Biochemical Reagents Market Overview:

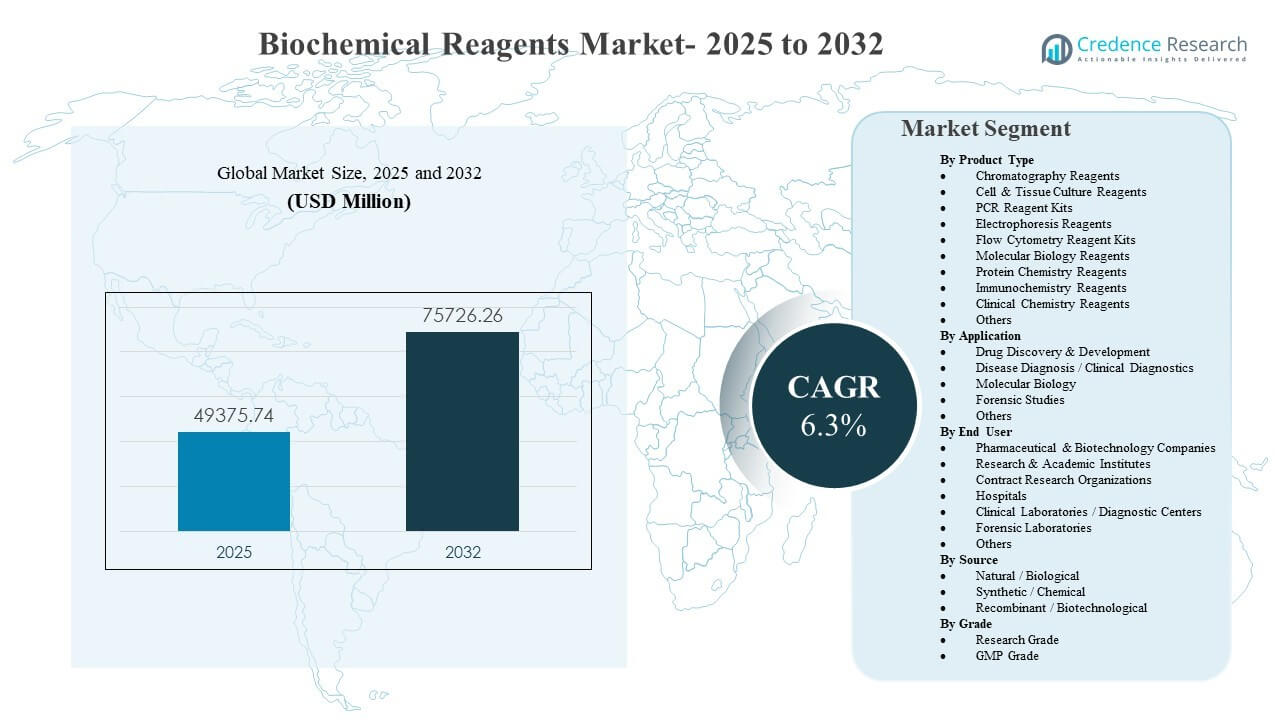

The global Biochemical Reagents Market size was estimated at USD 49,375.74 million in 2025 and is expected to reach USD 75,726.26 million by 2032, growing at a CAGR of 6.3% from 2025 to 2032. Growth is primarily driven by expanding biochemical and molecular workflows across biopharma R&D, academic research, and routine diagnostics, which increase recurring consumption of standardized, validated reagent kits and consumables. The Biochemical Reagents Market also benefits from wider adoption of lab automation, higher assay throughput, and stricter quality expectations that shift purchasing toward consistent, high-performance reagent formats across multi-site laboratories.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Biochemical Reagents Market Size 2025 |

USD 49,375.74 million |

| Biochemical Reagents Market, CAGR |

6.3% |

| Biochemical Reagents Market Size 2032 |

USD 75,726.26 million |

Key Market Trends & Insights

- The Biochemical Reagents Market is projected to expand from USD 49,375.74 million (2025) to USD 75,726.26 million (2032) at a 6.3% CAGR (2025–2032).

- North America accounted for 37.9% in 2025, reflecting strong demand concentration across biopharma R&D, advanced diagnostics, and well-funded research ecosystems.

- Molecular Biology Reagents held 22.8% share in 2025, supported by broad use across PCR-centric workflows, sample prep, and nucleic-acid quantification routines.

- Research & Academic Institutes represented 33.2% in 2025, sustained by high purchasing frequency, diverse experimental workflows, and grant-funded procurement cycles.

- Asia Pacific reached 24.1% share in 2025, indicating near-parity with Europe driven by expanding tertiary research capacity and growing installed base of modern lab instrumentation.

Segment Analysis

The Biochemical Reagents Market shows recurring demand characteristics because many workflows require repeat purchases tied to assay throughput rather than one-time capital buys. Buyers increasingly prioritize batch-to-batch consistency, validated performance, and time-saving formats such as ready-to-use mixes and integrated kits to reduce variability in results. Procurement also favors suppliers that offer broad portfolios across core assays, sample preparation, and analytical workflows to simplify vendor consolidation and technical support.

Demand intensity varies by workflow complexity and compliance requirements. Research-grade reagents remain central for exploratory applications, but quality management expectations in translational research and regulated testing increase adoption of higher documentation standards. Growth also reflects higher utilization of multi-omics and targeted molecular workflows, which expands consumption of nucleic-acid and protein-related reagents across both research and clinical-adjacent laboratories.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product Type Insights

Molecular Biology Reagents accounted for the largest share of 22.8% in 2025. Molecular Biology Reagents benefit from broad applicability across PCR-based testing, routine nucleic-acid workflows, and standardized assays that drive repeat purchasing. Molecular Biology Reagents also gain from expanding automation and higher sample throughput, which increases reagent pull-through. Molecular Biology Reagents remain supported by research programs that prioritize sensitivity, reproducibility, and validated performance across multi-site laboratories.

By Application Insights

Drug discovery and disease diagnosis workflows remain core consumption centers because biochemical assays, cell-based workflows, and clinical testing require frequent replenishment of reagents. Application mix is increasingly shaped by higher assay throughput, workflow standardization, and adoption of validated kits that reduce hands-on time. Application purchasing decisions also reflect assay performance requirements, compatibility with installed instrumentation, and availability of technical support and documentation.

By End User Insights

Research & Academic Institutes accounted for the largest share of 33.2% in 2025. Research & Academic Institutes sustain high demand due to broad experimental diversity, high frequency of routine laboratory protocols, and recurring procurement funded through institutional budgets and grants. Research & Academic Institutes also support stable baseline consumption across core molecular biology, protein chemistry, and cell culture workflows. Research & Academic Institutes increasingly emphasize reproducibility and standardized inputs, which supports demand for validated reagent kits and consistent quality.

By Source Insights

Natural/biological, synthetic/chemical, and recombinant/biotechnological sourcing options serve different performance, reproducibility, and documentation needs. Recombinant/biotechnological sourcing is gaining importance as buyers prioritize higher specificity, reduced variability, and better alignment with advanced therapy and complex molecular workflows. Source choice is also influenced by downstream application sensitivity, regulatory expectations, and quality system requirements across research-to-production transitions.

By Grade Insights

Research grade remains essential for exploratory and hypothesis-driven studies, but GMP grade demand rises as workflows transition into regulated testing, clinical validation, and manufacturing-linked quality systems. Grade selection increasingly depends on traceability requirements, documentation depth, and supplier validation packages. Grade dynamics also reflect the growing overlap between translational research and clinical-adjacent laboratory operations.

Biochemical Reagents Market Drivers

Expansion of biopharma R&D and translational research

Biopharma pipelines increasingly rely on biochemical assays, cell-based workflows, and molecular readouts that require frequent reagent replenishment. Higher study volumes and broader modality mix increase consumption across chromatography, immunochemistry, and molecular biology reagent families. Standardization initiatives in R&D labs reinforce preference for validated reagent kits that improve reproducibility across sites. Supplier portfolios that bundle reagents with workflow guidance and technical support benefit from consolidation trends.

- For instance, Qiagen notes that its QIAamp nucleic acid extraction kits are validated in more than 500 peer‑reviewed studies, with inter‑laboratory variation in yield typically below 10% when SOPs are followed, supporting multi‑site translational research programs.

Rising diagnostic and clinical-adjacent testing volumes

Routine diagnostics and clinical laboratory workflows expand demand for reagent kits that deliver consistent performance and strong quality control. Growing testing intensity increases the pull-through of PCR reagent kits, clinical chemistry reagents, and immunochemistry reagents. Laboratories also prioritize throughput and reliability, which supports adoption of ready-to-use formulations and automated-compatible consumables. Documentation and performance validation requirements strengthen preference for suppliers with established quality systems.

- For instance, Bio‑Rad’s fully automated BioPlex 2200 multiplex system can deliver up to 1,400 autoimmune and up to 400 infectious disease results per hour, nearly three times more autoimmune results per hour than the closest competitor, illustrating how reagent+system bundles reshape consumable usage patterns.

Growth of lab automation and higher sample throughput

Automation adoption increases reagent usage predictability and supports recurring purchasing tied to instrument utilization. Integrated workflows reduce manual variability, creating demand for standardized inputs and validated reagent formats. High-throughput environments also favor suppliers that provide consistent lot performance and stable supply continuity. Automation-linked procurement commonly emphasizes compatibility, workflow reliability, and service responsiveness.

Increasing emphasis on reproducibility and quality compliance

Reproducibility concerns push buyers toward suppliers that provide consistent performance, clear specifications, and robust validation data. Quality expectations expand demand for higher documentation, traceability, and standardized kit-based workflows across research and regulated testing environments. Quality-driven procurement also reinforces vendor consolidation as laboratories standardize materials across teams and sites. These dynamics support premiumization for performance-critical reagents and higher grade options in sensitive workflows.

Biochemical Reagents Market Challenges

Cost sensitivity remains a constraint in many laboratories because recurring reagent spending competes with instrument upgrades and staffing budgets. Budget pressure increases evaluation of total workflow cost, including failure rates, re-testing, and time-to-result, which can delay conversion to premium or specialized reagents. Supply continuity and lot-to-lot variability also create risk for standardized workflows, especially where protocols depend on strict performance tolerances. Procurement cycles can be lengthy when laboratories require extended validation for supplier changes.

- For instance, QBench documented that laboratories tracking specimen rejection rate and first-pass yield found that even a 3–4% specimen rejection rate translated into significant reagent waste, leading one multi-site lab network to link reagent selection to achieving first-pass yields above 95% to justify any reagent upgrade.

Technical qualification requirements can slow adoption of new reagent formats because laboratories often require stability testing, protocol re-optimization, and documentation checks before switching suppliers. Regulatory and quality expectations increase the burden of validation, particularly for diagnostic-adjacent use cases and GMP-aligned workflows. Fragmentation of end-user needs across research and clinical environments makes portfolio positioning complex. Competitive pricing pressure can intensify where commoditized reagent categories face multiple equivalent alternatives.

Biochemical Reagents Market Trends and Opportunities

Kit-based workflows and ready-to-use formulations continue to expand as laboratories seek faster setup, reduced variability, and higher throughput. Workflow standardization supports broader adoption of integrated reagent systems that align with instrument platforms and automation pipelines. Vendors that provide validated protocols, strong lot consistency, and clear documentation are better positioned to win consolidated procurement. These trends also increase recurring demand through stronger pull-through from installed workflows.

- For instance, Thermo Fisher Scientific says its Ion Chef System cuts setup time to 15 minutes, keeps total hands-on time below 45 minutes, and can prepare up to 8 Ion AmpliSeq libraries or 2 sequence-ready chips per run, underscoring how validated reagent-instrument pairing can improve reproducibility and throughput in routine laboratory workflows.

Growth opportunities are strengthening in high-complexity molecular workflows and advanced research applications where performance differentiation is measurable. Recombinant and biotechnological reagents gain traction as laboratories prioritize specificity, reproducibility, and reduced background noise in sensitive assays. Demand also rises for reagents aligned with multi-omics workflows, next-generation sample preparation, and scalable analytics. Regional expansion opportunities improve as laboratory infrastructure and research capacity expand in emerging markets.

Regional Insights

North America

North America held 37.9% share in 2025, supported by strong biopharma R&D intensity, mature diagnostics infrastructure, and high adoption of standardized reagent workflows. Procurement commonly favors validated performance, consistent supply, and robust technical support to sustain high-throughput operations. Demand is reinforced by large installed bases of advanced instrumentation and broad use of molecular and protein assays. Competitive activity emphasizes portfolio breadth, workflow integration, and reliability across multi-site laboratory networks.

Europe

Europe captured 24.7% share in 2025, supported by strong academic research networks and well-established laboratory capacity across major countries. Purchasing priorities typically include quality compliance, workflow standardization, and cost effectiveness across public and private systems. Demand remains steady across clinical-adjacent testing and research workflows, with replacement and upgrade cycles supporting ongoing reagent consumption. Vendor success often depends on meeting documentation requirements, supply reliability, and interoperability with installed platforms.

Asia Pacific

Asia Pacific represented 24.1% share in 2025, driven by expanding research capacity, rising diagnostic activity, and increased instrumentation penetration in large urban centers. Growth is supported by broader access to advanced workflows and increasing adoption of standardized kits in high-throughput laboratories. Market demand varies by country due to funding levels, reimbursement environments, and procurement maturity. Vendors benefit from scalable portfolios, strong distribution, and localized technical support that improves adoption.

Latin America

Latin America held 7.1% share in 2025, with demand concentrated in major urban centers and leading research and diagnostic hubs. Procurement often prioritizes cost efficiency, dependable supply, and flexible pack sizes suitable for variable throughput. Growth is supported by gradual modernization of laboratory infrastructure and increasing demand for routine testing and research workflows. Supplier performance depends on channel strength, service coverage, and consistent availability.

Middle East & Africa

Middle East & Africa accounted for 6.2% share in 2025, supported by targeted investments in healthcare modernization and laboratory capacity in select countries. Demand is concentrated in centralized laboratories, tertiary hospitals, and national reference facilities that prioritize standardized workflows. Growth opportunities rise with infrastructure investments and higher diagnostic testing intensity in major cities. Distribution strength, training support, and supply continuity are key success factors across heterogeneous end-user environments.

Competitive Landscape

The Biochemical Reagents Market remains competitive with suppliers differentiating through portfolio breadth, workflow compatibility, validation support, and supply reliability. Product strategy increasingly emphasizes integrated kits, automation-ready formats, and consistent lot performance to support standardized laboratory operations. Commercial differentiation also relies on technical support quality, documentation depth, and the ability to serve multiple end-user segments ranging from academic research to regulated clinical-adjacent workflows.

Thermo Fisher Scientific Inc. maintains strong positioning through broad reagent portfolios aligned to molecular biology, analytical workflows, and laboratory standardization requirements. Thermo Fisher Scientific Inc. also benefits from workflow-aligned product ecosystems that support repeat purchasing through laboratory pull-through. Thermo Fisher Scientific Inc. continues to compete on performance validation, availability, and support services that reduce operational risk in high-throughput laboratory settings.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Bio-Rad Laboratories, Inc.

- Agilent Technologies, Inc.

- QIAGEN N.V.

- Takara Bio Inc.

- Promega Corporation

- Danaher Corporation

- F. Hoffmann-La Roche Ltd.

- Abbott Laboratories

- Becton, Dickinson and Company

- Waters Corporation

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In March 2025, Thermo Fisher Scientific launched its next-generation high-throughput biochemical reagents for protein and nucleic acid analysis, with the portfolio positioned to improve laboratory efficiency in life sciences research.

- In October 2025, Saguaro Biosciences announced a distribution partnership with Bio-Techne to expand global access to Saguaro’s live-cell imaging reagents, including ChromaLIVE, NucleoLIVE, and MortaLIVE dyes.

- In October 2025, Merck KGaA, through its MilliporeSigma life science business, agreed to acquire Mirus Bio for about 600 million dollars to strengthen its viral vector–based gene therapy tools, particularly transfection reagents critical for advanced biotherapeutic development.

- In March 2026, Thermo Fisher Scientific Inc. announced new color-based (chromogenic) culture media designed to help laboratories detect Candida infections more rapidly, extending its clinical microbiology reagents portfolio for routine diagnostic use.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 49,375.74 million |

| Revenue forecast in 2032 |

USD 75,726.26 million |

| Growth rate (CAGR) |

6.3% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Type; By Application; By End User; By Source; By Grade |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Thermo Fisher Scientific Inc., Merck KGaA, Bio-Rad Laboratories, Inc., Agilent Technologies, Inc., QIAGEN N.V., Takara Bio Inc., Promega Corporation, Danaher Corporation, F. Hoffmann-La Roche Ltd., Abbott Laboratories, Becton, Dickinson and Company, Waters Corporation. |

| No. of Pages |

340 |

Segmentation

Product Type

- Chromatography Reagents

- Cell & Tissue Culture Reagents

- PCR Reagent Kits

- Electrophoresis Reagents

- Flow Cytometry Reagent Kits

- Molecular Biology Reagents

- Protein Chemistry Reagents

- Immunochemistry Reagents

- Clinical Chemistry Reagents

- Others

Application

- Drug Discovery & Development

- Disease Diagnosis / Clinical Diagnostics

- Molecular Biology

- Forensic Studies

- Others

End User

- Pharmaceutical & Biotechnology Companies

- Research & Academic Institutes

- Contract Research Organizations

- Hospitals

- Clinical Laboratories / Diagnostic Centers

- Forensic Laboratories

- Others

Source

- Natural / Biological

- Synthetic / Chemical

- Recombinant / Biotechnological

Grade

Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa