Market Overview:

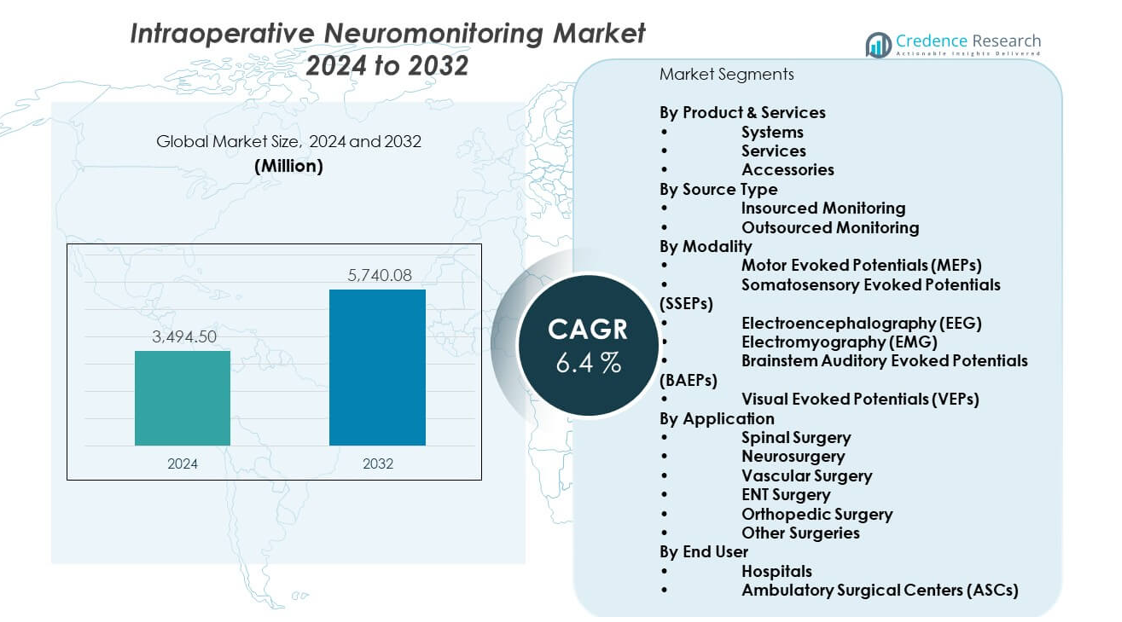

The Intraoperative neuromonitoring market is projected to grow from USD 3,494.5 million in 2024 to an estimated USD 5,740.08 million by 2032, with a compound annual growth rate (CAGR) of 6.4% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Intraoperative Neuromonitoring Market Size 2024 |

USD 3,494.5 million |

| Intraoperative Neuromonitoring Market, CAGR |

6.4% |

| Intraoperative Neuromonitoring Market Size 2032 |

USD 5,740.08 million |

Strong demand comes from the need to prevent postoperative complications during complex procedures. Healthcare providers rely on neuromonitoring to protect nerve pathways in high-risk surgeries, which boosts system adoption. Awareness grows among surgeons who seek better accuracy through EMG, EEG, and evoked potential techniques. Expanding use in ambulatory surgical centers supports market momentum. Rising focus on patient safety strengthens uptake across developed and developing healthcare systems.

North America leads the market due to high surgical volumes, strong reimbursement, and early adoption of monitoring technologies. Europe follows with robust demand from advanced neurosurgical and orthopedic centers. Asia Pacific emerges as the fastest-growing region as countries expand specialty care and invest in modern operating rooms. China, India, and South Korea record rising adoption because healthcare providers upgrade surgical infrastructure. Latin America and the Middle East show steady growth supported by improving clinical capabilities and rising specialty surgery rates.

Market Insights:

- The Intraoperative neuromonitoring market is valued at USD 3,494.5 million in 2024 and is expected to reach USD 5,740.08 million by 2032, growing at a 4% CAGR due to rising complex surgical procedures and stronger adoption of multimodal monitoring.

- North America holds 38–40%, Europe holds 28–30%, and Asia-Pacific holds 22–25%, driven by high surgical volumes, strong hospital infrastructure, and wider adoption of advanced monitoring technologies.

- Asia-Pacific is the fastest-growing region, supported by rapid upgrades in surgical facilities, rising patient loads, and broader investment in modern operating rooms across China, India, Japan, and South Korea.

- By product, Systems account for nearly 55% of the market due to high demand for multimodal monitoring platforms, while Services hold about 35% as outsourced and remote monitoring gain wider acceptance.

