Market Overview:

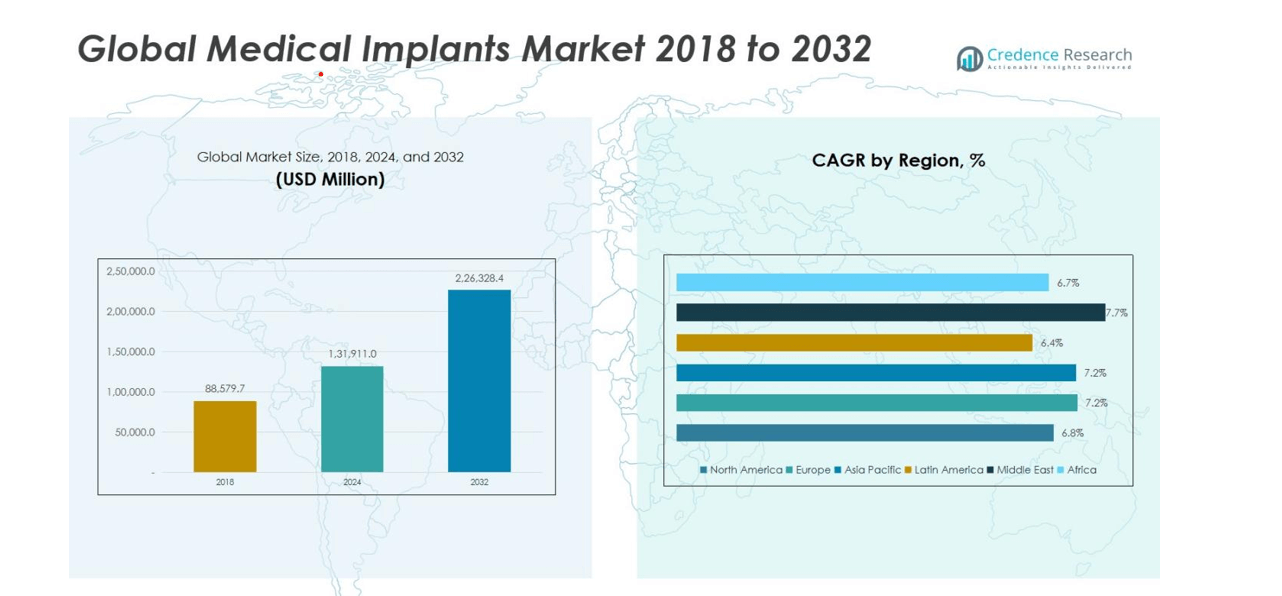

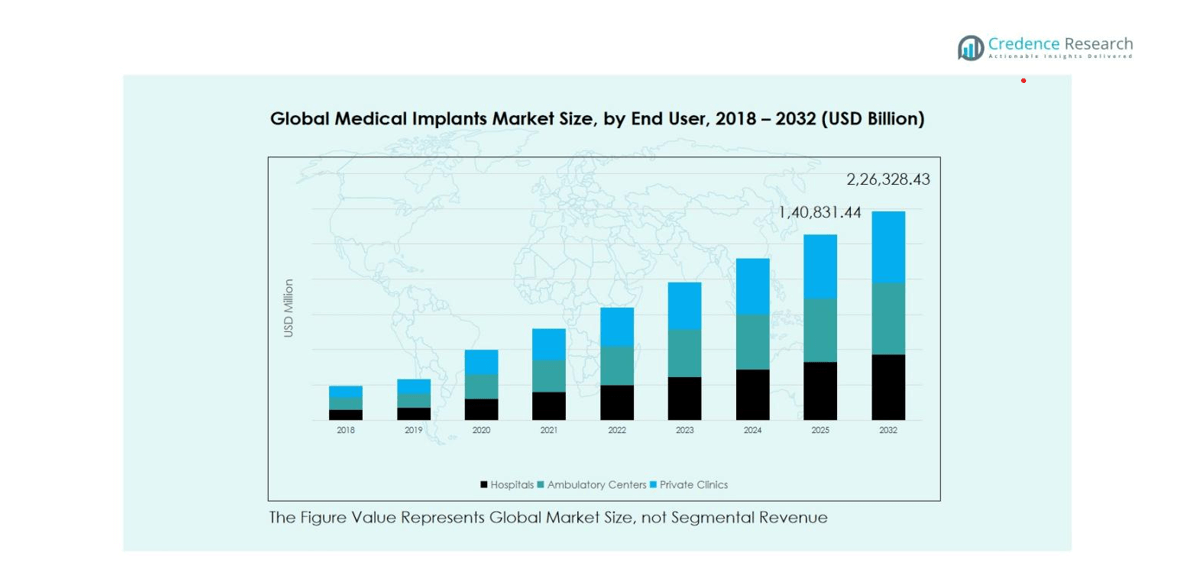

Medical Implants Market size was valued at USD 88,579.7 million in 2018 and USD 131,911.0 million in 2024, and is anticipated to reach USD 226,328.4 million by 2032, at a CAGR of 7.01% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Medical Implants Market Size 2024 |

