Butterfly Needle Sets Market

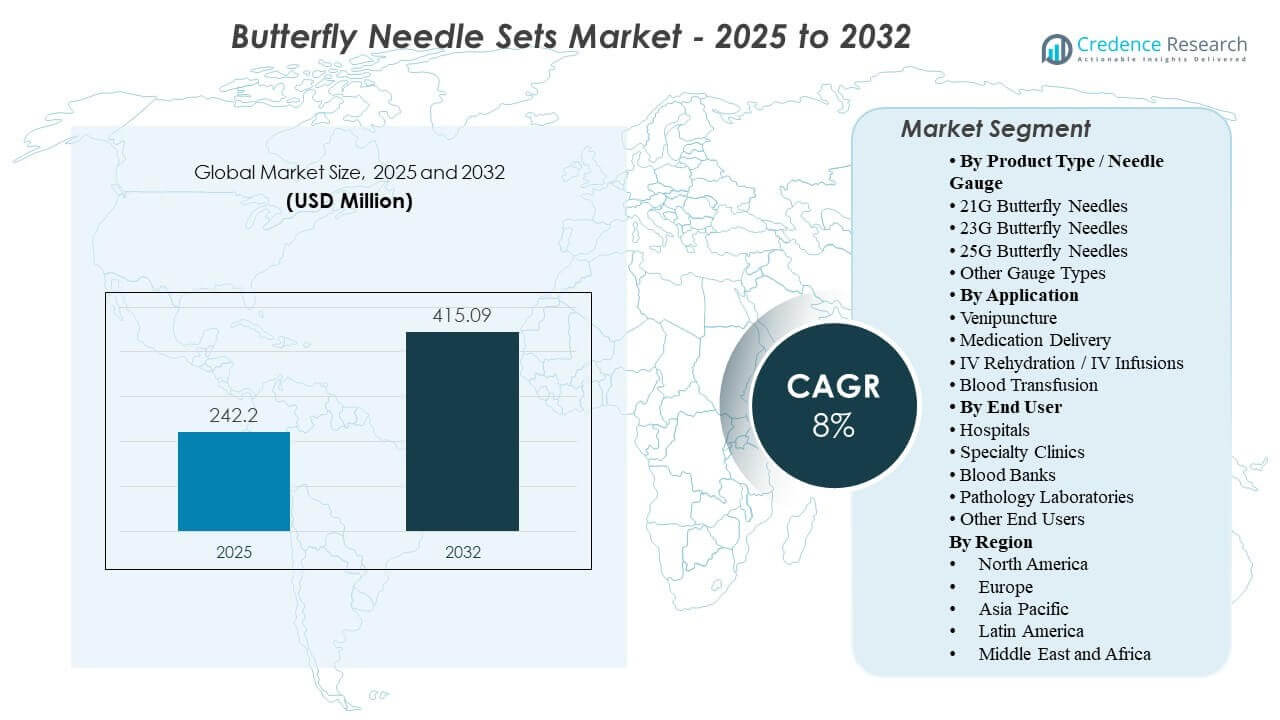

The global Butterfly Needle Sets Market size was estimated at USD 242.2 million in 2025 and is expected to reach USD 415.09 million by 2032, growing at a CAGR of 8% from 2025 to 2032. Growth is primarily supported by the sustained increase in routine blood collection and short-duration infusion procedures across hospitals, diagnostic laboratories, and outpatient settings where stable venous access and consistent first-stick performance are critical. Demand remains strongest in mature healthcare systems, while expanding diagnostic capacity in emerging markets continues to broaden the installed base of blood collection consumables.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Butterfly Needle Sets Market Size 2025 |

USD 242.2 Million |

| Butterfly Needle Sets Market, CAGR |

8% |

| Butterfly Needle Sets Market Size 2032 |

USD 415.09 Million |

Key Market Trends & Insights

- The Butterfly Needle Sets Market is projected to expand from USD 242.2 million (2025) to USD 415.09 million (2032) at a CAGR of 8% (2025–2032).

- 23G Butterfly Needles represented 42.0% share in 2025, reflecting broad preference for balancing flow performance and patient comfort in routine venipuncture.

- Blood Transfusion accounted for 61.3% share in 2025, indicating continued reliance on butterfly sets for controlled access in transfusion-related workflows.

- Hospitals contributed 56.5% share in 2025, supported by high procedure volumes across inpatient, emergency, and perioperative pathways.

- North America held 38.9% share in 2025, driven by high diagnostic testing intensity and standardized procurement across large provider networks.

Segment Analysis

The Butterfly Needle Sets Market is shaped by repeat-use clinical workflows where buyers prioritize handling stability, patient comfort, and consistent performance across high-throughput phlebotomy environments. Purchasing decisions typically focus on gauge standardization, ease of use across varying staff experience levels, and compatibility with established blood collection and infusion routines. Safety expectations also influence adoption as healthcare providers emphasize sharps-injury reduction practices and standardized training for routine venous access procedures.

Segment performance is also influenced by the increasing clinical burden of chronic disease monitoring that requires frequent blood draws, alongside growing preventive screening volumes. Gauge selection reflects trade-offs between flow rate requirements and vein fragility across adult, pediatric, and geriatric populations. Application demand remains concentrated in transfusion and related blood access workflows where stability and control are important for short-duration access. End-user concentration in hospitals persists due to scale and procedural density, although blood banks and diagnostic networks continue to increase consumption as collection footprints expand.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product Type / Needle Gauge Insights

23G Butterfly Needles accounted for the largest share of 42.0% in 2025. The 23G gauge leads because it supports routine venipuncture with a practical balance of flow efficiency and patient comfort in everyday clinical settings. Healthcare providers often standardize around 23G to reduce variation across staff technique and to simplify procurement and inventory planning. The gauge is also well aligned with high-volume blood collection workflows in hospitals and laboratories that prioritize consistent first-stick outcomes.

By Application Insights

Blood Transfusion accounted for the largest share of 61.3% in 2025. Blood transfusion leads because transfusion-related workflows require controlled venous access across diverse patient populations, including patients with fragile veins and complex care needs. Butterfly needle sets are frequently used where stability and handling control support monitored administration and short-duration access needs. High transfusion procedure intensity in acute-care environments reinforces recurring consumption and sustained demand in this application.

By End User Insights

Hospitals accounted for the largest share of 56.5% in 2025. Hospitals lead because they concentrate large volumes of venipuncture, infusion, and transfusion procedures across multiple departments and patient acuity levels. Hospital procurement teams typically standardize consumables to support consistent training, protocol adherence, and supply-chain efficiency across wards and outpatient departments. Centralized purchasing and high daily throughput sustain higher unit consumption compared with smaller specialty clinics and standalone facilities.

Butterfly Needle Sets Market Drivers

Growth in routine diagnostic testing and chronic disease monitoring

Rising diagnostic testing volumes support steady demand for butterfly needle sets across hospitals and laboratories. Chronic disease management requires repeated blood draws for monitoring and therapy optimization, increasing procedure frequency over time. Screening programs also expand routine collection volumes, particularly in mature healthcare systems. These dynamics elevate the importance of reliable venous access tools that support consistent performance and efficient patient throughput.

- For instance, Becton Dickinson’s BD Vacutainer UltraTouch Push Button Blood Collection Set combines a 25G 5-bevel needle with an ultra-thin wall cannula, lowering penetration force to 34.5 g versus 50.6 g for a traditional 23G wingset, a 32% reduction, while 56% of pediatric patients reported no pain and 5 mL tube fill times were reduced by 50% versus BD’s 23G push-button wingset.

Sharps safety practices and workflow standardization in healthcare facilities

Healthcare facilities increasingly adopt standardized consumables to reduce variability and support safer clinical practice. Butterfly needle sets benefit when organizations implement consistent phlebotomy protocols that emphasize handling control and predictable performance. Training alignment across large staff pools increases demand for products that are easy to use and support consistent outcomes. Safety-driven purchasing also encourages replacement cycles and vendor consolidation with suppliers that can support supply reliability.

Expansion of outpatient care and specialty service delivery

Outpatient care growth increases venipuncture and short-duration infusion procedures outside the hospital core. Specialty clinics and ambulatory centers value devices that streamline workflow, reduce setup time, and support patient experience objectives. Butterfly needle sets align with these priorities in routine blood draws and short access needs. As care delivery shifts toward distributed networks, consumption grows across a wider range of sites.

- For instance, Greiner Bio-One’s VACUETTE Safety Blood Collection Set is designed for blood collection or infusions for up to 5 hours and is offered in 21G and 23G formats with 19 cm and 30 cm tubing options, which fits the operational needs of ambulatory and specialty care settings handling short-duration access procedures.

Scaling of blood collection infrastructure and collection-point networks

Blood banks and diagnostic networks continue to expand collection footprints, increasing the volume of routine blood access procedures. Growth in collection sites increases recurring consumable demand and strengthens supplier opportunities for standardized gauge portfolios. Operational efficiency requirements in collection settings drive preference for consistent products and dependable distribution coverage. This expansion supports both volume growth and broader geographic adoption.

Butterfly Needle Sets Market Challenges

Procurement-driven price pressure remains a persistent challenge because butterfly needle sets are high-volume consumables often purchased under competitive tenders and framework agreements. Buyers may prioritize unit cost unless operational efficiency or safety benefits are clearly demonstrated, which can limit supplier differentiation. Frequent contract rebids can compress margins and increase pricing volatility across regions. Cost sensitivity is particularly pronounced in price-regulated markets and in systems with centralized purchasing controls.

- For example, BD says its Vacutainer UltraTouch Push Button Blood Collection Set enables single-handed, in-vein needle retraction and can cut accidental needlesticks by up to 88% versus traditional wingsets. In one hospital rollout cited at launch, butterfly-needle needlestick injuries dropped 88%, with zero incidents in the final 21 months, supporting premium pricing based on measurable safety gains.

Operational variability across end users can also constrain uniform adoption because procedure mix, staff training intensity, and protocol adherence differ widely between hospitals, clinics, and laboratories. Inventory complexity increases when facilities carry multiple gauges and configurations to serve diverse patient groups, raising logistics and forecasting requirements. Supply disruptions can quickly impact routine operations due to the essential nature of blood collection supplies. These factors can extend evaluation cycles and slow product conversions for large accounts.

Butterfly Needle Sets Market Trends and Opportunities

Healthcare systems are increasingly optimizing gauge mix and standardizing preferred configurations to improve workflow consistency across sites. Suppliers that provide broad gauge portfolios and support training-friendly product selection can strengthen long-term account retention. Opportunities also expand through distribution partnerships that improve availability across outpatient networks and collection centers. Product positioning that emphasizes ease of use and procedural consistency can support wins in high-throughput settings.

Growth in diagnostic capacity across emerging markets creates opportunities as laboratories and collection networks expand and formalize standardized practices. Facilities seek dependable supply, stable performance, and simplified inventory management as procedure volumes rise. Companies that can support local distribution and consistent fulfillment can accelerate adoption in underserved regions. Targeted offerings for pediatric, geriatric, and difficult-access segments also provide a practical differentiation route.

- For instance, Nipro’s Blood Collection Set is available in 21G, 22G, and 23G variants with minimum flow rates of 15.0 ml/min, 12.0 ml/min, and 7.0 ml/min respectively at 190 mm tubing and a 0.39 ml priming volume across all three versions.

Regional Insights

North America

North America accounted for 38.9% of revenue in 2025. Regional demand is supported by high diagnostic testing intensity and strong utilization across hospitals, laboratories, and outpatient centers. Standardized procurement and protocol-driven phlebotomy workflows contribute to consistent product consumption. Mature distribution networks and stable purchasing cycles support recurring demand across large provider systems.

Europe

Europe accounted for 27.4% of revenue in 2025. Demand is supported by established healthcare infrastructure and sustained routine diagnostic activity in hospital and outpatient settings. Procurement systems emphasize standardization and supply continuity, reinforcing steady consumable usage. Growth opportunities remain linked to expanding outpatient services and continued focus on workflow efficiency in blood collection.

Asia Pacific

Asia Pacific accounted for 22.7% of revenue in 2025. Expansion in healthcare access and diagnostic testing capacity supports rising procedure volumes, particularly in major urban centers. Growth is reinforced by scaling hospital throughput and broader laboratory network development. Improving procurement formalization and distribution coverage continues to expand market penetration across the region.

Latin America

Latin America accounted for 6.6% of revenue in 2025. Demand is concentrated in large metropolitan healthcare systems and diagnostic laboratories where routine blood collection volumes are highest. Cost sensitivity influences product selection and procurement outcomes, emphasizing value and distribution reliability. Expanding outpatient services and laboratory access support gradual demand growth over time.

Middle East & Africa

Middle East & Africa accounted for 4.4% of revenue in 2025. Demand is supported by ongoing healthcare infrastructure investment in select markets and steady utilization in hospitals and diagnostic facilities. Growth is uneven across countries due to differences in funding levels, procurement maturity, and access to routine diagnostics. Opportunities are strongest where private healthcare networks and centralized hospital systems are expanding.

Competitive Landscape

The Butterfly Needle Sets Market is competitive and shaped by gauge portfolio breadth, supply reliability, and the ability to support standardized clinical workflows across large healthcare accounts. Manufacturers differentiate through consistent product performance, ease of handling, training simplicity, and distribution reach, particularly in tender-based procurement environments. Competitive positioning also reflects supplier capability to maintain quality and continuity at scale for high-volume hospital and laboratory demand. Strategic priorities often include contract wins with integrated delivery networks, distributor alignment, and incremental product refinements that improve usability and procedure consistency.

Becton, Dickinson and Company (BD) remains a leading participant through scale manufacturing, broad medical consumables coverage, and strong relationships with large healthcare systems. BD commonly focuses on supply continuity, consistent product specifications, and alignment with standardized clinical protocols across multi-site provider networks. BD’s approach supports recurring demand in high-throughput hospital and diagnostic settings where procurement favors dependable fulfillment and uniform device performance. Investments in production and operational resilience strengthen BD’s competitiveness in long-term contracts and high-volume channels.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In December 2024, Haemonetics announced a definitive agreement to sell its whole blood assets to GVS, S.p.A., marking an acquisition-related update relevant to companies involved in blood collection systems. The transaction covers Haemonetics’ portfolio of proprietary whole blood collection, processing, and filtration solutions, along with manufacturing assets in Covina, California, and related equipment in Tijuana, Mexico.

- In November 2024, Terumo Blood and Cell Technologies announced a strategic partnership with Terumo Medical Products (Hangzhou) Co., Ltd. and said it would invest in the Hangzhou production facility to support locally made medical products for China. The company stated that the site would manufacture devices used to collect and separate blood and cells, linking the partnership to the broader blood collection device ecosystem that includes butterfly needle set participants.

- In April 2024, BD (Becton, Dickinson, and Company) launched the BD Vacutainer UltraTouch Push Button Blood Collection Set in India, making it one of the clearest recent product launches tied to the butterfly-style blood collection segment. The company said the device was designed to reduce patient pain, improve single-prick success, and use RightGauge, PentaPoint, and push-button safety technologies during blood collection.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 242.2 million |

| Revenue forecast in 2032 |

USD 415.09 million |

| Growth rate (CAGR) |

8% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2025–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Type / Needle Gauge; By Application; By End User |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Becton, Dickinson and Company (BD), Terumo Corporation, Cardinal Health, Inc., Nipro Corporation, ICU Medical, Inc., Smiths Medical, B. Braun Melsungen AG, Medline Industries, Inc., Kawasumi Laboratories, Inc., ISO-MED, BioMatrix S.r.l. |

| No. of Pages |

330 |

Segmentation

By Product Type / Needle Gauge

- 21G Butterfly Needles

- 23G Butterfly Needles

- 25G Butterfly Needles

- Other Gauge Types

By Application

- Venipuncture

- Medication Delivery

- IV Rehydration / IV Infusions

- Blood Transfusion

By End User

- Hospitals

- Specialty Clinics

- Blood Banks

- Pathology Laboratories

- Other End Users

By Region

-

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa