Arteriovenous Fistula Devices Market Overview:

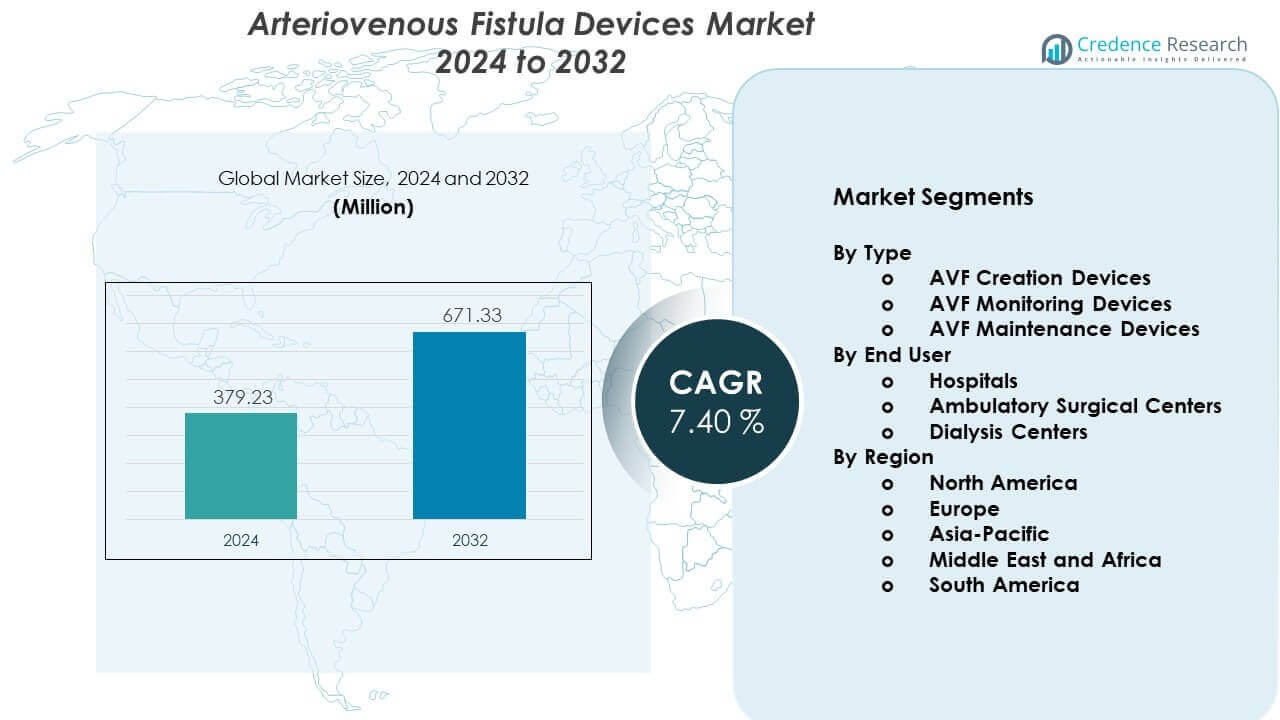

The Arteriovenous Fistula Devices Market is projected to grow from USD 379.23 million in 2024 to an estimated USD 671.33 million by 2032, with a CAGR of 7.40% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Arteriovenous Fistula Devices Market Size 2024 |

USD 379.23 million |

| Arteriovenous Fistula Devices Market, CAGR |

7.40% |

| Arteriovenous Fistula Devices Market Size 2032 |

USD 671.33 million |

Strong market drivers include the growing shift toward early fistula placement and rising awareness of long-term access outcomes in chronic kidney disease management. Manufacturers continue to enhance biocompatible graft materials and minimally invasive creation systems, allowing physicians to reduce complications and shorten recovery time. The increase in aging populations and the rise of comorbidities, including diabetes and hypertension, expand the candidate base. Continued clinical evidence supporting better patency and reduced intervention rates helps accelerate acceptance among nephrologists and vascular surgeons.

Regional demand varies, with North America leading due to advanced dialysis networks, strong reimbursement structures, and higher adoption of innovative vascular access technologies. Europe follows with steady uptake driven by established CKD management guidelines and improved training programs for vascular access teams. Asia Pacific emerges rapidly as India, China, and Southeast Asian nations invest in dialysis infrastructure and expand access to renal care. Growing awareness, rising CKD prevalence, and improved healthcare spending make the region a key future growth area.

Arteriovenous Fistula Devices Market Insights:

- The Arteriovenous Fistula Devices Market is valued at USD 379.23 million in 2024 and is expected to reach USD 671.33 million by 2032, registering a 40% CAGR driven by rising dialysis needs and improved access technologies.

- North America (40%), Europe (30%), and Asia-Pacific (24%) dominate due to strong renal care infrastructure, established clinical pathways, and large patient populations that support high device utilization.

- Asia-Pacific, holding 24%, is the fastest-growing region, supported by rapid CKD growth, expanding dialysis centers, and wider adoption of advanced access tools in emerging healthcare systems.

- The AVF Creation Devices segment accounts for the largest share at 45%, supported by strong clinical preference for early and durable access formation.

- Hospitals lead end-user adoption with 50% share due to high procedural volume, advanced imaging capability, and stronger integration of multidisciplinary access teams.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Arteriovenous Fistula Devices Market Drivers

Rising Need For Reliable Vascular Access In Growing Dialysis Population

The Arteriovenous Fistula Devices Market expands due to the rising number of patients who require long-term dialysis support. The chronic kidney disease burden grows fast across many regions due to diabetes and hypertension. Healthcare providers adopt advanced fistula creation tools to achieve better access durability for dialysis patients. It supports lower infection risk compared with catheters, which strengthens demand. Hospitals seek devices that allow faster healing and stable blood flow. Physicians prefer solutions that improve procedural precision during fistula creation. The market gains from greater awareness about early intervention. Governments strengthen renal care programs, which helps the adoption curve.

- For example, according to Medtronic, the Ellipsys® EndoAVF System demonstrated a functional patency rate of 92% at 90 days and reported an average procedure time of less than 30 minutes, highlighting a significant performance advantage over surgical options.

Growing Use Of Minimally Invasive Techniques In Access Creation Procedures

The adoption of minimally invasive fistula creation options pushes the Arteriovenous Fistula Devices Market forward. Surgeons choose systems that help limit tissue damage and reduce recovery time. It supports higher acceptance among elderly patients who need safer procedures. Device makers design tools that increase accuracy in vessel joining. The trend improves clinical outcomes and lowers revision needs. Hospitals invest in advanced technologies that streamline workflow. Faster discharge time increases patient turnover in high-volume centers. Training programs help professionals adopt new access creation methods.

Rapid Advancements In Biocompatible And High-Resilience Graft Materials

Material innovation creates strong momentum for the Arteriovenous Fistula Devices Market. Manufacturers enhance graft durability and resistance to repeated pressure cycles. It delivers better long-term patency for dialysis access. Biocompatible materials aim to reduce inflammatory response after placement. Vascular specialists trust devices that show lower complication risk. New graft structures support consistent blood flow under varied conditions. Hospitals prefer solutions that help reduce unplanned interventions. Research centers work to expand material performance testing to support regulatory approvals.

- For example, Gore’s PROPATEN® Heparin-Bonded Vascular Graft has demonstrated a 48% reduction in thrombotic occlusion events and maintains higher primary patency over 12 months compared with standard ePTFE grafts, supported by peer-reviewed clinical studies.

Increasing Preference For Early Fistula Placement In Renal Care Pathways

Clinical guidelines promote early fistula placement, supporting growth in the Arteriovenous Fistula Devices Market. Nephrologists adopt structured care pathways to start access planning sooner. It improves dialysis readiness and reduces catheter usage. Early planning reduces procedural delays in high-risk patients. Hospitals upgrade pre-operative imaging tools to improve access mapping. Care teams train staff to identify suitable vessels at earlier disease stages. Patients gain better outcomes when access is created before urgent dialysis. Health systems focus on reducing total treatment cost through better access management.

Arteriovenous Fistula Devices Market Trends

Growing Integration Of Imaging And Navigation Support During Access Creation

The Arteriovenous Fistula Devices Market experiences strong demand for imaging-guided procedures. Surgeons seek tools that improve accuracy during vessel selection. It helps reduce access failure rates. High-definition ultrasound and real-time mapping strengthen decision making. Hospitals invest in imaging platforms that support precise planning. Advanced navigation helps reduce repeated interventions. Training centers include imaging guidance in vascular access programs. Vendors expand compatibility between devices and imaging consoles.

- For instance, GE HealthCare’s LOGIQ E10 ultrasound platform delivers up to a 10× processing speed improvement with its cSound™ Architecture, enabling clearer visualization of small-caliber vessels critical to AVF planning and reducing preoperative mapping errors.

Rise Of Smart Monitoring Technologies For Fistula Function Assessment

The adoption of digital monitoring systems supports growth in the Arteriovenous Fistula Devices Market. Clinics use sensors to track flow changes in real time. It helps detect access dysfunction early. Remote monitoring tools support long-term management for dialysis patients. Hospitals prefer data-enabled solutions to reduce emergency interventions. Device makers integrate analytics features to support predictive insights. Patients gain better confidence through regular access performance updates. Providers use monitoring data to plan timely maintenance procedures.

- For instance, Crit-Line® technology from Fresenius Medical Care measures real-time hematocrit, blood volume changes, and oxygen saturation with accuracy exceeding 95%, enabling early detection of fistula flow issues during dialysis sessions.

Increasing Shift Toward Outpatient Settings For Fistula Creation

More care providers move fistula creation procedures to outpatient centers, influencing the Arteriovenous Fistula Devices Market. Ambulatory facilities deliver cost-efficient care for vascular access. It reduces hospital burden and improves patient convenience. Surgeons adopt devices that support faster discharge times. Workflow efficiency improves through compact access creation systems. Outpatient teams invest in advanced sterilization tools. Training efforts help broaden procedural capability in community settings. Industry players design solutions aimed at low-complexity environments.

Higher Use Of Customized Access Solutions For Complex Anatomy Cases

Demand for personalized access tools grows within the Arteriovenous Fistula Devices Market. Complex anatomy cases require tailored graft options. It improves outcomes for high-risk patients. Surgeons choose devices that adapt to vessel irregularities. Manufacturers create specialized designs for narrow or fragile veins. Hospitals focus on improving success rates in difficult scenarios. Clinical studies evaluate performance in diverse patient groups. Providers adopt patient-specific planning to reduce revision needs.

Arteriovenous Fistula Devices Market Challenges Analysis:

Limited Vessel Suitability And High Variation In Patient Anatomy

Challenges in vessel suitability continue to affect the Arteriovenous Fistula Devices Market. Many patients present with small or damaged vessels that complicate access creation. It raises procedural difficulty for surgeons. Failure rates increase when vessel quality is poor. Imaging helps, yet anatomical limitations persist. Elderly patients face higher risk due to fragile vessels. Hospitals must manage repeated interventions in difficult cases. Training programs aim to improve decision making for complex anatomies.

High Complication Rates And Limited Availability Of Skilled Access Teams

Complication management remains a major barrier in the Arteriovenous Fistula Devices Market. Access thrombosis and stenosis reduce long-term success. It drives repeated clinical visits and increases treatment cost. Skilled vascular access teams remain scarce in many regions. Hospitals struggle to maintain high procedural standards without trained specialists. Device makers work to design tools that reduce complication risk. Regulatory pathways require extensive data, which slows innovation adoption. Care centers invest in staff development to meet growing demand.

Arteriovenous Fistula Devices Market Opportunities:

Expansion Of Renal Care Infrastructure And Growing Focus On Early Diagnosis

Expanding renal care infrastructure creates strong openings in the Arteriovenous Fistula Devices Market. Many regions improve screening programs to detect chronic kidney disease sooner. It supports early planning for vascular access. Hospitals upgrade dialysis units, boosting device demand. Outreach programs educate patients about access options. Governments enhance funding for long-term renal therapy. Device firms enter new facilities through training support.

Rising Adoption Of Next-Generation Technologies For Access Longevity Enhancement

Next-generation tools create new pathways for growth in the Arteriovenous Fistula Devices Market. Advanced graft designs offer higher durability. It lowers revision frequency across dialysis patients. Smart monitoring expands preventive care capability. Clinics choose tools that support real-time data insights. Vendors explore partnerships with digital health firms to expand features. Hospitals aim to reduce complications through technology-driven care models.

Arteriovenous Fistula Devices Market Segmentation Analysis:

By Type

The Arteriovenous Fistula Devices Market shows strong growth across creation, monitoring, and maintenance devices due to rising demand for reliable vascular access. AVF creation devices hold a leading share because physicians prioritize durable and early access formation for dialysis patients. It supports better long-term outcomes and lowers dependence on catheters. AVF monitoring devices gain traction due to the rising focus on flow surveillance and early dysfunction detection. Clinics prefer tools that alert teams before access failure. AVF maintenance devices expand steadily due to the need for regular interventions to preserve patency. Hospitals and dialysis centers invest in solutions that improve workflow efficiency.

- For instance, BD’s WavelinQ™ 4F EndoAVF System uses radiofrequency energy to create a percutaneous AVF and has demonstrated technical success rates between 72% and 88% across multicenter clinical studies, with maturation typically achieved within 42 to 56 days.

By End User

Hospitals dominate due to high procedure volume, broad clinical expertise, and strong integration of imaging support. It strengthens demand for advanced creation and monitoring systems. Ambulatory surgical centers grow faster because many providers shift low-risk procedures to outpatient settings. These centers adopt compact devices that support quick turnaround and cost-effective care. Dialysis centers increase usage of monitoring and maintenance tools to manage long-term access performance. They rely on early alerts to reduce emergency interventions and improve patient stability. Growth across all end-user groups reflects the rising need for durable access throughout the dialysis pathway.

- For instance, Medtronic’s Ellipsys® Vascular Access System is widely adopted in Ambulatory Surgical Centers (ASCs), with published clinical studies reporting an average procedure time of 15 to 30 minutes for percutaneous fistula creation, supporting higher patient throughput compared with traditional open surgical AVF procedures

Segmentation:

By Type

- AVF Creation Devices

- AVF Monitoring Devices

- AVF Maintenance Devices

By End User

- Hospitals

- Ambulatory Surgical Centers

- Dialysis Centers

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America

North America holds the largest share of the Arteriovenous Fistula Devices Market, driven by advanced dialysis infrastructure and strong adoption of new vascular access technologies. The region accounts for 40% of the market due to high chronic kidney disease prevalence and established clinical guidelines. It benefits from early diagnosis programs that support timely fistula planning. Hospitals invest in imaging tools and maintenance systems to improve access durability. Leading manufacturers maintain strong distribution networks across the United States. Training programs for access teams support higher procedural success rates. Innovation uptake remains steady due to supportive reimbursement structures.

Europe

Europe represents the second-largest share, holding 30% of the global market. The region maintains strong demand for advanced creation and monitoring devices due to structured renal care pathways. The Arteriovenous Fistula Devices Market gains from national dialysis programs that promote early access formation. It supports higher adoption of biocompatible grafts and minimally invasive tools. Western Europe leads due to mature healthcare systems, while Eastern Europe shows growing need for affordable options. Collaboration between hospitals and industry players strengthens clinical training. Increased focus on reducing access complications encourages investment in surveillance technologies.

Asia-Pacific, Middle East & Africa, and South America

Asia-Pacific shows the fastest growth, holding 24% of the market due to rising CKD incidence and expanding dialysis capacity. It gains strong momentum from large patient pools in China and India. Middle East and Africa account for 3%, driven by new dialysis centers and steady investment in renal care modernization. South America holds 3%, supported by improved access to vascular procedures in Brazil and neighboring countries. The Arteriovenous Fistula Devices Market in these regions benefits from growing awareness of fistula durability and lower infection risk. It strengthens demand for cost-effective devices that meet the needs of diverse clinical environments. Expansion of private healthcare further supports long-term growth.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

Competitive Analysis:

The Arteriovenous Fistula Devices Market features strong competition driven by product innovation, material advancement, and expanding clinical applications. Leading companies strengthen portfolios with devices that improve access creation, monitoring, and long-term maintenance. It intensifies competition as firms enhance durability, biocompatibility, and ease of use. Key players focus on partnerships with hospitals to support training and improve procedural outcomes. Vendors expand distribution networks to reach high-growth regions. Digital monitoring tools create new differentiation points. Market leadership depends on strong regulatory approvals and consistent product upgrades.

Recent Developments:

- In February 2026, Medtronic announced its intent to exercise its option to acquire CathWorks, a deal valued at up to $585 million. While primarily focused on coronary artery disease diagnosis, this acquisition reinforces Medtronic’s broader strategy of integrating advanced imaging and computational tools into its vascular portfolio, complementing its existing AV access solutions like the IN.PACT™ AV drug-coated balloon, which recently demonstrated sustained long-term patency benefits in 60-month trial results released in May 2024.

- In February 2025, Fresenius Medical Care reported the successful acceleration of its FME25 transformation program, reaching €567 million in accumulated savings. As the world’s leading provider of renal products, the company is optimizing its portfolio by exiting non-core clinic operations while simultaneously increasing investments in Care Enablement, focusing on integrated dialysis technologies and digital monitoring tools that track the health and viability of patient fistulas.

Report Coverage:

The research report offers an in-depth analysis based on By Type and By End User. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Demand for advanced vascular access solutions will rise as more patients enter long-term dialysis programs and require stable, durable fistula options.

- Adoption of minimally invasive creation systems will expand due to faster recovery, reduced tissue trauma, and growing surgeon preference for precision-based access tools.

- Digital monitoring platforms will gain wider use as care teams focus on early identification of flow changes to prevent access failure and reduce emergency interventions.

- Outpatient vascular centers will perform a larger share of access procedures, driving demand for compact, efficient devices that support quick turnover and lower overall care costs.

- Innovation in graft materials will accelerate, with manufacturers developing designs that improve flexibility, reduce inflammation, and extend patency duration for high-risk patients.

- Training programs for vascular access teams will increase, helping providers manage complex anatomies and improve consistency in procedural outcomes across care settings.

- Integration of predictive analytics and AI-supported flow assessment will reshape surveillance practices, enabling clinicians to intervene before complications develop.

- Emerging regions will strengthen renal care infrastructure, leading to higher device adoption driven by rising CKD awareness and wider access to specialized treatment centers.

- Partnerships between device manufacturers and dialysis networks will deepen, supporting product testing, workflow optimization, and broader real-world adoption.

- Regulatory bodies will encourage innovations that improve patient safety, which will help streamline approval pathways and accelerate market entry for next-generation access technologies.