USD 131,911.0 million |

| Medical Implants Market, CAGR |

7.01% |

| Medical Implants Market Size 2032 |

USD 226,328.4 million |

The Medical Implants Market is highly competitive, led by major players such as Zimmer Biomet Holding, Inc., Abbott, Boston Scientific Corp., Edwards Lifesciences Corp., Straumann Holding AG, Osstem Implants Co., Dentsply Sirona, Arthrex Inc., Cook Medical, and CONMED Corporation. These companies drive growth through product innovation, strategic partnerships, and geographic expansion, focusing on advanced orthopedic, cardiovascular, spinal, and dental implants. North America is the leading region, commanding approximately 35% of the global market, supported by strong healthcare infrastructure, high adoption of technologically advanced implants, and an aging population. Europe follows with a 25% share, driven by government support, reimbursement policies, and growing demand for minimally invasive procedures. Asia Pacific is emerging as a high-growth region with a 22% share, fueled by rising healthcare investments, increasing chronic disease prevalence, and expanding medical infrastructure, making it a key target for market expansion.

Market Insights

- The Medical Implants Market was valued at USD 131,911.0 million in 2024 and is projected to reach USD 226,328.4 million by 2032, growing at a CAGR of 7.01%. Orthopedic and trauma implants hold the largest segment share of 32%, followed by cardiovascular implants at 20%.

- Market growth is driven by rising prevalence of chronic and degenerative diseases, aging populations, and increasing healthcare expenditure, which are boosting demand for orthopedic, cardiovascular, spinal, and dental implants globally.

- A key trend is the growing adoption of minimally invasive surgeries and outpatient procedures, reducing recovery time and hospital stays while increasing patient acceptance of advanced implants.

- The competitive landscape is dominated by Zimmer Biomet, Abbott, Boston Scientific, Edwards Lifesciences, Straumann, Osstem Implants, Dentsply Sirona, Arthrex, Cook Medical, and CONMED Corporation, focusing on innovation, partnerships, and geographic expansion.

- Regionally, North America leads with 35% market share, Europe holds 25%, Asia Pacific contributes 22%, Latin America 10%, Middle East 5%, and Africa 4%, driven by infrastructure, awareness, and adoption trends.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

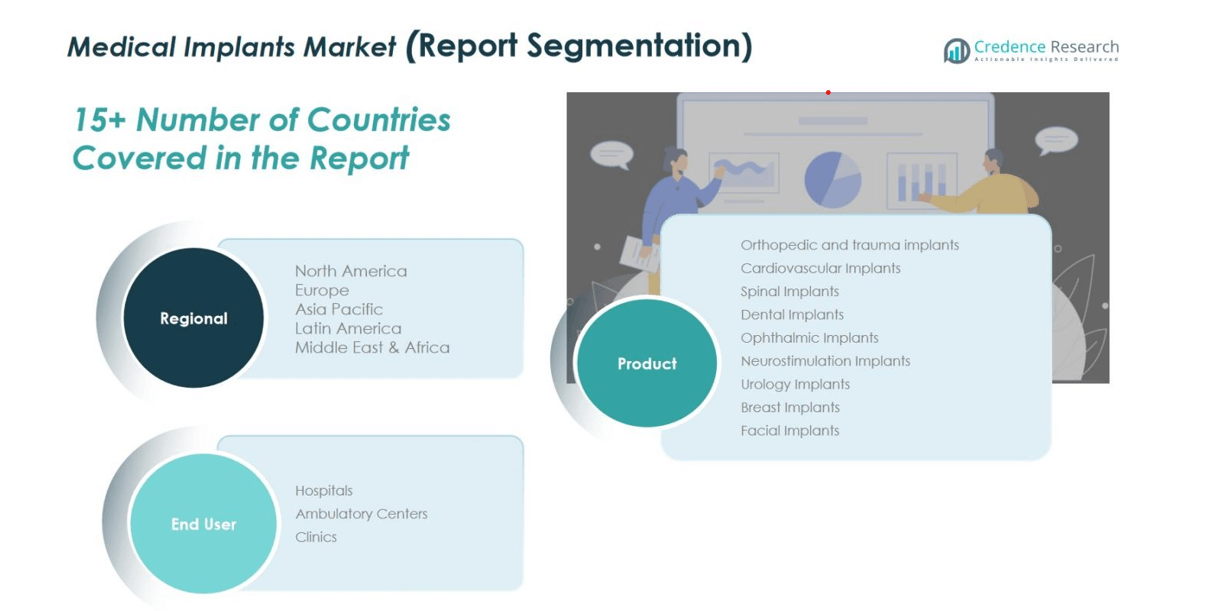

Market Segmentation Analysis:

By Product:

The orthopedic and trauma implants segment dominates the medical implants market, capturing 32% of total market share. Growth is driven by the rising prevalence of musculoskeletal disorders, aging populations, and technological advancements in implant design. Cardiovascular implants hold a significant share of around 20%, fueled by increasing cardiovascular disease incidence and minimally invasive surgical procedures. Spinal implants account for 14%, supported by the growing adoption of advanced spinal fixation systems. Dental implants represent 12%, with demand driven by oral health awareness and cosmetic dentistry. Ophthalmic, neurostimulation, urology, breast, and facial implants collectively account for the remaining market, benefiting from rising chronic conditions and cosmetic procedures.

- For instance, Meril offers total hip and knee replacement systems such as the Latitud Hip Replacement System, which is designed with advanced manufacturing technology and is used in over 50 countries worldwide.

By End User:

Hospitals are the leading end-user segment, holding 60% of the market share, owing to their advanced surgical infrastructure and higher patient inflow. Ambulatory centers contribute 25%, supported by cost-effective outpatient procedures and increasing preference for same-day surgeries. Clinics hold around 15% share, growing steadily due to specialized implant treatments and localized healthcare access. The overall growth in end-user adoption is driven by rising healthcare expenditure, increasing surgical procedures, and enhanced accessibility to advanced implants across various healthcare facilities.

- For instance, Medtronic’s SynchroMed II drug delivery pump is extensively implanted in hospitals and outpatient surgery centers to provide targeted pain management through programmable infusion systems, optimizing patient outcomes.

Key Growth Drivers

Rising Prevalence of Chronic and Degenerative Diseases

The growing incidence of chronic conditions such as arthritis, cardiovascular disorders, osteoporosis, and spinal deformities continues to drive demand for medical implants. Aging populations in developed and emerging regions increasingly require orthopedic, cardiovascular, and spinal implants to maintain mobility and quality of life. Technological advancements in minimally invasive procedures and biocompatible materials further support adoption. Hospitals and specialized clinics are expanding surgical offerings to meet this demand, contributing significantly to overall market growth.

- For instance, the FDA recently approved the SetPoint System, an implant that electrically stimulates the vagus nerve to reduce inflammation in rheumatoid arthritis patients, offering a new treatment paradigm beyond conventional drugs.

Technological Advancements and Innovation

Innovation in implant design, materials, and surgical techniques is a critical growth driver for the medical implants market. Development of 3D-printed implants, smart implants, and bioresorbable materials enhances patient outcomes and reduces recovery times. Advanced cardiovascular stents, spinal fixation systems, and customized dental implants are witnessing higher adoption due to improved durability and performance. Integration of digital imaging, robotics, and AI-assisted surgery enables precision in implant placement, boosting confidence among surgeons and accelerating market growth globally.

- For instance, companies like Restor3D are producing personalized 3D-printed orthopedic implants that improve surgical precision and patient-specific fit, reducing operative time and accelerating recovery.

Increasing Healthcare Expenditure and Accessibility

Rising healthcare spending and improved access to advanced medical facilities are fueling market expansion. Government initiatives, favorable reimbursement policies, and private healthcare investments enhance patient affordability for complex implant procedures. Expanding infrastructure in emerging economies, including hospitals and ambulatory centers, allows broader access to orthopedic, cardiovascular, and dental implants. Growing awareness of early intervention and preventive care, combined with urbanization and rising disposable incomes, supports steady global demand growth for medical implants.

