Market Overview:

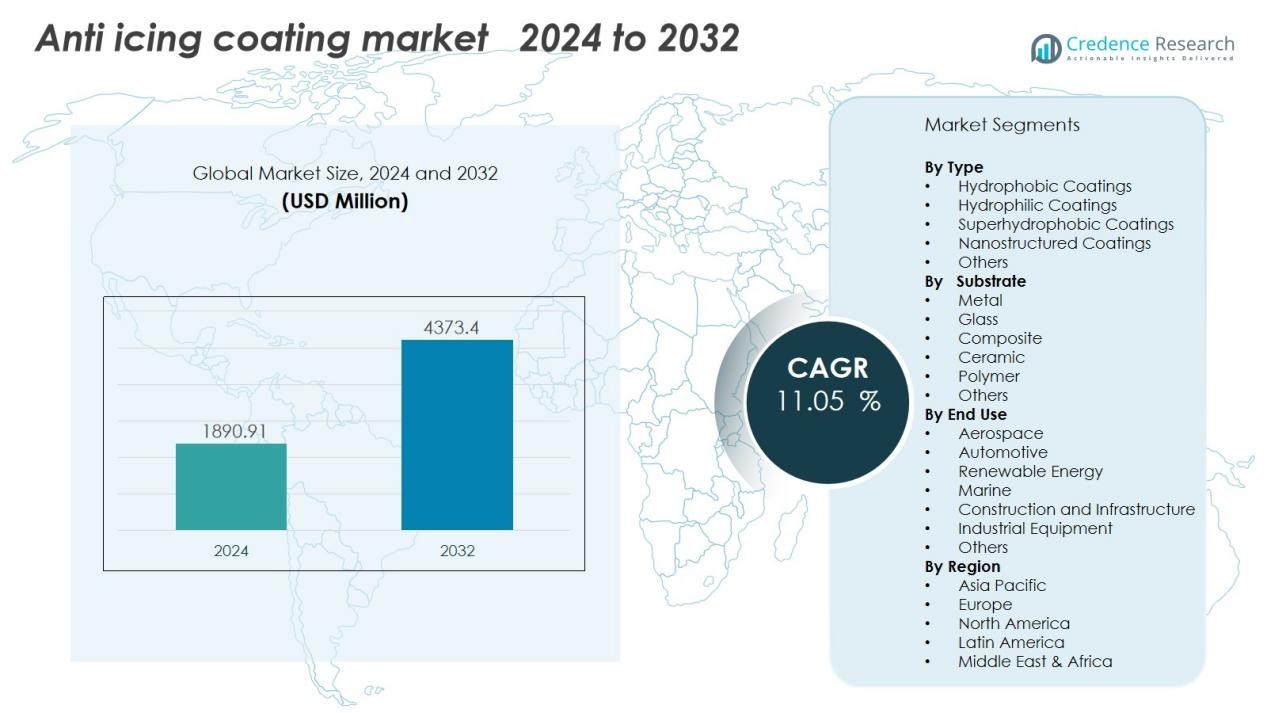

The Anti Icing Coating Market size was valued at USD 1890.91 million in 2024 and is anticipated to reach USD 4373.4 million by 2032, at a CAGR of 11.05 % during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Anti Icing Coating Market Size 2024 |

USD 1890.91 Million |

| Anti Icing Coating Market, CAGR |

11.05% |

| Anti Icing Coating Market Size 2032 |

USD 4373.4 Million |

Growing awareness of energy loss and performance degradation caused by ice accumulation drives product demand. Industries prioritize coatings that reduce maintenance costs and improve operational reliability in low-temperature environments. The development of nanotechnology-based and fluoropolymer coatings with strong hydrophobic and anti-frost properties accelerates product innovation. Rising environmental concerns encourage the adoption of eco-friendly, solvent-free formulations, pushing manufacturers toward sustainable coating technologies.

North America leads the global market due to advanced aerospace infrastructure and strong investments in wind energy. Europe follows with strict regulatory standards for aircraft and automotive safety. The Asia-Pacific region is projected to witness the fastest growth, driven by increasing infrastructure development and cold-weather operations in China, Japan, and South Korea. Emerging economies in Latin America and the Middle East offer new growth prospects through expanding industrial activities and transportation infrastructure.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The Anti-Icing Coating Market was valued at USD 1,023.47 million in 2018 and reached USD 1,890.91 million in 2024, projected to attain USD 4,373.4 million by 2032, expanding at a CAGR of 11.05% from 2024 to 2032.

- North America leads the market with a 36% share, driven by advanced aerospace infrastructure, strong R&D, and widespread adoption in renewable energy and automotive sectors.

- Europe holds 29% share, supported by strict emission regulations, sustainable coating innovations, and investments in aviation and electric mobility.

- Asia-Pacific accounts for 22% share and is the fastest-growing region, propelled by industrialization, cold-weather infrastructure expansion, and technological progress in China, Japan, and South Korea.

- By type, hydrophobic coatings dominate with 46% share due to superior ice-repellent performance, while metal substrates lead by substrate segment with 41% share, reflecting their extensive use in aircraft, vehicles, and wind turbines.

Market Drivers:

Rising Demand from Aviation and Aerospace Industries

The Anti-Icing Coating Market grows steadily due to strong demand from aviation and aerospace sectors. Aircraft face safety risks and operational delays due to ice accumulation on wings, turbines, and sensors. Anti-icing coatings reduce drag, enhance efficiency, and prevent ice-related failures during flight. Airlines and manufacturers invest in advanced coatings to comply with strict safety standards set by aviation authorities. The growing number of aircraft deliveries and maintenance programs continues to support coating adoption across civil and military fleets.

- For instance, NASA Langley Research Center developed an epoxy-based polymer coating that demonstrated a 56% reduction in ice adhesion strength at -16°C compared to untreated aluminum alloy surfaces.

Expanding Application in Renewable Energy and Automotive Sectors

The growing use of anti-icing coatings in wind turbines, electric vehicles, and infrastructure strengthens the market outlook. Ice formation on turbine blades reduces power generation efficiency, prompting energy companies to use advanced coatings for smoother operations. In the automotive sector, manufacturers apply these coatings to sensors, windshields, and cameras to enhance visibility and safety in cold regions. It supports energy conservation and reliability across various climate conditions. Increasing investments in sustainable mobility and clean energy projects drive further demand.

- For instance, Wicetec has deployed its Ice Prevention System (WIPS) featuring patented carbon fabric blade heating technology across more than 700 MW of installed wind power capacity globally.

Technological Innovations in Nanostructured and Hydrophobic Coatings

Continuous innovation in nanomaterials and surface engineering supports product improvement across industries. Researchers develop coatings with enhanced adhesion resistance, durability, and self-cleaning capabilities. These coatings provide superior performance under extreme cold, reducing maintenance frequency and downtime. It helps manufacturers differentiate products through superior hydrophobic properties and corrosion resistance. The introduction of smart coatings that respond to temperature variations also increases adoption in critical applications.

Growing Emphasis on Cost Efficiency and Environmental Compliance

Industrial users adopt anti-icing coatings to reduce energy loss, equipment damage, and operational downtime caused by icing. The focus on cost-effective maintenance and longer service life enhances their appeal in industrial and infrastructure applications. Governments and regulatory bodies encourage low-VOC, solvent-free, and eco-friendly formulations. It aligns with sustainability goals while ensuring compliance with environmental standards. The trend toward green chemistry and reduced chemical waste strengthens the long-term demand outlook.

Market Trends:

Adoption of Advanced Nanotechnology and Smart Coating Solutions

The Anti-Icing Coating Market witnesses strong growth through integration of nanotechnology and smart materials. Manufacturers focus on developing coatings with superior hydrophobic and anti-adhesion properties that resist frost and ice buildup under extreme weather. Nanostructured surfaces reduce the surface energy, allowing ice to detach easily, which enhances safety and efficiency across aircraft, wind turbines, and vehicles. It helps industries extend maintenance intervals and minimize operational downtime. Smart coatings that respond dynamically to temperature or moisture changes gain interest for next-generation applications. Aerospace and automotive OEMs invest in research collaborations to develop coatings with enhanced wear resistance and chemical stability. The trend supports improved performance, energy savings, and operational reliability in cold climates.

- For instance, Lufthansa Technik collaborated with BASF to develop AeroSHARK technology, a durable surface film (not a liquid nanocoating) featuring microscopic riblet structures that achieved approximately 1% fuel savings per flight. This translates to an annual fuel consumption reduction of around 300 to 400 metric tons of kerosene per individual Boeing 777 aircraft, depending on the specific variant and flight operations.

Shift Toward Sustainable and Long-Lasting Eco-Friendly Coatings

Global focus on sustainability drives the development of environmentally compliant anti-icing coatings with reduced volatile organic compounds (VOC). Manufacturers transition toward bio-based polymers and waterborne formulations to meet regulatory and environmental goals. It strengthens the position of suppliers offering products that balance performance with ecological safety. Extended product lifespan and recyclability are now key differentiators influencing buyer preference. Companies aim to reduce maintenance costs while ensuring effective ice prevention on transportation and renewable energy assets. Rapid industrialization in cold regions promotes wider acceptance of eco-friendly solutions for infrastructure and energy projects. The growing emphasis on cleaner, long-lasting coatings highlights a shift toward sustainable innovation within the market.

- For example, their product Intergard 251HS is a two-component, low VOC, high-solids, solvent-based epoxy primer that offers robust anticorrosive protection. This product is an excellent primer for industrial use and its low VOC content (243 g/l by EPA Method 24) supports compliance with the VOC content limits set by the EU Paints Directive 2004/42/EC for certain product categories

Market Challenges Analysis:

High Production Costs and Complex Application Processes

The Anti-Icing Coating Market faces cost challenges due to expensive raw materials, complex formulation, and specialized application techniques. Nanomaterials and fluoropolymer compounds require advanced synthesis, which increases production expenses. Applying these coatings demands precise surface preparation and professional handling, raising operational costs for end users. It limits adoption among small and medium enterprises that operate under strict budget constraints. Inconsistent coating thickness and curing issues can reduce long-term effectiveness. Manufacturers continue to invest in cost optimization and scalable production technologies to enhance affordability and market reach.

Performance Limitations Under Extreme Environmental Conditions

Maintaining coating durability and functionality under severe temperature variations remains a major obstacle. Continuous exposure to UV radiation, abrasion, and de-icing chemicals can degrade coating performance over time. It challenges manufacturers to balance durability with flexibility and environmental safety. Limited field data on long-term performance under real-world conditions slows market confidence. End users in aviation, automotive, and energy sectors demand consistent results under varying humidity and pressure levels. Companies are focusing on advanced testing and material improvements to address these operational barriers and strengthen reliability across critical applications.

Market Opportunities:

Growing Integration Across Renewable Energy and Transportation Sectors

The Anti-Icing Coating Market offers strong opportunities within renewable energy and transportation industries. Wind turbine operators adopt these coatings to prevent ice accumulation that reduces power generation efficiency in cold regions. Railways, electric vehicles, and marine vessels also explore anti-icing applications to improve safety and reliability. It supports reduced maintenance costs and uninterrupted operations in harsh weather. Rising investments in offshore wind farms and cold-climate infrastructure expand product demand. Collaborations between coating developers and equipment manufacturers enhance tailored solutions for sector-specific requirements. This integration opens new revenue streams across sustainable energy and mobility sectors.

Advancements in Smart and Environmentally Compliant Coating Technologies

Continuous research into smart materials and eco-friendly formulations creates major growth potential. Self-healing, self-cleaning, and temperature-responsive coatings are gaining attention for their adaptive functionality. It strengthens product adoption in aerospace, defense, and industrial applications seeking efficiency and compliance. The shift toward low-VOC and bio-based alternatives aligns with global environmental regulations. Government incentives for green technologies encourage further product development. Expanding research partnerships and patent filings highlight increasing innovation in sustainable coatings. These advancements position the market for long-term expansion across both developed and emerging economies.

Market Segmentation Analysis:

By Type

The Anti-Icing Coating Market is segmented into hydrophobic coatings, hydrophilic coatings, and others. Hydrophobic coatings hold the largest share due to their superior water-repellent properties and effectiveness in preventing ice formation on exposed surfaces. Hydrophilic variants are gaining demand for applications where controlled moisture spreading improves de-icing efficiency. It offers flexibility across diverse environmental conditions and supports the growing need for durable surface protection. Ongoing R&D focuses on hybrid coatings that combine both properties for improved performance and longer service life in extreme temperatures.

- For Instance, Hempel A/S has applied its Hempaguard silicone hull coatings to over 5,000 vessels since 2013, with third-party verification from DNV confirming fuel savings performance. The company also produces Hempadur Multi-Strength GF 35870, a glass-flake-reinforced epoxy coating for ice-class vessels, which can be immersed in seawater after 4 hours at 20°C, suitable for early water exposure according to some data sheets.

By Substrate

Based on substrate, the market includes metals, glass, composites, and others. Metal substrates dominate due to widespread use in aircraft, wind turbines, and automotive components. Glass substrates gain traction in transportation and infrastructure applications where visibility and surface clarity are essential. Composite substrates are expanding rapidly in aerospace and renewable energy sectors for lightweight efficiency. It supports strong adhesion and enhanced protection against corrosion and mechanical stress.

- For Instance, Boeing utilizes a significant amount of aluminum alloys in the structural frameworks of many of its commercial aircraft, with traditional models like the 737 being composed of approximately 80% aluminum alloys by weight.

By End Use

The market covers key end-use industries such as aerospace, automotive, renewable energy, and industrial equipment. Aerospace remains the leading segment due to safety requirements and aircraft efficiency needs. Automotive manufacturers apply these coatings on sensors, mirrors, and windshields for improved winter performance. Renewable energy applications grow rapidly, driven by wind turbine maintenance savings. It continues to find new opportunities in cold-weather infrastructure and marine environments.

Segmentations:

By Type

- Hydrophobic Coatings

- Hydrophilic Coatings

- Superhydrophobic Coatings

- Nanostructured Coatings

- Others

By Substrate

- Metal

- Glass

- Composite

- Ceramic

- Polymer

- Others

By End Use

- Aerospace

- Automotive

- Renewable Energy

- Marine

- Construction and Infrastructure

- Industrial Equipment

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America Leading with Strong Industrial and Aerospace Base

North America holds 36% share of the global Anti-Icing Coating Market in 2024. The region benefits from advanced aerospace manufacturing, strong research capabilities, and early adoption of nanotechnology-based coatings. The United States drives regional growth with major aircraft manufacturers, wind turbine operators, and automotive producers integrating anti-icing solutions into their systems. It supports safety, efficiency, and environmental compliance across multiple sectors. Government initiatives promoting renewable energy expansion in cold climates increase demand for long-lasting and eco-friendly coatings. Canada also contributes through its strong focus on aviation safety and wind energy infrastructure in northern regions. The regional dominance is expected to continue due to sustained technological innovation and high investment in material science.

Europe Strengthened by Stringent Regulations and Sustainable Innovations

Europe accounts for 29% share of the Anti-Icing Coating Market in 2024. The region’s growth is supported by strict regulatory frameworks promoting energy efficiency and low-emission coating formulations. Germany, France, and the United Kingdom lead adoption through investments in aviation safety and electric mobility. It also benefits from R&D collaborations between coating producers and research institutes focused on hydrophobic and self-cleaning technologies. The European Union’s policies encouraging sustainable construction and renewable energy accelerate product deployment. Scandinavian countries invest heavily in coating solutions for infrastructure and wind turbines exposed to harsh weather. Regional demand continues to rise due to industrial modernization and emphasis on environmental sustainability.

Asia-Pacific Emerging as the Fastest-Growing Regional Market

Asia-Pacific holds 22% share of the Anti-Icing Coating Market in 2024 and is projected to register the highest growth rate during the forecast period. China, Japan, and South Korea lead industrial adoption driven by expansion in automotive and renewable energy sectors. It benefits from large-scale infrastructure projects and increasing use of advanced coatings for transportation and construction. Local manufacturers invest in cost-effective, high-performance formulations suitable for diverse climate conditions. The region’s rapid technological development and favorable government policies support local production capacity. Expanding aerospace and wind energy industries in India and Southeast Asia create new growth avenues. Strong supply chains and improving manufacturing standards position Asia-Pacific as a critical contributor to global market expansion.

Key Player Analysis:

- AkzoNobel N.V.

- CG2 Nanocoatings

- Cytonix

- Dow inc

- Fraunhofer-Gesellschaft

- Helicity Technologies, Inc

- Henkel AG & Co. KGaA

- NanoSonic Inc.

- NEI Corporation

- NeverWet, LLC

- Oceanit

- PPG Industries, Inc.

Competitive Analysis:

The Anti-Icing Coating Market is moderately consolidated, with key players focusing on product innovation and strategic partnerships. Major companies include AkzoNobel N.V., CG2 Nanocoatings, Cytonix, Dow Inc., Fraunhofer-Gesellschaft, Helicity Technologies, Inc., and Henkel AG & Co. KGaA. These firms invest heavily in nanotechnology and hydrophobic material development to enhance coating durability and adhesion. It emphasizes expanding application areas across aerospace, automotive, and renewable energy sectors. Companies focus on developing environmentally compliant and high-performance solutions to meet regulatory standards. Strategic collaborations with research institutions strengthen technology transfer and product testing. Continuous innovation and customized solutions help leading players maintain competitiveness and address evolving industry demands.

Recent Developments:

- In June 2025, Akzo Nobel N.V. signed an agreement to sell its shareholding in Akzo Nobel India Limited to the JSW Group, with the transaction valued at approximately €1.4 billion, and will retain its India Powder Coatings business and International Research Center while planning a technology partnership for long-term collaboration with JSW.

- In October 2025, Henkel Adhesive Technologies and Dow expanded their strategic partnership to accelerate decarbonization in adhesives manufacturing, introducing low-carbon feedstocks and renewable electricity into Henkel’s hot melt adhesive production processes, aiming to reduce product carbon footprints by 20–40% depending on the product line.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage:

The research report offers an in-depth analysis based on Type, Substrate, End Use and Region. It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- The Anti-Icing Coating Market is set to witness sustained growth driven by technological innovation and industrial expansion.

- Nanostructured and self-cleaning coatings will gain wider adoption in aerospace and renewable energy applications.

- Manufacturers will focus on developing eco-friendly, low-VOC, and bio-based coating formulations to meet global sustainability standards.

- Smart coatings with temperature-responsive and self-healing properties will redefine performance expectations in critical environments.

- Automotive and transportation sectors will increase usage to improve safety and reliability during winter operations.

- Collaborations between coating producers and research organizations will accelerate innovation and commercialization.

- Regulatory support for green materials will encourage product diversification and faster certification approvals.

- Infrastructure development in cold-climate regions will create long-term demand for durable anti-icing solutions.

- Cost optimization and scalable manufacturing processes will enhance product accessibility across emerging markets.

- The market will continue evolving toward high-performance, multi-functional coatings that combine safety, durability, and environmental responsibility.