Market Overview

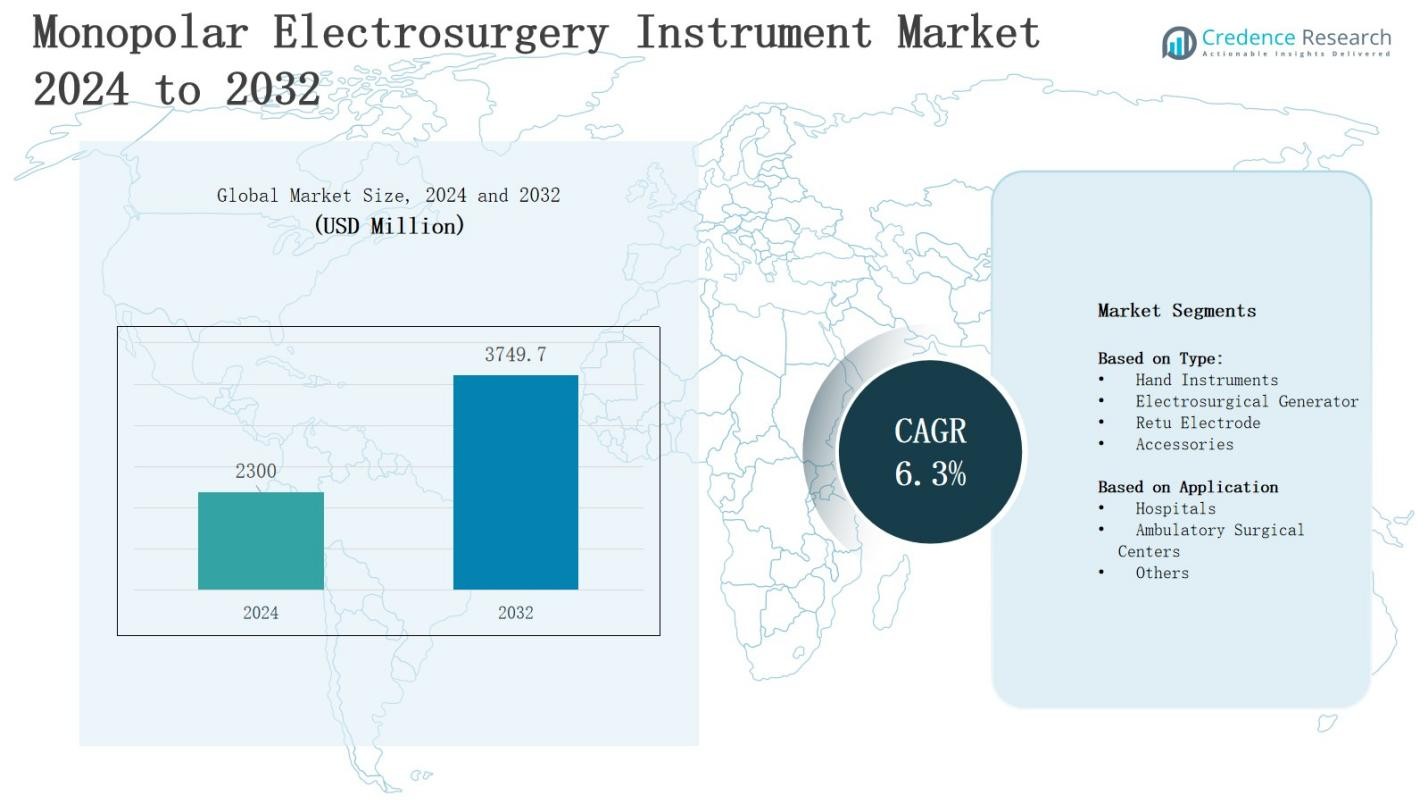

The Monopolar Electrosurgery Instrument Market is projected to grow from USD 2300 million in 2024 to USD 3749.7 million by 2032, registering a CAGR of 6.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Monopolar Electrosurgery Instrument Market Size 2024 |

USD 2300 Million |

| Monopolar Electrosurgery Instrument Market, CAGR |

6.3% |

| Monopolar Electrosurgery Instrument Market Size 2032 |

USD 3749.7 Million |

The monopolar electrosurgery instrument market is driven by rising surgical procedures, growing demand for minimally invasive techniques, and increasing adoption of advanced electrosurgical devices in hospitals and ambulatory surgical centers. Surge in chronic diseases, aging populations, and preference for quicker recovery times strengthen its growth. Technological advancements, including devices with enhanced safety features and precision, are improving outcomes and reducing complications. Market trends highlight integration of digital platforms, adoption in outpatient settings, and expansion in emerging economies due to improved healthcare access. Continuous R&D efforts by key players further support innovation and competitive differentiation in this market.

The monopolar electrosurgery instrument market demonstrates diverse regional dynamics, with North America holding the largest share, followed by Europe and Asia-Pacific as key growth hubs. Latin America and the Middle East & Africa contribute smaller shares but show rising potential with healthcare modernization and expanding access. It is shaped by strong competition from global players including Conmed, Olympus Corporation, Medtronic Plc, KLS Martin, B. Braun Melsungen AG, Stryker, Apyx Medical Corporation, Johnson & Johnson, Integra LifeSciences, Stingray Surgical Products, LLC, and Surgical Holdings.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The monopolar electrosurgery instrument market will grow from USD 2300 million in 2024 to USD 3749.7 million by 2032, registering a CAGR of 6.3% during the forecast period.

- Rising surgical procedures, aging populations, and demand for minimally invasive techniques drive adoption, while hospitals and ambulatory surgical centers accelerate growth through advanced infrastructure and preference for quicker recovery outcomes.

- Electrosurgical generators dominated with 38% share in 2024, followed by hand instruments at 27%, return electrodes at 20%, and accessories at 15%, reflecting varied clinical utility across surgical settings.

- By application, hospitals led with 61% share, ambulatory surgical centers captured 28%, and others held 11%, showing strong preference for established surgical facilities supported by advanced equipment availability.

- Regionally, North America led with 34%, Europe held 28%, Asia-Pacific reached 24%, Latin America stood at 8%, and Middle East & Africa captured 6%, highlighting broad yet uneven global market presence.

Market Drivers

Rising Demand for Minimally Invasive Surgeries

The monopolar electrosurgery instrument market is supported by the increasing demand for minimally invasive procedures. Patients prefer such surgeries due to shorter hospital stays, reduced blood loss, and faster recovery. Surgeons use monopolar electrosurgery devices for precise cutting and coagulation during various procedures. Growing acceptance of advanced surgical tools in both developed and developing healthcare systems strengthens adoption. It also aligns with healthcare providers’ focus on cost-effective treatment solutions while maintaining high patient safety standards.

- For instance, Medtronic’s Valleylab™ electrosurgical generators are used by surgeons to perform monopolar cutting and coagulation during laparoscopic and open surgeries, supporting tissue dissection and hemostasis in a variety of minimally invasive procedures

Growing Prevalence of Chronic Diseases and Aging Population

The monopolar electrosurgery instrument market benefits from the growing burden of chronic diseases such as cancer, cardiovascular disorders, and gastrointestinal conditions. These illnesses often require surgical intervention supported by reliable electrosurgical instruments. Aging populations in major regions further contribute, as elderly patients frequently need surgeries for age-related diseases. It gains importance in ensuring effective surgical management and shorter recovery timelines. Expanding access to healthcare in emerging economies also drives higher procedural volumes.

- For instance, the World Health Organization reported in 2022 that cardiovascular diseases account for approximately 17.9 million deaths annually worldwide, many necessitating surgical treatment where electrosurgical devices are essential for precision and safety.

Technological Advancements in Electrosurgical Devices

The monopolar electrosurgery instrument market experiences strong growth with the integration of advanced technologies. Innovations in energy delivery, precision cutting, and improved safety features enhance surgical outcomes and minimize risks. Manufacturers invest in research and development to create instruments with ergonomic designs and higher efficiency. It enables surgeons to perform complex procedures with greater control. Continuous product innovation strengthens competitive advantage and supports increasing adoption across healthcare facilities worldwide.

Expansion of Outpatient and Ambulatory Surgical Centers

The monopolar electrosurgery instrument market is influenced by the rapid growth of ambulatory surgical centers and outpatient facilities. These centers emphasize efficiency, cost-effectiveness, and reduced patient recovery time. Monopolar electrosurgery instruments support quick procedures in such environments with consistent safety. It encourages broader acceptance of these devices outside traditional hospitals. Rising healthcare expenditure and focus on decentralized surgical care create favorable conditions for expansion, further driving sustained demand across multiple regions.

Market Trends

Integration of Advanced Safety and Precision Features

The monopolar electrosurgery instrument market is witnessing increasing adoption of devices equipped with advanced safety features. Surgeons prefer instruments that minimize collateral tissue damage and ensure precise energy delivery. Companies are innovating with controlled energy settings and improved insulation technologies to enhance patient outcomes. It strengthens the trust of healthcare providers in using these instruments for complex surgeries. Growing awareness of safer surgical practices supports this trend across both developed and emerging regions.

- For instance, Medtronic’s Valleylab FX8 energy platform includes the TissueFect sensing technology, which continuously monitors tissue response to deliver consistent energy while reducing the risk of thermal injury.

Shift Toward Ambulatory and Outpatient Surgical Settings

The monopolar electrosurgery instrument market benefits from the shift toward outpatient and ambulatory care centers. Healthcare systems are focusing on reducing hospital stays while maintaining quality care standards. Instruments designed for portability and cost-effectiveness are increasingly used in these settings. It helps facilities perform high volumes of routine and elective surgeries efficiently. Rising healthcare expenditure and expansion of same-day surgery centers further promote this trend, boosting instrument adoption across multiple specialties.

Adoption of Digital Platforms and Smart Electrosurgery Systems

The monopolar electrosurgery instrument market is evolving with the integration of digital technologies. Smart systems with automated energy control and real-time monitoring improve surgical accuracy. Manufacturers are introducing devices that integrate with hospital IT systems for better procedural tracking and documentation. It supports data-driven clinical decisions and enhances efficiency during surgeries. Growing demand for technologically advanced instruments positions digital adoption as a key trend shaping the competitive landscape.

- For instance, Ethicon, a Johnson & Johnson company, has developed advanced digital electrosurgery platforms with automated energy modulation that enhance surgical precision while linking with electronic medical records for seamless documentation.

Expansion in Emerging Economies with Healthcare Modernization

The monopolar electrosurgery instrument market is expanding rapidly in emerging economies driven by rising healthcare investments. Countries in Asia-Pacific, Latin America, and the Middle East are modernizing surgical infrastructure to meet rising patient demand. Affordable devices with reliable performance are gaining significant traction in these regions. It supports higher surgical volumes and wider accessibility to advanced care. International manufacturers are partnering with regional distributors, strengthening the availability of electrosurgery instruments across diverse healthcare markets.

Market Challenges Analysis

Risk of Surgical Complications and Safety Concerns

The monopolar electrosurgery instrument market faces challenges due to risks linked with tissue burns, unintended injuries, and electrical hazards. Surgeons and hospitals remain cautious, as improper use can cause complications that impact patient safety. It requires strict adherence to training protocols and safety standards, which can delay adoption in some facilities. Regulatory bodies demand compliance with rigorous guidelines, increasing approval timelines. Growing awareness of potential risks creates hesitation among healthcare providers and limits widespread acceptance.

High Costs and Limited Access in Emerging Markets

The monopolar electrosurgery instrument market encounters barriers related to high device costs and limited access in developing regions. Advanced instruments equipped with safety features often remain expensive for smaller healthcare centers. It restricts usage to well-funded hospitals, leaving rural and low-income areas underserved. Economic constraints in emerging economies reduce purchasing capacity for high-end instruments. Competitive pricing pressure also challenges manufacturers striving to balance affordability with innovation. These factors slow down global market penetration.

Market Opportunities

Growing Adoption in Emerging Healthcare Systems

The monopolar electrosurgery instrument market holds strong opportunities in emerging healthcare systems where surgical volumes are rapidly increasing. Countries in Asia-Pacific, Latin America, and parts of the Middle East are investing heavily in modernizing hospital infrastructure. It creates demand for advanced surgical instruments that ensure efficiency and safety. Expanding insurance coverage and government healthcare initiatives are improving patient access to surgical care. Rising awareness among surgeons and healthcare providers further accelerates adoption in these high-growth regions.

Innovation and Integration of Advanced Technologies

The monopolar electrosurgery instrument market can benefit significantly from ongoing technological innovation. Manufacturers are focusing on integrating advanced safety mechanisms, real-time monitoring, and ergonomic designs. It opens opportunities for premium product segments catering to hospitals and specialized surgical centers. Growing demand for minimally invasive surgeries supports adoption of instruments with enhanced precision. Strategic collaborations between device makers and healthcare facilities encourage faster commercialization. Expanding digital integration also positions this market for long-term growth potential.

Market Segmentation Analysis:

By Type

The monopolar electrosurgery instrument market, by type, is categorized into hand instruments, electrosurgical generators, return electrodes, and accessories. Electrosurgical generators held the dominant share of 38% in 2024, driven by their critical role in providing controlled energy for diverse surgical procedures. Hand instruments accounted for 27% share, supported by their widespread use in routine operations. Return electrodes captured 20% share due to their importance in ensuring patient safety. Accessories represented 15%, reflecting steady demand for complementary components.

- For instance, Ethicon’s Harmonic Ace® hand instruments are frequently utilized in minimally invasive procedures to enable precise tissue dissection alongside electrosurgery tools. Return electrodes captured 20% share due to their importance in ensuring patient safety.

By Application

The monopolar electrosurgery instrument market, by application, is divided into hospitals, ambulatory surgical centers, and others. Hospitals dominated with a 61% share in 2024, attributed to high patient volumes, advanced infrastructure, and adoption of innovative electrosurgical technologies. Ambulatory surgical centers accounted for 28% share, supported by the rising shift toward outpatient procedures and cost-effective care. The others segment held 11% share, representing usage across smaller clinics and specialty centers seeking efficient surgical solutions.

- For instance, the Mayo Clinic integrated Medtronic’s Valleylab™ FT10 energy platform across multiple specialty departments to enhance precision and reduce procedure time.

Segments:

Based on Type:

- Hand Instruments

- Electrosurgical Generator

- Retu Electrode

- Accessories

Based on Application

- Hospitals

- Ambulatory Surgical Centers

- Others

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America held the largest share of 34% in the monopolar electrosurgery instrument market in 2024. Strong presence of advanced healthcare infrastructure and early adoption of innovative surgical technologies drive regional growth. High prevalence of chronic diseases and growing demand for minimally invasive procedures strengthen the market position. It benefits from favorable reimbursement policies and strong purchasing power among hospitals and surgical centers. Leading manufacturers actively expand portfolios and distribution networks, ensuring consistent market dominance across the region.

Europe

Europe accounted for 28% share in the monopolar electrosurgery instrument market in 2024. Rising number of surgical procedures and increased preference for electrosurgery in complex operations support market expansion. Regulatory focus on patient safety drives the adoption of advanced devices with improved energy control and safety features. It gains momentum from robust public healthcare systems and rising healthcare expenditure. Strong presence of established medical device companies and strategic collaborations continue to boost product availability across major European countries.

Asia-Pacific

Asia-Pacific represented 24% share in the monopolar electrosurgery instrument market in 2024. Rapid growth of healthcare infrastructure, increasing patient population, and rising medical tourism accelerate demand. Emerging economies like China and India invest significantly in hospital modernization and surgical advancements. It benefits from rising awareness about advanced surgical solutions and growing acceptance of minimally invasive techniques. Expansion of private healthcare providers and strong focus on affordability encourage adoption, making Asia-Pacific the fastest-growing region in this market.

Latin America

Latin America accounted for 8% share in the monopolar electrosurgery instrument market in 2024. Growing investments in healthcare modernization and increasing accessibility of surgical services drive regional growth. Brazil and Mexico lead with higher demand, supported by government initiatives and private sector expansion. It benefits from rising surgical volumes in urban centers and broader awareness of advanced surgical technologies. Limited resources in rural areas pose challenges, but rising collaborations with international suppliers enhance market penetration.

Middle East & Africa

The Middle East & Africa captured 6% share in the monopolar electrosurgery instrument market in 2024. Investments in modern hospitals and specialty care centers support market demand. Gulf countries lead adoption due to higher healthcare expenditure and strong focus on advanced treatment solutions. It gains traction with international players entering regional markets through partnerships. Limited healthcare infrastructure in parts of Africa remains a challenge, yet growing government initiatives improve surgical care access and create long-term opportunities.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Johnson & Johnson

- Conmed

- Stryker

- Olympus Corporation

- Surgical Holdings

- Apyx Medical Corporation

- Medtronic Plc

- Stingray Surgical Products, LLC

- KLS Martin

- Braun Melsungen AG

- Integra LifeSciences

Competitive Analysis

The monopolar electrosurgery instrument market is highly competitive, with global and regional players focusing on innovation, safety, and performance. Key companies such as Conmed, Olympus Corporation, Medtronic Plc, KLS Martin, B. Braun Melsungen AG, Stryker, Apyx Medical Corporation, Johnson & Johnson, Integra LifeSciences, Stingray Surgical Products, LLC, and Surgical Holdings strengthen their positions through continuous product development, strategic collaborations, and distribution expansion. It is influenced by rising demand for minimally invasive surgeries, driving companies to enhance device precision, safety mechanisms, and digital integration. Established players invest in advanced technologies to address surgical complexities, while smaller companies compete by offering cost-effective solutions with niche advantages. The market also reflects strong emphasis on regulatory compliance, pushing firms to meet stringent safety standards. Competitive intensity remains high, as companies pursue mergers, acquisitions, and regional partnerships to expand portfolios and gain access to emerging economies. It highlights a dynamic landscape where innovation, global reach, and pricing strategies play critical roles in determining long-term leadership.

Recent Developments

- In January 2024, Olympus Corporation announced the full market availability of its redesigned ESG-410 Surgical Energy Platform, which offers a comprehensive energy solution for various surgical specialties including monopolar and bipolar modes, advanced energy applications, ultrasonic dissection, and hybrid energy.

- In March 2025, Johnson & Johnson introduced the DUALTO™ surgical energy system, a modular platform designed to power monopolar, bipolar, ultrasonic, and advanced bipolar instruments from a single unit. It reduces footprint by 46% compared to separate generators and offers a dual configuration that allows two surgeons to operate simultaneously from one electrosurgical unit.

- In February 2024, Medtronic introduced a new generation of electrosurgical generators with enhanced energy delivery algorithms aimed at improving surgical precision. This launch adds to their monopolar and bipolar electrosurgery product portfolio.

Report Coverage

The research report offers an in-depth analysis based on Type, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Growing demand for minimally invasive surgeries will continue driving adoption across global healthcare facilities.

- Hospitals will maintain dominance, but ambulatory surgical centers will expand rapidly with outpatient procedure growth.

- Technological innovation will focus on safety features, energy control, and enhanced surgical precision worldwide.

- Digital integration and smart electrosurgery systems will improve efficiency and support data-driven surgical decision making.

- Emerging economies will create strong opportunities through healthcare modernization and increasing surgical infrastructure investments.

- Aging populations and chronic disease prevalence will consistently boost surgical volumes requiring electrosurgery instruments.

- Key players will strengthen positions through mergers, acquisitions, and global distribution network expansion strategies.

- Cost-effective instruments will gain traction in developing markets, addressing affordability challenges and wider accessibility.

- Rising awareness about patient safety will drive stricter regulatory compliance and adoption of advanced devices.

- Continuous R&D investments will foster product differentiation, enhancing competitiveness and supporting long-term market growth.