Market Overview

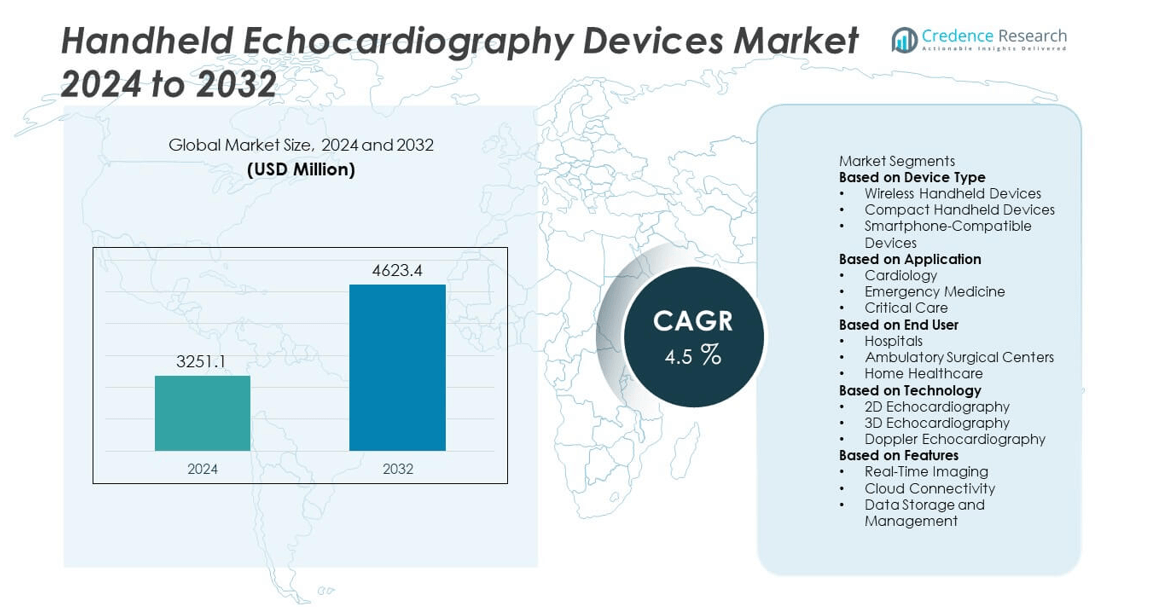

The Handheld Echocardiography Devices Market was valued at USD 3,251.1 million in 2024 and is projected to reach USD 4,623.4 million by 2032, reflecting a CAGR of 4.5% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Handheld Echocardiography Devices Market Size 2024 |

USD 3,251.1 million |

| Handheld Echocardiography Devices Market, CAGR |

4.5% |

| Handheld Echocardiography Devices Market Size 2032 |

USD 4,623.4 million |

The Handheld Echocardiography Devices Market grows due to rising cardiovascular disease prevalence, increasing demand for point-of-care diagnostics, and expanding use in emergency and primary care settings. Technological advancements, including AI integration, enhanced imaging resolution, and wireless connectivity, are improving diagnostic accuracy and efficiency. Growing adoption in telecardiology and remote healthcare delivery supports access in underserved regions. Miniaturization and ergonomic designs enhance portability, while multifunctional capabilities drive wider clinical applications.

North America leads the Handheld Echocardiography Devices Market due to advanced healthcare infrastructure, high adoption of point-of-care imaging, and strong presence of global manufacturers. Europe follows with robust demand driven by preventive cardiology programs and supportive regulatory policies. Asia-Pacific is experiencing rapid growth, fueled by rising healthcare investments, expanding telemedicine infrastructure, and increasing cardiovascular disease prevalence. Latin America and the Middle East & Africa are witnessing gradual adoption through mobile health initiatives and government-supported outreach programs. Key players shaping the market include Philips, known for advanced portable imaging systems; GE Healthcare, offering AI-enabled handheld solutions; Fujifilm, with innovative compact ultrasound platforms; and Mindray, delivering competitively priced, high-performance devices targeting both developed and emerging healthcare markets.

Market Insights

- The Handheld Echocardiography Devices Market was valued at USD 3,251.1 million in 2024 and is projected to reach USD 4,623.4 million by 2032, growing at a CAGR of 4.5% during the forecast period.

- Rising prevalence of cardiovascular diseases, increasing demand for point-of-care diagnostics, and expanding use in emergency and primary care settings are key factors driving market growth.

- Technological advancements such as AI-enabled image analysis, wireless connectivity, and improved probe miniaturization are enhancing diagnostic accuracy and expanding clinical applications.

- The competitive landscape features global leaders including Philips, GE Healthcare, Fujifilm, Mindray, and Chison, focusing on innovation, ergonomic designs, and expanding telecardiology capabilities to gain market share.

- High costs of advanced handheld systems, limited budget allocation in low-resource settings, and operator dependency for accurate diagnosis are restraining widespread adoption.

- North America leads the market due to advanced healthcare infrastructure and strong manufacturer presence, while Asia-Pacific is witnessing the fastest growth driven by rising healthcare investments and growing telemedicine adoption.

- Emerging markets in Latin America and the Middle East & Africa present untapped potential, supported by mobile health initiatives, government outreach programs, and partnerships between local healthcare providers and global device manufacturers.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Prevalence of Cardiovascular Diseases Driving Diagnostic Demand

The Handheld Echocardiography Devices Market benefits from the increasing global burden of cardiovascular diseases. Early detection and continuous monitoring have become critical for reducing morbidity and mortality rates. Handheld devices enable rapid, point-of-care cardiac imaging, facilitating timely intervention. Their compact design and high portability allow use in emergency care, rural clinics, and mobile health units. Growing demand for accessible diagnostics in both developed and developing economies supports wider adoption. It addresses the clinical need for cost-effective and accurate cardiac assessments outside traditional hospital settings.

- For instance, GE Healthcare’s Vscan Air SL maintains up to 50 minutes of scanning time on a full battery—a fully charged device that supports 80% black‑and‑white and 20% color imaging.

Technological Advancements Enhancing Imaging Capabilities

Continuous innovation in handheld echocardiography technology has improved image quality, processing speed, and connectivity features. Manufacturers integrate advanced Doppler imaging, AI-based analysis, and wireless data transfer to enhance diagnostic efficiency. Compact probes now deliver image resolutions comparable to full-sized systems, enabling precise clinical evaluation. These advancements allow healthcare providers to make faster, evidence-based decisions. It supports remote consultations and telecardiology, expanding the reach of cardiac diagnostics. Enhanced battery life and user-friendly interfaces further encourage adoption across various medical specialties.

- For instance, Philips’ Compact Ultrasound 5500CV, launched in March 2025, reduces cardiac exam time by up to 50% through AI-driven automated measurements, while maintaining high diagnostic accuracy comparable to premium cart-based systems, enabling clinicians to complete standard echo protocols in under 10 minutes.

Growing Adoption in Point-of-Care and Emergency Settings

Point-of-care testing in emergency rooms, intensive care units, and ambulances is driving uptake of handheld echocardiography devices. Immediate access to cardiac imaging accelerates triage and treatment decisions, improving patient outcomes. Portable systems reduce the dependency on fixed echocardiography labs, lowering diagnostic delays. Field use in military medicine, disaster response, and rural healthcare underscores their versatility. It enables cardiac assessment in environments where traditional equipment is impractical. Increasing integration into emergency care protocols strengthens their market presence.

Favorable Healthcare Policies and Expanding Access

Government initiatives and institutional policies promoting early cardiac screening support the adoption of handheld echocardiography devices. Training programs and subsidies for portable diagnostic equipment improve accessibility in underserved regions. Public health agencies prioritize investments in mobile and community-based diagnostic solutions. Insurance coverage expansion for portable echocardiography examinations boosts patient access and affordability. It aligns with global strategies to reduce cardiovascular disease burden through early detection. Collaboration between device manufacturers and healthcare systems accelerates market penetration and long-term adoption.

Market Trends

Integration of Artificial Intelligence for Automated Analysis

The Handheld Echocardiography Devices Market is experiencing a strong shift toward AI-enabled diagnostic capabilities. Automated measurement tools assist clinicians in interpreting images with higher accuracy and reduced examination time. AI integration supports early detection of subtle abnormalities, enhancing clinical decision-making. Real-time analysis reduces operator dependency, making the devices suitable for use by general practitioners and not only cardiology specialists. It enables standardized reporting, improving diagnostic consistency across different healthcare settings. The trend aligns with the broader movement toward precision medicine and data-driven healthcare delivery.

