Bovine Pericardial Valve Market

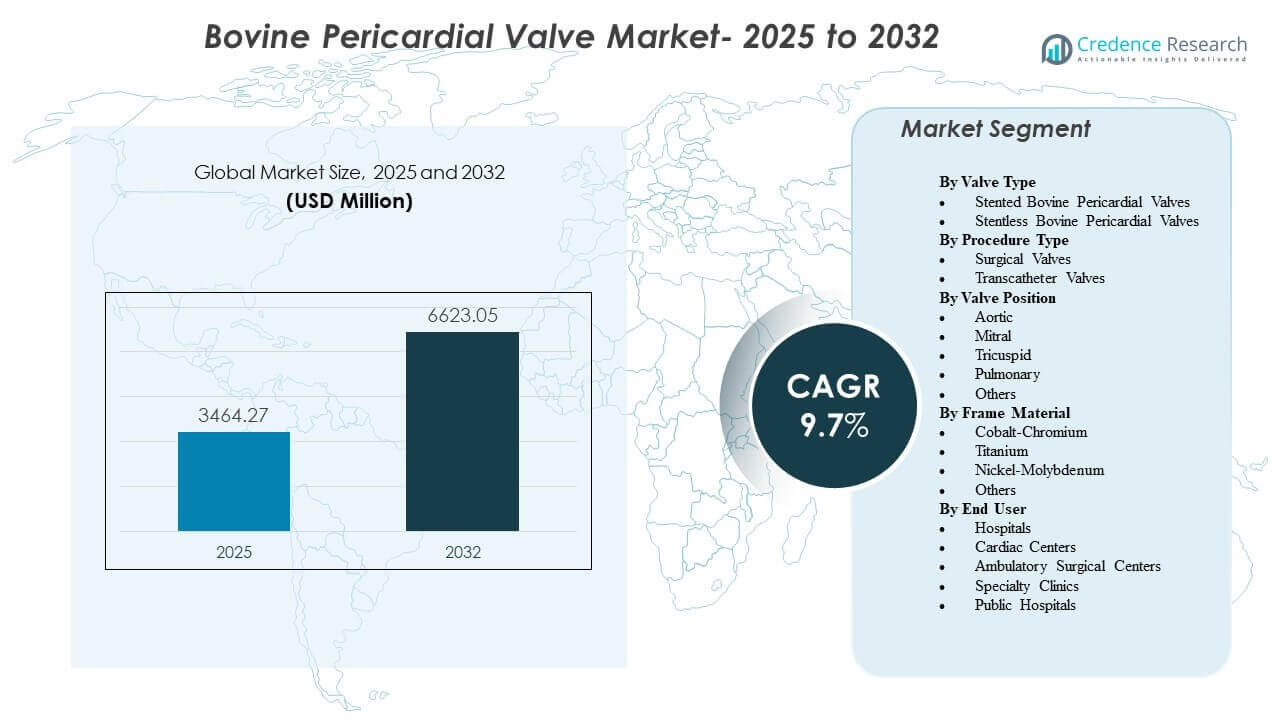

The global Bovine Pericardial Valve Market size was estimated at USD 3464.27 million in 2025 and is expected to reach USD 6623.05 million by 2032, growing at a CAGR of 9.7% from 2025 to 2032. Demand is being shaped by rising structural heart procedure volumes and a continued shift toward bioprosthetic valve replacement in patients where long-term anticoagulation avoidance is clinically preferred. Adoption is also supported by procedural standardization across heart teams, improving peri-procedural management, and broader availability of surgical and catheter-delivered platforms across mature and emerging healthcare systems.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Buccal Cavity Devices Market Size 2025 |

USD 2,795.05 million |

| Buccal Cavity Devices Market, CAGR |

6.8% |

| Buccal Cavity Devices Market Size 2032 |

USD 4,429.85 million |

Key Market Trends & Insights

- The global Bovine Pericardial Valve Market is projected to expand from USD 3464.27 million in 2025 to USD 6623.05 million by 2032, reflecting a 9.7% CAGR over 2025–2032.

- Stented bovine pericardial valves accounted for the largest share of 68.9% in 2025, reflecting continued preference for predictable sizing and streamlined implantation workflows.

- Surgical valves held 55.2% share in 2025, indicating that open procedures remain a core volume driver despite accelerating transcatheter adoption.

- Aortic position represented 71.0% share in 2025, supported by higher disease prevalence and established care pathways for aortic stenosis management.

- North America contributed 39.6% of 2025 revenue, with Europe at 25.4% and Asia Pacific at 23.7%, highlighting concentration in high-procedure, high-spend systems with rapid growth in Asia.

Segment Analysis

Bovine pericardial valves are increasingly selected where clinicians prioritize bioprosthetic performance, operational familiarity, and scalable implantation workflows across surgical and catheter-based pathways. Decision-making is influenced by anatomy, lifetime management considerations (including reintervention planning), and site-of-care capabilities, which together shape adoption across valve types, positions, and frame materials. Purchasing dynamics also reflect institutional preferences for platforms supported by robust clinical evidence, predictable sizing, and stable supply availability.

Technology progress is most visible in delivery systems, frame engineering, and tissue handling strategies that aim to improve deployability, sealing, and follow-up outcomes. At the provider level, standardization of procedural protocols supports broader access and throughput, and it encourages adoption beyond tertiary centers as training and infrastructure expand. Across geographies, market expansion is supported by increasing diagnosis and referral for structural heart disease, rising procedural capacity, and widening access to specialty cardiac care.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Valve Type Insights

Stented Bovine Pericardial Valves accounted for the largest share of 68.9% in 2025. Stented designs remain preferred in routine clinical pathways due to predictable anchoring behavior and sizing consistency across a wide range of anatomies. Higher procedural familiarity and established inventory practices also support adoption in high-volume centers. Stented platforms typically align well with standardized peri-procedural workflows and enable faster learning curves for expanding programs.

Procedure Type Insights

Surgical Valves accounted for the largest share of 55.2% in 2025. Surgical implantation continues to lead because a meaningful portion of patients require open procedures due to anatomy, concomitant cardiac interventions, or clinical suitability. Surgical pathways also benefit from entrenched hospital infrastructure and established referral networks. At the same time, procedural planning and lifetime management considerations keep surgical valve selection relevant even as transcatheter volumes expand.

Valve Position Insights

Aortic accounted for the largest share of 71.0% in 2025. Aortic valve disease contributes a large procedural pool, supported by mature screening and referral pathways and standardized treatment algorithms. Platform availability across both surgical and transcatheter approaches further reinforces aortic dominance. Compared with other positions, aortic replacement benefits from broader clinician familiarity, streamlined imaging criteria, and well-established clinical protocols.

Frame Material Insights

Cobalt-Chromium accounted for the largest share of 43.1% in 2025. Cobalt-chrome remains widely used due to proven structural characteristics, established manufacturing maturity, and broad incorporation across legacy and current valve platforms. Procurement preferences also favor materials with long-standing performance histories and stable supply chains. Frame engineering remains a key differentiator, and alloy selection is increasingly paired with design features intended to support sealing, deliverability, and long-term valve performance.

End User Insights

Hospitals accounted for the largest share of 82.4% in 2025. Hospitals remain the primary setting because they concentrate the heart-team model, imaging resources, intensive care capacity, and multidisciplinary support needed for complex valve replacement. Hospitals also handle higher-acuity patients and combined procedures that require broader peri-operative infrastructure. While specialized cardiac centers are expanding capacity, hospitals continue to dominate procurement due to centralized budgets, standardized formularies, and higher procedural throughput.

Bovine Pericardial Valve Market Drivers

Expanding structural heart procedure volumes and aging demographics

Rising prevalence of degenerative valvular disease supports sustained growth in bovine pericardial valve demand. As screening improves and referral pathways mature, more patients enter definitive valve replacement programs. Broader procedural capacity across cardiac surgery and interventional cardiology teams increases addressable volumes. Institutional focus on throughput and clinical outcomes reinforces procurement of platforms that support standardized implantation and consistent performance.

Clinical preference for bioprosthetic pathways in suitable patients

Bioprosthetic valves remain clinically attractive where long-term anticoagulation avoidance is important and where quality-of-life considerations influence therapy choice. Practice patterns increasingly align with evidence-led selection based on anatomy, age, and lifetime management strategy. Provider familiarity with pericardial tissue behavior supports continued adoption across routine aortic workflows. Device selection is also guided by platform maturity, evidence depth, and post-procedure management expectations.

- For instance, Edwards reported eight-year data for its RESILIA tissue platform in a 947-patient study showing 99.3% freedom from structural valve deterioration and 99.2% freedom from reoperation due to structural valve deterioration, compared with 90.5% and 93.9%, respectively, for non-RESILIA bioprosthetic valves

Technology progress in delivery systems and implant performance optimization

Advances in delivery catheters, deployment control, and frame design support improved procedural efficiency and broaden adoption across center types. Platform refinement targets sealing, positioning accuracy, and hemodynamic performance, which strengthens physician confidence. Standardized procedural protocols support the scaling of programs across geographies and hospital networks. As technology improves, replacement decisions increasingly consider lifetime management, including potential reintervention strategies.

- For instance, Abbott’s Navitor TAVI system reported 0.0% moderate or severe paravalvular leak at 30 days, with 79.8% of patients showing none or trace leak, 20.2% showing mild leak, 1.9% all-cause mortality, and 1.9% disabling stroke, underscoring how sealing and delivery refinements are translating into more predictable implant performance.

Geographic expansion of cardiac care infrastructure and access

Healthcare systems are expanding structural heart programs through investments in cath labs, imaging, and specialist training. Emerging markets are developing procedure capacity through center-of-excellence models and broader cardiology coverage. Expanding access supports increased diagnosis-to-treatment conversion, driving incremental valve volumes. Public and private providers also strengthen procurement capabilities as procedure pathways become more standardized and predictable.

Bovine Pericardial Valve Market Challenges

Pricing pressure and reimbursement variability can constrain adoption, particularly where procedure funding is limited or approval pathways are inconsistent across payers and regions. Hospitals and procurement bodies increasingly demand value-based justification, which can compress margins and intensify tender competition among suppliers. In parallel, platform selection requires careful alignment with institutional capabilities, including imaging, specialist teams, and post-procedure monitoring infrastructure. These constraints can delay program expansion and limit uptake in lower-resource settings.

Clinical complexity and patient heterogeneity also remain practical challenges, as outcomes depend on careful patient selection, imaging accuracy, and procedural experience. Complications management and long-term performance expectations influence purchasing behavior and may slow switching between platforms. Training, credentialing, and maintaining procedural volumes are essential for consistent outcomes, which can be difficult for smaller centers. Supply continuity for specialized components and sizes can further affect standardization and inventory planning.

- For instance, Medtronic reported in its Evolut Low Risk Trial that the Evolut TAVR system delivered a 5.3% rate of all-cause mortality or disabling stroke at 2 years and a 0.8% disabling stroke rate at 30 days, but centers must still manage multiple valve sizes, including 23 mm, 26 mm, 29 mm, and 34 mm options covering annulus ranges from about 18 mm to 30 mm, which adds complexity to sizing, training, and inventory planning.

Bovine Pericardial Valve Market Trends and Opportunities

Adoption is increasingly shaped by the expansion of transcatheter programs and the push toward lower-acuity care pathways where clinically appropriate. Procedural standardization, simplified anesthesia protocols, and refined imaging planning support broader program scalability and improved throughput. These shifts create opportunities for suppliers that can support training, service reliability, and consistent availability across sizes and configurations. Platforms that demonstrate procedural efficiency and predictable outcomes are positioned to benefit as programs scale.

- For instance, Edwards reported that in an analysis of more than 9,000 propensity-matched patients from the STS/ACC TVT Registry, its SAPIEN 3 Ultra RESILIA valve showed no paravalvular leak in 84.4% of cases, a one-day hospital stay, a 31-point average improvement in KCCQ score, and 93% discharge-to-home, highlighting the type of recovery and throughput profile that can help high-volume TAVR programs scale efficiently.

Product differentiation is also moving beyond core implant performance toward lifetime management, follow-up imaging compatibility, and reintervention planning. Frame material and design choices are increasingly linked to deployment behavior, sealing performance, and post-procedural monitoring practices. Suppliers that align device engineering with hospital workflow efficiency and evidence generation can gain share in tender-based environments. Expanding access in Asia Pacific and selected emerging markets also creates opportunities for localized commercialization models and broader distribution partnerships.

Regional Insights

North America

North America represented 39.6% of 2025 revenue, supported by high procedure volumes, mature reimbursement pathways, and broad availability of both surgical and transcatheter programs. Market demand is reinforced by structured referral networks and concentration of specialized centers capable of complex structural heart interventions. Procurement decisions often emphasize clinical evidence depth, platform reliability, and service support for consistent outcomes. Innovation adoption tends to be rapid where clinical protocols and hospital infrastructure support scaling.

Europe

Europe accounted for 25.4% of 2025 revenue, reflecting strong procedural penetration across major countries and consistent adoption of standardized valve replacement pathways. Many systems maintain structured purchasing processes that favor proven performance and predictable supply. Clinical adoption is reinforced by established cardiology networks and high utilization of structured heart-team approaches. Competitive dynamics are shaped by tendering and evidence-based differentiation.

Asia Pacific

Asia Pacific contributed 23.7% of 2025 revenue and continues to expand due to increasing access to specialized cardiac care and rising diagnosis rates for valvular disease. Program build-outs across large population markets support higher procedure capacity over time. Adoption is influenced by hospital investment in cath lab infrastructure, specialist training, and the development of high-throughput care pathways. Suppliers benefit from commercialization strategies aligned to local procurement structures and scalable service models.

Latin America

Latin America held 6.4% of 2025 revenue, with demand concentrated in larger healthcare markets and urban specialty centers. Adoption is shaped by reimbursement variability and uneven access to advanced structural heart programs. Procurement emphasis often balances clinical performance requirements against affordability and supply continuity. Growth is supported by gradual expansion of specialty cardiac capacity and increasing availability of trained clinicians.

Middle East & Africa

Middle East & Africa represented 4.9% of 2025 revenue, driven by pockets of advanced care capacity in select countries and private healthcare hubs. Access remains uneven across the region, and procedure volumes are typically concentrated in top-tier facilities. Adoption depends on specialist availability, funding pathways, and infrastructure for imaging and peri-procedural support. Opportunities exist where center-of-excellence models and public-private investments expand structural heart programs.

Competitive Landscape

The Bovine Pericardial Valve Market is characterized by active competition across surgical and transcatheter platforms, with vendors differentiating on clinical evidence strength, procedural workflow efficiency, delivery system refinement, and portfolio breadth across valve sizes and indications. Market participants also compete on lifetime management positioning, service support, and training capabilities that help hospitals scale procedural throughput. Tender participation, long-term supply reliability, and post-implant follow-up frameworks increasingly influence purchasing decisions. Competitive intensity is elevated where provider networks prioritize standardized platforms across multi-hospital systems.

Abbott Laboratories maintains a structural heart focus through platform development and geographic expansion strategies aligned to transcatheter valve replacement adoption. Abbott Laboratories typically emphasizes workflow-aligned delivery improvements, portfolio positioning across patient risk categories, and commercialization in growth markets as program capacity expands. Abbott Laboratories also benefits when hospitals seek vendor support for training, procedural standardization, and dependable availability across valve configurations. Competitive progress is reinforced through continued refinement of device performance, procedural efficiency, and clinician familiarity.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbottL aboratories

- Artivion, Inc.

- Boston Scientific Corporation

- Braile Biomedica

- Colibri Heart Valve

- Edwards Lifesciences Corporation

- Labcor Laboratórios Ltda.

- LivaNova PLC

- Medtronic plc

- Meril Life Sciences Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In July 2025, Abbott Laboratories said sales of its Navitor transcatheter aortic valve replacement implant had doubled over the prior two years and disclosed that first-in-human procedures had already been completed for a new balloon-expandable TAVR implant, marking a recent structural-heart pipeline update rather than a disclosed acquisition or partnership.

- In April 2025, Braile Biomedica entered a global licensing and commercialization partnership with Zydus MedTech for its TAVI technology across India, Europe, and other selected markets, and the reported valve design uses a single bovine pericardium sheet rather than three separate leaflets.

- In May 2024, Edwards Lifesciences announced the European launch of the SAPIEN 3 Ultra RESILIA valve, which it described as the only transcatheter aortic heart valve using RESILIA tissue at launch in Europe. Edwards states that RESILIA is bovine pericardial tissue treated with advanced anti-calcification technology intended to help extend valve durability.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 3464.27 million |

| Revenue forecast in 2032 |

USD 6623.05 million |

| Growth rate (CAGR) |

9.7% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

Valve Type Outlook; Procedure Type Outlook; Valve Position Outlook; Frame Material Outlook; End User Outlook |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Abbott Laboratories; Artivion, Inc.; Boston Scientific Corporation; Braile Biomedica; Colibri Heart Valve; Edwards Lifesciences Corporation; Labcor Laboratórios Ltda.; LivaNova PLC; Medtronic plc; Meril Life Sciences Pvt. Ltd. |

| No. of Pages |

326 |

By Segmentation

By Valve Type

- Stented Bovine Pericardial Valves

- Stentless Bovine Pericardial Valves

By Procedure Type

- Surgical Valves

- Transcatheter Valves

By Valve Position

- Aortic

- Mitral

- Tricuspid

- Pulmonary

- Others

By Frame Material

- Cobalt-Chromium

- Titanium

- Nickel-Molybdenum

- Others

By End User

- Hospitals

- Cardiac Centers

- Ambulatory Surgical Centers

- Specialty Clinics

- Public Hospitals

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa