Brain Tumor Diagnostics Market Overview:

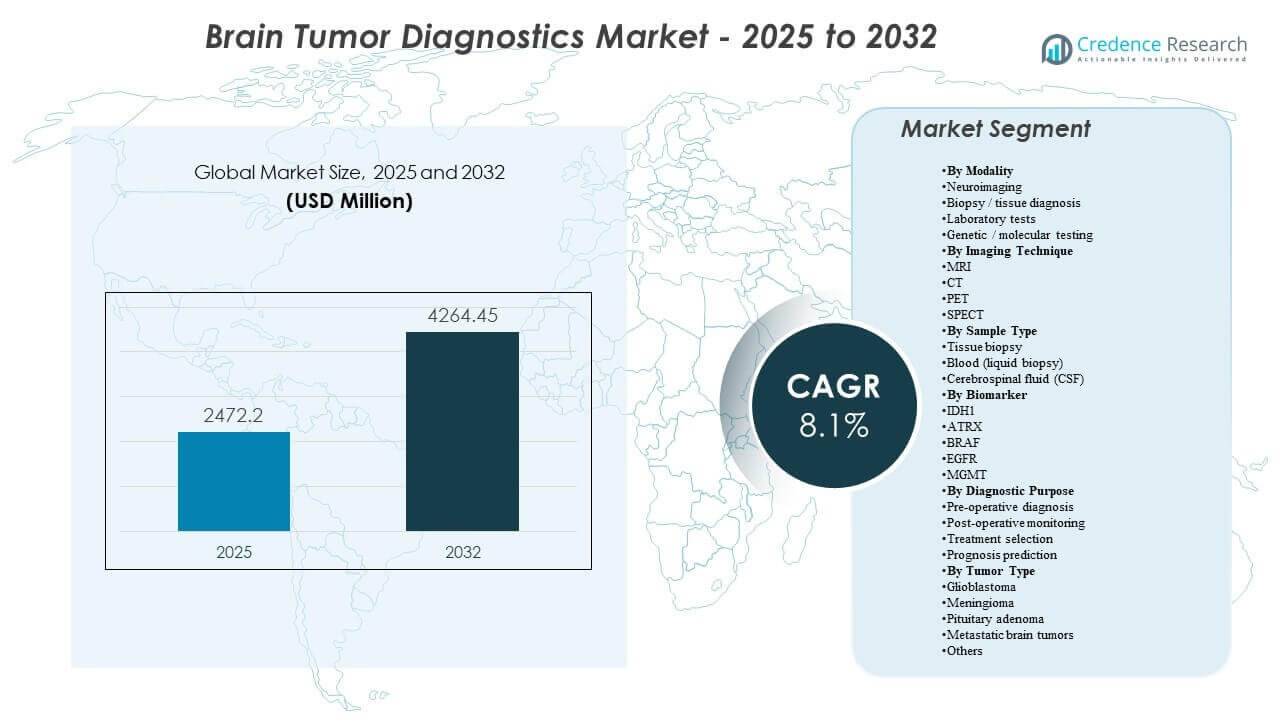

The global Brain Tumor Diagnostics Market size was estimated at USD 2472.2 million in 2025 and is expected to reach USD 4264.45 million by 2032, growing at a CAGR of 8.1% from 2025 to 2032. Demand is being reinforced by rising reliance on imaging-led decision making across the full care pathway, from initial suspicion and surgical planning to post-therapy surveillance where repeat scans are clinically routine. Increasing incorporation of molecular markers into classification and treatment selection is also pushing more standardized testing workflows across hospitals and reference laboratories.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Brain Tumor Diagnostics Market Size 2025 |

USD 2472.2 million |

| Brain Tumor Diagnostics Market, CAGR |

8.1% |

| Brain Tumor Diagnostics Market Size 2032 |

USD 4264.45 million |

Key Market Trends & Insights

- The Brain Tumor Diagnostics Market is forecast to expand at an 8.1% CAGR (2025–2032), reflecting sustained diagnostic intensity across imaging, tissue diagnosis, and molecular profiling.

