Market overview

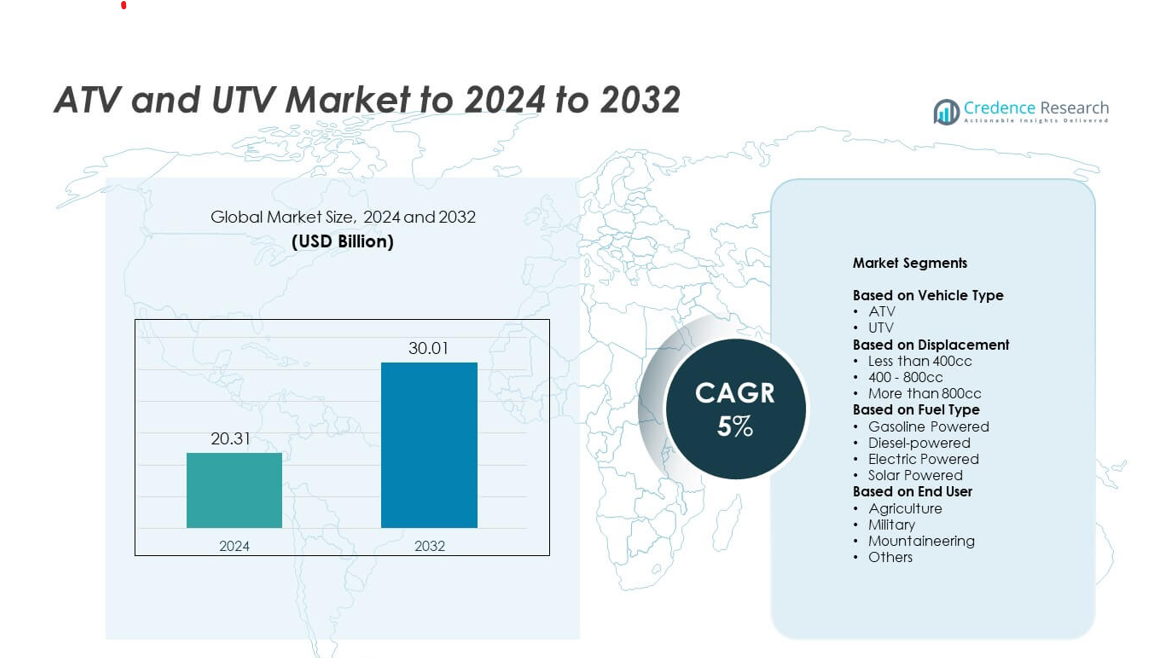

ATV and UTV Market size was valued USD 20.31 Billion in 2024 and is anticipated to reach USD 30.01 Billion by 2032, at a CAGR of 5% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| ATV and UTV Market Size 2024 |

USD 20.31 Billion |

| ATV and UTV Market, CAGR |

5% |

| ATV and UTV Market Size 2032 |

USD 30.01 Billion |

The ATV and UTV Market features prominent players such as Polaris Inc., Honda Motor Corporation, John Deere, Textron Inc., Yamaha Motor Corporation, Kwang Yang Motor Company Ltd., Kawasaki Motors Corp, BRP, Kubota Corporation, and Suzuki Motor LLC, all competing through technology upgrades and wide product portfolios. North America dominated the global market in 2024 with about 52% share, supported by strong recreational use, advanced dealership networks, and high utility demand in agriculture and construction. Europe and Asia Pacific followed with notable shares driven by expanding mechanization, rising tourism activity, and steady adoption across commercial and off-road applications.

Market Insights

- The ATV and UTV Market reached USD 20.31 Billion in 2024 and is projected to hit USD 30.01 Billion by 2032, growing at a CAGR of 5%.

- Strong utility demand in farming and construction drives market expansion, with UTVs leading the vehicle type segment at about 61% share due to superior load capacity and safety.

- Electrification, digital dashboards, and improved suspension systems shape key trends as users shift toward cleaner, low-noise, and tech-enhanced models.

- Competition intensifies as major brands upgrade performance, expand service networks, and strengthen aftermarket offerings, while rising component costs act as a restraint.

- North America dominated in 2024 with nearly 52% share, followed by Europe at 21% and Asia Pacific at 18%, while the 400–800cc displacement segment led globally with about 48% share.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Vehicle Type

The UTV category led the ATV and UTV Market in 2024 with about 61% share. Buyers preferred UTVs due to strong load capacity, better safety, and wider utility in farming, construction, and outdoor recreation. Growth increased as fleet users adopted UTVs for transport and towing tasks across rugged sites. Rising demand for side-by-side models with enhanced suspension and cabin comfort also supported segment expansion. The ATV segment held a smaller share but remained popular in sports racing and trail riding.

- For instance, the official specifications for the John Deere Gator XUV865R confirm a cargo box capacity of 454 kg (1,000 lb) and a total vehicle payload capacity of 487 kg (1,074 lb)

By Displacement

The 400-800cc displacement segment dominated the market in 2024 with nearly 48% share. This range stayed ahead because users viewed mid-range engines as the best balance between power, fuel efficiency, and price. The segment gained further traction in agriculture, forestry, and adventure tourism as operators needed stronger torque for cargo and towing. Models in this category offered improved durability and smoother performance on uneven terrain, which increased adoption among both private and commercial buyers.