- By application, Spinal Surgery contributes about 40% of total procedures, while Neurosurgery holds nearly 28%, reflecting the need for accurate nerve protection in high-risk surgical interventions.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Growing Use of Monitoring in Complex Surgical Procedures

The Intraoperative neuromonitoring market expands due to rising complex surgeries. Surgeons rely on real-time feedback for safer outcomes. Demand grows in spine, neuro, and ENT procedures. Hospitals upgrade systems to reduce nerve injury risks. Monitoring teams support surgical accuracy through multimodal tools. Awareness grows among specialists across regions. Training programs help improve clinical adoption. It drives strong preference for advanced monitoring platforms.

- For instance, Medtronic’s NIM-Eclipse system can support up to 32 channels for electromyography (EMG) monitoring and manage numerous modalities, delivering high-resolution signals used in major spine and ENT procedures. The system can be used in either a Surgeon Directed (SD) or Neurophysiologist Supported (NS) configuration, offering extensive support for various surgeries including minimally invasive spinal procedures and head and neck cases.

Rising Focus on Patient Safety and Surgical Precision

Patient safety concerns encourage wider neuromonitoring use. Hospitals adopt systems that reduce postoperative deficits. Surgeons value clear signals during high-risk procedures. Monitoring supports confident decision-making in difficult cases. Providers use structured protocols for better protection. Health systems promote standardized monitoring guidelines. Demand increases from rising surgical expectations. It strengthens adoption in both large and mid-size facilities.

- For instance, NuVasive’s Pulse platform provides real-time EMG feedback with less than 2-millisecond latency, helping surgeons track neural responses during complex spine surgery.

Higher Surgical Volumes Driven by Aging Populations

Growing elderly populations push surgical numbers higher. Degenerative disorders lead many patients to surgical care. Surgeons adopt monitoring to avoid nerve complications. Hospitals invest in modern systems for repeat cases. Providers track outcomes through improved digital tools. Demand rises across orthopedic and neurological units. Insurance groups support safer surgical practices. It encourages consistent neuromonitoring use across care levels.

Technology Improvements Boost Clinical Confidence

Device makers advance signal quality and software tools. New systems offer stable baseline readings. Surgeons rely on accurate alarms during critical phases. Automated analysis reduces manual interpretation time. Hospitals use portable units for multiple rooms. Improved electrodes support cleaner signal capture. Faster setup increases procedure efficiency. It leads to higher adoption across surgical centers.

Market Trends:

Rising Integration of AI-Enhanced Monitoring Platforms

AI tools support faster interpretation in many surgeries. Systems detect subtle signal changes quickly. Automated alerts improve early response during procedures. Surgeons gain clarity in high-stress moments. Hospitals adopt AI modules to support teams. Improved analysis offers stronger predictive insight. Trend grows across advanced surgical units. The Intraoperative neuromonitoring market gains stable traction from these upgrades.

Shift Toward Remote Neuromonitoring Services

Many hospitals choose remote support models. Specialists monitor signals from central hubs. Smaller centers gain access to skilled teams. Surgeons receive expert guidance during key steps. Remote teams handle multiple cases daily. Providers lower staffing gaps through remote links. Adoption grows in ambulatory facilities. It supports wider service reach across regions.

- For instance, SpecialtyCare delivers remote IONM coverage for over 110,000 to 115,000 surgeries each year, giving hospitals access to certified technologists across regions. The company is the largest provider of IONM services in the U.S. and has monitored over a million cases in total since its founding.

Growing Demand for Multimodal Monitoring Setups

Clinicians prefer setups with multiple signal types. Combined EMG, EEG, and EP tools guide decisions. Surgeons value integrated dashboards. Hospitals choose units that support varied surgeries. Multimodal systems reduce device clutter. Training becomes easier with unified design. Providers gain consistent readings in long cases. It builds confidence in modern neuromonitoring solutions.

Expansion of Monitoring in Ambulatory Surgical Centers

Ambulatory centers adopt neuromonitoring for safety. Rising outpatient surgeries push demand. Centers focus on protecting patients with limited recovery time. Monitoring reduces risks in delicate procedures. Portable systems support these fast environments. Staff rely on simple workflows and fast setup. Adoption spreads across emerging care clusters. It strengthens demand for compact neuromonitoring systems.

Market Challenges Analysis:

High Operational Costs and Skilled Workforce Limitations

The Intraoperative neuromonitoring market faces cost pressures. Hospitals manage high expenses for equipment and staff. Skilled technologists remain limited in many regions. Training demands slow adoption in smaller centers. Providers struggle with inconsistent staffing levels. System maintenance adds financial strain yearly. Budget limits affect procurement cycles. It creates adoption barriers in developing markets.

Variability in Signal Interpretation and Regulatory Constraints

Signal interpretation varies between teams. Inexperienced staff face difficulty with complex readings. Surgeons need consistent data flow during procedures. Regulatory demands differ across countries. Many hospitals face long approval processes. Quality rules increase procurement time. Small facilities find compliance tasks difficult. It slows expansion in regulated healthcare segments.

Market Opportunities:

Expansion of Monitoring Use in Emerging Healthcare Systems

Growth rises in regions building surgical capacity. Hospitals upgrade operating rooms for advanced care. Providers adopt monitoring to match global standards. Demand grows in spine and neuro specialties. Training programs expand regional workforce size. Policymakers support safer surgical practices overall. It creates strong penetration potential across emerging markets.

Adoption of Portable and Wireless Monitoring Technologies

New portable devices support flexible room use. Wireless systems reduce setup constraints. Surgeons gain cleaner workspaces and better mobility. Hospitals prefer systems with low installation demands. Compact units help centers handle rising cases. Device makers design user-friendly interfaces for teams. It opens strong innovation opportunities across product lines.

Market Segmentation Analysis:

By Product & Services

The Intraoperative neuromonitoring market shows strong demand across systems, services, and accessories. Systems hold steady growth because hospitals adopt advanced platforms for multimodal monitoring. Services gain wider use due to rising outsourcing among facilities that need skilled technologists. Accessories such as electrodes and sensors support recurring demand and create consistent revenue cycles. Hospitals prefer integrated setups that combine hardware and service support. Service providers expand their presence across high-volume surgical centers. It strengthens market penetration across diverse care settings.

- For instance, the Nihon Kohden Neuromaster system offers up to 32 channels for acquisition, with the capacity to use up to four breakout boxes for a total of 64 inputs for broad neurophysiological monitoring in surgical settings. The specific number of channels can be configured as either 16 or 32 depending on the amplifier unit selected.

By Source Type

Insourced monitoring remains important in large hospitals with in-house teams. Skilled staff manage signals directly during complex procedures. Outsourced monitoring grows faster because many facilities rely on remote specialists for accurate interpretation. Outsourcing reduces staffing gaps in smaller and mid-sized centers. Providers choose external teams for predictable quality during high-risk surgeries. Remote coverage supports flexible scheduling. It widens access across regions with limited neuromonitoring expertise.

- For instance, the Mayo Clinic Department of Neurosurgery performs more than 9,300 complex surgical procedures each year. Many of these intricate surgeries, especially those involving the spine and brainstem, necessitate intraoperative neuromonitoring (IONM) to help minimize the risk of nerve damage. The procedures are supported by a team of trained professionals, and the hospital system uses advanced technology for this purpose.

By Modality

Motor evoked potentials and somatosensory evoked potentials lead usage in spine and neuro procedures. EEG and EMG support detailed nerve and brain function tracking. BAEPs and VEPs remain vital for delicate cranial surgeries. Surgeons choose multimodal setups to improve precision. Hospitals prefer platforms that handle varied modalities in one system. Providers integrate signals through unified dashboards. It improves decision-making during long procedures.

By Application and End User

Spinal and neurosurgery create the highest procedure volume. Vascular, ENT, and orthopedic surgeries follow with rising adoption. Hospitals remain the primary users because they handle complex surgeries. ASCs increase use for outpatient spine and orthopedic procedures. Providers invest in portable units for flexible room usage. Demand grows across centers focused on safer surgical outcomes. It supports strong adoption across both large and emerging care environments.

Segmentation:

By Product & Services

- Systems

- Services

- Accessories

By Source Type

- Insourced Monitoring

- Outsourced Monitoring

By Modality

- Motor Evoked Potentials (MEPs)

- Somatosensory Evoked Potentials (SSEPs)

- Electroencephalography (EEG)

- Electromyography (EMG)

- Brainstem Auditory Evoked Potentials (BAEPs)

- Visual Evoked Potentials (VEPs)

By Application

- Spinal Surgery

- Neurosurgery

- Vascular Surgery

- ENT Surgery

- Orthopedic Surgery

- Other Surgeries

By End User

- Hospitals

- Ambulatory Surgical Centers (ASCs)

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America

The Intraoperative neuromonitoring market records its highest share in North America with nearly 38–40%. Hospitals in the United States lead adoption due to high surgical volumes and strong access to skilled technologists. Providers invest in advanced systems that support complex spine and neuro procedures. Canada and Mexico expand use as surgical safety programs gain importance. Reimbursement support in the United States strengthens adoption across large hospital networks. Training availability improves clinician confidence. It keeps North America in a dominant position across global demand.

Europe

Europe holds an estimated 28–30% share driven by structured surgical protocols and early technology adoption. Germany, the UK, and France lead usage due to robust neurosurgical and orthopedic care infrastructure. Hospitals in Italy and Spain adopt monitoring systems to support higher procedure accuracy. Providers expand multimodal monitoring in high-risk units across major cities. Demand grows for standardized services that support nerve protection in complex procedures. Cross-border clinical programs encourage monitoring use across specialized centers. It positions Europe as a steady growth contributor.

Asia-Pacific

Asia-Pacific accounts for around 22–25% and remains the fastest-growing regional segment. China, Japan, and South Korea lead adoption with rapid upgrades in surgical infrastructure. India and Australia expand clinical use due to rising complex procedures in private and public hospitals. Healthcare systems invest in modern operating rooms to improve surgical safety. Demand rises for outsourced monitoring services where local technologists remain limited. Providers adopt portable systems to support expanding surgical departments. It drives a strong upward trajectory across emerging Asia-Pacific markets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Medtronic plc

- Natus Medical Incorporated

- NuVasive, Inc.

- Accurate Monitoring LLC

- SpecialtyCare

- Nihon Kohden Corporation

- Neuromonitoring Technologies

- inomed Medizintechnik GmbH

- Neurosoft

- Ambu A/S

- Brainlab AG (Dr. Langer Medical GmbH)

- Computational Diagnostics, Inc.

- IntraNerve, LLC

- Cadwell Industries

- GE HealthCare

Competitive Analysis:

The Intraoperative neuromonitoring market remains competitive with strong participation from device manufacturers, service providers, and software solution companies. Global leaders focus on advanced multimodal platforms that support complex neuro, spine, and vascular surgeries. Service-focused firms expand remote and outsourced monitoring coverage to meet rising demand across hospitals and ASCs. Companies invest in training programs to improve workforce capability and support consistent signal interpretation. Product developers focus on improving signal clarity, automation, and integration with surgical navigation tools. Strategic partnerships help firms expand clinical reach in high-volume surgical centers. It strengthens competitive positioning across established and emerging regions by aligning technology upgrades with rising surgical safety requirements.

Recent Developments:

- In June 2025, inomed Medizintechnik GmbH received FDA 510(k) clearance (K242852) for ALM Tube, EMG endotracheal tubes used for recording EMG activity of the laryngeal musculature while providing an open airway for patient ventilation when connected to an appropriate neuromonitoring device. As of 2024, inomed continues to develop and manufacture medical technology products across three business areas—Intraoperative Neuromonitoring, Functional Neurosurgery, and Pain Treatment—with devices used in over 5,000 hospitals in 100 countries worldwide.

- In February 2025, Medtronic received U.S. Food and Drug Administration (FDA) approval for its BrainSense™ Adaptive Deep Brain Stimulation (aDBS) system, marking the world’s first adaptive deep brain stimulation technology for Parkinson’s disease patients. In this groundbreaking development, BrainSense™ Adaptive DBS personalizes therapy based on a patient’s brain activity in real time, both in clinical settings and in daily life, with the approval also including the BrainSense electrode identifier that helps reduce time spent by patients in clinic to program their DBS settings by 85% compared to traditional electrode selection. In October 2025, Medtronic’s BrainSense™ Adaptive DBS technology was named one of TIME Magazine’s Best Inventions of 2025, recognizing it as one of the year’s most important medical innovations and representing the largest commercial launch of brain-computer interface (BCI) technology ever, with more than 40,000 DBS patients worldwide receiving Medtronic Percept devices.

Report Coverage:

The research report offers an in-depth analysis based on By Product & Services and By Modality. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Rising surgical volumes will push higher adoption across spine and neuro procedures.

- Growth in outsourced monitoring services will improve access for mid-size hospitals.

- AI-based signal interpretation tools will support faster intraoperative decisions.

- Portable multimodal systems will gain traction in ASCs and emerging care units.

- Workforce training programs will strengthen clinical reliability across regions.

- Hospitals will integrate neuromonitoring with navigation and imaging platforms.

- Demand for single-use accessories will grow due to infection-control preferences.

- Emerging markets will upgrade operating rooms to support advanced monitoring.

- Remote monitoring networks will expand coverage across high-volume centers.

- Technology partnerships will help companies enhance signal quality and workflow automation