Anti-Tuberculosis Drugs Market Overview:

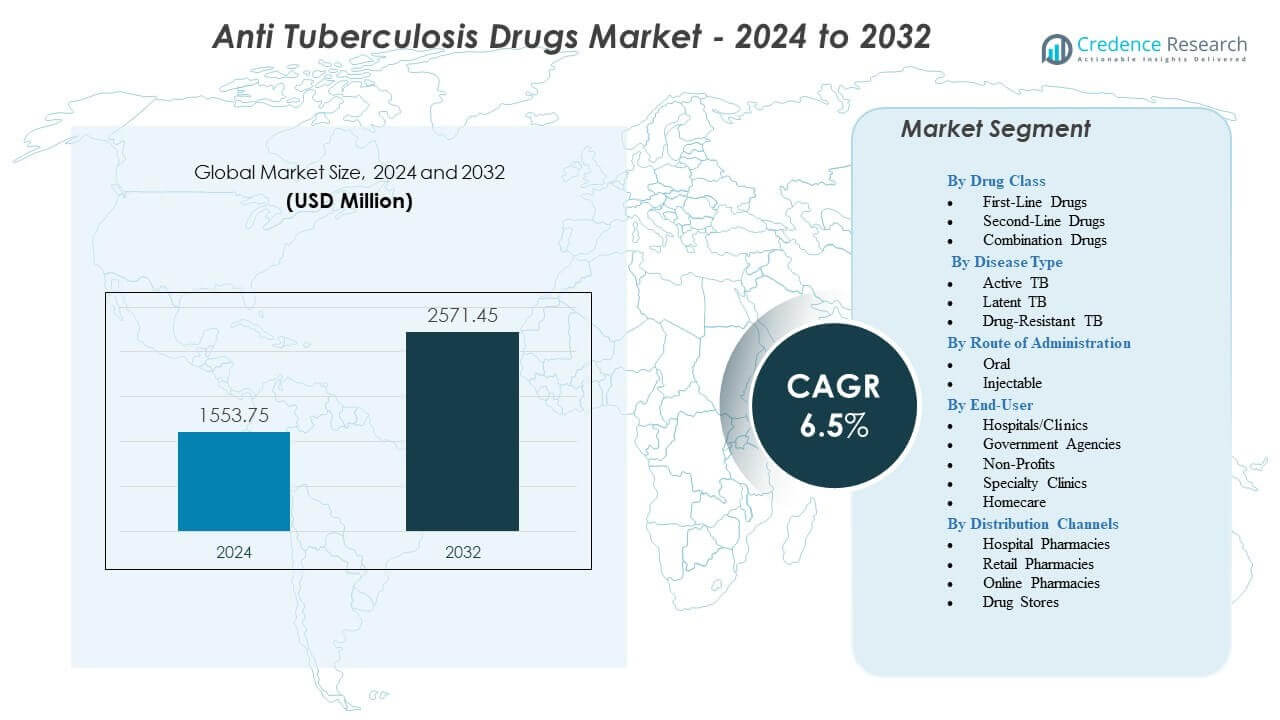

The Anti-Tuberculosis Drugs Market is projected to grow from USD 1553.75 million in 2024 to an estimated USD 2571.45 million by 2032, with a compound annual growth rate (CAGR) of 6.5% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Anti-Tuberculosis Drugs Market Size 2024 |

USD 1553.75 million |

| Anti-Tuberculosis Drugs Market, CAGR |

6.5% |

| Anti-Tuberculosis Drugs Market Size 2032 |

USD 2571.45 million |

Growing drivers include improved diagnostic capabilities, wider adoption of shorter all-oral regimens, and stronger public health investments. Countries strengthen national TB programs to increase patient identification and shorten delays between diagnosis and treatment. Pharmaceutical manufacturers update fixed-dose combinations that support adherence and reduce pill burden. Digital adherence technologies reduce therapy drop-offs and create measurable improvements in treatment continuity. Preventive therapy uptake grows in high-risk groups, lowering future disease progression. Global guideline updates reinforce the shift toward simplified regimens that boost completion rates across varied healthcare settings.

Asia-Pacific leads the Anti-Tuberculosis Drugs Market due to high disease prevalence, strong programmatic investment, and large-scale use of standardized regimens. North America and Europe maintain steady adoption through structured public health frameworks and advanced diagnostic systems. Latin America shows progress as integrated surveillance and treatment models expand access. Africa continues to emerge as countries strengthen supply chains and increase the availability of all-oral therapies. The Middle East experiences moderate growth supported by improving healthcare infrastructure and rising awareness. These regional developments create a diversified landscape that shapes long-term market direction.

Anti-Tuberculosis Drugs Market Insights:

- The Anti-Tuberculosis Drugs Market is projected to grow from USD 1553.75 million in 2024 to USD 2571.45 million by 2032, supported by a 6.5% CAGR.

- Stronger diagnostic capacity, shorter all-oral regimens, and broader preventive therapy adoption continue to drive steady treatment demand.

- Treatment restraints include rising drug resistance, long therapy durations for complex cases, and uneven adherence across high-burden populations.

- Asia-Pacific leads the market due to high prevalence and strong national program efforts, while North America and Europe sustain stable uptake through advanced care systems.

- Emerging growth is seen in Africa and Latin America as supply chains strengthen and countries expand access to quality-assured first-line and second-line therapies.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Anti-Tuberculosis Drugs Market Drivers

Growing Emphasis On Early Detection And Strengthened National Control Programs

Early detection efforts power stronger treatment demand in the Anti-Tuberculosis Drugs Market. Many countries scale diagnostic reach through community screening and rapid test deployment. Wider case detection improves timely treatment starts and lowers transmission. National control programs integrate digital adherence tools that reduce therapy drop-offs. It also supports structured treatment plans in both high-burden and urban clusters. Policymakers expand latent TB testing in primary care networks to raise preventive therapy use. Funding agencies support program expansion to reach underserved regions. These coordinated measures create a sustained push for drug uptake.

- For instance, Cepheid’s GeneXpert platform is deployed across more than 20,000 sites worldwide and enables rapid TB diagnosis, providing detection of tuberculosis and rifampicin resistance in approximately 90 minutes.

Rising Adoption Of Shorter Regimens And Improved Treatment Protocol Standards

Shorter regimens strengthen therapy preference in many treatment settings within the Anti-Tuberculosis Drugs Market. Clinicians move toward simplified regimens that reduce fatigue linked to long courses. It increases completion rates and lowers resistance development. Pharmaceutical firms update formulations to reduce pill burden and simplify combinations. Medical bodies update guidelines to support evidence-backed regimen selection. Hospitals adopt structured therapy monitoring models that track patient response. Community health teams expand counseling programs to minimize therapy interruption. These protocol enhancements raise market dependence on new and established drug classes.

Expansion Of Public Health Investments Targeting High-Burden Regions

Public health budgets rise to support better therapy access in the Anti-Tuberculosis Drugs Market. Governments prioritize TB management in national health agendas. It encourages stable procurement pipelines for essential drugs across district networks. Donor agencies strengthen supply chains to reduce stockouts in remote regions. Expanded outreach programs target high-risk groups with tailored support services. Mobile clinics reach underserved populations with screening and treatment follow-ups. Health ministries align TB programs with universal healthcare frameworks to widen reach. Stronger investment flows help maintain predictable drug demand.

- For instance, the Stop TB Partnership’s Global Drug Facility supplies quality-assured TB medicines to more than 150 countries through a pooled procurement model that consistently maintains high on-time delivery performance for first-line regimens.

Increasing Integration Of Digital Tools That Enhance Treatment Adherence And Monitoring

Digital tools influence clinician workflows and patient behavior in the Anti-Tuberculosis Drugs Market. Remote adherence platforms alert providers when therapy interruptions occur. It enables faster action to prevent drug resistance. Smartphone-based reminders help patients stay on schedule for daily doses. Program managers gain real-time visibility into adherence performance across regions. Teleconsultation models support patients who face access barriers. Hospitals use electronic treatment cards to improve communication between teams. National programs rely on integrated dashboards to track progress. These tools reinforce structured and uninterrupted therapy cycles.

Anti-Tuberculosis Drugs Market Trends

Shift Toward Novel Drug Classes Designed To Address Resistance And Safety Concerns

Novel drug classes guide therapeutic direction in the Anti-Tuberculosis Drugs Market. Developers prioritize regimens with lower toxicity and quicker action. It supports stronger clinician confidence in next-generation therapies. Regulatory bodies accelerate review pathways for promising compounds. Safety improvements reshape preference patterns in many regions. Hospitals adopt updated protocols that highlight reduced monitoring needs. Pharmaceutical firms conduct trials focused on difficult-to-treat cases. These shifts point to a pipeline that supports reliable long-term treatment outcomes.

Growing Focus On Combination Therapies Tailored To Diverse Patient Profiles

Combination therapies gain wider acceptance in the Anti-Tuberculosis Drugs Market. Clinicians choose multi-agent combinations to improve response across resistant and non-resistant forms. It reduces complexity seen in fragmented treatment plans. Research groups design combinations that match individual risk profiles. Manufacturers release fixed-dose options that improve consistency. Global programs support models that evaluate combination impact on adherence. Hospitals adopt decision-support tools to optimize therapy selection. This shift enhances personalization strength in TB care.

- For instance, Lupin Limited received WHO prequalification for its 4-drug fixed-dose combination (FDC), which integrates Isoniazid 75mg, Rifampicin 150mg, Pyrazinamide 400mg, and Ethambutol 275mg into a single tablet to ensure precise dosing across varied body weights.

Widening Use Of Real-World Evidence To Support Drug Optimization And Policy Planning

Real-world evidence shapes strategic planning in the Anti-Tuberculosis Drugs Market. Health systems collect large datasets to refine protocol decisions. It improves clarity on regimen performance across diverse patient groups. Public health agencies use real-time information for regional resource planning. Pharmaceutical firms evaluate long-term outcomes to adjust development priorities. Clinical teams assess evidence to predict regimen suitability. Data-driven practices influence global policy alignment. These trends push the market toward an evidence-centered decision environment.

- For instance, the Nix-TB trial conducted by the TB Alliance demonstrated that the 6-month all-oral BPaL regimen achieved about 90% success in treating highly drug-resistant TB, far outperforming historical long-course regimens. Its results, supported by later studies such as ZeNix and TB-PRACTECAL, contributed to WHO’s 2022 decision to recommend BPaL/BPaLM as preferred short-course options for eligible MDR- and XDR-TB patients.

Strengthening Alignment Between TB, HIV, And Primary Care Programs Across Regions

Integrated care programs influence service delivery in the Anti-Tuberculosis Drugs Market. Many regions merge TB and HIV treatment pathways for seamless management. It reduces patient burden linked to fragmented care systems. Clinics streamline diagnostic protocols for co-managed conditions. Care teams coordinate therapy counseling to improve response. Policymakers unify tracking systems for better oversight. Training modules prepare providers for multi-condition care. This alignment increases treatment stability for vulnerable populations.

Market Challenges Analysis

Escalating Burden Of Drug Resistance And Treatment Non-Completion Across High-Burden Regions

Drug resistance creates a major barrier within the Anti-Tuberculosis Drugs Market. High-burden regions struggle with therapy completion due to logistic and socioeconomic gaps. It increases the risk of complicated treatment cycles and poor outcomes. MDR and XDR cases demand longer regimens that strain health systems. Providers face difficulty securing timely second-line drug supply in remote areas. National programs manage rising operational costs linked to advanced therapies. Many communities lack awareness about treatment consistency. These gaps weaken long-term disease control efforts.

Persistent Disparities In Access, Supply Chain Stability, And Trained Clinical Workforce

Access disparities limit progress in the Anti-Tuberculosis Drugs Market. Many rural areas face inconsistent supply chain performance. It disrupts therapy schedules and increases drop-off risk. Health systems report shortages of trained specialists in remote districts. Infrastructure gaps reduce diagnostic accuracy during early detection. Funding differences create uneven service coverage across regions. Community networks lack consistent follow-up capability. These disparities restrict timely and effective treatment for many patients.

Market Opportunities

Rising Scope For Next-Generation Regimens, Preventive Treatments, And Personalized Therapy Models

Next-generation regimens open strong opportunities within the Anti-Tuberculosis Drugs Market. Pharmaceutical firms target safer, shorter, and more personalized therapy options. It strengthens long-term adoption in public and private care settings. New preventive therapy programs expand reach among high-risk groups. Diagnostic innovations support earlier patient segmentation. Hospitals integrate genetic insights to guide treatment refinements. Public health programs encourage trials that validate innovative drug classes. These opportunities widen pathways for advanced therapeutic strategies.

Expansion Potential Through Public-Private Partnerships And Strengthened Regional Health Infrastructure

Public-private partnerships create new growth windows in the Anti-Tuberculosis Drugs Market. Governments collaborate with developers to stabilize procurement pipelines. It ensures predictable access to essential and emerging therapies. Infrastructure upgrades strengthen service delivery in underserved regions. Supply chains gain better resilience through structured investment. Digital platforms enhance communication between community teams and hospitals. Policy frameworks evolve to support integrated program design. These coordinated efforts position the market for stronger long-term expansion.

Market Segmentation Analysis:

By Drug Class

First-line drugs maintain a dominant share in the Anti-Tuberculosis Drugs Market due to their role in standard initial therapy and strong clinical acceptance. Demand stays high because they deliver reliable outcomes for most patients. Second-line drugs gain traction where resistance patterns rise and treatment complexity increases. It supports extended regimens for MDR and XDR cases that require broader therapeutic coverage. Combination drugs show steady growth due to fixed-dose convenience and stronger adherence rates. FDCs reduce pill burden and minimize risks linked to missed doses. Many programs favor them for large-scale public health distribution through streamlined procurement channels.

- For instance, Lupin Limited is one of the world’s largest manufacturers of WHO-prequalified Ethambutol formulations and supplies TB medicines to more than 50 countries through the Global Drug Facility and national TB programs.

By Disease Type

Active TB leads demand in the Anti-Tuberculosis Drugs Market due to higher treatment volume and structured case detection. Screening programs generate consistent patient identification that drives rapid therapy initiation. Latent TB grows due to rising preventive therapy uptake in high-risk populations. It reduces conversion risk and supports long-term disease control goals. Drug-resistant TB expands where resistance patterns shift and diagnostic precision improves. This segment relies on specialized regimens that require closer monitoring and stronger supply chain reliability across public systems.

- For instance, Sanofi’s Priftin (rifapentine) has enabled the “3HP” regimen, which reduces latent TB treatment duration from 270 daily doses of isoniazid to just 12 weekly doses.

By Route of Administration

Oral drugs hold substantial presence in the Anti-Tuberculosis Drugs Market because they align with ease of use and broad patient suitability. Most first-line and FDC therapies support daily oral dosing that improves adherence. It also simplifies distribution models across urban and rural settings. Injectable drugs retain relevance in resistant cases that need second-line agents. These therapies demand trained staff and structured oversight. Usage grows where hospital-based programs support severe or complicated cases.

By End-User

Hospitals and clinics drive significant use in the Anti-Tuberculosis Drugs Market due to their role in diagnosis, initiation, and oversight. Government agencies maintain strong procurement responsibility through national TB programs. It ensures drug supply stability across regions with varied infrastructure. Non-profits engage in outreach and support services where resource gaps persist. Specialty clinics manage complex or resistant cases that need monitored therapy. Homecare gains traction where digital adherence tools improve remote supervision.

By Distribution Channels

Hospital pharmacies lead distribution in the Anti-Tuberculosis Drugs Market due to their link with formal treatment initiation. Retail pharmacies support ongoing patient access in suburban and rural areas. It improves refill continuity for long treatment cycles. Online pharmacies expand reach where digital ordering grows and convenience preferences shift. Drug stores maintain presence in regions with mixed healthcare access models. They support community-level treatment continuity through accessible dispensing points.

Segmentation:

By Drug Class

- First-Line Drugs

- Second-Line Drugs

- Combination Drugs

By Disease Type

- Active TB

- Latent TB

- Drug-Resistant TB

By Route of Administration

By End-User

- Hospitals/Clinics

- Government Agencies

- Non-Profits

- Specialty Clinics

- Homecare

By Distribution Channels

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Drug Stores

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

Asia-Pacific holds the largest share of the Anti-Tuberculosis Drugs Market, accounting for nearly 45% of global demand due to high disease prevalence and strong government-led treatment programs. Many countries scale screening networks to support early detection and sustained therapy access. Public procurement systems strengthen drug availability across rural districts. It benefits from wide adoption of fixed-dose combinations and structured treatment protocols. National TB programs remain central drivers of consistent market activity. Research collaborations also support local access to second-line therapies.

North America represents roughly 20% of the market share due to robust surveillance systems and structured clinical guidelines. High-income healthcare frameworks support reliable drug access and precise management of resistant cases. It benefits from strong regulatory oversight that ensures consistent drug quality. Public health agencies monitor trends through integrated reporting systems. Migrant health programs contribute to steady therapy needs. Hospitals and specialty clinics manage a defined patient base with standardized protocol pathways.

Europe accounts for close to 18% of global share, driven by coordinated public health strategies and well-developed care infrastructure. Many countries focus on migrant screening programs that identify new cases earlier. It receives strong policy support for integrated TB-HIV management models. Regional agencies invest in training and diagnostic upgrades. Eastern Europe records higher treatment volume linked to resistant strain patterns. Western Europe sustains stable demand through structured pharmaceutical distribution networks.

Middle East & Africa hold about 12% of market share, supported by international aid and expanding care access. South America represents nearly 5%, with growth tied to improved surveillance and steady adoption of fixed-dose regimens.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Johnson & Johnson (Janssen)

- Otsuka Pharmaceutical

- Lupin Limited

- Macleods Pharmaceuticals Ltd.

- Viatris

- Pfizer

- Sanofi

- Novartis

- Cipla Limited

- GlaxoSmithKline (GSK)

- Merck

- Cadila Healthcare (Zydus)

- Hetero Labs Ltd.

- Sandoz Group

- Strides Pharma Science Ltd.

Competitive Analysis:

Competition in the Anti-Tuberculosis Drugs Market centers on broad product portfolios, supply chain reliability, and alignment with public health procurement systems. Global firms such as Johnson & Johnson, Otsuka, and Pfizer focus on advanced formulations and resistant-case therapeutics. It sees strong participation from regional producers like Macleods, Lupin, Cipla, and Hetero that supply essential first-line and combination drugs to high-burden regions. Companies compete on manufacturing scale, pricing stability, and regulatory compliance. Fixed-dose combination capability strengthens competitive positioning in public tenders. Partnerships with government agencies shape long-term procurement outcomes. Expansion into digital adherence support tools further differentiates major players in this evolving market landscape.

Recent Developments:

- In February 2026, Lupin Limited entered a strategic partnership with TB Alliance to advance the clinical development and commercialization of Telacebec, an investigational drug for tuberculosis, leprosy, and Buruli ulcer, leveraging Lupin’s manufacturing and global distribution capabilities.

- In January 2026, Novartis collaborated with TB Alliance to provide scientific and strategic advice on the research and development of telacebec, a novel investigational compound targeting leprosy, a neglected mycobacterial disease.

- In December 2025, TB Alliance and the Asian Development Bank formed a strategic partnership via a Memorandum of Understanding to bolster TB control in Asia and the Pacific. The collaboration focuses on health system strengthening, R&D for new TB tools, equitable access to treatments, and regional manufacturing of therapies and diagnostics.

- In July 2024, Johnson & Johnson received full FDA and European Commission approval for its TB drug SIRTURO (bedaquiline), converting it from accelerated to traditional approval for treating multidrug-resistant pulmonary TB in adults and children over 5 years weighing at least 15 kg.

Report Coverage:

The research report offers an in-depth analysis based on Drug Class, Disease Type, Route of Administration, End-User, Distribution Channels and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Demand strengthens as high-burden regions expand screening networks and improve early detection across public systems.

- Wider adoption of shorter regimens supports better adherence and raises therapy completion rates in diverse patient groups.

- Growth in fixed-dose combinations increases due to their role in simplifying treatment and reducing pill fatigue.

- Digital adherence tools gain traction and support more consistent monitoring across rural and urban care settings.

- Development of safer next-generation agents improves clinician confidence in evolving treatment protocols.

- Stronger investment flows from national programs enhance procurement stability for essential first-line drugs.

- Rising adoption of second-line therapies expands treatment capacity for drug-resistant cases with complex profiles.

- Integration of TB care with HIV and primary care programs improves patient management across high-burden regions.

- Expansion of public-private partnerships strengthens manufacturing scale and broadens global supply reach.

- Evidence-driven policy updates influence protocol refinement and promote long-term planning within major treatment ecosystems.