Key Trends & Opportunities

Shift Towards Minimally Invasive and Outpatient Procedures

A notable trend in the medical implants market is the increasing preference for minimally invasive surgeries and outpatient procedures. These approaches reduce hospitalization time, lower procedural risks, and shorten recovery periods, driving higher patient acceptance. Ambulatory surgical centers and specialized clinics are gaining prominence as cost-effective alternatives to traditional hospital-based surgeries. This trend encourages manufacturers to innovate implants compatible with minimally invasive techniques, improving overall market penetration in both developed and emerging regions.

- For instance, Globus Medical’s XLIF® system in minimally invasive spine surgery enables smaller incisions with less tissue damage, leading to quicker recovery and reduced complications.

Growth in Emerging Markets

Emerging economies, particularly in Asia Pacific, Latin America, and the Middle East, present significant growth opportunities for the medical implants market. Rising healthcare investments, improving infrastructure, and increasing prevalence of chronic and lifestyle diseases are expanding demand. Manufacturers are focusing on region-specific product customization, local partnerships, and awareness programs to tap into these markets. Additionally, rising medical tourism in countries with cost-effective yet high-quality healthcare services further accelerates adoption, creating a lucrative environment for expanding the footprint of medical implants globally.

- For instance, Medtronic has integrated its Hugo™ robotic-assisted surgery system at Hospital Clinico UC CHRISTUS in Chile as part of a new robotic surgery program, improving minimally invasive surgery access and outcomes.

Key Challenges

High Cost of Advanced Implants

The high cost of sophisticated implants, including orthopedic, cardiovascular, and spinal devices, poses a major challenge to widespread adoption. Limited reimbursement coverage in certain regions restricts access for cost-sensitive patients, especially in emerging markets. Advanced materials and technology integration increase manufacturing expenses, impacting affordability. Hospitals and clinics may face difficulties in procuring high-end implants, slowing market penetration. Companies are increasingly exploring cost-optimization strategies and localized production to address this challenge while maintaining product quality and clinical effectiveness.

Regulatory and Compliance Barriers

Stringent regulatory requirements and prolonged approval processes for medical implants limit market entry for new products. Each region enforces strict safety, efficacy, and quality standards, requiring extensive clinical trials and documentation. Delays in regulatory approvals increase time-to-market, affecting innovation adoption and revenue growth. Compliance with ISO, FDA, CE, and local guidelines demands significant investment and expertise, posing barriers for small and mid-sized manufacturers. Navigating these complex regulatory frameworks remains a persistent challenge while ensuring patient safety and maintaining market competitiveness.

Regional Analysis

North America

North America dominates the medical implants market with a share of approximately 35%, reflecting strong healthcare infrastructure, high adoption of advanced implants, and an aging population. The market grew from USD 28,442.96 million in 2018 to USD 41,859.12 million in 2024 and is projected to reach USD 70,682.37 million by 2032, registering a CAGR of 6.8%. Growth is supported by technological advancements in orthopedic, cardiovascular, and spinal implants, coupled with favorable reimbursement policies. The U.S. leads the region, driven by increased surgical procedures, private healthcare investments, and rising awareness of innovative implant solutions among patients.

Europe

Europe accounts for around 25% of the global medical implants market, with strong adoption in countries such as Germany, France, and the UK. The market increased from USD 20,470.78 million in 2018 to USD 30,863.40 million in 2024 and is expected to reach USD 53,820.90 million by 2032, reflecting a CAGR of 7.2%. Growth is driven by an aging population, rising prevalence of orthopedic and cardiovascular diseases, and advancements in minimally invasive procedures. Government support, reimbursement frameworks, and increasing awareness of quality-of-life improvement procedures further contribute to steady market expansion across the region.

Asia Pacific

Asia Pacific is emerging as a high-growth region, contributing approximately 22% to the global medical implants market. The market grew from USD 23,314.19 million in 2018 to USD 35,103.39 million in 2024 and is projected to reach USD 61,108.68 million by 2032, registering a CAGR of 7.2%. Key growth drivers include rising geriatric populations, increasing chronic disease prevalence, expanding healthcare infrastructure, and rising medical tourism. China, Japan, and India lead adoption, supported by investments in advanced surgical technologies and growing awareness of orthopedic, dental, and cardiovascular implants. Rapid urbanization and disposable income growth further enhance market potential.

Latin America

Latin America holds a market share of approximately 10%, with Brazil and Argentina being the primary contributors. The market increased from USD 9,451.46 million in 2018 to USD 13,633.94 million in 2024 and is projected to reach USD 22,383.88 million by 2032, at a CAGR of 6.4%. The region’s growth is driven by rising prevalence of chronic diseases, increasing healthcare expenditure, and improving medical infrastructure. Expanding private healthcare facilities and government initiatives to increase access to advanced implants further support market growth. Rising awareness of minimally invasive procedures is also contributing to higher adoption rates.

Middle East

The Middle East accounts for around 5% of the global medical implants market, with the GCC countries, Israel, and Turkey being key contributors. The market expanded from USD 3,844.36 million in 2018 to USD 5,973.68 million in 2024 and is expected to reach USD 10,818.50 million by 2032, growing at a CAGR of 7.7%. Market growth is supported by rising healthcare investments, increasing prevalence of orthopedic and cardiovascular conditions, and improvements in medical infrastructure. Adoption of advanced implants, combined with supportive government policies and rising medical tourism, further strengthens the regional market outlook

Africa

Africa contributes 4% to the global medical implants market, with South Africa and Egypt being key markets. The market grew from USD 3,056.00 million in 2018 to USD 4,477.43 million in 2024 and is projected to reach USD 7,514.10 million by 2032, reflecting a CAGR of 6.7%. Growth is driven by increasing healthcare awareness, investments in hospital infrastructure, and rising demand for orthopedic and cardiovascular implants. Limited access to advanced surgical procedures and rising urbanization are gradually improving adoption, while regional initiatives to enhance healthcare accessibility provide further opportunities for market expansion.

Market Segmentations:

By Product:

- Orthopedic and Trauma Implants

- Cardiovascular Implants

- Spinal Implants

- Dental Implants

- Ophthalmic Implants

- Neurostimulation Implants

- Urology Implants

- Breast Implants

- Facial Implants

By End User:

- Hospitals

- Ambulatory Centers

- Clinics

By Region:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the medical implants market features major players such as Zimmer Biomet Holding, Inc., Abbott, Boston Scientific Corp., Edwards Lifesciences Corp., Straumann Holding AG, Osstem Implants Co., Dentsply Sirona, Arthrex Inc., Cook Medical, and CONMED Corporation. These companies are driving growth through strategic initiatives including mergers and acquisitions, product innovations, and geographic expansion. Intense competition is characterized by continuous investment in R&D to develop advanced orthopedic, cardiovascular, spinal, and dental implants with improved durability and performance. Market players are also focusing on partnerships with hospitals and healthcare providers to strengthen distribution networks and enhance patient accessibility. Additionally, emerging players in Asia Pacific and Latin America are leveraging cost-effective manufacturing and local collaborations to gain market share, intensifying competition. Overall, innovation, technological advancements, and strategic collaborations remain central to sustaining a competitive edge in this rapidly evolving market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Zimmer Biomet Holding, Inc.

- Abbott

- Boston Scientific Corp.

- Edwards Lifesciences Corp.

- Straumann Holding AG

- Osstem Implants Co.

- Dentsply Sirona

- Arthrex Inc.

- Cook Medical

- CONMED Corporation

- Others

Recent Developments

- In May 2023, Henry Schein expanded its presence in Latin America by acquiring S.I.N. Implant System, a Brazilian dental implant manufacturer, strengthening its dental market footprint.

- In February 2024, Zeda acquired The Orthopaedic Implant Company to broaden its trauma implant offerings and accelerate access to trauma solutions.

- In July 2025, Zimmer Biomet acquired a robotic knee technology company, boosting its adoption of robotic-assisted knee solutions in the U.S. market.

- In January 2025, Boston Scientific acquired Bolt Medical, a developer of intravascular lithotripsy technology, expanding its cardiovascular implant portfolio.

Report Coverage

The research report offers an in-depth analysis based on Product, End User and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market is expected to witness steady growth driven by increasing prevalence of chronic and degenerative diseases.

- Technological advancements in 3D-printed, smart, and bioresorbable implants will accelerate adoption.

- Minimally invasive surgical procedures will continue to gain preference, boosting implant demand.

- Hospitals and ambulatory centers will remain the dominant end users due to advanced infrastructure and patient inflow.

- Asia Pacific will emerge as a high-growth region with rising healthcare investments and improving medical infrastructure.

- Adoption of digital imaging, robotics, and AI-assisted surgery will enhance precision and outcomes.

- Demand for dental, orthopedic, and cardiovascular implants will continue to expand with aging populations.

- Strategic collaborations, partnerships, and mergers among key players will drive market competitiveness.

- Awareness programs and government initiatives will improve accessibility in emerging markets.

- Focus on cost-effective and locally manufactured implants will support broader market penetration globally.