Battery Cell Market Overview:

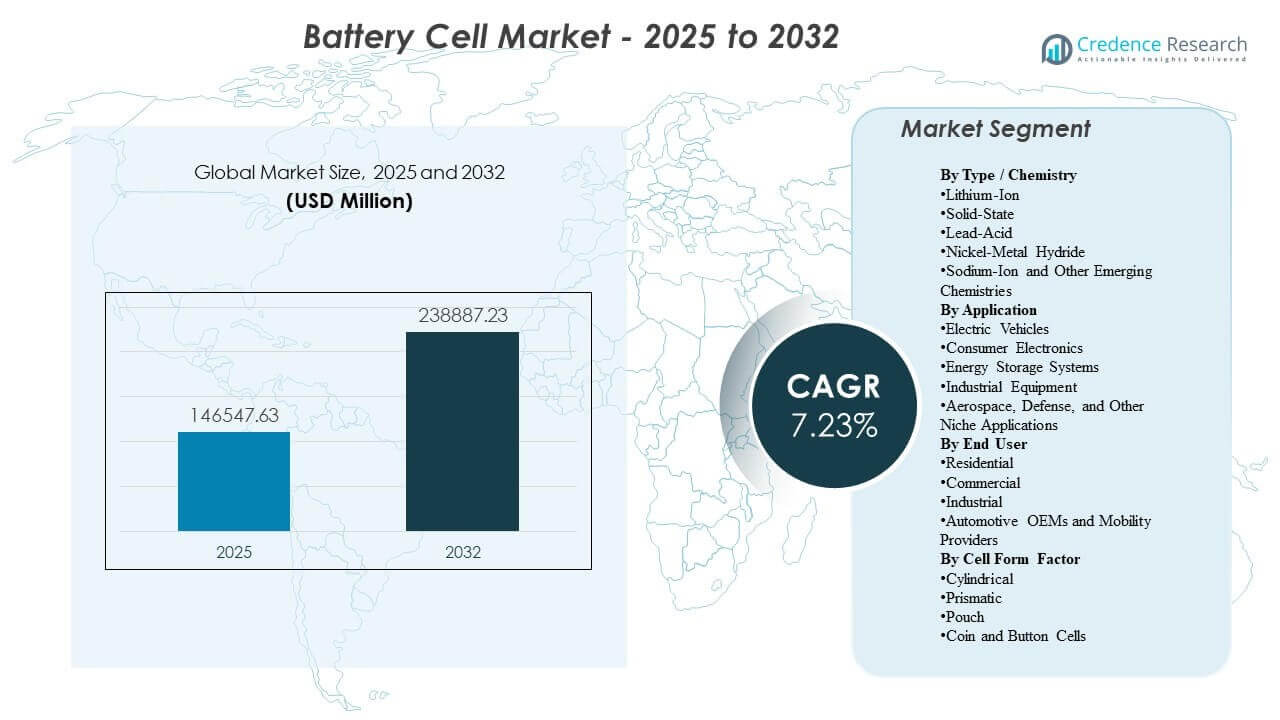

The global Battery Cell Market size was estimated at USD 146,547.63 million in 2025 and is expected to reach USD 238,887.23 million by 2032, growing at a CAGR of 7.23% from 2025 to 2032. Growth is primarily driven by accelerating electrification across mobility and the steady expansion of battery-backed power systems that require scalable, qualified cell supply. Asia Pacific continues to anchor both manufacturing concentration and demand intensity, supported by deep supplier ecosystems and large downstream consumption across multiple applications.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Battery Cell Market Size 2025 |

USD 146,547.63 million |

| Battery Cell Market, CAGR |

7.23% |

| Battery Cell Market Size 2032 |

USD 238,887.23 million |

Key Market Trends & Insights

- Asia Pacific accounted for an estimated 6% share in 2025, reflecting the region’s continued leadership in cell production scale and downstream demand concentration.

- Lithium-Ion held 67.2% share in 2024 by chemistry, supported by established supply chains, platform standardization, and broad adoption across mobility and storage use cases.

- Prismatic cells represented 38.9% share in 2020 by form factor, benefiting from packaging efficiency and widespread use in applications prioritizing space utilization.

- The market is projected to expand at a 23% CAGR (2025–2032) as cell demand rises across transport electrification, stationary storage, and industrial electrification pathways.

- Industry revenues are expected to reach USD 238,887.23 million by 2032, supported by rising capacity additions and long-term procurement programs from large downstream buyers.

