Market Overview:

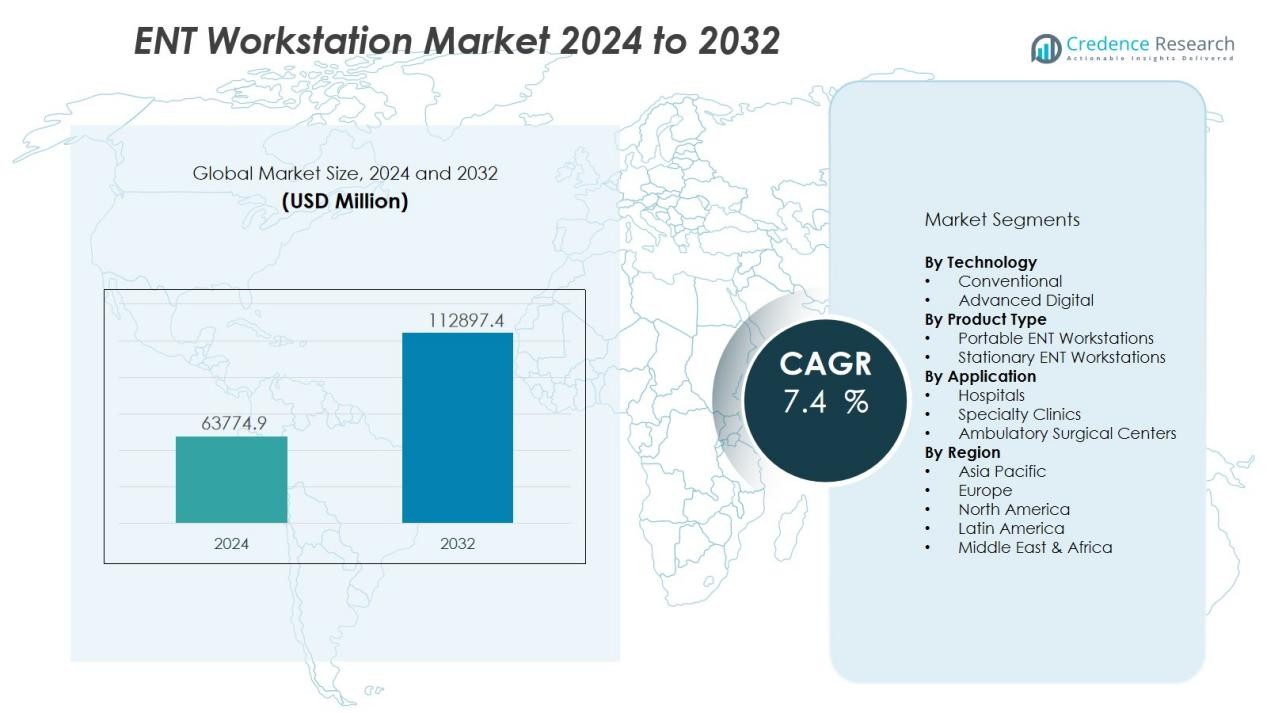

The ENT Workstation Market size was valued at USD 63774.9 million in 2024 and is anticipated to reach USD 112897.4 million by 2032, at a CAGR of 7.4 % during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| ENT Workstation Market Size 2024 |

USD 63774.9 Million |

| ENT Workstation Market, CAGR |

7.4 % |

| ENT Workstation Market Size 2032 |

USD 112897.4 Million |

Market growth is fueled by the rising prevalence of ear, nose, and throat disorders, an aging population, and increasing adoption of minimally invasive diagnostic procedures. Advances in medical imaging, improved ergonomics, and the integration of digital technologies for enhanced visualization and data management are further supporting adoption. The expansion of ENT specialty clinics and the growing need for equipment upgrades in hospitals strengthen market prospects. Supportive healthcare infrastructure investments, particularly in emerging economies, also contribute to the upward trajectory.

Regionally, North America holds a significant share of the ENT workstation market due to high healthcare spending, strong adoption of advanced medical technologies, and a well-established ENT care network. Europe follows with robust demand in countries such as Germany, France, and the UK, driven by favorable reimbursement policies and advanced clinical practices. The Asia-Pacific region is expected to record the fastest growth, supported by rapid healthcare infrastructure development, rising ENT disease incidence, and expanding access to specialty care in countries like China and India.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The ENT workstation market was valued at USD 63,774.9 million in 2024 and is projected to reach USD 112,897.4 million by 2032, reflecting strong growth at a CAGR of 7.4% from 2024 to 2032.

- Rising prevalence of ENT disorders such as chronic sinusitis, hearing loss, and throat infections is significantly boosting demand for advanced diagnostic and treatment solutions.

- Technological advancements in imaging, endoscopy, and digital data management are enhancing diagnostic precision and improving procedural efficiency.

- Growing adoption of minimally invasive procedures is increasing the demand for compact, multifunctional workstations that streamline clinical workflows.

- High equipment costs and limited reimbursement support remain key barriers, particularly in budget-sensitive and developing healthcare markets.

- North America holds 38% market share, Europe 30%, and Asia-Pacific 22%, with the latter expected to witness the fastest growth due to healthcare infrastructure expansion.

- Emerging markets in Asia-Pacific, Latin America, and the Middle East present strong growth potential, driven by government investments, rising insurance coverage, and increasing access to specialty ENT care.

Market Drivers:

Rising Prevalence of ENT Disorders Driving Equipment Demand:

The increasing incidence of ear, nose, and throat disorders worldwide is a primary driver for the ENT workstation market. Conditions such as chronic sinusitis, hearing loss, and throat infections are becoming more common due to aging populations, pollution, and lifestyle factors. This trend is boosting the demand for advanced diagnostic and treatment solutions that improve patient outcomes. It is also prompting healthcare facilities to invest in comprehensive workstations equipped with multiple functionalities.

- For instance, ATMOS Rhino 31 enables precise quantification and differentiation of nasal resistance using real-time measurement and individualized analysis parameters, incorporating a unique hygiene concept with replaceable filter pads to prevent contamination, resulting in reliable diagnosis and safer patient exams.

Technological Advancements Enhancing Diagnostic Efficiency:

Continuous innovation in imaging, endoscopy, and integrated software solutions is accelerating adoption in the ENT workstation market. High-definition visualization, ergonomic designs, and digital data management are improving diagnostic accuracy and procedural efficiency. It is enabling ENT specialists to perform precise interventions with minimal patient discomfort. Integration of modular components further allows customization based on clinical requirements.

- For instance, the ATMOS Scope flexible HD video nasopharyngo-laryngoscope features an integrated CMOS sensor delivering 1,280×800 pixel resolution, allowing ENT specialists to perform precise interventions while minimizing patient discomfort.

Growing Adoption of Minimally Invasive Procedures:

The shift toward minimally invasive ENT procedures is fueling the demand for multifunctional and compact workstations. These systems allow physicians to conduct diagnostics and treatments in a single setting, reducing patient turnaround time. It supports faster recovery and lower complication risks, increasing patient preference for advanced ENT care. Healthcare providers are increasingly opting for such integrated solutions to improve operational efficiency.

Healthcare Infrastructure Development in Emerging Markets:

Rapid expansion of healthcare facilities in developing regions is opening new growth opportunities for the ENT workstation market. Rising government investments in hospital modernization and specialty clinics are creating demand for technologically advanced equipment. It is further supported by the growing availability of skilled ENT professionals and expanding insurance coverage. This environment is fostering higher adoption rates in Asia-Pacific, Latin America, and parts of the Middle East.

Market Trends:

Integration of Digital Technologies and Advanced Imaging:

The ENT workstation market is witnessing a growing trend toward integration of digital technologies, high-definition imaging, and data connectivity. Modern workstations now incorporate advanced endoscopic cameras, touch-screen controls, and software for real-time image capture and storage. It enables ENT specialists to conduct more accurate diagnostics and document procedures seamlessly. Cloud-based connectivity is gaining traction, allowing secure sharing of patient records and images across healthcare networks. The adoption of AI-assisted image analysis is also expanding, supporting early detection of abnormalities. This technological convergence is redefining workflow efficiency and diagnostic precision in ENT practices.

- For instance, Olympus launched the VISERA S video processor, featuring noise reduction and advanced visualization for ENT imaging, and their CV-1500 EVIS X1 system enables digital output (3G-SDI, HDMI) and observation modes like NBI, TXI, and RDI for more accurate diagnostics.

Rising Demand for Modular and Ergonomic Designs:

Healthcare providers are increasingly favoring modular ENT workstations that can be customized to suit specific clinical requirements. Manufacturers are focusing on designs that optimize space, enhance ergonomics, and improve operator comfort during long procedures. It is leading to the development of compact units with adjustable components, integrated suction, and lighting systems. The trend toward patient-centric care is also influencing the inclusion of noise-reduction features and smoother operation controls. Growing emphasis on infection control is driving the use of antimicrobial surfaces and easy-to-clean materials. These design innovations are aligning with the industry’s shift toward efficiency, safety, and patient comfort.

- For instance, Olympus’s WM-DP3 double-wide workstation supports up to 60 kg of endoscopy equipment on its articulated arms, ensuring stable positioning throughout procedures.