- Neuroimaging proxy (imaging technique) represented 52.6%, underlining the central role of MRI/CT/PET/SPECT in first-line detection and longitudinal monitoring.

- Glioblastoma accounted for 29.4% (2025), supported by high diagnostic complexity, frequent follow-up needs, and therapy-planning dependence on imaging and biomarker results.

- North America held 40.7% (2025), driven by advanced imaging penetration, high specialist density, and earlier adoption of integrated radiology–pathology–molecular workflows.

- EGFR alterations are reported in about 60% of glioblastoma cases, supporting routine inclusion of actionable-marker testing in profiling strategies where available.

Segment Analysis

Diagnostic workflows in brain tumors are increasingly structured around imaging-first pathways, where neuroimaging establishes suspicion, guides biopsy planning, and supports treatment response tracking over time. Higher scan frequency in aggressive tumors strengthens utilization of installed imaging capacity, encouraging upgrades that improve throughput, standardization, and interpretability. Alongside imaging, tissue diagnosis remains essential when feasible, particularly to confirm histology and enable downstream biomarker testing that shapes risk stratification and therapy choices.

Molecular and genetic testing is gaining a larger role as clinical practice moves toward subtype-driven management, with markers used to refine classification, support treatment selection, and improve prognostic confidence. This shift increases demand for integrated testing workflows that connect radiology findings with pathology and molecular results, improving reporting consistency across multi-site health systems. Over time, this integration is expected to raise the value contribution of advanced laboratory assays, even when imaging remains the entry point for most patients.

By Modality Insights

Neuroimaging leads modality demand because most suspected brain tumor pathways begin with imaging-based detection and characterization, followed by imaging-guided clinical decision making. The neuroimaging proxy (imaging technique) accounted for ~52.6%, reflecting the high dependence on MRI/CT/PET/SPECT across diagnosis, pre-operative planning, and monitoring. Biopsy and tissue diagnosis remain critical for confirmation and grading when clinically feasible, while laboratory tests and genetic or molecular testing expand in importance as classification and treatment decisions become more biomarker-driven.

By Imaging Technique Insights

MRI is typically prioritized for brain tumor evaluation due to its soft-tissue contrast and flexibility across advanced sequences used for lesion characterization and surgical planning. CT remains important for rapid evaluation in acute settings and complements MRI where speed and access are key constraints. PET is used selectively to support metabolic assessment and response evaluation in specific clinical contexts, while SPECT remains more limited and tends to be used where PET access is constrained or for narrower functional indications. This mix supports around 52.6% imaging-technique share by sustaining high scan frequency in both initial workups and longitudinal follow-up.

By Sample Type Insights

Tissue biopsy remains the most definitive sample type when appropriate, enabling histopathology and confirmatory molecular workups that directly affect treatment pathways. Blood-based testing is attracting attention as a minimally invasive approach that could support longitudinal monitoring, although adoption depends on clinical validation and local reimbursement. CSF sampling supports specific clinical scenarios and can complement molecular assessment where tumor biology or clinical presentation makes CSF analysis relevant, particularly in CNS-focused pathways where repeat assessment is needed.

By Biomarker Insights

IDH1, ATRX, BRAF, EGFR, and MGMT are commonly referenced biomarkers because they support more refined classification and can inform treatment strategy and prognosis in relevant tumor contexts. Biomarker selection varies by tumor type and clinical setting, with broader panel testing more common where NGS or methylation profiling is available. Standardization of testing and reporting is increasingly important for multi-disciplinary tumor boards and consistent care across networks, helping connect molecular results to imaging and pathology findings.

By Diagnostic Purpose Insights

Pre-operative diagnosis remains fundamental because early characterization determines next steps such as referral, surgical planning, and biopsy approach. Post-operative monitoring creates sustained demand due to repeat imaging and follow-up testing to assess recurrence risk and treatment response, reinforcing the large imaging contribution around 52.6%. Treatment selection increasingly relies on combining imaging features with tissue and biomarker results, while prognosis prediction benefits from integrated interpretation across modalities and molecular findings.

By Tumor Type Insights

Glioblastoma leads tumor-type demand because it typically requires intensive diagnostic workups and frequent monitoring across the disease course. In 2025, glioblastoma accounted for 29.4%, reflecting higher diagnostic complexity, therapy-planning dependence, and repeat follow-up intensity. Meningioma and pituitary adenoma contribute materially through higher detection volumes in many settings, while metastatic brain tumors expand demand via oncology-driven surveillance and cross-specialty care pathways.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Brain Tumor Diagnostics Market Drivers

Rising reliance on neuroimaging across the care pathway

Neuroimaging remains the primary entry point for suspected brain tumors and is repeated through diagnosis, planning, and surveillance. Imaging supports lesion localization, treatment planning, and longitudinal progression assessment, making utilization structurally high. Increased availability of advanced MRI and hybrid imaging capabilities reinforces scan volumes in tertiary centers and expanding networks. Workflow optimization and quantitative tools further encourage standardization, supporting replacement and upgrade demand.

- For instance, Philips states that its SmartSpeed MRI technology can make scans up to 3 times faster, deliver up to 65% higher resolution, and remain compatible with 97% of clinical protocols, highlighting why providers continue upgrading neuroimaging platforms for higher-volume, standardized workflows.

Expansion of integrated molecular classification and profiling

Modern classification and management increasingly incorporate molecular markers, pushing broader adoption of genetic and molecular testing. This integration increases demand for standardized laboratory workflows and multi-disciplinary interpretation that connects imaging, pathology, and molecular data. As targeted approaches and risk stratification become more prevalent, profiling expands beyond complex referral cases into more routine pathways in larger systems. This shift supports higher testing intensity per patient and broader adoption of advanced assays.

- For instance, Illumina’s TruSight Oncology 500 platform is designed to analyze 523 cancer-related genes from DNA and RNA in one workflow, while the ctDNA version covers a 1.94 Mb panel, including 59 genes for copy number variants and 23 genes for rearrangements, demonstrating the increasing scale and standardization of molecular profiling.

Growth in specialist care capacity and oncology pathway formalization

Health systems are strengthening neuro-oncology pathways through dedicated centers, tumor boards, and standardized diagnostic protocols. Structured pathways tend to increase repeat testing because they emphasize monitoring cadence and consistent follow-up. Referral concentration into specialist centers raises imaging and molecular testing density, improving utilization of high-end platforms. This also supports service and software demand tied to reporting, interoperability, and longitudinal tracking.

Technology upgrades to improve throughput and decision consistency

Radiology and laboratory environments face volume pressure and staffing constraints, increasing the value of productivity improvements. Faster acquisition, improved image quality, dose-management features, and integrated reporting reduce repeat scans and interpretation variability. In laboratories, automation and informatics improve turnaround time and reduce manual handling risks. These improvements support purchasing decisions that favor integrated platforms rather than isolated components.

Brain Tumor Diagnostics Market Challenges

Clinical variability and access gaps remain persistent constraints across regions and facility tiers. Advanced imaging and molecular profiling require specialized infrastructure, trained staff, and stable reimbursement, which can limit adoption outside major centers. Differences in testing protocols and reporting standards can also introduce inconsistency in how results are interpreted across sites, raising the need for harmonization. In lower-resource settings, delayed diagnosis and fragmented referrals can further reduce the clinical value captured from advanced diagnostic tools.

- For instance, Siemens Healthineers’ Biograph Vision Quadra PET/CT offers a 106-cm axial field of view, 128 CT slices, 228 ps time-of-flight performance, and 1000 cps/kBq effective sensitivity.

Cost sensitivity also influences procurement and utilization decisions, particularly in systems facing budget constraints or uneven reimbursement coverage. High upfront equipment costs, ongoing maintenance, and consumable requirements can delay upgrades or constrain usage intensity. In molecular testing, limited local availability, sample logistics, and turnaround time challenges can restrict routine integration into care pathways. These constraints often lead providers to prioritize essential imaging over broader profiling, slowing adoption of comprehensive diagnostic panels.

Brain Tumor Diagnostics Market Trends and Opportunities

Multi-modal integration is becoming a defining direction, with growing emphasis on connecting imaging features with histopathology and molecular results in a single diagnostic narrative. This trend strengthens demand for interoperable informatics, structured reporting, and longitudinal patient tracking that improves follow-up consistency. Providers also increasingly value tools that reduce interpretation variability, creating opportunities for advanced visualization, quantitative analysis, and guided workflow solutions. Vendors that combine AI-enabled imaging with decision support and lab connectivity are better positioned to win enterprise-wide deployments.

Decentralization of diagnostics is also creating opportunity as imaging and testing extend beyond top-tier hospitals into networks of imaging centers and regional oncology hubs. As capacity expands, buyers prioritize reliable platforms, service quality, and standardized protocols to ensure comparable outcomes across sites. This shift supports growth for vendors offering scalable deployments, robust training, and integrated service models. Partnerships with regional labs and tele-radiology networks can accelerate uptake by reducing expertise and reporting bottlenecks.

- For instance, 5C Network says its AI-powered teleradiology platform serves 1,500+ healthcare facilities with 400+ radiologists, delivers reports in an average of 30 minutes, enables PACS go-live in 72 hours, and reports 96.7% accuracy with 40% fewer quality-control rejections, while Teleradiology Solutions states that it has reported scans for over 8.5 million patients and serves more than 150 hospitals across 21 countries.

Regional Insights

North America

North America represents the largest regional share at 40.7% (2025), supported by high penetration of advanced imaging, specialist care concentration, and broader access to molecular profiling. Diagnostic pathways are typically standardized through tumor boards and multi-disciplinary workflows that increase repeat monitoring volumes. Procurement decisions often emphasize uptime, workflow integration, and compatibility with enterprise imaging and laboratory informatics. This environment supports premium system upgrades and software-led differentiation.

Europe

Europe accounts for 24.9% (2025), driven by established imaging infrastructure and mature oncology referral networks in major countries. The region benefits from structured clinical pathways that encourage consistent follow-up imaging and confirmatory testing where indicated. Adoption levels vary by country depending on reimbursement structures and local capacity, influencing the pace of molecular workflow expansion. Standardization and interoperability remain important themes for multi-site health systems.

Asia Pacific

Asia Pacific holds 23.6% (2025), supported by expanding imaging access, increasing cancer care capacity, and rising adoption of precision diagnostics in leading markets. Urban tertiary centers drive high-end demand, while broader network expansion supports mid-range systems with strong service models. Growth is influenced by infrastructure investment, workforce scaling, and payer coverage decisions that determine how widely advanced testing is used. As capability spreads, demand strengthens for standardized reporting and scalable platforms.

Latin America

Latin America contributes 6.4% (2025), where adoption is concentrated in larger private hospital networks and reference centers. Access constraints and uneven reimbursement can limit high-end imaging and routine molecular profiling in some settings. However, expanding oncology care capacity and modernization of imaging fleets can steadily increase utilization. Vendors with strong channel coverage and service capability tend to perform better in dispersed markets.

Middle East & Africa

Middle East & Africa represents 4.4% (2025), with demand led by wealthier Gulf markets and select urban centers where investment in advanced care is higher. Growth is supported by capacity expansion in oncology and diagnostic infrastructure, though access remains uneven across many countries. Procurement often prioritizes dependable service, training support, and end-to-end solutions that reduce operational variability. Over time, network expansion can broaden demand beyond flagship hospitals.

Competitive Landscape

Competition is shaped by the ability to deliver integrated diagnostic ecosystems that connect imaging hardware, advanced visualization, workflow software, and interoperability with hospital systems. Vendors differentiate through productivity features, image quality, and decision-support capabilities that improve reporting consistency in complex neuro-oncology cases. Partnerships and platform integration strategies are increasingly important as providers seek unified pathways across radiology, pathology, and molecular diagnostics. Service coverage, upgrade paths, and installed-base expansion continue to influence competitive intensity.

GE Healthcare remains positioned around strengthening imaging-centric workflows through portfolio depth and expanding software and AI capabilities that support neurological imaging analysis and enterprise-scale deployment. The company’s strategy typically emphasizes throughput improvements, consistency in interpretation, and scalable solutions that fit multi-site systems. Progress is also supported by moves that broaden imaging informatics reach and enable more standardized assessment across longitudinal monitoring workflows. This approach aligns with buyer demand for integrated systems that reduce variability and improve operational reliability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- GE Healthcare

- Koninklijke Philips N.V. (Philips Healthcare)

- Siemens Healthineers

- Fujifilm Corporation

- Hitachi, Ltd. (Hitachi Healthcare)

- Roche Diagnostics (F. Hoffmann-La Roche Ltd.)

- Thermo Fisher Scientific

- Abbott Laboratories

- Illumina, Inc.

- Canon Medical Systems

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In July 2025, Plus Therapeutics said its subsidiary CNSide Diagnostics would commercially launch the CNSide cerebrospinal fluid assay platform in Texas from August 2025, expanding access to a platform designed to identify and molecularly characterize tumor cells and circulating tumor DNA in cerebrospinal fluid for CNS cancers.

- In August 2025 update, MedGenome announced the launch of India’s first CNS Tumor Methylation Classifier Test, a diagnostic assay designed to classify more than 90 brain and central nervous system tumor classes through DNA methylation profiling.

- In November 2025, GenomOncology partnered with the Glioblastoma Foundation to integrate GenomOncology’s Pathology Workbench into the foundation’s genomic testing laboratory, with the aim of speeding genomic testing and clinical reporting for glioblastoma patients.

- In February 2026, Azurity Pharmaceuticals said Ferabright became available in the U.S. for magnetic resonance imaging of the brain, and the company described it as the first and only iron-based contrast agent indicated for MRI of the brain in adults with known or suspected malignant brain neoplasms.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 2472.2 million |

| Revenue forecast in 2032 |

USD 4264.45 million |

| Growth rate (CAGR) |

8.1% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Modality Outlook: Neuroimaging; Biopsy / tissue diagnosis; Laboratory tests; Genetic / molecular testing.

By Imaging Technique Outlook: MRI; CT; PET; SPECT.

By Sample Type Outlook: Tissue biopsy; Blood (liquid biopsy); Cerebrospinal fluid (CSF).

By Biomarker Outlook: IDH1; ATRX; BRAF; EGFR; MGMT.

By Diagnostic Purpose Outlook: Pre-operative diagnosis; Post-operative monitoring; Treatment selection; Prognosis prediction.

By Tumor Type Outlook: Glioblastoma; Meningioma; Pituitary adenoma; Metastatic brain tumors; Others |

| Regional scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Key companies profiled |

GE Healthcare, Koninklijke Philips N.V. (Philips Healthcare), Siemens Healthineers, Fujifilm Corporation, Hitachi, Ltd. (Hitachi Healthcare), Roche Diagnostics (F. Hoffmann-La Roche Ltd.), Thermo Fisher Scientific, Abbott Laboratories, Illumina, Inc., Canon Medical Systems |

| No. of Pages |

340 |

Segmentation

By Modality

- Neuroimaging

- Biopsy / tissue diagnosis

- Laboratory tests

- Genetic / molecular testing

By Imaging Technique

By Sample Type

- Tissue biopsy

- Blood (liquid biopsy)

- Cerebrospinal fluid (CSF)

By Biomarker

By Diagnostic Purpose

- Pre-operative diagnosis

- Post-operative monitoring

- Treatment selection

- Prognosis prediction

By Tumor Type

- Glioblastoma

- Meningioma

- Pituitary adenoma

- Metastatic brain tumors

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa