Market Overview

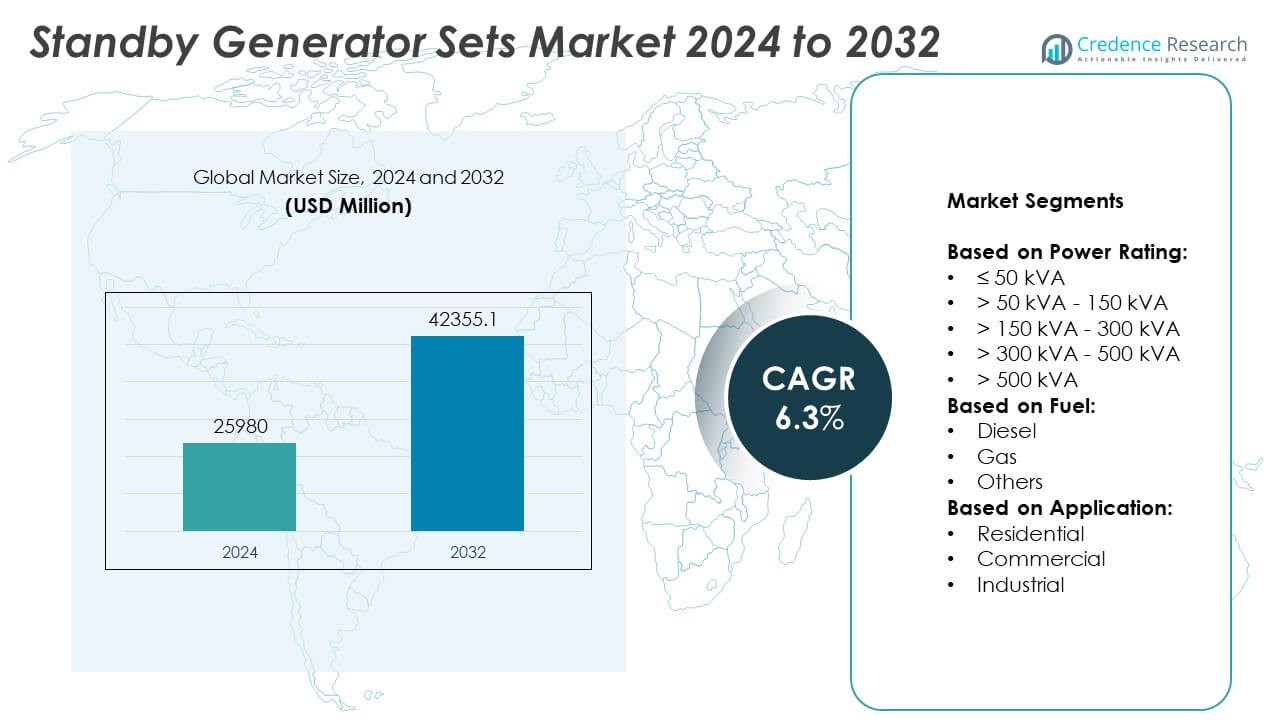

Standby Generator Sets Market size was valued at USD 25,980 million in 2024 and is anticipated to reach USD 42,355.1 million by 2032, at a CAGR of 6.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Standby Generator Sets Market Size 2024 |

USD 25,980 Million |

| Standby Generator Sets Market, CAGR |

6.3% |

| Standby Generator Sets Market Size 2032 |

USD 42,355.1 Million |

The Standby Generator Sets market advances due to rising power outages, aging grid infrastructure, and the critical need for uninterrupted power across data centers, healthcare, telecom, and industrial sectors. Urbanization, infrastructure growth, and climate-related disruptions further accelerate adoption. Smart features such as remote monitoring, predictive diagnostics, and fuel-efficient systems gain popularity among commercial and residential users. Demand for low-emission and gas-powered units grows amid tightening environmental regulations.

Asia-Pacific leads the Standby Generator Sets market due to rapid industrialization, infrastructure growth, and frequent power disruptions across countries like China, India, and Indonesia. North America follows with strong adoption in commercial and residential sectors, supported by weather-related outages and technological advancements. Europe sees consistent demand driven by regulatory compliance and urban power security needs. Key players operating globally include Caterpillar, Cummins, Generac Power Systems, and Rolls-Royce, all offering diversified portfolios across multiple power ratings and fuel types.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Standby Generator Sets market was valued at USD 25,980 million in 2024 and is projected to reach USD 42,355.1 million by 2032, growing at a CAGR of 6.3%.

- Grid instability, climate-induced outages, and infrastructure development drive strong demand across industrial, commercial, and residential sectors.

- Adoption of gas-powered, low-emission, and remote-monitored generator sets reflects a clear shift toward cleaner and smarter power solutions.

- Leading companies like Caterpillar, Cummins, Generac, and Rolls-Royce focus on emission compliance, hybrid systems, and digital diagnostics to strengthen market position.

- Regulatory restrictions on diesel emissions and high operational costs challenge adoption in urban areas and push users to explore alternatives.

- Asia-Pacific dominates due to large-scale industrialization and electrification needs, followed by North America and Europe with strong commercial and technological adoption.

- Latin America and the Middle East & Africa show steady growth driven by telecom expansion, infrastructure gaps, and remote power applications.

Market Drivers

Rising Demand for Reliable Backup Power in Critical Infrastructure

The growth of data centers, hospitals, and communication networks intensifies the demand for continuous power supply. Any interruption in operations can result in service failure, safety risks, or financial losses. Standby generator sets play a vital role in ensuring seamless power availability in such environments. Governments and private sectors prioritize emergency power preparedness, further driving installation volumes. The Standby Generator Sets market benefits from strong adoption across healthcare, IT, and defense sectors. It supports business continuity and disaster recovery efforts. Market expansion aligns with the global rise in mission-critical infrastructure.

- For instance, Generac Power Systems supplied over 20,000 standby generator units to U.S. healthcare facilities in 2024, including advanced monitoring capability through its Mobile Link™ platform.

Frequent Grid Failures and Power Outages Driving Deployment

Aging grid infrastructure, extreme weather events, and rising electricity demand contribute to widespread grid instability. Businesses and households face increasing risks of blackouts, prompting backup power investments. Standby generator sets provide an immediate and reliable solution for minimizing downtime. It enables users to maintain essential operations during grid failures. The Standby Generator Sets market responds to the need for resilient energy systems. Urban and industrial areas with weak utility networks represent key growth areas. Consumers view backup power as a necessity rather than a luxury.

- For instance, Cummins Inc. deployed more than 9,000 diesel-powered standby generators across commercial and residential projects in Texas during the winter outages. These generators were deployed to ensure a reliable power supply during a period of significant energy disruptions

Industrialization and Construction Growth in Emerging Economies

Rapid industrialization across Asia-Pacific, Africa, and Latin America creates high energy demands and stresses on local grids. Construction of manufacturing hubs, commercial buildings, and infrastructure projects fuels demand for temporary and backup power sources. Standby generator sets address both planned and unplanned outages at industrial and construction sites. It ensures uninterrupted operation of machinery, safety systems, and construction schedules. The Standby Generator Sets market sees strong growth in these regions due to infrastructure gaps. Government incentives and industrial policy reforms further support equipment purchases.

Expanding Energy Access and Off-Grid Applications

Many rural and semi-urban regions still lack reliable grid connectivity. In these locations, standby generator sets serve as the primary or secondary power source for homes, schools, clinics, and small enterprises. Off-grid installations contribute significantly to market volume in energy-deficient areas. It enables economic activity and social development where conventional power is absent or unstable. The Standby Generator Sets market gains momentum from electrification efforts and rural energy programs. NGOs, government bodies, and micro-utilities support the deployment of decentralized power solutions.

Market Trends

Integration of Remote Monitoring and Smart Control Systems

Manufacturers integrate IoT-based monitoring and control features into standby generator sets to improve operational efficiency. Smart technologies allow users to track fuel levels, load performance, runtime, and fault diagnostics from remote locations. These systems reduce unplanned downtime and optimize maintenance schedules. It enables centralized control across multiple generator units deployed in different sites. The Standby Generator Sets market aligns with the broader trend of digitization and predictive asset management. Connectivity features increase appeal among commercial and industrial users. Operators seek advanced features that offer both performance transparency and long-term cost savings.

- For instance, Kirloskar Oil Engines Ltd. delivered over 4,500 units above 250 kVA across infrastructure projects in India’s eastern region under government industrial corridor schemes.

Adoption of Low-Emission and Biofuel-Compatible Generator Sets

Tightening emission norms and customer preference for sustainable solutions drive demand for low-emission generator sets. Manufacturers invest in R&D to develop engines compatible with biodiesel, natural gas, and hybrid systems. These fuel-flexible models support environmental compliance without sacrificing reliability. It positions companies to address the needs of both developed and developing markets with varied regulatory requirements. The Standby Generator Sets market sees a gradual shift from traditional diesel-only units to greener alternatives. Public institutions and large corporates lead this transition. Product innovation in combustion and filtration technologies supports the trend.

- For instance, Rolls-Royce introduced its mtu Series 4000 L64 gas-powered generator set, delivering 1,400 kW of standby power with NOx emissions reduced below 250 mg/Nm³.

Growth in Residential Backup Generator Demand Due to Climate Instability

Unpredictable weather events, including hurricanes, floods, and wildfires, trigger higher adoption of residential standby generators. Homeowners invest in permanent backup systems to safeguard their homes and maintain essential functions during power interruptions. Rising awareness of climate-induced disruptions influences purchase decisions. It prompts suppliers to design compact, quiet, and aesthetically compatible systems for urban households. The Standby Generator Sets market responds with customized residential solutions that meet varied capacity and installation needs. Consumer preference shifts toward fully automated transfer systems. Suppliers cater to this niche with plug-and-play and mobile app-compatible units.

Expansion of Rental and Mobile Generator Business Models

Temporary power solutions gain popularity in events, disaster recovery, mining, and infrastructure development sectors. Rental companies expand their fleet of mobile standby generators to meet demand from short-term and seasonal users. It provides cost flexibility to customers who require backup power without permanent installation. The Standby Generator Sets market supports this trend with robust, towable, and weather-resistant units. Manufacturers collaborate with rental providers to offer scalable and maintenance-ready systems. The rental segment grows in parallel with the infrastructure boom and emergency service readiness efforts.

Market Challenges Analysis

Stringent Emission Regulations and Environmental Compliance Barriers

Tightening global emission regulations challenge manufacturers of standby generator sets, particularly those dependent on diesel. Regulatory bodies enforce limits on nitrogen oxides (NOx), particulate matter, and carbon emissions, which require costly design modifications and advanced after-treatment systems. It forces companies to reengineer engines and integrate emission control technologies, increasing production complexity and price. The Standby Generator Sets market faces resistance in urban areas where air quality laws restrict the use of conventional fossil-fuel-based units. Product approvals and certifications also vary by region, slowing time-to-market for new models. Compliance costs impact small and mid-size manufacturers more severely than large global players.

High Operational Costs and Shift Toward Alternative Backup Technologies

Fuel expenses, periodic maintenance, and component replacements contribute to high total ownership costs over the generator’s lifespan. In regions with volatile fuel prices or limited service networks, operating standby generator sets becomes financially burdensome. It encourages customers to explore solar-plus-battery systems or grid-tied energy storage as cleaner and cost-effective alternatives. The Standby Generator Sets market sees competition from emerging technologies offering silent, emission-free, and lower-maintenance solutions. Long-term return on investment becomes a decisive factor for buyers. Market players must address the gap between traditional reliability and evolving economic expectations.

Market Opportunities

Rising Infrastructure Investments and Energy Security Initiatives

Governments across emerging economies invest heavily in infrastructure development, including transportation networks, healthcare facilities, industrial parks, and public utilities. These projects require dependable backup power to ensure uninterrupted execution and long-term operation. Standby generator sets serve as essential support systems during both construction and post-completion phases. It enables resilience where grid reliability remains uncertain. The Standby Generator Sets market finds strong opportunity in public-private infrastructure partnerships and smart city programs. Demand extends across sectors such as metro rail, airports, logistics hubs, and government buildings. Suppliers benefit from multi-year procurement contracts tied to national development agendas.

Expansion of Telecom, Data Centers, and Remote Connectivity Zones

The global surge in digital services, cloud computing, and 5G deployment drives continuous expansion of telecom towers and data centers. These facilities require uninterrupted power to meet uptime guarantees and operational stability. Standby generator sets offer a scalable and reliable solution for both urban installations and remote connectivity zones. It supports network continuity in areas where renewable integration or battery systems face limitations. The Standby Generator Sets market gains momentum from rapid digitization in both developed and underserved regions. Rural broadband rollouts and last-mile connectivity projects create new demand pockets. Providers offering compact, low-noise, and fuel-flexible units hold a competitive edge.

Market Segmentation Analysis:

By Power Rating:

Standby generators rated between > 50 kVA and 150 kVA dominate installations across healthcare facilities, small industries, commercial buildings, and construction sites. These units offer a strong balance between performance, portability, and fuel efficiency. The ≤ 50 kVA segment caters to residential and small office backup needs, where compact size and low noise are prioritized. Generators in the > 150 kVA – 300 kVA and > 300 kVA – 500 kVA ranges serve mid-sized factories, data centers, and institutional facilities with higher load requirements. The > 500 kVA category addresses large-scale industrial complexes, refineries, and infrastructure projects with critical power needs. The Standby Generator Sets market reflects growing adoption across all power bands to meet specific operational risks and power continuity standards.

- For instance, Himoinsa added a new production center in Spain in late 2023 with the capacity to manufacture 7,000 units per year, supporting its growth in sizable generator ratings and diversified applications

By Fuel:

Diesel generators continue to lead due to their power reliability, widespread availability, and cost-effective performance in high-load applications. Industrial and commercial users favor diesel units for their quick startup and operational resilience. Gas-powered generators gain market share driven by regulatory support for cleaner fuels and lower emissions. It appeals to users in urban zones, hospitality, and healthcare sectors with access to piped natural gas. The “Others” segment, including biodiesel, dual-fuel, and propane variants, addresses eco-conscious users and niche operational conditions. Fuel selection influences total cost of ownership, installation viability, and environmental compliance strategy.

- For instance, Briggs & Stratton Energy Solutions enhanced its 26 kW PowerProtect™ home standby generator in May 2024, offering 65.6 kVA motor‑starting capacity—about 68 percent.

By Application:

Industrial applications hold the largest share due to the need for continuous operations in energy-intensive sectors like manufacturing, mining, and logistics. These facilities depend on high-capacity standby systems to prevent costly disruptions. Commercial users rely on generator sets for backup in hospitals, telecom infrastructure, educational institutions, and retail hubs where operational uptime is essential. It ensures safety, service continuity, and regulatory adherence during grid outages. Residential demand grows in response to rising climate-related disruptions and urban grid instability. The Standby Generator Sets market evolves with tailored solutions that match end-user expectations across diverse applications.

Segments:

Based on Power Rating:

- ≤ 50 kVA

- > 50 kVA – 150 kVA

- > 150 kVA – 300 kVA

- > 300 kVA – 500 kVA

- > 500 kVA

Based on Fuel:

Based on Application:

- Residential

- Commercial

- Industrial

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America accounts for 28.4% of the global Standby Generator Sets market, driven by strong adoption across commercial, residential, and industrial sectors. The United States leads the regional market with high demand from healthcare, data centers, and telecommunications facilities, where uninterrupted power is critical to operations. Frequent extreme weather events such as hurricanes and winter storms increase deployment across households and emergency services. Businesses in Canada and the U.S. invest in backup solutions to comply with safety codes and insurance requirements. It also supports public infrastructure resilience planning, especially in energy-sensitive sectors. Technological advancements in natural gas-powered generators, remote monitoring, and hybrid systems further stimulate market penetration. The region also benefits from a mature service ecosystem and strong manufacturer presence, including Tier I players offering integrated energy solutions.

Europe

Europe holds 22.7% of the Standby Generator Sets market, supported by its diversified industrial base and emphasis on power security. Countries such as Germany, France, the UK, and Italy experience steady deployment of standby systems in commercial complexes, logistics centers, and government institutions. Frequent updates to environmental regulations have accelerated the transition toward low-emission generator technologies, including gas and dual-fuel variants. It drives investments in sustainable and noise-compliant solutions, particularly in urban centers. Aging grid infrastructure and grid decentralization strategies further contribute to market growth. The rise in data-driven infrastructure, including cloud hubs and telecom towers, adds new demand channels across the region. Suppliers offering EU Stage V-compliant units and smart control systems gain a competitive edge in this regulated environment.

Asia-Pacific

Asia-Pacific leads the global market with a share of 33.9%, fueled by rapid industrialization, expanding infrastructure, and increasing energy insecurity. China, India, Japan, Indonesia, and South Korea serve as the region’s major growth engines. Power outages caused by overburdened grids, rural electrification gaps, and weather volatility drive the widespread adoption of standby generator sets. It finds robust use in manufacturing plants, commercial buildings, telecom towers, and healthcare facilities. Urban population growth and infrastructure investments under smart city and energy security programs add further momentum. Government incentives, rising construction of industrial corridors, and public-private infrastructure projects contribute to long-term market strength. Local and international players compete with cost-competitive and customized models suitable for high-temperature, dust-prone, or remote environments.

Latin America

Latin America contributes 8.1% to the global Standby Generator Sets market, with Brazil and Mexico accounting for the largest share. Frequent grid disturbances, low electrification in remote zones, and increasing investments in mining, oil & gas, and logistics infrastructure support generator demand. It enables operational continuity in sectors prone to natural disasters or regulatory constraints. Telecommunication providers and small industrial units also deploy backup power systems for service reliability. The commercial sector, including banks and medical facilities, shows growing preference for compact and low-maintenance units. The market sees gradual introduction of gas-based and hybrid models driven by sustainability concerns and regional gas availability.

Middle East & Africa

The Middle East & Africa region holds a 6.9% share, anchored by critical demand in oil and gas operations, utilities, and construction. Countries like Saudi Arabia, the UAE, South Africa, and Nigeria represent key deployment centers due to infrastructure expansion and frequent voltage instability. It supports emergency response networks, hospitality, public utilities, and commercial buildings in urban growth corridors. Off-grid applications in remote mining sites and semi-urban settlements further reinforce demand. Growth in the data center segment and healthcare infrastructure across Gulf nations adds to long-term opportunity. Governments increasingly promote fuel-efficient technologies, which encourages procurement of gas-based standby units. The market remains price-sensitive, with strong potential for hybrid solutions in locations with limited grid access.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Gillette

- Rhelko

- Himoinsa

- Wartsila

- JCB

- Briggs and Stratton

- MAHINDRA POWEROL

- Hipower

- Rolls-Royce

- Yamaha Motor

- Cummins

- Generac Power Systems

- Atlas Copco

- Powerica

- Eaton

- Ashok Leyland

- Kirloskar

- Caterpillar

Competitive Analysis

The leading players in the Standby Generator Sets market include Caterpillar, Cummins, Generac Power Systems, Rolls-Royce, Atlas Copco, Briggs and Stratton, Wartsila, Himoinsa, Kirloskar, MAHINDRA POWEROL, Ashok Leyland, Eaton, JCB, Hipower, Gillette, Yamaha Motor, Rhelko, and Powerica.These companies compete on technological innovation, fuel efficiency, product reliability, and service network strength. Market leaders invest in R&D to enhance remote monitoring capabilities, emission compliance, and hybrid fuel compatibility. They offer a wide range of generator sets tailored for residential, commercial, and industrial applications. Global players maintain competitive advantage through vertical integration, extensive dealer networks, and multi-region manufacturing facilities. Regional companies focus on cost-effective solutions and application-specific designs suited to local grid conditions and fuel availability. Partnerships with infrastructure developers, telecom operators, and public sector agencies help secure long-term contracts. Sustainability remains a key differentiator, with manufacturers introducing low-emission models and gas-powered alternatives. Customization, after-sales support, and product scalability are essential factors influencing buyer preferences. The market remains fragmented with a mix of global OEMs and region-focused suppliers addressing diverse operational and regulatory requirements. Competitive intensity increases as users demand smarter, quieter, and environmentally compliant solutions, pushing firms to innovate and expand their market footprint.

Recent Developments

- In August 2025, Caterpillar launched the Cat® D1500 diesel generator set delivering 1.5 MW of standby power with reduced footprint and weight. It also supports remote monitoring via web or mobile interfaces

- In June 2024, Cummins has earned the bronze award in the power category at Consulting Specifying Engineer’s 2024 product of the year awards for its 125kW-200kW natural gas standby generators (QSJ8.9G). This marks the fourth consecutive year that Cummins has been recognized by CSE for its excellence in power generation. These generators are engineered to meet the rigorous codes, and compliance needs of our customers, furthering our mission to serve both the industry and the planet.

- In July 2023, Rhelko has introduced its 26 kW air-cooled home standby generator, (26RCA) in order to expand its lineup of air-cooled backup power solutions for residential applications, now covering a range from 6 kW to 26 kW. The 26RCA model offers fully automated operation, utilizing the home’s natural gas or propane supply to provide continuous power during outages. This new generator ensures homeowners a reliable, low-maintenance backup power option, offering peace of mind, while giving dealers and partners a complete solution to meet the increasing demand for residential energy security.

Market Concentration & Characteristics

The Standby Generator Sets market exhibits moderate to high concentration, with a mix of global OEMs and strong regional manufacturers shaping competition. Leading players control significant market share through diversified product portfolios, global supply chains, and robust service networks. It remains highly technology-driven, where innovation in emissions compliance, digital monitoring, and fuel flexibility differentiates offerings. The market favors companies that provide scalable solutions across power ratings and end-user segments. Price sensitivity in emerging regions coexists with demand for premium, low-noise, and automated systems in developed markets. It reflects characteristics of both standardization in industrial-grade models and customization in residential or off-grid applications. Regulatory frameworks influence design, fuel type, and deployment feasibility, making compliance a key characteristic of product success. The Standby Generator Sets market supports a recurring revenue model through service contracts, spare parts, and performance upgrades, creating long-term customer engagement beyond initial equipment sales.

Report Coverage

The research report offers an in-depth analysis based on Power Rating, Fuel, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand will rise across data centers, hospitals, and telecom networks due to the need for uninterrupted power.

- Residential generator adoption will increase in response to extreme weather and urban grid instability.

- Manufacturers will expand gas and hybrid fuel offerings to meet emission compliance targets.

- Remote monitoring and smart diagnostics will become standard features across product lines.

- Emerging economies will drive strong volume growth through infrastructure expansion and industrialization.

- Rental and mobile generator segments will gain traction in construction, mining, and events.

- Regulatory pressure will push diesel-based units toward cleaner alternatives and Stage V compliance.

- Compact, low-noise units will see high demand in urban residential and commercial segments.

- Strategic collaborations with infrastructure developers and utilities will expand market reach.

- Long-term growth will benefit from digitalization, sustainability goals, and decentralized energy systems.