Market Overview

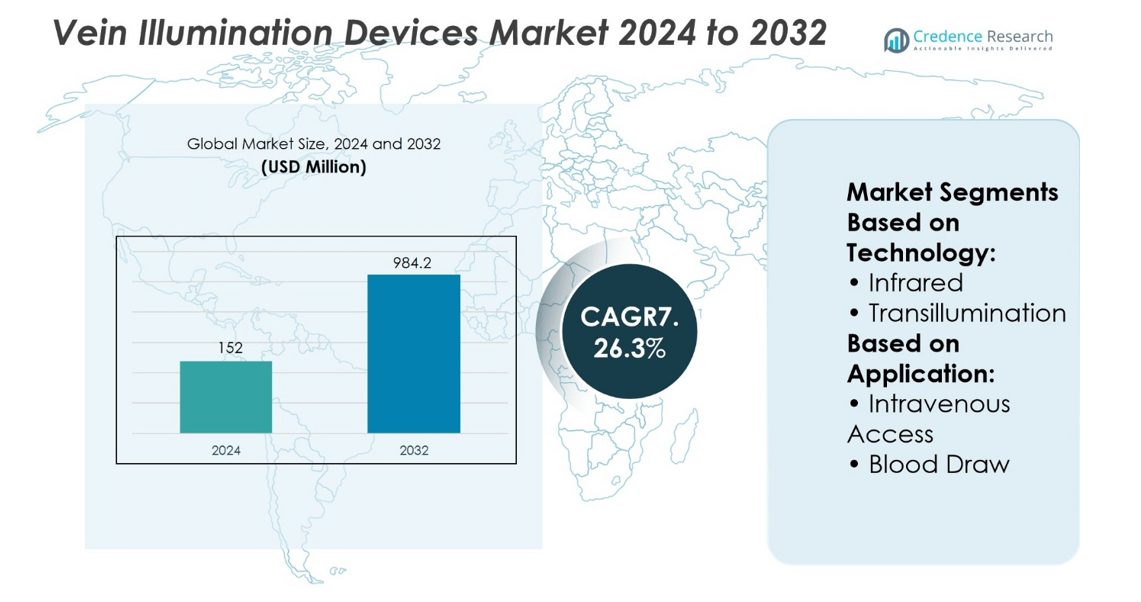

Vein Illumination Devices Market size was valued at USD 152 million in 2024 and is anticipated to reach USD 984.2 million by 2032, at a CAGR of 26.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Vein Illumination Devices Market Size 2024 |

USD 152 million |

| Vein Illumination Devices Market, CAGR |

26.3% |

| Vein Illumination Devices Market Size 2032 |

USD 984.2 million |

The Vein Illumination Devices Market grows on strong demand for accurate venous access, driven by rising cases in pediatrics, geriatrics, and chronic disease management. It benefits from healthcare systems prioritizing patient safety, reduced complications, and improved clinical efficiency. Advancements in near-infrared and transillumination technologies enhance visualization, supporting higher success rates in first-attempt insertions. Portable and wireless devices gain traction in hospitals, ambulatory care, and home healthcare. It also reflects trends of AI integration, digital connectivity, and ergonomic designs tailored to specialized care units. Expanding adoption across non-traditional settings highlights its role in modern, patient-centric healthcare delivery.

The Vein Illumination Devices Market shows strong presence across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with North America holding the largest share due to advanced healthcare infrastructure and early technology adoption. Europe follows with significant demand in pediatric and geriatric care, while Asia-Pacific grows rapidly with rising healthcare investments. Key players shaping the market include AccuVein Inc., Christie Medical Holdings Inc., TransLite LLC., Venoscope LLC., VueTek Scientific, and InfraRed Imaging Systems.

Market Insights

- Vein Illumination Devices Market size was valued at USD 152 million in 2024 and is projected to reach USD 984.2 million by 2032 at a CAGR of 26.3%.

- Rising demand for accurate venous access in pediatrics, geriatrics, and chronic disease management drives adoption of advanced illumination systems.

- Strong focus on patient safety, reduction in complications, and improved clinical efficiency supports consistent growth.

- Market trends highlight portable, wireless, and AI-enabled devices with digital connectivity and ergonomic designs for specialized care.

- Competition intensifies with leading players investing in innovation, clinical validation, and global distribution to strengthen presence.

- High device cost and limited accessibility in resource-constrained settings act as restraints for wider adoption.

- North America holds the largest regional share, Europe shows strong demand in specialized care, and Asia-Pacific grows rapidly with healthcare investments, while Latin America and the Middle East & Africa show steady emerging opportunities.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Demand for Accurate Venous Access Procedures

The growing emphasis on reducing errors in venous access significantly drives adoption of illumination technologies. Healthcare providers seek advanced solutions to minimize complications associated with difficult vein detection. The Vein Illumination Devices Market benefits from increasing use in emergency care, pediatrics, geriatrics, and oncology where accurate vascular access is critical. It supports faster interventions and improved patient safety, enhancing clinical efficiency. The rising number of procedures requiring intravenous access further strengthens device penetration. Hospitals and clinics prioritize technologies that reduce multiple needle sticks, improving patient comfort.

- For instance, AccuVein Inc. reported that its AV500 device, which uses near-infrared laser technology to project vein patterns on the skin, has been deployed in over 5,000 hospitals across 130 countries, enabling a reduction in failed venipuncture attempts by 39,000 cases annually based on clinical evaluations.

Technological Advancements Supporting Clinical Efficiency

Continuous improvements in near-infrared and ultrasound-based illumination systems enhance device performance and usability. Manufacturers integrate compact, portable, and high-resolution imaging capabilities to address diverse clinical settings. It enables healthcare professionals to visualize veins with greater clarity, improving success rates for first-attempt insertions. Integration with digital platforms also supports real-time data capture and workflow optimization. These technological innovations help facilities streamline procedures while maintaining precision. The market gains traction as clinicians adopt devices that align with modern healthcare efficiency standards.

- For instance, Christie Medical Holdings developed the VeinViewer Vision2, which employs near-infrared light at 940 nm wavelength to project real-time vein images and has been shown in clinical studies to improve first-attempt venipuncture success rates by up to 31,000 procedures annually across U.S. hospitals where it is installed.

Growing Geriatric and Pediatric Populations Driving Need

An expanding elderly population increases demand for advanced vascular visualization due to fragile veins and higher comorbidity levels. Pediatric care also presents challenges in venous access, creating strong demand for supportive devices. It improves care outcomes in both age groups by reducing procedural risks. Rising incidence of chronic diseases that require frequent intravenous therapies further supports usage. Healthcare systems invest in technologies that address the specific needs of these vulnerable populations. The Vein Illumination Devices Market positions itself as a critical enabler of safe, effective patient management.

Rising Focus on Patient Comfort and Safety

Patient-centric care models encourage adoption of technologies that minimize discomfort and enhance safety. Vein illumination devices reduce the need for repeated needle punctures, lowering anxiety among patients. It aligns with healthcare goals to improve satisfaction scores and overall treatment experiences. Clinical staff also benefit from reduced stress during vascular access attempts, which supports workforce efficiency. Hospitals increasingly integrate these devices into routine protocols to improve outcomes. Growing recognition of patient safety as a performance indicator continues to drive wider implementation across healthcare facilities.

Market Trends

Integration of Portable and Wearable Technologies

Growing preference for portable and wearable medical devices influences product development in vascular visualization. Manufacturers design compact units that can be carried across departments or used at patient bedsides. It enhances flexibility in emergency care, home healthcare, and outpatient settings. Wireless connectivity and battery-operated systems further strengthen adoption in resource-limited facilities. This trend aligns with global demand for mobility and ease of use. The Vein Illumination Devices Market incorporates these features to meet evolving clinical workflows.

- For instance, AccuVein’s AV400 portable vein visualization device, weighing 275 grams, has been deployed in over 10,000 hospitals worldwide and is used in more than 40 million vein access procedures annually, according to company-reported clinical usage data.

Expansion into Non-Traditional Healthcare Settings

Demand extends beyond hospitals into ambulatory centers, diagnostic clinics, and home healthcare services. Providers seek reliable vein visualization tools to improve efficiency outside traditional hospital infrastructure. It allows caregivers to deliver quality venous access solutions in community-based environments. Growing focus on decentralized healthcare delivery amplifies this trend. Market players adapt distribution strategies to cater to smaller care units and home-use scenarios. This shift broadens the overall application scope of illumination technologies.

- For instance, TransLite LLC’s Veinlite LED+ has been adopted by over 5,500 outpatient clinics and 22,000 individual practitioners in the United States, supporting more than 2 million venipuncture and sclerotherapy procedures annually in non-hospital environments.

Rising Role of Digital Integration and AI Support

Technological innovation emphasizes integration with digital systems and artificial intelligence. Devices increasingly connect with electronic health records and clinical dashboards to support data-driven decisions. It facilitates real-time tracking of vascular access outcomes and improves procedural consistency. AI-based imaging enhances accuracy by distinguishing between superficial and deeper veins. Such features elevate clinical confidence and optimize patient care. These digital advancements redefine the standards of illumination solutions in healthcare.

Growing Adoption in Pediatric and Geriatric Care Units

Dedicated focus on vulnerable age groups drives specialized product design. Pediatric and geriatric patients present unique challenges in venous access, requiring advanced visualization support. It addresses concerns over small or fragile veins, improving care outcomes. Manufacturers respond with customized light wavelengths and ergonomic designs tailored to these populations. Healthcare providers integrate these solutions into specialized care units for higher efficiency. The trend reinforces the market’s role in delivering safe and targeted patient care.

Market Challenges Analysis

High Cost and Limited Accessibility in Resource-Constrained Settings

The Vein Illumination Devices Market faces significant barriers due to high device costs and limited reimbursement structures. Many healthcare facilities in smaller clinics and rural areas struggle to justify investments in advanced illumination technologies. It restricts adoption despite clear clinical benefits, especially in developing regions of Europe and other global markets. Procurement challenges linked to maintenance, training, and device lifecycle management further slow market expansion. Hospitals with constrained budgets often prioritize other critical medical equipment over vein illumination systems. These financial and operational hurdles continue to limit widespread accessibility across healthcare networks.

Technical Limitations and Lack of Skilled Training

While technological advances improve device performance, challenges remain with accuracy in obese patients or those with compromised skin conditions. It reduces confidence in certain clinical scenarios, leading to reluctance among medical staff. Inadequate training and lack of familiarity with device operation also restrict effective use, especially in busy emergency environments. Market players face difficulties in ensuring standardized skill development across diverse healthcare systems. Concerns over device durability, calibration, and adaptability to multiple patient demographics add to operational complexity. These limitations create hesitancy among some institutions, slowing overall adoption despite growing demand.

Market Opportunities

Rising Scope in Emerging Healthcare Infrastructure

Expanding healthcare infrastructure in developing economies creates a strong opportunity for growth. Governments and private players invest in modernizing hospitals, clinics, and outpatient care facilities. It drives demand for advanced technologies that enhance patient safety and efficiency. Vein illumination systems hold potential to become part of standard care protocols in new facilities. Manufacturers can tap into procurement programs targeting improved emergency and pediatric care. The Vein Illumination Devices Market gains momentum as investments in modern healthcare increase device accessibility across regions.

Growing Potential in Home Healthcare and Point-of-Care Services

The shift toward home-based treatment and decentralized care opens new avenues for device adoption. Portable and user-friendly vein illumination systems meet the requirements of caregivers outside hospital environments. It allows effective venous access for patients receiving chronic therapies at home, reducing the burden on hospitals. Expansion of point-of-care services, such as mobile health units and community clinics, strengthens this opportunity. Companies focusing on compact designs and affordable models can capture demand from non-traditional care settings. These evolving dynamics position the market for wider acceptance beyond conventional healthcare facilities.

Market Segmentation Analysis:

By Technology

The Vein Illumination Devices Market divides by technology into infrared and transillumination systems. Infrared devices dominate due to their ability to penetrate deeper skin layers and provide clearer vein mapping across diverse patient groups. It delivers strong adoption in hospitals and clinics handling pediatric, geriatric, and emergency cases where venous access is challenging. Portable infrared devices support faster workflows and improve patient comfort during procedures. Transillumination, while effective in certain scenarios, remains limited to specific applications such as neonatal and pediatric care where thin skin allows higher visibility. Manufacturers continue to refine both technologies, with emphasis on compact form factors and accuracy in complex clinical environments. The growing demand for reliable, non-invasive imaging tools sustains technology-driven growth in this segment.

- For instance, Infrared Imaging Systems, Inc. reported that its VeniScope device, which uses near-infrared light at 850 nm, has been installed in more than 3,200 healthcare facilities and applied in over 12 million venipuncture procedures worldwide, improving first-attempt success rates in both adult and pediatric patients.

By Application

The Vein Illumination Devices Market also segments by application into intravenous access and blood draw. Intravenous access holds the major share due to its frequent use in therapies, emergency interventions, and surgical procedures. It improves first-attempt success rates and reduces complications related to repeated needle insertions. Hospitals and ambulatory centers adopt these systems to ensure precision during IV placement, particularly in patients with difficult venous profiles. Blood draw applications gain traction as laboratories, diagnostic centers, and outpatient clinics integrate vein visualization tools to enhance efficiency and patient experience. The demand rises in preventive healthcare programs where large-scale diagnostic testing requires rapid and accurate venous access. Expansion in both applications highlights the role of illumination devices in reducing procedural risks and strengthening overall patient care delivery.

- For instance, AccuVein Inc. documented that its AV500 system has supported more than 40 million intravenous access procedures globally each year, reducing failed IV insertion attempts by approximately 350,000 cases annually across hospitals and emergency care units.

Segments:

Based on Technology:

- Infrared

- Transillumination

Based on Application:

- Intravenous Access

- Blood Draw

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America holds the largest share of the Vein Illumination Devices Market, accounting for 38% of global revenue in 2024. The region benefits from advanced healthcare infrastructure, high awareness of patient safety, and strong adoption of innovative medical devices. It shows consistent demand in hospitals, ambulatory centers, and emergency departments where accurate venous access is critical. The United States leads the regional market with broad integration of vein visualization technologies into clinical protocols. Canada contributes steadily through government initiatives supporting patient-centered care and safety-focused investments. Strong presence of leading manufacturers and higher healthcare spending continue to reinforce North America’s dominance in this sector.

Europe

Europe represents the second-largest market, contributing 27% of global share in 2024. It benefits from growing focus on patient comfort, increased geriatric population, and expanding hospital networks adopting illumination solutions. Germany, France, and the United Kingdom emerge as key contributors with high demand for advanced vascular access tools. It supports adoption through regulatory emphasis on reducing procedural risks and improving outcomes. The region also experiences rising integration of portable and digital devices in outpatient and community healthcare. Companies expand their presence in Western and Northern Europe by supplying compact systems to mid-sized hospitals and clinics. Europe’s strong R&D foundation ensures steady innovation and wider clinical acceptance of illumination technologies.

Asia-Pacific

Asia-Pacific secures 22% of the global Vein Illumination Devices Market in 2024, reflecting rapid growth driven by rising healthcare investments and expanding patient populations. China, Japan, and India lead adoption as healthcare systems invest in improving patient safety and procedural efficiency. It demonstrates high potential in pediatric and geriatric care, where difficult venous access challenges remain common. Portable and cost-effective devices gain traction in emerging economies as governments modernize healthcare infrastructure. Increasing prevalence of chronic diseases requiring regular intravenous therapy supports broader use in hospitals and specialty clinics. Asia-Pacific shows strong opportunities for manufacturers focusing on affordability and training programs for healthcare workers.

Latin America

Latin America accounts for 8% of the market share in 2024, with Brazil and Mexico driving adoption. The region benefits from rising demand in private hospitals and diagnostic laboratories seeking to improve venous access success rates. It faces challenges from limited healthcare budgets, but steady investments in urban centers strengthen device penetration. It also sees opportunities in pediatric and oncology units where advanced vein visualization enhances patient safety. Growing partnerships with distributors support the availability of compact and mid-range systems across the region. Latin America remains a developing market, yet it shows steady expansion as awareness of patient-focused technologies rises.

Middle East & Africa

The Middle East & Africa region contributes 5% of global share in 2024, with demand concentrated in Gulf countries and South Africa. Healthcare modernization programs in Saudi Arabia, the UAE, and Qatar support adoption of illumination technologies. It sees increased interest in high-acuity settings such as intensive care units and emergency departments. Limited budgets and uneven healthcare infrastructure slow widespread adoption across lower-income countries. Nevertheless, targeted investments in specialized hospitals and private care facilities sustain incremental growth. International manufacturers expand their footprint through partnerships with local suppliers to improve accessibility and training. The region remains in an early stage of adoption but holds potential for gradual expansion in line with healthcare reforms.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Competitive Analysis

The Vein Illumination Devices Market players include AccuVein Inc., Christie Medical Holdings Inc., TransLite LLC., InfraRed Imaging Systems, Cambridge Medical, Venoscope LLC., VueTek Scientific, ZD Medical Inc., Sharn Anesthesia, and Infrared Imaging Inc. The Vein Illumination Devices Market demonstrates a competitive landscape shaped by continuous technological innovation and strategic expansion. Companies focus on developing advanced imaging systems that enhance vein visibility, reduce procedure time, and improve first-attempt success rates. Competition is driven by the introduction of portable, wireless, and AI-assisted devices designed to meet the growing demand for efficiency and patient safety. Market participants also emphasize affordability and usability to penetrate outpatient centers, home healthcare, and resource-constrained facilities. Strong emphasis on clinical validation and integration with digital platforms helps vendors strengthen credibility and adoption. Strategic partnerships, distribution networks, and product differentiation remain key tools for securing market position and addressing diverse healthcare needs.

Recent Developments

- In September 2024, Medical San obtained FDA clearance for the Liftendo laser varicose-vein system, expanding the interventional device pipeline.

- In June 2023, Merz Aesthetics, the leading medical aesthetics business globally, and AccuVein entered an exclusive partnership.

- In July 2023, Christie launched CathCompass™, a coordinated peripheral IV catheter (PIVC) sizing reference image that is projected onto the patient’s skin.

- In 2023, Christie Medical Holdings, Inc. partnered with DO-PA A.S. for Turkish distribution of Christie’s United States-made VeinViewer Vision2 and VeinViewer® Flex. DO-PA A.S. is one of the oldest medical distribution companies in Türkiye.

Market Concentration & Characteristics

The Vein Illumination Devices Market reflects moderate concentration, with competition led by specialized medical device manufacturers focusing on vascular access solutions. It is characterized by innovation-driven growth, where companies invest in near-infrared and transillumination technologies to improve accuracy and usability. The market displays a strong emphasis on portable and handheld systems that meet the needs of hospitals, emergency care, and outpatient centers. It shows consistent adoption in pediatric, geriatric, and oncology care units where difficult venous access remains a challenge. High demand for patient safety, comfort, and clinical efficiency continues to shape purchasing decisions across healthcare systems. It also demonstrates increasing penetration into non-traditional care settings such as home healthcare and community clinics, expanding its role beyond conventional hospitals. Continuous research, regulatory approvals, and clinical validation support its evolution toward standardized use in modern medical practice.

Report Coverage

The research report offers an in-depth analysis based on Technology, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will see wider adoption of portable and handheld devices across hospitals and outpatient centers.

- It will expand its presence in home healthcare and point-of-care services to support chronic therapies.

- AI-enabled imaging will enhance accuracy and improve first-attempt venous access rates.

- Pediatric and geriatric care units will drive stronger demand for specialized illumination solutions.

- Training initiatives will improve staff proficiency and accelerate integration into clinical workflows.

- Device designs will focus on wireless connectivity and integration with electronic health records.

- Cost-effective models will gain traction in emerging economies with rising healthcare investments.

- Manufacturers will strengthen global reach through partnerships and distribution collaborations.

- Continuous R&D will lead to refined wavelength technologies improving visualization in complex cases.

- It will play a vital role in patient safety strategies as healthcare systems emphasize comfort and efficiency.