| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Canada Industrial Solvents Market Size 2024 |

USD 1,167.12 Million |

| Canada Industrial Solvents Market, CAGR |

6.56% |

| Canada Industrial Solvents Market Size 2032 |

USD 1,940.86 Million |

Market Overview

Canada Industrial Solvents Market size was valued at USD 1,167.12 million in 2024 and is anticipated to reach USD 1,940.86 million by 2032, at a CAGR of 6.56% during the forecast period (2024-2032).

The Canada Industrial Solvents market is driven by increasing demand across industries such as pharmaceuticals, chemicals, paints and coatings, and adhesives, where solvents play a vital role in production processes. The growing focus on sustainability is also influencing market trends, with rising adoption of eco-friendly and bio-based solvents that meet environmental regulations. Additionally, innovations in solvent formulations, such as the development of high-performance, low-toxicity alternatives, are expanding market opportunities. The expansion of the manufacturing sector, particularly in automotive and construction, is further fueling the demand for industrial solvents. Furthermore, technological advancements in solvent extraction and purification processes are improving operational efficiency and reducing costs, which benefits industries relying on solvents for production. These factors, combined with strong economic growth, are expected to continue driving the market’s expansion in the coming years.

The Canada Industrial Solvents market is characterized by regional variations, with key demand originating from provinces like Ontario, Quebec, and British Columbia due to their robust industrial bases. Ontario leads the market, driven by manufacturing, automotive, and chemical industries, while Quebec’s chemical and pharmaceutical sectors contribute significantly to solvent consumption. Western Canada, although smaller in market share, is influenced by its strong oil and gas industry, driving demand for solvents in extraction and refining processes. The market is also shaped by the increasing adoption of eco-friendly solvents across these regions, as companies align with sustainability trends and stricter environmental regulations. Key players in the Canadian industrial solvents market include global giants such as Dow Inc., ExxonMobil, Eastman Chemical, and Huntsman Corporation, which supply a wide range of solvents used across various industries like paints, coatings, pharmaceuticals, and adhesives. Their ongoing innovations and focus on sustainability continue to shape market dynamics.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Canada Industrial Solvents market was valued at USD 1,167.12 million in 2024 and is projected to reach USD 1,940.86 million by 2032, growing at a CAGR of 6.56% from 2024 to 2032.

- The global industrial solvents market was valued at USD 34,660.50 million in 2024 and is expected to reach USD 60,647.79 million by 2032, growing at a CAGR of 7.24% during the forecast period (2024-2032).

- Increasing demand for industrial solvents across key industries such as pharmaceuticals, paints, and coatings is driving market growth.

- The shift towards eco-friendly, bio-based, and low-toxicity solvents is a significant market trend due to growing sustainability concerns and strict environmental regulations.

- Technological advancements in solvent formulations and recovery processes are enhancing product efficiency and reducing operational costs.

- The market faces challenges due to regulatory pressures and high compliance costs, which can impact product development and market entry for smaller players.

- Ontario and Quebec dominate the market, driven by strong industrial sectors, while Western Canada and British Columbia also contribute to demand with specialized applications.

- Key players such as Dow Inc., ExxonMobil, and Eastman Chemical maintain a competitive edge with their wide product portfolios and focus on sustainability.

Report Scope

This report segments the Canada Industrial Solvents Market as follows:

Market Drivers

Growing Demand Across Key Industries

One of the primary drivers of the Canada Industrial Solvents market is the increasing demand for solvents across key industries such as pharmaceuticals, chemicals, paints and coatings, adhesives, and personal care. For instance, the Industry Sector Intelligence provides market intelligence and business resources for various industry sectors, including manufacturing, construction, and consumer products, reinforcing the growing demand for industrial solvents. In the pharmaceutical sector, solvents are integral in drug manufacturing, where they are used for the production of active ingredients and formulations. The chemical industry also relies heavily on solvents for processes such as polymerization, cleaning, and extraction. The paints and coatings sector benefits from solvents for thinning paints and improving application properties, while the adhesives industry uses solvents for the creation of high-performance bonding agents. As these industries expand in response to consumer demand, the need for industrial solvents is expected to grow accordingly.