Segment Analysis

Battery cell demand is increasingly shaped by two high-volume pull factors: electrified mobility and energy storage deployments. EV programs require multi-year supply stability, repeatable performance, and safety validation, which strengthens demand for mature chemistries and standardized production lines. At the same time, storage deployments are scaling across grid and behind-the-meter applications, widening demand for cost-optimized cells and manufacturing efficiency. This dual demand base is pushing suppliers to balance capacity allocation, diversify chemistry portfolios, and improve throughput and yield.

Across the supply chain, manufacturers are prioritizing design-to-cost, localized production footprints, and tighter integration with downstream system needs. Cell form factor choices are becoming more application-specific, with pack architecture, thermal constraints, and manufacturability influencing selection. While lithium-ion remains dominant, emerging chemistries are gaining visibility where cost, materials availability, and safety profiles can provide differentiation. Overall, supplier competitiveness is increasingly determined by qualification speed, cost control, and the ability to serve both automotive and stationary markets without compromising delivery reliability.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Type / Chemistry Insights

Lithium-Ion accounted for the largest share of 67.2% in 2024. It leads due to a mature global supply chain, high-volume manufacturing experience, and strong downstream standardization across major applications. Large-scale investments in production lines and quality systems continue to reinforce cost advantages and dependable availability. Emerging chemistries are progressing, but broader commercialization is still constrained by qualification timelines, supply readiness, and cost-performance trade-offs at scale.

By Application Insights

Demand is shaped by the mix of electrified mobility, consumer devices, and accelerating storage deployments across grid and distributed energy settings. Electric vehicles remain a key volume driver because platform-based procurement creates long, predictable supply cycles. Energy storage systems are expanding rapidly as utilities and commercial users add flexibility, peak management, and resilience. Industrial and niche applications remain smaller but create premium demand pockets where safety, cycle life, and mission reliability are prioritized.

By End User Insights

End-user dynamics reflect distinct purchasing behaviors and deployment economics across residential, commercial, industrial, and automotive buyers. Automotive OEMs and mobility providers typically influence the largest contracted volumes through long-term sourcing agreements and strict validation requirements. Commercial buyers are expanding storage adoption to manage energy costs and improve uptime, increasing demand for reliable cell supply and consistent performance. Residential and industrial demand contributes additional diversification, with adoption influenced by local incentives, installation economics, and operational continuity needs.

By Cell Form Factor Insights

Prismatic accounted for the largest share of 38.9% in 2020. It remains favored where packaging efficiency, space optimization, and pack-level integration matter, supporting broad usage in high-volume systems. Cylindrical formats maintain strength where standardized production and scalable manufacturing are prioritized. Pouch cells compete where weight and design flexibility are valued, though system integration approaches vary by application. Coin and button cells continue to serve compact device requirements where low-power, small-format solutions are needed.

Battery Cell Market Drivers

Electrification of mobility and expanding platform-based procurement

Automotive electrification is expanding across passenger vehicles, commercial fleets, and mobility services, creating sustained demand for qualified cell supply. OEM procurement structures favor long-term sourcing relationships, tightening the link between capacity planning and platform roadmaps. This supports stable volume pull-through and increases the importance of validated manufacturing quality. It also encourages suppliers to diversify product portfolios to serve multiple vehicle segments.

- For instance, LG Energy Solution achieved over 90% battery yield in just one month of mass production at its Ultium Cells Plant 2 in Tennessee. This supports stable volume pull-through and increases the importance of validated manufacturing quality.

Scale-up of energy storage deployments across grid and commercial use cases

Energy storage is being deployed to improve grid flexibility, integrate renewables, and enhance resilience for commercial and industrial users. These deployments create large order volumes that can absorb manufacturing scale, supporting cost downtrends. Storage buyers also value cycle life, safety, and predictable performance under varied operating conditions. This accelerates product optimization and pushes suppliers to expand beyond EV-focused strategies.

Manufacturing maturity and yield improvement in high-volume chemistries

Continuous improvement in process control, yield, and throughput supports cost reduction and supply reliability. Mature production ecosystems can deliver consistent quality at scale and shorten lead times for large contracts. As plants scale, manufacturers benefit from learning curves and tighter supplier integration. These advantages reinforce demand concentration around proven chemistries and scalable formats.

Strategic localization and supply-chain resilience initiatives

Capacity expansion decisions are increasingly influenced by supply security priorities and regional industrial strategies. Local production footprints reduce logistics risk and can improve customer responsiveness for large buyers. Localization also supports closer collaboration during product qualification and pack integration stages. These factors collectively strengthen investment cycles and long-term capacity planning.

- For instance, Samsung SDI is converting its Indiana facility lines to produce LFP batteries locally for a $1.36 billion U.S. ESS order starting 2027. Localization also supports closer collaboration during product qualification and pack integration stages.

Battery Cell Market Challenges

Battery cell markets face volatility across raw material pricing, supply availability, and shifting demand signals across EV and storage segments. Such variability can compress margins and complicate long-term contracting, particularly when cost changes are rapid. Qualification cycles are also resource-intensive, requiring extended testing, safety validation, and consistent production stability before adoption at scale. These constraints can slow commercialization for newer chemistries and limit rapid product switching.

- For instance, spot prices for lithium carbonate swung from around 70,000 to nearly 11,000 per tonne within about one year, forcing cell makers and cathode suppliers to renegotiate procurement formulas and compressing upstream gross margins by an estimated 4–10% as pricing moved from previous‑month to same‑month indexation.

Additionally, intensifying competition increases pressure on pricing, delivery performance, and technology differentiation. Manufacturers must balance expansion speed with quality consistency, since reliability issues can trigger costly warranty exposure and reputational risk. Policy changes and trade measures can also alter market access and shift where capacity is economically viable. As a result, strategic flexibility and disciplined execution are critical for sustainable performance.

Battery Cell Market Trends and Opportunities

Product strategies are increasingly converging on chemistry diversification and application-specific optimization, especially as suppliers serve both mobility and stationary storage demand. This creates opportunities for portfolio rationalization, modular platform design, and faster customization across customer requirements. Manufacturers that improve design-to-cost and simplify pack integration requirements can expand addressable demand across more price-sensitive deployments. Emerging chemistries can open additional pathways where material availability, safety characteristics, or cost structures provide differentiation.

- For instance, BYD’s Blade LFP platform now reaches around 166–168 Wh/kg at the cell level while its next generation targets about 190 Wh/kg, enabling the same pack architecture to be tuned separately for high-range passenger EVs and high-cycle stationary storage without changing the core manufacturing footprint.

Another opportunity is the expansion of localized supply partnerships with downstream integrators and large-scale buyers. Co-development models can reduce qualification friction, accelerate ramp schedules, and improve performance alignment at the system level. Service-led offerings, including performance assurance, lifecycle analytics, and recycling-aligned procurement, also support differentiation beyond cell pricing. Collectively, these trends create multiple value pools beyond pure volume growth.

Regional Insights

North America

North America is supported by rising demand from electrified mobility and accelerating energy storage deployments across utilities and commercial users. Localization strategies are increasingly important as buyers seek supply resilience and tighter integration with downstream manufacturing. The region accounted for an estimated 18.9% share in 2025, reflecting strong demand growth despite a smaller manufacturing concentration than Asia Pacific. Supplier competitiveness is influenced by qualification readiness, reliable delivery, and the ability to meet customer performance standards at scale.

Europe

Europe continues to be a major demand center tied to automotive manufacturing, electrification targets, and expanding stationary storage installations. The market benefits from strong downstream pull and a growing focus on resilient supply chains and quality compliance. Europe represented an estimated 22.1% share in 2025, supported by sustained EV penetration and industrial applications. Growth is increasingly shaped by partnerships, local capacity planning, and application-driven portfolio strategies.

Asia Pacific

Asia Pacific anchors global battery cell activity through its deep manufacturing base, broad supplier ecosystems, and strong downstream consumption. High-volume production capabilities and supply-chain integration support competitive cost structures and rapid scaling. The region accounted for an estimated 51.6% share in 2025, maintaining clear leadership across both production and demand. Ongoing investment cycles and technology iteration continue to reinforce Asia Pacific’s central role in global cell markets.

Latin America

Latin America remains an emerging region for large-scale battery cell demand, with growth linked to storage deployments, industrial electrification, and selective mobility adoption. While the region’s manufacturing footprint is comparatively limited, downstream projects are increasing in scale and sophistication. Latin America held an estimated 4.1% share in 2025, reflecting smaller installed bases but improving project pipelines. Market expansion is supported by energy reliability needs and gradual infrastructure modernization.