- For instance, Polaris states that the Sportsman 570 uses a 567cc engine producing 44 hp, verified from the company’s official model sheet.

By Fuel Type

Gasoline-powered models held the leading position in 2024 with about 68% share. This dominance came from strong availability, lower upfront cost, and wider consumer familiarity with gasoline engines. Users also preferred gasoline units for higher speed, flexible maintenance, and better performance across varied terrains. Diesel-powered vehicles grew in heavy-duty tasks, while electric options expanded steadily as buyers showed interest in low-noise and low-maintenance machines. Solar-powered units remained limited due to low output and slow charging.

Key Growth Drivers

Rising Utility Adoption Across Agriculture and Construction

Demand for ATV and UTV models grew as farmers and site operators relied on compact vehicles for transport, hauling, and field mobility. These vehicles offered strong torque, low operating cost, and the ability to access narrow or rough areas that larger machines could not reach. Expanding mechanization in small and mid-scale farms strengthened adoption, while construction crews used UTVs for equipment movement and worker transport. Better payload ratings and improved off-road capability supported consistent market growth.

- For instance, Kubota confirms the RTV-X1140 offers a total vehicle payload capacity of 739 kg (1,629 lb) and a towing capacity of 590 kg (1,300 lb)

Expanding Recreational and Adventure Activities

Growth accelerated as outdoor tourism, motorsports events, and trail riding gained traction. Buyers showed stronger interest in off-road leisure due to rising disposable income and the appeal of adventure travel. Manufacturers introduced safer frames, better suspension systems, and advanced braking, which attracted more new users, including beginners. Clubs, rental services, and guided tour operators expanded fleets to meet rising rider participation across North America, Europe, and Asia, strengthening long-term recreational demand.

- For instance, Can-Am officially specifies the Maverick X3 X RS Turbo RR at 200 hp from its 900cc engine, supported by BRP’s product sheet.

Increased Technological Advancements in Powertrain and Safety

Innovation in engine performance, electric drivetrains, digital displays, and driver-assist features boosted market expansion. Modern vehicles offered smoother handling, lower emissions, and enhanced stability systems, making them safer and easier to operate across difficult terrain. Growth also improved with advanced telematics, GPS tracking, and smartphone integration that supported fleet monitoring and maintenance planning. Enhanced reliability and reduced service needs encouraged more adoption across commercial, utility, and recreational applications.

Key Trends and Opportunities

Shift Toward Electrification and Low-Noise Mobility

Electric ATV and UTV models gained momentum as users searched for cleaner, quieter, and lower-maintenance alternatives. Advancements in battery density, thermal management, and charging systems widened the appeal of electric options in parks, estates, and tourism operations. Regulatory support for low-emission transport opened new opportunities for manufacturers. As more fleets evaluated long-term operating savings, the electric segment emerged as a major growth avenue for upcoming product launches and investment.

- For instance, Polaris confirms the Ranger XP Kinetic produces 110 hp and 140 lb-ft of torque using its electric motor, based on Polaris corporate data.

Growing Fleet Demand from Defense and Public-Safety Agencies

Defense forces and rescue teams increased their use of ATVs and UTVs due to the vehicles’ agility, load-carrying capability, and ability to reach remote or dangerous areas quickly. These units supported border patrol, surveillance, and rapid-response tasks. Manufacturers gained opportunities by offering armored frames, communication systems, and enhanced lighting for tactical operations. The focus on lightweight mobility and fast deployment created strong prospects for specialized defense-grade and rescue-oriented models.

- For instance, Polaris Government & Defense lists the MRZR Alpha with a payload rating of up to 907 kg (2,000 lb) (for the four-seat variant) and a towing capacity of 680 kg (1,500 lb), confirmed through Polaris defense specifications.

Rising Customization and Aftermarket Upgrades

Users showed growing interest in tailored components such as improved tires, suspension kits, storage racks, lighting systems, and protective gear. The trend allowed buyers to modify vehicles for farming, hunting, patrolling, or recreational use. This expansion in aftermarket parts opened new revenue channels for manufacturers and dealers. Growing online sales and accessory bundles supported a wider customer base, making customization a significant opportunity for long-term market differentiation.

Key Challenges

High Maintenance Costs and Rising Component Prices

Growth faced pressure from increasing costs related to spare parts, labor, and routine service. Complex drivetrains, safety electronics, and advanced suspension systems required skilled maintenance, raising long-term ownership expense for commercial users and families. Higher prices for metal components and imported parts added further challenges. These cost barriers limited adoption in price-sensitive regions and made buyers reconsider upgrades or new vehicle purchases.

Safety Concerns and Regulatory Restrictions

Stringent rules on off-road vehicle operation, trail access, and speed control affected market expansion. Accident risks, especially among untrained riders, pushed regulators to tighten guidelines for helmets, age limits, and vehicle usage areas. Some regions imposed limits on riding zones to protect wildlife and reduce environmental impact. These restrictions reduced recreational access and created hurdles for tourism operators, limiting demand in certain markets despite rising interest.