Sustainability and Eco-friendly Solutions

The growing emphasis on sustainability is driving a shift toward the use of eco-friendly and bio-based solvents in the Canada market. For instance, the Government of Canada Green Solutions Investment discusses federal investments in manufacturers adopting environmentally friendly technologies, supporting the transition to a greener economy. Eco-friendly solvents, derived from renewable resources such as plant-based materials, are gaining popularity as they offer lower toxicity levels and a reduced environmental footprint. This trend is particularly important in industries such as paints and coatings, where low-VOC solvents are becoming the standard. The adoption of sustainable solvents is not only meeting regulatory requirements but is also enhancing the reputation of manufacturers who prioritize environmental responsibility. As demand for greener solutions grows, the market for eco-friendly industrial solvents is likely to expand significantly.

Technological Advancements and Innovation

Technological advancements and innovation in the development of high-performance solvents are playing a crucial role in driving the growth of the industrial solvents market in Canada. Manufacturers are increasingly focused on improving the efficiency, safety, and functionality of solvents through research and development. Innovations such as the development of solvent blends with improved solubility, reduced toxicity, and better overall performance are meeting the evolving needs of industries. In addition, new solvent extraction and purification techniques are making the production processes more cost-effective and sustainable. Automation in solvent manufacturing and enhanced solvent recovery technologies are reducing operational costs, increasing productivity, and minimizing waste, thus contributing to the market’s growth. These advancements are making industrial solvents more versatile and efficient, further driving their adoption across various sectors.

Economic Growth and Industrial Expansion

Economic growth and the expansion of manufacturing and construction sectors in Canada are key factors contributing to the increasing demand for industrial solvents. As Canada’s economy continues to grow, the demand for construction materials, automotive products, and consumer goods rises, which in turn drives the need for industrial solvents in the production process. In particular, the automotive sector relies heavily on solvents for tasks such as surface cleaning, paint application, and manufacturing of interior materials. Similarly, the construction industry uses solvents in the production of adhesives, coatings, and sealants. The overall expansion of manufacturing capacity in Canada, supported by investments in infrastructure, is further fueling the demand for solvents. As industries continue to grow and diversify, industrial solvents will remain a critical component in a wide range of manufacturing and production activities. This economic expansion presents a significant opportunity for the industrial solvents market to thrive.

Market Trends

Shift Towards Eco-friendly and Bio-based Solvents

A significant trend in the Canada Industrial Solvents market is the growing adoption of eco-friendly and bio-based solvents. Driven by stringent environmental regulations and consumer demand for sustainable products, industries are increasingly opting for solvents derived from renewable resources. For instance, the Green Analytical Approaches Review discusses advancements in eco-friendly solvent technologies, emphasizing their role in reducing environmental impact. These solvents offer reduced toxicity and lower volatile organic compound (VOC) emissions, aligning with Canada’s commitment to environmental sustainability. Applications in paints and coatings, adhesives, and pharmaceuticals are particularly prominent, as these sectors seek to minimize their ecological footprint while maintaining product performance.

Technological Advancements in Solvent Applications

Technological innovation is reshaping the industrial solvents landscape in Canada. Advancements in solvent formulations have led to the development of high-performance solvents with enhanced efficacy and reduced environmental impact. Industries such as electronics, aerospace, and healthcare are increasingly adopting precision cleaning methods that utilize specialized solvents to meet stringent cleanliness standards. Additionally, the rise of solvent blends and vapor degreasing techniques is enabling more efficient and residue-free cleaning processes, catering to the evolving needs of high-tech manufacturing sectors.

Regulatory Pressures and Compliance Challenges

The Canadian industrial solvents market is influenced by evolving regulatory frameworks aimed at reducing environmental and health risks associated with solvent use. For instance, the Impact of Regulatory Compliance Costs discusses the effects of regulatory burden on business performance, highlighting compliance challenges for industries. Stricter regulations concerning VOC emissions and hazardous substances are prompting manufacturers to reformulate products and adopt alternative solvents that comply with national and international standards. While these regulations drive innovation towards safer and more sustainable solvent options, they also present compliance challenges for manufacturers, necessitating investments in research and development to meet the new requirements.

Integration of Solvents in Emerging Industries

Emerging industries in Canada are increasingly integrating industrial solvents into their operations, further diversifying the market. The growth of sectors such as biotechnology, renewable energy, and advanced manufacturing is expanding the applications of solvents beyond traditional uses. In biotechnology, solvents are essential for processes like extraction and purification, while in renewable energy, they are used in the production of biofuels and energy storage systems. This diversification is contributing to the resilience and expansion of the industrial solvents market in Canada, as it adapts to the needs of these burgeoning industries.

Market Challenges Analysis

Regulatory and Environmental Challenges

One of the key challenges faced by the Canada Industrial Solvents market is the increasing complexity of regulatory requirements related to solvent use and emissions. The Canadian government has imposed strict environmental regulations, particularly concerning the reduction of volatile organic compounds (VOCs) and other hazardous chemicals. For instance, the Regulatory Accumulation discusses the impact of evolving regulations on economic growth, highlighting compliance challenges for industries. These regulations are prompting manufacturers to seek cleaner, eco-friendly alternatives, but the transition to such solvents can be costly and technically challenging. Developing and implementing new formulations that comply with these regulations while maintaining performance standards requires substantial investment in research and development. Additionally, compliance with both local and international environmental standards adds an extra layer of complexity for companies that operate in global markets. Meeting these regulations without compromising on efficiency or increasing costs poses a significant challenge for the industry.

Price Volatility and Supply Chain Disruptions

Price volatility and supply chain disruptions are other pressing challenges in the Canada Industrial Solvents market. The cost of raw materials, such as petrochemical derivatives, can fluctuate significantly due to factors such as geopolitical instability, natural disasters, or supply chain bottlenecks. These fluctuations create uncertainty for solvent manufacturers, making it difficult to predict costs and maintain stable pricing structures. Furthermore, global supply chain disruptions, particularly during the COVID-19 pandemic, have highlighted the vulnerability of the industry to external shocks. Shortages of key materials and delays in production or distribution can hinder the ability of manufacturers to meet demand in a timely manner. These challenges can ultimately lead to higher production costs, longer lead times, and reduced profitability, which can affect the overall growth of the market.

Market Opportunities

The Canada Industrial Solvents market presents significant opportunities driven by the growing demand for eco-friendly and sustainable products. As industries face increasing pressure to comply with stringent environmental regulations, the shift toward green and bio-based solvents is becoming a key market trend. Manufacturers are investing in the development of low-toxicity, high-performance solvents derived from renewable resources, which not only meet regulatory standards but also appeal to environmentally conscious consumers. The adoption of these sustainable solutions in sectors such as paints and coatings, pharmaceuticals, and adhesives presents a substantial growth opportunity. With Canada’s strong commitment to environmental sustainability, there is a clear market potential for companies to capitalize on the demand for eco-friendly solvents, particularly as industries seek to improve their ecological footprint while maintaining product efficacy.

Additionally, technological advancements in solvent formulations and production processes offer substantial opportunities for growth. The rise of solvent innovations, including specialized solvent blends and more efficient recovery techniques, allows industries to enhance their operations while reducing waste and costs. The expanding manufacturing sector, particularly in automotive, electronics, and construction, creates demand for solvents that offer enhanced performance and precision. Moreover, the increasing integration of solvents in emerging industries, such as renewable energy and biotechnology, further diversifies the market. With the expansion of these sectors in Canada, there is considerable potential for the industrial solvents market to explore new applications and drive growth. Companies that can adapt to these technological shifts and cater to emerging industries will be well-positioned to take advantage of these growing market opportunities.

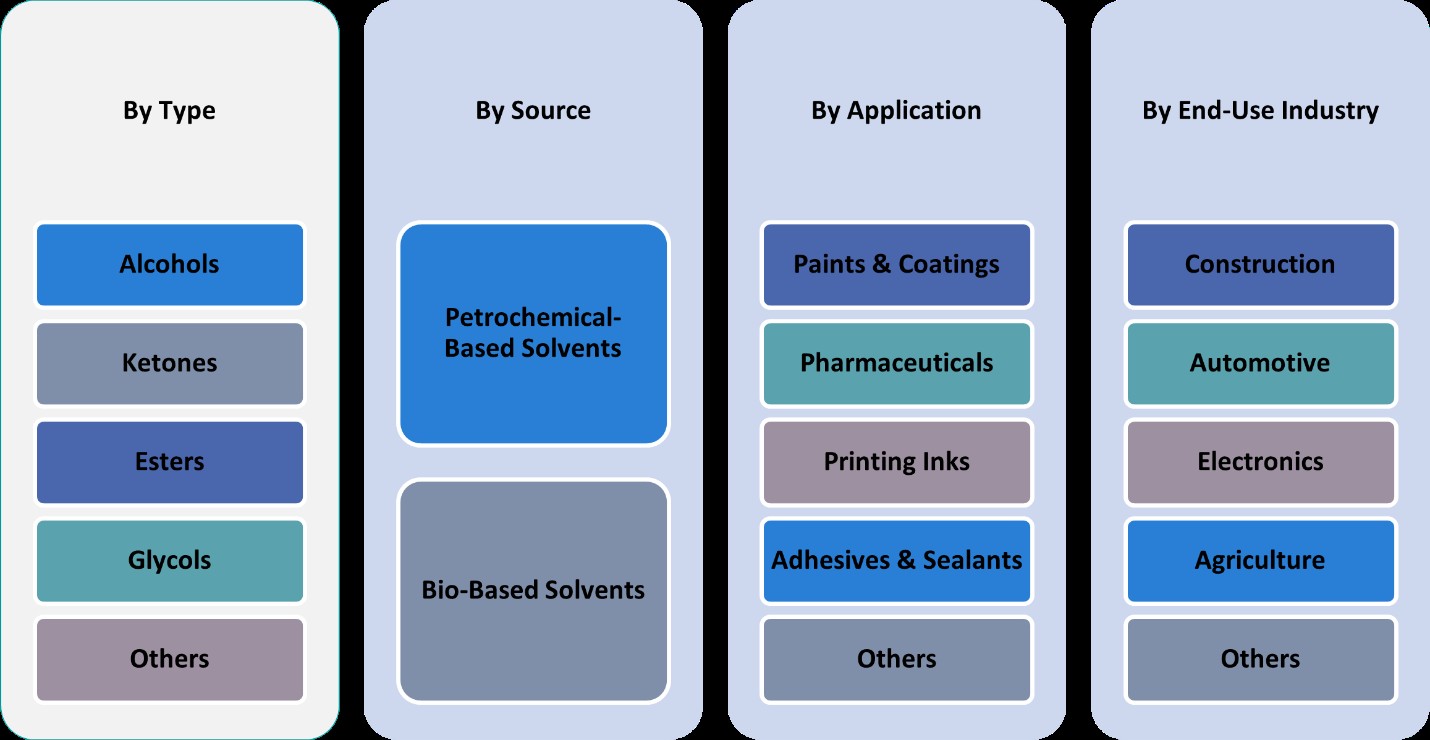

Market Segmentation Analysis:

By Type:

The Canada Industrial Solvents market is segmented by type into alcohols, ketones, esters, glycols, and others, each playing a critical role in different industrial applications. Alcohols, particularly ethanol and isopropyl alcohol, dominate the market due to their widespread use in pharmaceuticals, paints, coatings, and cleaning products. These solvents offer excellent solubility, evaporation rates, and compatibility with various formulations. Ketones, such as acetone and MEK, are commonly used in the production of coatings, adhesives, and cleaning agents due to their strong solvency properties. Esters, including ethyl acetate and butyl acetate, are popular in the coatings and adhesives sectors for their ability to provide a smooth finish and fast evaporation rate. Glycols, particularly ethylene and propylene glycol, are increasingly utilized in the production of antifreeze, lubricants, and various chemical formulations due to their low volatility and ability to absorb water. The “others” category includes a range of specialized solvents used for niche applications, offering tailored properties for specific industrial needs.

By Application:

In terms of application, the Canada Industrial Solvents market is primarily driven by the paints and coatings, pharmaceuticals, printing inks, and adhesives and sealants sectors. The paints and coatings industry is the largest consumer of industrial solvents, as they are essential in thinning paints, improving flow properties, and reducing drying times. The pharmaceutical sector relies heavily on solvents for drug formulation, extraction, and purification, with alcohols and ketones being the most commonly used solvents. Printing inks also represent a significant portion of the market, where solvents are used to adjust viscosity, ensure smooth application, and prevent clogging. Adhesives and sealants are another major segment, with solvents like esters and alcohols being used to dissolve resins and improve bonding properties. The “others” category encompasses various smaller industries, such as automotive, cleaning, and textile manufacturing, which also contribute to the overall demand for industrial solvents in Canada. Each of these applications is expected to experience steady growth, further driving the demand for solvents in Canada.

Segments:

Based on Type:

- Alcohols

- Ketones

- Esters

- Glycols

- Others

Based on Application:

- Paints & Coatings

- Pharmaceuticals

- Printing Inks

- Adhesives & Sealants

- Others

Based on End- Use:

- Construction

- Automotive

- Electronics

- Agriculture

- Others

Based on Source:

- Petrochemical-Based Solvents

- Bio-Based Solvents

Based on the Geography:

- Ontario

- Quebec

- Western Canada

- British Columbia

- Atlantic Canada

Regional Analysis

Ontario

Ontario holds the largest market share in the Canada Industrial Solvents market, accounting for approximately 35% of the overall market. This dominance is largely attributed to Ontario’s robust industrial base, which includes key sectors such as automotive, manufacturing, and chemicals. The province’s well-developed infrastructure, proximity to major transportation hubs, and strong economic growth contribute significantly to the demand for industrial solvents. Additionally, Ontario’s thriving pharmaceutical and paint industries drive solvent consumption, with alcohols and esters being particularly prevalent in these sectors. As one of Canada’s most populous provinces, Ontario also benefits from the continuous expansion of residential, commercial, and industrial construction, further increasing demand for solvents used in coatings, adhesives, and sealants.

Quebec

Quebec holds the second-largest market share, contributing around 30% to the total Canadian industrial solvents market. Quebec’s industrial solvent consumption is driven by the diverse manufacturing sectors, including chemicals, aerospace, and food processing. The province’s strong presence in the chemical industry, particularly in the production of petrochemicals and plastics, significantly impacts the demand for industrial solvents such as ketones and alcohols. Furthermore, Quebec’s pharmaceutical industry is expanding, leading to an increased need for solvents in drug manufacturing. The regional market is also supported by a growing focus on sustainability, with an increasing shift towards eco-friendly solvents in response to stringent environmental regulations.

Western Canada

Western Canada, which includes the provinces of Alberta, Saskatchewan, and Manitoba, holds a smaller market share of around 15%. This region’s solvent consumption is largely influenced by the oil and gas industry, which is a major economic driver. Solvents such as alcohols and glycols are essential in oil extraction and refining processes. Additionally, the construction, agriculture, and chemical industries in Western Canada contribute to the demand for industrial solvents. Although the region’s market is smaller compared to Ontario and Quebec, its dependence on key sectors such as energy and manufacturing presents growth potential, especially with advancements in sustainable technologies and increased investment in industrial growth.

British Columbia (BC)

British Columbia (BC) accounts for approximately 10% of the Canadian industrial solvents market. The province’s solvent demand is driven primarily by the growth in the construction, automotive, and forestry industries, where solvents are used in coatings, adhesives, and cleaning products. BC’s commitment to sustainability and environmental standards is prompting greater adoption of eco-friendly and bio-based solvents, particularly in sectors such as paints and coatings, where VOC regulations are stringent. The province also benefits from a growing demand in its technology sector, where solvents are utilized in electronics and precision cleaning. Although BC represents a smaller share of the market, its continued economic development and push for green technologies contribute to the evolving demand for industrial solvents.

Atlantic Canada

Atlantic Canada, comprising the provinces of Newfoundland and Labrador, Nova Scotia, New Brunswick, and Prince Edward Island, holds a market share of around 10%. The solvent market in this region is smaller due to its relatively lower industrial output compared to other regions. However, demand for solvents is driven by local industries such as seafood processing, paper manufacturing, and construction. The ongoing development of the energy sector and a growing focus on sustainable practices in Atlantic Canada are expected to result in steady market growth. While the region’s share is modest, increasing investments in infrastructure, manufacturing, and eco-friendly initiatives present opportunities for future expansion in the industrial solvents market.

Key Player Analysis

- Dow Inc.

- ExxonMobil Corporation

- Eastman Chemical Company

- Ashland Canada Holdings Inc.

- Huntsman Corporation

- LyondellBasell Industries

- Celanese Corporation

- PPG Industries, Inc.

- Chevron Phillips Chemical Company

Competitive Analysis

The competitive landscape of the Canada Industrial Solvents market is dominated by several global and regional players who leverage their extensive product portfolios, technological innovations, and strategic market positions. Leading players in the market include Dow Inc., ExxonMobil Corporation, Eastman Chemical Company, Ashland Canada Holdings Inc., Huntsman Corporation, LyondellBasell Industries, Celanese Corporation, PPG Industries, Inc., and Chevron Phillips Chemical Company. These companies have a strong presence in the Canadian market, driven by their ability to cater to a wide range of industries such as pharmaceuticals, paints, coatings, automotive, and adhesives. The competition is largely driven by advancements in technology, particularly the development of eco-friendly and bio-based solvents that meet stringent environmental regulations. Manufacturers are increasingly adopting sustainable practices to align with the growing demand for low-toxicity and low-VOC solvents.

In addition to innovation, companies are also competing based on their ability to offer cost-effective solutions while meeting industry-specific requirements. The focus on improving solvent recovery processes and reducing environmental impact is gaining momentum, as regulations around VOC emissions and environmental sustainability become more stringent. Moreover, regional players are able to capitalize on their local presence and supply chain efficiencies to offer competitive pricing. Overall, companies in the market are differentiating themselves through product performance, sustainability, and cost-effectiveness. The competition is expected to intensify as demand for industrial solvents continues to grow, particularly in emerging sectors like renewable energy, biotechnology, and green construction materials.

Recent Developments

- In April 2025, Eastman announced off-list price increases for several EOD (Ethylene Oxide Derivatives) solvents, including Eastman™ DB Solvent, effective April 7, 2025, reflecting ongoing cost and market pressures.

- In March 2025, BASF reported generating approximately €11 billion in 2024 sales from products launched in the past five years, driven by R&D focused on sustainability, biodegradable materials, and digital transformation. The company filed 1,159 new patents in 2024, with 45% targeting sustainability. R&D investment in 2024 was €2.1 billion, with a similar budget planned for 2025.

- In March and April 2025, Shell is restructuring its global chemicals business to boost profitability and reduce capital spending by 2030. This includes exploring strategic partnerships in the U.S., potentially closing some European assets, and selling existing assets like the Singapore refinery and chemical complex. The company aims to streamline operations, focus on core businesses, and improve returns for shareholders.

- In March 2025, BASF is expanding its production capacity for aminic antioxidants at its Puebla, Mexico site, targeting the growing demand for long-life lubricants. The project is set for completion in 2026.

- In March 2025, ExxonMobil announced a $100 million upgrade to its Baton Rouge, Louisiana plant to produce ultra-high-purity (99.999%) isopropyl alcohol (IPA) for the semiconductor industry by 2027.

- In March 2024, Dow announced plans to invest in new ethylene derivatives capacity-including carbonate solvents-on the U.S. Gulf Coast. This investment, supported by the U.S. Department of Energy, aims to supply carbonate solvents for lithium-ion batteries, supporting the domestic EV and energy storage market. The facility will capture over 90% of CO₂ from ethylene oxide production, aligning with sustainability goals.

Market Concentration & Characteristics

The Canada Industrial Solvents market is moderately concentrated, with a mix of global players and regional companies dominating the industry. The market characteristics include a strong emphasis on product innovation, particularly in response to increasing demand for sustainable and eco-friendly solvents. Leading companies often invest in research and development to create low-toxicity, high-performance alternatives that comply with stringent environmental regulations. Despite the presence of several large players, regional companies also hold a significant share, benefiting from their ability to cater to local market needs with cost-effective solutions. The industry is marked by high competition in terms of product offerings, with companies differentiating themselves through the quality and efficiency of their solvent formulations. Additionally, the market is characterized by steady demand from key sectors such as pharmaceuticals, paints and coatings, and adhesives, which ensures consistent growth opportunities. This mix of global and regional competition fosters a dynamic market environment.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Type, Application, End-Use, Source and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The Canadian industrial solvents market is projected to continue its steady growth trajectory, driven by increasing demand across various end-use industries.

- Advancements in solvent recovery technologies are enabling companies to recycle solvents, thereby minimizing costs and reducing environmental impact.

- The integration of automation and digitalization in solvent manufacturing processes is streamlining production, resulting in higher output and reduced labor costs.

- Research and development efforts are leading to the formulation of high-performance solvents that enhance product quality while decreasing the volume required for applications.

- The trend towards sustainability is prompting the adoption of green and bio-based solvents, aligning with global environmental goals and regulatory standards.

- Emerging applications in renewable energy and biotechnology are expanding the scope of industrial solvent use, creating new market opportunities.

- Regional variations in industrial activity are influencing solvent demand, with provinces like Ontario and Quebec showing strong consumption patterns.

- The competitive landscape is characterized by both global players and regional manufacturers, fostering innovation and diverse product offerings.

- Stricter environmental regulations are encouraging companies to invest in sustainable practices and low-emission solvent alternatives.

- Ongoing investments in research and development are expected to drive continuous improvement in solvent performance and environmental compatibility.