outpatient infusion expansion. The Ambulatory Infusion Centers Market benefits from rising urbanization and growing private healthcare investment. It gains momentum when providers enter regions with limited inpatient infusion options. Digital care models support remote monitoring and ease patient management. Telehealth screening creates smoother workflows. Hybrid infusion models help patients transition safely between home and center care. Investment in mobile infusion units expands reach. Geographic expansion creates strong long-term growth pathways.

Ambulatory Infusion Centers Market Segmentation Analysis:

By Therapy Type

The Ambulatory Infusion Centers Market shows strong diversity across therapy types, driven by rising demand for complex outpatient care. Anti-infective and hydration therapies support routine treatment needs, while chemotherapy infusions strengthen high-acuity services. Immunoglobulin therapies create steady recurring volumes across chronic conditions. It benefits from biological and targeted therapies that require controlled administration and skilled monitoring. Enteral and parenteral nutrition broadens support for patients with nutritional deficiencies. Other infusion therapies extend service reach into pain, steroid, and supportive care segments. Wider therapy coverage enhances center utilization and patient retention.

- For instance, Fresenius Kabi reports producing over 1 billion IV infusion units annually across its global manufacturing network, demonstrating the scale of therapy demand supplied to outpatient and ambulatory centers.

By Application

Oncology remains one of the strongest applications in the Ambulatory Infusion Centers Market, supported by structured treatment cycles. Autoimmune diseases drive recurring demand due to long-term biologic therapy needs. It supports neurological and gastrointestinal disorders that require supervised infusions. Infectious diseases contribute consistent patient flow for short-term therapy sessions. Immune deficiency disorders rely on scheduled IVIG or SCIG administration. Other chronic or acute conditions expand the therapeutic footprint of outpatient centers. Broad clinical relevance strengthens steady multi-specialty adoption across regions.

By End-User

Standalone infusion centers lead due to flexible scheduling, specialized staffing, and strong patient preference. Physician office–based suites expand access for patients who prefer continuity within clinical practices. The Ambulatory Infusion Centers Market includes hospital-affiliated centers that manage complex or risk-sensitive infusions. Home infusion providers with ambulatory support improve convenience for stable patients. It gains value from diversified care settings that meet varied patient needs. End-user segmentation supports broader regional penetration. Distinct care models drive competitive differentiation across the market.

- For instance, HCA Healthcare reports delivering over 37 million outpatient visits annually across its national hospital network, a portion of which includes outpatient infusion services integrated into affiliated centers.

By Payor Type

Commercial insurance plans remain the primary reimbursement source in the Ambulatory Infusion Centers Market, supporting broad patient access. It benefits from policies that encourage outpatient infusion models over higher-cost hospital settings. Medicare programs contribute significant treatment volume through older adults with chronic conditions. Other public or private payers maintain demand across specialized therapies. Payor diversity stabilizes patient flow throughout the year. Clear reimbursement structures support operational planning. Consistent payer participation strengthens long-term market growth.

Segmentation:

By Therapy Type

- Anti-infective Therapies

- Hydration Therapies

- Chemotherapy Infusions

- Immunoglobulin (IVIG/SCIG) Therapies

- Biological and Targeted Therapies

- Enteral and Parenteral Nutrition Support

- Other Infusion Therapies

By Application

- Oncology Conditions

- Autoimmune Diseases

- Neurological Disorders

- Infectious Diseases

- Gastrointestinal Disorders

- Immune Deficiency Disorders

- Other Chronic or Acute Conditions

By End-User

- Standalone or Independent Infusion Centers

- Physician Office–Based Infusion Suites

- Hospital-Affiliated Infusion Centers

- Home Infusion Providers with Ambulatory Support Models

By Payor Type

- Commercial Insurance Plans

- Medicare Programs

- Other Public or Private Payers

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America holds the leading share of the Ambulatory Infusion Centers Market, accounting for an estimated 45% of the global landscape. Strong adoption of biologics, well-developed outpatient care infrastructure, and favorable reimbursement support continuous market expansion. It benefits from large independent infusion chains and expanding physician office infusion models. Oncology and autoimmune conditions drive recurring patient volume. Hospital-affiliated outpatient centers support complex therapies that require clinical oversight. Growing payer preference for cost-efficient infusion delivery strengthens long-term demand.

Europe follows with roughly 28% share, supported by structured day-care infusion models and steady integration of biologic therapies. It gains momentum from national healthcare systems that promote outpatient treatment pathways to reduce inpatient pressure. Adoption grows across oncology, neurology, and immune-related disorders. Independent centers expand in urban regions with high patient density. Hospital-linked infusion suites maintain strong roles in complex case management. Broader patient awareness improves acceptance of scheduled outpatient infusion care.

Asia Pacific emerges as the fastest-growing region with about 18% share of the Ambulatory Infusion Centers Market, driven by expanding private healthcare networks and rising chronic disease incidence. It benefits from large patient populations that require recurring biologic and IVIG therapies. Demand rises in India, China, and Southeast Asia as outpatient models replace traditional inpatient infusion settings. Physician office–based centers gain traction in metro areas. Hospital-affiliated infusion units support advanced treatments that require specialist oversight. Investment in skilled clinicians strengthens service capability across emerging markets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- InfuCare Rx

- KabaFusion

- Soleo Health

- Paragon Healthcare

- Amerita (a PharMerica company)

- United Infusion

- PromptCare

- Nufactor (FFF Enterprises)

- Option Care Health

- IVX Health

- Vital Care Infusion Services

- Accredo (Cigna Group)

- Healix Infusion Therapy

- Altus Infusion

Competitive Analysis:

The Ambulatory Infusion Centers Market features a competitive landscape defined by service differentiation, geographic expansion, and integration of specialty therapies. Large providers expand national footprints to increase patient reach and secure payer contracts. It pushes smaller regional operators to specialize in complex therapies or partner with physician practices. Independent infusion centers compete on convenience, short wait times, and personalized care models. Hospital-affiliated centers maintain an advantage in handling advanced or risk-sensitive treatments that require specialist oversight. Home-based infusion programs influence competition by attracting stable patients seeking flexible care. Technology investments in workflow automation, EMR integration, and remote monitoring strengthen operational efficiency. Payer alignment plays a significant role in shaping competitiveness, with reimbursement terms influencing provider expansion strategies.

Recent Developments:

- In November 2025, InfuCare Rx completed a recapitalization with Guggenheim Investments as a new strategic capital partner underscoring the company’s focus on scaling its specialty infusion services.

- In September 2025, Premier Infusion and Healthcare Services, Inc. entered a five-year group purchasing agreement with Premier, Inc., supporting expansion into the ambulatory infusion clinic market with an estimated annual contract spend exceeding $50 million. This collaboration enhances operational efficiency and access to high-quality infusion care.

- In July 2024, Vivo Infusion acquired Infusion Associates, an industry leader with centers in Michigan, Minnesota, Ohio, and Wisconsin. The acquisition expanded Vivo Infusion’s network to nearly 80 ambulatory infusion centers across 15 states.

Report Coverage:

The research report offers an in-depth analysis based on Therapy Type, Application, End-User, and Payor Type. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Expanding adoption of biologics will strengthen long-term demand across the Ambulatory Infusion Centers Market, driven by recurring therapy schedules.

- Growing preference for outpatient treatment will encourage rapid expansion of independent infusion networks.

- Rising chronic disease prevalence will push providers to scale capacity and diversify therapy portfolios.

- Wider payer support for cost-efficient outpatient infusion models will enhance patient access.

- Digital workflow tools and remote monitoring features will streamline clinical operations and improve treatment oversight.

- Strong physician–infusion center partnerships will increase patient referrals for complex therapies.

- Investment in skilled clinical staff will improve service quality and support advanced infusion protocols.

- Expansion into semi-urban regions will extend care availability beyond major metro centers.

- Growth in specialty pharmacy integration will improve continuity between drug dispensing and therapy delivery.

- Emerging markets will accelerate adoption as private healthcare networks build modern outpatient infusion infrastructure.