Regional Analysis

North America

North America led the ATV and UTV Market in 2024 with about 52% share. Strong recreational culture, wide trail networks, and high demand from farming and ranching supported this leadership. The region also benefited from advanced product availability, strong dealership networks, and consistent fleet purchases from forestry, defense, and search-and-rescue units. Rising interest in outdoor tourism and hunting further expanded adoption. Major manufacturers in the United States and Canada introduced upgraded utility models, strengthening market presence across both recreational and utility applications.

Europe

Europe held nearly 21% share in 2024, driven by growing use of ATV and UTV units in agriculture, forestry, and mountain rescue. The region showed steady expansion due to strict safety standards and rising adoption in rural mobility tasks. Recreational usage also improved in Nordic and Alpine areas where off-road trails remained popular. Government programs promoting mechanization in small farms supported utility-driven demand. Fleet purchases increased in rescue services, vineyards, and estate management, helping the region maintain stable long-term growth.

Asia Pacific

Asia Pacific accounted for about 18% share in 2024, supported by rising agriculture mechanization and expanding adventure tourism. Countries such as China, India, Japan, and Australia increased use of these vehicles for patrol, plantation work, and commercial recreation. Growing interest in outdoor sports and desert riding contributed to higher sales in Southeast Asia and Oceania. Expanding local manufacturing and improving regional dealership networks helped reduce ownership costs. Commercial buyers also adopted UTVs for construction and mining site mobility, strengthening overall demand.

Latin America

Latin America captured nearly 6% share in 2024, mainly driven by demand from agriculture, ranching, and tourism activities. Brazil, Mexico, and Argentina showed steady adoption as operators required compact vehicles for field work and transport across uneven terrain. Growth also came from adventure parks and coastal tourism operators offering off-road rentals. Limited regional manufacturing and higher import duties slowed broader expansion, but improving distribution channels supported moderate growth. Utility-focused models gained traction in rural and semi-urban areas.

Middle East and Africa

demand due to strong interest in dune riding and adventure activities. Safari operators, farms, and construction sites adopted UTVs for logistics and mobility in remote terrains. Limited awareness and high vehicle prices restricted wider adoption across parts of Africa. However, gradual infrastructure development and tourism investments continued to support long-term opportunities.

Market Segmentations:

By Vehicle Type

By Displacement

- Less than 400cc

- 400 – 800cc

- More than 800cc

By Fuel Type

- Gasoline Powered

- Diesel-powered

- Electric Powered

- Solar Powered

By End User

- Agriculture

- Military

- Mountaineering

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the ATV and UTV Market is shaped by major companies including Polaris Inc., Honda Motor Corporation, John Deere, Textron Inc., Yamaha Motor Corporation, Kwang Yang Motor Company Ltd., Kawasaki Motors Corp, BRP, Kubota Corporation, and Suzuki Motor LLC. Market competition intensified as brands focused on advanced off-road capability, stronger suspension systems, and improved cabin safety to attract both recreational and utility buyers. Manufacturers expanded portfolios with electric and hybrid options to meet rising demand for low-noise and low-emission vehicles. Companies strengthened distribution networks, offered flexible financing, and enhanced aftersales support to retain customers. Product upgrades, digital dashboards, and driver-assist technologies further differentiated offerings across global markets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Polaris Inc.

- Honda Motor Corporation

- John Deere

- Textron Inc.

- Yamaha Motor Corporation

- Kwang Yang Motor Company Ltd.

- Kawasaki Motors Corp

- BRP

- Kubota Corporation

- Suzuki Motor LLC

Recent Developments

- In 2025, Kawasaki Motors Corp. unveiled its highly anticipated 2026 supercharged H2 UTV lineup. The lineup includes the Teryx4 H2 (a true four-seater model) and the all-new Teryx5 H2 (a five-seater model with a rear bench seat).

- In 2024, Yamaha Motor Corporation launched its 2025 Proven Off-Road lineup including new RMAX4 1000 models, enhanced On-Command 4WD, a new Turf Mode, and higher output Electric Power Steering (EPS).

- In 2023, Suzuki Motor USA, LLC announced updates for the returning 2024 and 2025 KingQuad 750 and KingQuad 500 ATV models.

Report Coverage

The research report offers an in-depth analysis based on Vehicle Type, Displacement, Fuel Type, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will grow steadily as utility and recreational demand increases worldwide.

- Electric ATV and UTV models will gain stronger adoption due to lower maintenance needs.

- Safety technologies will improve, making vehicles more stable and easier to operate.

- Fleet purchases from agriculture, forestry, and construction will expand further.

- Tourism operators will increase investments to support rising off-road adventure activities.

- Defense and public-safety agencies will widen use of lightweight tactical UTV fleets.

- Customization and aftermarket upgrades will attract more buyers across all regions.

- Manufacturers will introduce more hybrid and low-emission models to meet regulations.

- Dealer networks will grow across Asia and Latin America to improve accessibility.

- Digital features such as GPS support and telematics will become standard in new models.