- For instance, Philips’ AI-powered Auto Measure HeartQuant, integrated into its Compact Ultrasound 5500CV, can perform fully automated left ventricular volume and ejection fraction measurements in under 15 seconds, with a reported measurement agreement within 2.5 mL for volumes compared to expert manual tracing

Expansion of Telecardiology and Remote Diagnostics

Telemedicine adoption has accelerated the demand for handheld echocardiography devices with remote connectivity features. Secure data transmission enables specialists to review cardiac scans from distant locations. This capability supports continuous patient monitoring and follow-up without requiring frequent hospital visits. Portable devices with cloud integration enhance collaboration between multidisciplinary teams. It offers opportunities for delivering advanced cardiac care in underserved areas. This trend is transforming how cardiac diagnostics are delivered in both acute care and chronic disease management.

- For instance, Philips’ Compact Ultrasound 5500CV allows secure cloud-based data transfer and supports remote expert review in under 60 seconds per scan, enabling cardiologists to provide near real-time feedback to point-of-care teams across different facilities

Advancements in Probe Design and Miniaturization

Manufacturers are focusing on reducing device size while improving image resolution and performance. High-frequency probes provide detailed cardiac imaging while maintaining lightweight and ergonomic designs. Compact devices enhance mobility for clinicians in emergency medicine, home healthcare, and sports medicine. Ergonomic improvements reduce user fatigue during prolonged use. It promotes adoption in non-traditional settings, expanding clinical applications beyond hospital walls. Continuous improvements in portability are redefining operational workflows in cardiovascular care.

Shift Toward Multi-Functional and Cost-Efficient Solutions

Healthcare providers are seeking portable echocardiography devices capable of performing multiple diagnostic functions. Integrated modes, such as color Doppler and 3D imaging, increase the utility of compact systems. Cost-efficient designs help facilities maximize return on investment while maintaining high diagnostic standards. It drives adoption in primary care, outpatient clinics, and developing regions where budget constraints are significant. Manufacturers are competing to deliver feature-rich devices at accessible price points. This trend is fostering wider availability of advanced cardiac imaging technologies globally.

Market Challenges Analysis

High Cost of Advanced Technologies and Limited Budget Allocation

The Handheld Echocardiography Devices Market faces constraints due to the high cost of advanced imaging technologies. Premium models with AI integration, 3D imaging, and wireless connectivity remain unaffordable for many small clinics and rural healthcare facilities. Limited budget allocation in public health systems restricts large-scale procurement, particularly in developing economies. Training expenses and maintenance requirements add to the overall ownership cost. It creates barriers to adoption despite the proven clinical benefits. Without cost-effective manufacturing strategies, price sensitivity will continue to hinder market penetration in low-resource settings.

Operator Dependency and Image Interpretation Limitations

Accurate echocardiographic assessment requires significant training and experience, posing a challenge for broader adoption. Inexperienced operators may generate suboptimal images, leading to potential misdiagnosis or delayed treatment decisions. Variability in image quality across different devices and skill levels reduces diagnostic consistency. It limits the ability to standardize results, especially in remote or primary care environments. Integration of AI-assisted analysis can mitigate these challenges, but adoption remains uneven across healthcare systems. Regulatory requirements for training and certification further slow deployment in new markets.

Market Opportunities

Expanding Role in Primary Care and Preventive Cardiology

The Handheld Echocardiography Devices Market holds significant growth potential through wider adoption in primary care and preventive healthcare programs. Early detection of cardiac conditions at the community level can reduce hospitalization rates and improve long-term outcomes. Portable systems enable routine cardiovascular assessments during general health check-ups. It creates opportunities for integration into public health screening initiatives, particularly in aging populations with high cardiac risk. Collaboration between device manufacturers and primary care networks can accelerate adoption. The shift toward preventive care supports consistent demand for accessible, easy-to-use cardiac imaging tools.

Rising Demand in Emerging Markets and Remote Healthcare Delivery

Emerging economies present strong opportunities for handheld echocardiography device manufacturers due to increasing healthcare investments. Governments and NGOs are funding mobile health units and telemedicine programs to expand cardiac care access in rural regions. Portable echocardiography systems can be deployed in these programs to provide diagnostic capabilities without the need for large infrastructure. It allows clinicians to extend advanced cardiac assessments to underserved populations. Competitive pricing strategies and locally adapted models can strengthen market entry. The growing emphasis on decentralized healthcare will continue to drive adoption in these high-potential regions.

Market Segmentation Analysis:

By Device Type

The Handheld Echocardiography Devices Market is segmented into single-probe and multi-probe systems. Single-probe devices dominate due to their compact design, ease of use, and suitability for quick point-of-care diagnostics. They offer portability and cost efficiency, making them ideal for primary care and emergency settings. Multi-probe devices, while larger, provide enhanced diagnostic versatility with multiple imaging modes and deeper penetration capabilities. It caters to specialized cardiology practices and advanced diagnostic applications. Continuous innovation in probe miniaturization and integration of AI-driven analysis is improving performance across both categories, supporting broader clinical adoption.

- For instance, Chison’s SonoEye handheld device uses a single probe weighing only 150 grams, yet delivers imaging depth up to 305 mm and frame rates exceeding 60 fps, matching the clarity of full-sized cart-based systems.

By Application

The market serves applications such as cardiovascular disease diagnosis, emergency medicine, critical care monitoring, and others. Cardiovascular diagnosis remains the largest segment due to the rising global burden of heart disease and the need for early detection. Emergency medicine increasingly adopts handheld echocardiography for rapid triage in ambulances, field hospitals, and disaster response units. Critical care settings use these devices for continuous monitoring of high-risk patients without transferring them to imaging departments. It enhances efficiency in acute care workflows and supports timely interventions. Expanding use in sports medicine and preoperative assessments is creating new application avenues.

- For instance, GE Healthcare’s Vscan Air SL has been deployed in emergency care units where its dual-probe configuration enables both deep cardiac scans and high-frequency superficial imaging, with each scan completed in under two minutes, reducing triage time for critical patients by up to 40%

By End-User

Key end-users include hospitals, diagnostic centers, and ambulatory care facilities. Hospitals remain the primary users, driven by high patient inflow and the need for advanced cardiac imaging within emergency departments, ICUs, and operating rooms. Diagnostic centers adopt handheld systems to provide quick cardiac assessments alongside other imaging services, improving patient throughput. Ambulatory care facilities, including mobile health units and rural clinics, benefit from the portability and ease of deployment of these devices. It strengthens cardiac care accessibility in underserved areas and supports preventive healthcare programs. The growing demand for decentralized diagnostics is expected to increase penetration across all end-user categories.

Segments:

Based on Device Type

- Wireless Handheld Devices

- Compact Handheld Devices

- Smartphone-Compatible Devices

Based on Application

- Cardiology

- Emergency Medicine

- Critical Care

Based on End User

- Hospitals

- Ambulatory Surgical Centers

- Home Healthcare

Based on Technology

- 2D Echocardiography

- 3D Echocardiography

- Doppler Echocardiography

Based on Features

- Real-Time Imaging

- Cloud Connectivity

- Data Storage and Management

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the largest share of the Handheld Echocardiography Devices Market, accounting for 37.2% in 2024. The region benefits from advanced healthcare infrastructure, high adoption of point-of-care diagnostic technologies, and strong presence of leading manufacturers. The United States leads in usage due to a high prevalence of cardiovascular diseases, well-established reimbursement frameworks, and widespread integration of portable imaging in emergency and critical care. Canada also contributes significantly, with government-funded initiatives aimed at improving access to cardiac diagnostics in remote communities. It remains a key innovation hub, with continuous product development focused on AI integration, wireless connectivity, and telemedicine compatibility. Strong demand from both hospital networks and independent diagnostic centers continues to sustain market leadership in this region.

Europe

Europe represents 29.4% of the global market, driven by increasing demand for mobile diagnostics and preventive cardiology programs. Countries such as Germany, the United Kingdom, and France lead adoption, supported by robust healthcare systems and emphasis on early detection. Regulatory frameworks encouraging the use of portable imaging devices in primary care have further accelerated uptake. It benefits from collaborative research initiatives between universities, hospitals, and manufacturers aimed at enhancing image quality and diagnostic accuracy. Demand in Eastern Europe is growing as healthcare systems modernize and seek cost-efficient diagnostic solutions. Strong focus on reducing hospital congestion by expanding outpatient diagnostic capabilities is also influencing device adoption.

Asia-Pacific

Asia-Pacific accounts for 21.1% of the market, with rapid growth expected due to rising healthcare investments and increasing cardiovascular disease prevalence. China and Japan are leading contributors, with high demand from urban hospitals and expanding telemedicine infrastructure. India and Southeast Asian countries are witnessing accelerated adoption through government health programs and mobile medical units targeting rural populations. It is becoming a critical growth engine for manufacturers offering competitively priced, high-performance devices. Expanding medical training programs and growing private healthcare sectors further support market expansion. Local production partnerships are emerging as a strategy to meet rising demand while addressing cost sensitivities in developing economies.

Latin America

Latin America holds 7.3% of the global market, with Brazil and Mexico leading in adoption. Increasing incidence of heart disease, combined with government-funded health programs, drives demand for portable diagnostic technologies. Rural and underserved communities are major beneficiaries of handheld echocardiography deployment, often through mobile health initiatives. It faces challenges related to budget limitations and uneven healthcare infrastructure, but ongoing investments in telehealth and diagnostic outreach are mitigating these barriers. Training and education programs by manufacturers and NGOs are also expanding the pool of skilled operators, improving diagnostic capabilities across the region.

Middle East & Africa

The Middle East & Africa region represents 5.0% of the market, with adoption concentrated in Gulf Cooperation Council (GCC) countries due to higher healthcare expenditure and modernization efforts. South Africa is a key market in the African segment, supported by targeted investments in mobile healthcare. Portable cardiac imaging devices are increasingly integrated into emergency response and rural outreach programs. It faces infrastructure and cost-related constraints in several sub-Saharan countries, limiting widespread deployment. International aid programs, along with partnerships between local healthcare providers and global manufacturers, are gradually improving access to handheld echocardiography technology across the region.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Chison

- Nihon Kohden

- Medtronic

- Fujifilm

- Sonosite

- GE Healthcare

- Edan Instruments

- Philips

- RIKEN

- Mindray

Competitive Analysis

The competitive landscape of the Handheld Echocardiography Devices Market is shaped by the strategic initiatives of leading players such as Philips, GE Healthcare, Fujifilm, Mindray, Chison, Edan Instruments, Medtronic, Sonosite, Nihon Kohden, and RIKEN. These companies focus on product innovation, technology integration, and expanding their global presence to strengthen market positioning. Philips and GE Healthcare lead with advanced AI-enabled imaging solutions, strong distribution networks, and robust after-sales support, catering to both hospital and point-of-care settings. Fujifilm and Mindray compete through cost-effective, high-performance portable systems designed for diverse clinical applications, particularly in emerging markets. Chison and Edan Instruments leverage affordability and compact designs to penetrate price-sensitive regions, while Medtronic and Sonosite emphasize specialized cardiovascular imaging solutions with enhanced portability and durability. Nihon Kohden and RIKEN contribute with research-driven device enhancements and niche applications in diagnostic imaging. Across the market, competition centers on improving image resolution, expanding telemedicine capabilities, and delivering multifunctional, user-friendly devices that meet the growing demand for decentralized cardiac diagnostics worldwide.

Recent Developments

- In June 2025, it continued its long-term “Project 2025”—an initiative partnering with global institutions to establish over 50 ultrasound training centers.

- In January 2025, Philips introduced a miniaturized intracardiac 3D transducer, enabling real-time imaging inside the heart—even for critically ill or small pediatric patients.

- In September 2024, GE HealthCare introduced the Venue Sprint, a highly portable, AI-enabled ultrasound system. This new device is designed to be a next-generation addition to the Venue family of ultrasound systems, offering wireless probing and AI-powered features.

Market Concentration & Characteristics

The Handheld Echocardiography Devices Market exhibits a moderately concentrated structure, with a mix of established global manufacturers and emerging regional players competing for market share. Leading companies such as Philips, GE Healthcare, Fujifilm Sonosite, Mindray, and Chison dominate through advanced technology integration, strong distribution networks, and broad clinical application coverage. It is characterized by high innovation intensity, with frequent product launches incorporating AI-driven diagnostics, wireless connectivity, and improved probe miniaturization. The market caters to diverse end-users, including hospitals, diagnostic centers, and mobile healthcare providers, driven by the need for portable, high-performance cardiac imaging solutions. Price sensitivity in developing economies encourages the entry of cost-focused manufacturers, while premium segments in developed markets emphasize image quality, multifunctionality, and workflow integration. Regulatory compliance, operator training, and after-sales support play critical roles in competitive differentiation, shaping purchasing decisions across regions.

Report Coverage

The research report offers an in-depth analysis based on Device Type, Application, End-User, Technology, Features and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- AI integration will enhance image interpretation accuracy and reduce operator dependency.

- Wireless connectivity will improve remote diagnostics and telecardiology adoption.

- Miniaturization will increase portability and expand use in non-traditional care settings.

- Multifunctional devices will gain preference for broader clinical applications.

- Preventive cardiology programs will drive demand in primary care and community health.

- Emerging markets will adopt affordable models to expand cardiac care access.

- Battery life improvements will support longer operational hours in field conditions.

- Training initiatives will boost skilled operator availability in underserved regions.

- Collaboration between manufacturers and healthcare systems will accelerate market penetration.

- Regulatory harmonization will streamline global product approvals and reduce time-to-market.