Market Challenges Analysis:

High Equipment Costs and Budget Constraints:

The ENT workstation market faces challenges due to the high cost of advanced equipment, which can limit adoption in budget-sensitive healthcare settings. Comprehensive workstations with integrated imaging, suction, and diagnostic tools require significant capital investment. It poses a barrier for small clinics and facilities in developing regions with limited funding. Maintenance and replacement parts further add to operational expenses, impacting long-term affordability. Price-sensitive markets may delay upgrades, slowing overall market penetration. This cost challenge is particularly critical in regions where reimbursement support is limited.

Shortage of Skilled Professionals and Technical Training Needs:

A lack of adequately trained ENT specialists and technical staff is restricting the effective utilization of advanced workstations. It is especially evident in rural and underdeveloped areas where healthcare infrastructure is still evolving. Complex systems require specialized training to operate efficiently and maintain optimal performance. Limited availability of continuous education programs slows down adoption rates. Inadequate technical support in certain markets can also lead to equipment underuse or downtime. Addressing this skills gap is essential for maximizing the benefits of advanced ENT workstation technology.

Market Opportunities:

Expanding Demand in Emerging Healthcare Markets:

Rapid growth in healthcare infrastructure across Asia-Pacific, Latin America, and the Middle East is creating significant opportunities for the ENT workstation market. Rising government investments in hospital modernization and specialty clinics are accelerating equipment procurement. It is further supported by increasing healthcare awareness and insurance penetration in these regions. Expanding middle-class populations with higher disposable incomes are boosting demand for advanced ENT care. Manufacturers can leverage these trends by introducing cost-effective models tailored for local needs. Strategic partnerships with regional distributors can also strengthen market reach.

Innovation in Portable and Telemedicine-Enabled Solutions:

The shift toward decentralized and remote healthcare is driving opportunities for portable ENT workstations integrated with telemedicine capabilities. Compact, mobile units can serve rural and underserved areas, improving access to specialist care. It is encouraging manufacturers to develop lightweight, battery-operated systems with wireless connectivity for real-time consultations. Integration with AI-based diagnostic tools can further enhance decision-making in remote settings. This innovation trend aligns with global efforts to expand patient access and reduce healthcare disparities. Companies that focus on portability, connectivity, and affordability stand to gain a competitive edge.

Market Segmentation Analysis:

By Technology:

The ENT workstation market is segmented by technology into conventional and advanced digital systems. Conventional models continue to serve small clinics and budget-sensitive facilities due to lower costs and simpler configurations. Advanced digital workstations integrate high-definition imaging, endoscopic systems, and data management software, improving diagnostic accuracy and workflow efficiency. It is witnessing growing demand for AI-enabled features and cloud connectivity that support telemedicine and collaborative care. Digital systems dominate in developed markets, driven by their ability to enhance precision and patient outcomes.

- For instance, the ZEISS SL Imaging Solution allows real-time live imaging at up to 40 frames-per-second with up to 18-megapixel resolution for advanced ENT diagnostics.

By Product Type:

Product segmentation includes portable and stationary ENT workstations. Portable units are gaining traction for their flexibility in rural healthcare settings and smaller clinics. Stationary systems remain preferred in large hospitals and specialty centers where comprehensive diagnostic capabilities and higher durability are critical. It is seeing innovation in modular designs that allow customization of components for different clinical needs. Demand is rising for compact stationary units that optimize space without compromising performance.

- For instance, HEINE’s mini 3000® LED handheld ENT diagnostic unit offers up to 10 hours of continuous battery-powered illumination on a single charge (10 hours).

By Application:

Applications cover hospitals, specialty clinics, and ambulatory surgical centers. Hospitals hold a significant share due to high patient volumes and the need for fully integrated diagnostic and treatment solutions. Specialty clinics benefit from workstations that enhance patient throughput and offer targeted ENT care. It is also finding increasing use in ambulatory surgical centers where efficiency, portability, and ease of sterilization are essential. Growing outpatient procedures are further expanding demand across all application segments.

Segmentations:

By Technology:

- Conventional

- Advanced Digital

By Product Type:

- Portable ENT Workstations

- Stationary ENT Workstations

By Application:

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

By Region:

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Regional Analysis:

North America :

North America accounts for 38% market share in the ENT workstation market, driven by advanced healthcare infrastructure and high adoption of innovative medical technologies. The region benefits from strong investment in ENT specialty clinics and hospitals, supported by favorable reimbursement frameworks. It is witnessing steady upgrades to digital and AI-enabled workstations that enhance diagnostic precision and workflow efficiency. The presence of leading manufacturers and established distribution networks strengthens market penetration. Continuous training programs for ENT professionals further improve utilization rates of advanced systems. Growing demand for minimally invasive procedures is also shaping product preferences in the region.

Europe :

Europe holds 30% market share in the ENT workstation market, supported by mature healthcare systems and strong regulatory compliance. Countries such as Germany, France, and the UK are key adopters due to their focus on high-quality patient care and efficient clinical workflows. It benefits from extensive use of modular, ergonomic designs that optimize space in ENT units. Government-funded healthcare facilities encourage adoption of technologically advanced solutions. The region’s emphasis on infection control and patient safety is influencing design and material innovations. Increasing prevalence of ENT disorders among aging populations continues to drive equipment demand.

Asia-Pacific :

Asia-Pacific commands 22% market share in the ENT workstation market, fueled by rapid healthcare infrastructure development and growing access to specialty care. China, India, and Japan are emerging as high-growth markets due to rising patient volumes and increased government healthcare spending. It is seeing higher demand for cost-effective yet technologically capable workstations to serve diverse patient segments. The expansion of private healthcare providers is accelerating procurement of advanced diagnostic equipment. Training programs and skill development initiatives are improving the effective use of modern systems. Urbanization and changing lifestyles are contributing to higher ENT disease incidence, further boosting market demand.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- ANA-MED

- Chammed

- ATMOS MedizinTechnik

- dantschke

- Euroclinic Medi-Care Solutions

- Entermed

- Heinemann Medizintechnik

- GAES Medical

- Foshan Gladent Medical

- Global Surgical Corporation

Competitive Analysis:

The ENT workstation market features a competitive landscape driven by innovation, product differentiation, and global expansion strategies. Key players include ANA-MED, Chammed, ATMOS MedizinTechnik, Dantschke, Euroclinic Medi-Care Solutions, and Entermed, alongside several regional manufacturers catering to specific market needs. It is marked by continuous advancements in imaging quality, ergonomic design, and modular configurations to meet diverse clinical requirements. Leading companies focus on integrating digital technologies, enhancing user comfort, and improving infection control features. Strategic partnerships with healthcare providers and distributors strengthen market penetration, while investments in R&D support the development of AI-enabled and telemedicine-ready systems. Pricing strategies vary, with premium brands targeting advanced healthcare settings and cost-efficient models addressing emerging market demand. The competitive environment remains dynamic, with manufacturers striving to balance technological sophistication, regulatory compliance, and affordability to capture a larger share in both developed and developing regions.

Recent Developments:

- In November 2024, Euroclinic Medi-Care Solutions prepared to showcase new medical innovations at MEDICA 2024 in Düsseldorf.

- In May 2025, MD Medical Group acquired Medical Centre Expert (part of the Expert Group network), integrating a network of clinics across 13 cities in Russia to expand diagnostic capacity, with official portfolio integration starting this month.

Market Concentration & Characteristics:

The ENT workstation market is moderately concentrated, with a mix of global manufacturers and regional players competing on technology, design, and service capabilities. It is characterized by continuous innovation, integration of digital imaging, and modular configurations to meet varied clinical needs. Leading companies focus on high-performance systems with enhanced ergonomics, infection control features, and compatibility with advanced diagnostic tools. Mid-tier and regional manufacturers target cost-sensitive segments with simplified yet efficient models. The market shows strong brand loyalty in established healthcare settings, while emerging markets present opportunities for new entrants through localized production and distribution. Regulatory compliance, product reliability, and after-sales support remain critical factors influencing purchasing decisions.

Report Coverage:

The research report offers an in-depth analysis based on Technology, Product Type, Application and Region. It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- Rising prevalence of ENT disorders will continue to drive the demand for advanced diagnostic and treatment solutions.

- Adoption of AI-assisted imaging and diagnostic tools will enhance accuracy and streamline clinical workflows.

- Integration of telemedicine capabilities into portable ENT workstations will expand access to remote and underserved areas.

- Demand for modular and customizable workstation designs will increase to accommodate diverse clinical requirements.

- Healthcare infrastructure development in emerging economies will create significant growth opportunities for manufacturers.

- Growing preference for minimally invasive procedures will shape product innovations with compact, multifunctional designs.

- Use of antimicrobial materials and improved infection control features will gain importance in product design.

- Collaboration between manufacturers and healthcare providers will accelerate the development of specialized ENT solutions.

- Expansion of training programs and technical support will improve equipment utilization rates in new markets.

- Continuous investment in R&D will lead to the launch of advanced, user-friendly, and digitally integrated ENT workstations.