Middle East & Africa

Middle East & Africa demand is developing around grid upgrades, resilience requirements, and large infrastructure projects that can incorporate storage solutions. Adoption remains selective but is increasing as renewables integration and reliability priorities gain traction. The region accounted for an estimated 3.3% share in 2025, indicating a smaller base with meaningful long-term growth potential. Partnerships, financing models, and project execution capability remain key to near-term scaling.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Competitive Landscape

Competition is defined by scale economics, qualification credibility, and the ability to deliver stable performance across high-volume applications. Leading suppliers invest in manufacturing efficiency, chemistry roadmaps, and customer integration to win long-term programs. Differentiation is increasingly driven by cost control, safety validation, and tailored product portfolios aligned with EV and storage requirements. As capacity expands, suppliers also focus on strengthening supply resilience and improving throughput and yield to protect margins.

CATL (Contemporary Amperex Technology Co., Limited) continues to represent a leading example of scale-led competitiveness through broad chemistry development and deep customer relationships. The company’s strategy reflects ongoing investment in product roadmaps and manufacturing execution to maintain leadership across high-demand application areas. Its approach emphasizes platform readiness, reliable delivery, and accelerated commercialization of next-generation pathways where feasible. This positioning supports strong relevance across both mobility and energy storage demand centers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- CATL (Contemporary Amperex Technology Co., Limited)

- BYD Co., Ltd.

- LG Energy Solution

- Panasonic Energy

- Samsung SDI

- SK On

- CALB (China Aviation Lithium Battery)

- Gotion High-Tech

- EVE Energy

- AESC (Envision AESC)

- GS Yuasa Corporation

- EnerSys

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments

- In February 2026, Lyten announced that it had completed the acquisition of Northvolt Ett, Ett Expansion, and Northvolt Labs in Sweden, gaining around 16 GWh of existing battery manufacturing capacity and associated industrial assets to support future lithium‑sulfur and lithium‑ion cell production for energy storage and other applications.

- In January 2026, Luminous Power Technologies inaugurated its first lithium‑ion battery assembly line at its Baddi facility in Himachal Pradesh, India, establishing a 500 MWh plant that uses advanced robotic automation to manufacture high‑performance battery packs and strengthen its position in the battery cell and energy storage market.

- In January 2026, ProLogium partnered with Darfon Energy Tech to launch new solid‑state battery solutions at CES 2026 in Las Vegas, combining ProLogium’s solid‑state cell technology with Darfon’s system integration capabilities to target next‑generation EV and energy storage applications.

- In November 2025, Beijing HyperStrong Technology and Contemporary Amperex Technology Co., Limited (CATL) signed a ten‑year strategic cooperation agreement under which HyperStrong will procure no less than 200 GWh of battery cells from CATL between January 1, 2026 and December 31, 2028, forming the basis for HyperStrong’s large‑scale global energy storage deployments.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 146,547.63 million |

| Revenue forecast in 2032 |

USD 238,887.23 million |

| Growth rate (CAGR) |

7.23% |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Type / Chemistry Outlook: Lithium-Ion, Solid-State, Lead-Acid, Nickel-Metal Hydride, Sodium-Ion and Other Emerging Chemistries; By Application Outlook: Electric Vehicles, Consumer Electronics, Energy Storage Systems, Industrial Equipment, Aerospace, Defense, and Other Niche Applications; By End User Outlook: Residential, Commercial, Industrial, Automotive OEMs and Mobility Providers; By Cell Form Factor Outlook: Cylindrical, Prismatic, Pouch, Coin and Button |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

CATL (Contemporary Amperex Technology Co., Limited), BYD Co., Ltd., LG Energy Solution, Panasonic Energy, Samsung SDI, SK On, CALB (China Aviation Lithium Battery), Gotion High-Tech, EVE Energy, AESC (Envision AESC), GS Yuasa Corporation, EnerSys |

| No. of Pages |

335 |

Segmentation

By Type / Chemistry

- Lithium-Ion

- Solid-State

- Lead-Acid

- Nickel-Metal Hydride

- Sodium-Ion and Other Emerging Chemistries

By Application

- Electric Vehicles

- Consumer Electronics

- Energy Storage Systems

- Industrial Equipment

- Aerospace, Defense, and Other Niche Applications

By End User

- Residential

- Commercial

- Industrial

- Automotive OEMs and Mobility Providers

By Cell Form Factor

- Cylindrical

- Prismatic

- Pouch

- Coin and Button

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa