Market Overview

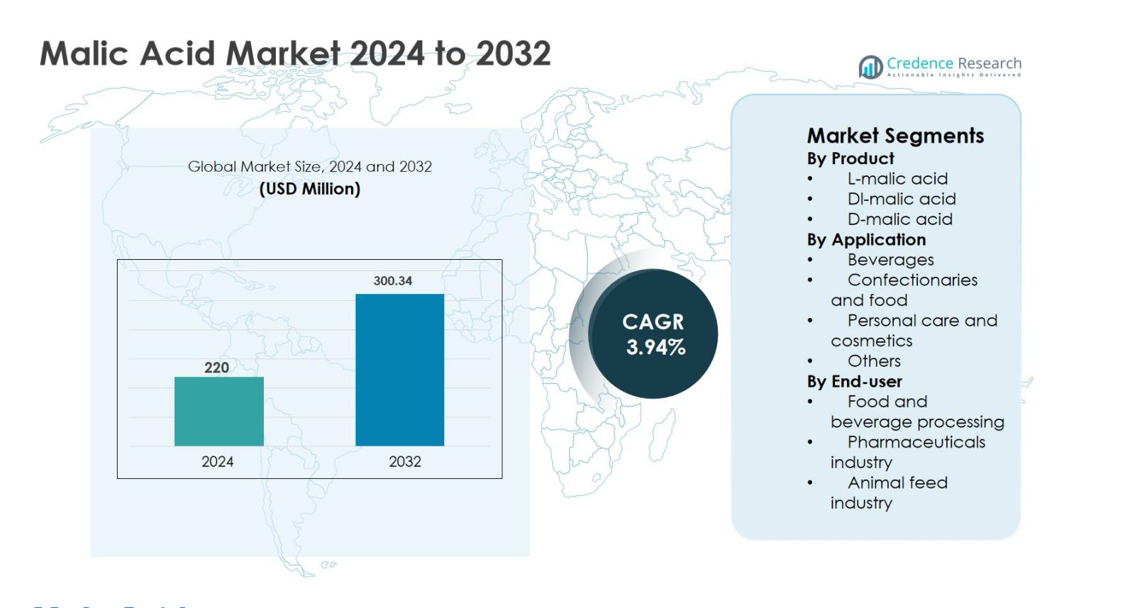

Malic Acid market size was valued at USD 220 million in 2024 and is anticipated to reach USD 300.34 million by 2032, growing at a CAGR of 3.94% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Malic Acid Market Size 2024 |

USD 220 million |

| Malic Acid Market, CAGR |

3.94% |

| Malic Acid Market Size 2032 |

USD 300.34 million |

Malic Acid market is driven by the strong presence of established global and regional manufacturers focused on food, pharmaceutical, and personal care applications. Key players such as Corbion N.V., Bartek Ingredients Inc., Lonza Group Ltd., Fuso Chemical Co. Ltd., Changmao Biochemical Engineering Co. Ltd., Anhui Sealong Biotechnology Co. Ltd., NACALAI TESQUE INC, Isegen South Africa Pty Ltd., Guangzhou ZIO Chemical Co. Ltd., and Muby Chem Ltd. compete through product quality, fermentation-based production, and expanded distribution networks. Asia-Pacific emerged as the leading region with an exact 34.9% market share in 2024, supported by large-scale manufacturing capacity and high consumption of processed foods and beverages. North America followed with 27.8% share, driven by clean-label demand, while Europe accounted for 24.6%, supported by regulatory preference for natural acidulants.

Market Insights

- Malic Acid market size was valued at USD 220 million in 2024 and is projected to reach USD 300.34 million by 2032, growing at a CAGR of 3.94% during the forecast period.

- Market growth is primarily driven by rising demand from the food and beverage industry, especially beverages and confectionery, where malic acid is widely used for flavor enhancement, pH control, and taste stability, supported by increasing clean-label and natural ingredient adoption.

- A key market trend is the growing preference for L-malic acid, which dominated the product segment with 62.4% share in 2024, due to its natural sourcing and compatibility with health-focused and premium formulations across food, nutraceutical, and personal care applications.

- The market remains moderately consolidated, with leading players focusing on fermentation-based production, capacity expansion, and long-term supply agreements to manage competition from substitute acidulants such as citric and lactic acid.

- Asia-Pacific led the Malic Acid market with 34.9% share in 2024, followed by North America at 27.8% and Europe at 24.6%, driven by strong food processing, pharmaceutical manufacturing, and rising consumption of processed and functional products.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Product

The Malic Acid market by product is led by L-malic acid, which accounted for 62.4% market share in 2024, driven by its natural occurrence in fruits and strong compatibility with clean-label formulations. L-malic acid is widely preferred in food, beverage, and nutraceutical applications due to its smoother taste profile, higher solubility, and broad regulatory acceptance. DL-malic acid follows with notable adoption in cost-sensitive food and industrial uses, while D-malic acid holds a smaller share because of limited commercial applications. Rising demand for naturally sourced acidulants continues to reinforce the dominance of L-malic acid.

- For instance, Coca‑Cola lists malic acid as an acidulant in select flavored beverages to enhance tartness while maintaining a balanced taste profile.

By Application

The beverages segment dominated the Malic Acid market with a 38.6% share in 2024, supported by extensive use in carbonated drinks, sports beverages, flavored waters, and fruit-based formulations. Malic acid improves flavor stability, enhances tartness, and balances sweetness, making it ideal for modern beverage formulations. Confectionery and food applications follow, driven by demand for taste enhancement and shelf-life improvement. Personal care and cosmetics show steady growth due to malic acid’s exfoliating and pH-regulating properties, while other applications maintain stable demand across specialty industrial uses.

- For instance, Mars Wrigley and other major candy manufacturers use malic acid in sour gums and candies to provide a long‑lasting, intense tart flavor.

By End-User

The food and beverage processing industry held the largest share of 46.9% in 2024, driven by high consumption of malic acid as an acidulant, flavor enhancer, and buffering agent in processed foods and drinks. Its functional advantages, including taste enhancement and formulation stability, support widespread adoption among manufacturers. The pharmaceuticals industry represents a growing end-user segment, utilizing malic acid in effervescent tablets and oral drug formulations. The animal feed industry also contributes steadily, using malic acid to improve feed palatability and digestive efficiency.

Key Growth Drivers

Rising Demand from Food and Beverage Industry

The Malic Acid market is significantly driven by rising demand from the global food and beverage industry, where malic acid is extensively used as an acidulant, flavor enhancer, and pH regulator. Increasing consumption of carbonated drinks, sports beverages, flavored waters, confectionery, and processed foods continues to support volume growth. Manufacturers prefer malic acid due to its superior flavor retention, smoother sourness profile, and ability to enhance fruit flavors compared to alternative acidulants. Growing consumer inclination toward ready-to-drink beverages and packaged foods, especially in emerging economies, further strengthens demand. Additionally, the shift toward clean-label and naturally derived ingredients has accelerated the adoption of L-malic acid in premium food and beverage formulations, reinforcing long-term market expansion across both developed and developing regions.

- For instance, Nestlé uses malic acid in selected powdered beverage mixes and juice drinks to deliver consistent tartness and maintain taste over shelf life.

Expansion of Clean-Label and Natural Ingredient Formulations

The increasing focus on clean-label products and natural ingredients acts as a major growth driver for the Malic Acid market. Food, beverage, and nutraceutical manufacturers are reformulating products to eliminate synthetic additives and meet consumer expectations for transparency and natural sourcing. Naturally derived L-malic acid, commonly extracted through fermentation processes, aligns well with these requirements and supports clean-label claims. This trend is particularly strong in functional foods, dietary supplements, and health-oriented beverages. Regulatory support for natural acidulants and rising awareness of ingredient safety further contribute to adoption. As brands emphasize product differentiation through natural positioning, malic acid demand continues to grow across multiple application areas, supporting steady market expansion.

- For instance, Danone has highlighted its move toward shorter, more recognizable ingredient lists in yogurt and beverage portfolios, incorporating organic acids that fit clean-label expectations.

Growing Utilization in Pharmaceutical and Nutraceutical Applications

The pharmaceutical and nutraceutical sectors represent another key growth driver for the Malic Acid market. Malic acid is widely used in effervescent tablets, syrups, and oral drug formulations due to its buffering capacity, pleasant taste, and compatibility with active pharmaceutical ingredients. Growth in preventive healthcare, increasing consumption of dietary supplements, and rising geriatric populations contribute to higher demand. In nutraceuticals, malic acid supports energy metabolism formulations and mineral absorption products. Expanding pharmaceutical manufacturing capacities in Asia-Pacific and Latin America further accelerate consumption. Continuous innovation in drug delivery formats and flavored dosage forms strengthens malic acid adoption, ensuring consistent demand growth from healthcare-related industries.

Key Trends & Opportunities

Increasing Adoption in Personal Care and Cosmetics

A notable trend in the Malic Acid market is its growing adoption in personal care and cosmetic formulations. Malic acid is increasingly used in skincare products as an alpha-hydroxy acid for exfoliation, skin renewal, and pH adjustment. Rising consumer demand for mild, fruit-derived acids in beauty products supports this trend. Clean beauty and dermatologically tested formulations further encourage manufacturers to replace harsh synthetic acids with naturally derived alternatives. Expanding skincare markets in Asia-Pacific and increasing premium cosmetic consumption in North America and Europe create attractive growth opportunities. Product innovation in anti-aging, acne treatment, and skin-brightening solutions continues to expand malic acid’s application scope.

- For instance, Paula’s Choice uses fruit-derived AHAs, including malic acid, in certain exfoliating treatments to support gentle resurfacing and smoother skin texture.

Technological Advancements in Bio-Based Production

Technological advancements in fermentation and bio-based production processes present strong growth opportunities for the Malic Acid market. Manufacturers are increasingly investing in sustainable production methods to reduce reliance on petrochemical-based synthesis and improve cost efficiency. Advances in microbial fermentation improve yield, purity, and scalability of L-malic acid production, supporting competitive pricing and environmental compliance. These innovations align with global sustainability goals and corporate ESG strategies. Improved production efficiency also enables suppliers to meet rising demand from food, pharmaceutical, and cosmetic industries. As sustainability becomes a critical purchasing criterion, bio-based malic acid production offers long-term competitive advantages.

- For instance, Anhui Huaheng Biological launched a fermentation-based L-malic acid project with around 50,000 tons per year capacity as an eco-friendly alternative to chemical routes, targeting food, pharmaceutical, cosmetic, and feed applications

Key Challenges

Price Volatility of Raw Materials

Price volatility of raw materials poses a key challenge for the Malic Acid market. Fluctuations in feedstock prices, energy costs, and fermentation inputs directly impact production economics and profit margins. Manufacturers operating in cost-sensitive markets face challenges in maintaining stable pricing while ensuring product quality. Sudden increases in raw material costs can disrupt supply chains and affect long-term contracts with end users. Smaller producers are particularly vulnerable to these fluctuations, which may limit capacity expansion and investment. Managing input cost volatility while remaining competitive continues to be a critical challenge for market participants.

Competition from Substitute Acidulants

The Malic Acid market faces strong competition from substitute acidulants such as citric acid, tartaric acid, and lactic acid, which are widely available and often lower in cost. Citric acid, in particular, dominates many food and beverage applications due to its extensive availability and established supply chain. This competitive pressure limits pricing flexibility for malic acid manufacturers and can restrict adoption in cost-driven formulations. End users often switch between acidulants based on price, functionality, and availability. Overcoming substitution risk requires continuous product differentiation, application-specific advantages, and education on malic acid’s superior flavor and functional performance.

Regional Analysis

North America

North America accounted for 27.8% of the Malic Acid market share in 2024, supported by strong demand from the food and beverage, pharmaceuticals, and personal care industries. The region benefits from high consumption of functional beverages, processed foods, and dietary supplements, where malic acid is widely used for flavor enhancement and formulation stability. Clean-label trends and preference for naturally derived ingredients further boost L-malic acid adoption. The presence of established food manufacturers, advanced pharmaceutical production, and stringent quality standards continues to drive consistent demand across the United States and Canada, ensuring steady regional market growth.

Europe

Europe held 24.6% market share in 2024, driven by strong regulatory support for natural additives and widespread adoption of clean-label formulations. The region shows high demand for malic acid in beverages, confectionery, bakery products, and cosmetic formulations. Countries such as Germany, France, and the United Kingdom lead consumption due to mature food processing and pharmaceutical industries. Growing focus on sustainable sourcing and bio-based production further supports market expansion. Additionally, increasing use of malic acid in personal care and dermatological products strengthens demand, positioning Europe as a stable and innovation-driven regional market.

Asia-Pacific

Asia-Pacific dominated the Malic Acid market with a 34.9% share in 2024, supported by rapid expansion of food and beverage processing, pharmaceuticals, and nutraceutical manufacturing. Rising population, urbanization, and increasing consumption of packaged foods and flavored beverages significantly drive demand. China and India lead regional growth due to large-scale production capacity and cost-efficient manufacturing. Growing awareness of natural ingredients and expanding middle-class consumption further support market expansion. Additionally, increasing investments in fermentation-based production technologies strengthen regional supply capabilities, making Asia-Pacific the fastest-growing and most influential regional market.

Latin America

Latin America accounted for 7.1% market share in 2024, supported by growing food and beverage production and rising consumption of processed foods and soft drinks. Countries such as Brazil and Mexico drive regional demand due to expanding beverage manufacturing and increasing adoption of acidulants in food processing. Improving pharmaceutical manufacturing capabilities and growing nutraceutical awareness also contribute to steady growth. Although the market remains smaller compared to developed regions, rising urbanization, improving disposable income, and gradual adoption of clean-label ingredients create favorable conditions for sustained malic acid demand across the region.

Middle East & Africa

The Middle East & Africa region held 5.6% market share in 2024, driven by growing food processing activities and increasing consumption of packaged and flavored food products. Expanding beverage production in Gulf countries and rising pharmaceutical manufacturing in select African economies support regional demand. The market benefits from gradual modernization of food supply chains and increasing import of specialty food ingredients. While adoption remains moderate, rising health awareness and improving regulatory frameworks for food additives are expected to support gradual growth, positioning the region as an emerging opportunity within the global Malic Acid market.

Market Segmentations:

By Product

- L-malic acid

- Dl-malic acid

- D-malic acid

By Application

- Beverages

- Confectionaries and food

- Personal care and cosmetics

- Others

By End-user

- Food and beverage processing

- Pharmaceuticals industry

- Animal feed industry

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The Malic Acid market features a moderately consolidated landscape, characterized by the presence of both global manufacturers and regional producers competing on product quality, purity, pricing, and supply reliability. Key players such as Corbion N.V., Bartek Ingredients Inc., Lonza Group Ltd., Fuso Chemical Co. Ltd., Changmao Biochemical Engineering Co. Ltd., Anhui Sealong Biotechnology Co. Ltd., NACALAI TESQUE INC, Isegen South Africa Pty Ltd., Guangzhou ZIO Chemical Co. Ltd., and Muby Chem Ltd. focus on expanding production capacity and strengthening distribution networks to serve food, pharmaceutical, and personal care applications. Companies increasingly emphasize L-malic acid to address growing clean-label and natural ingredient demand. Strategic investments in fermentation technology, process optimization, and sustainability initiatives help players enhance cost efficiency and meet regulatory standards. Long-term supply agreements with food and beverage manufacturers and geographic expansion across emerging markets remain key competitive strategies.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Corbion N.V.

- Muby Chem Ltd.

- NACALAI TESQUE INC

- Lonza Group Ltd.

- Fuso Chemical Co. Ltd.

- Anhui Sealong Biotechnology Co. Ltd.

- Isegen South Africa Pty Ltd.

- Changmao Biochemical Engineering Co. Ltd.

- Guangzhou ZIO Chemical Co. Ltd

- Bartek Ingredients Inc.

Recent Developments

- In December 2025, TCL Specialties LLC (subsidiary of Thirumalai Chemicals Ltd.) commenced pre-commissioning and start-up activities at its new West Virginia, USA manufacturing facility, which includes a Food Ingredients plant producing malic acid alongside maleic anhydride, boosting domestic supply for North America and other regions.

- In June 2024, Anhui Huaheng Biology Company Ltd. (AHB) developed and launched Bioscentis MA, a bio-based L-Malic Acid under its Bioscentis brand an eco-friendly malic acid with higher acidity suited for beverages, confectionery, and baking applications.

- In 2024, NNB Nutrition introduced a Moisture-Resistant DL-Malic Acid product using its patented FlowTech™ technology to improve stability and processing performance in food and beverage applications.

Report Coverage

The research report offers an in-depth analysis based on Product, Application, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The Malic Acid market will continue to expand steadily, supported by consistent demand from food, beverage, pharmaceutical, and personal care industries.

- Adoption of L-malic acid will increase further as manufacturers prioritize clean-label, natural, and fruit-derived ingredients.

- Beverage applications will remain the primary consumption segment, driven by growth in functional drinks, flavored waters, and sports beverages.

- Pharmaceutical and nutraceutical usage will rise due to increasing production of effervescent tablets and flavored oral formulations.

- Bio-based and fermentation-driven production technologies will gain wider adoption to improve sustainability and supply efficiency.

- Asia-Pacific will maintain its leading position due to strong manufacturing capacity and rising processed food consumption.

- Personal care and cosmetic applications will grow steadily, supported by demand for mild exfoliating and pH-balancing ingredients.

- Competitive intensity will increase as manufacturers focus on product differentiation and application-specific solutions.

- Price sensitivity and substitution by alternative acidulants will encourage innovation in performance and cost optimization.

- Regulatory support for natural food additives will strengthen long-term demand across global markets.