Market Overview:

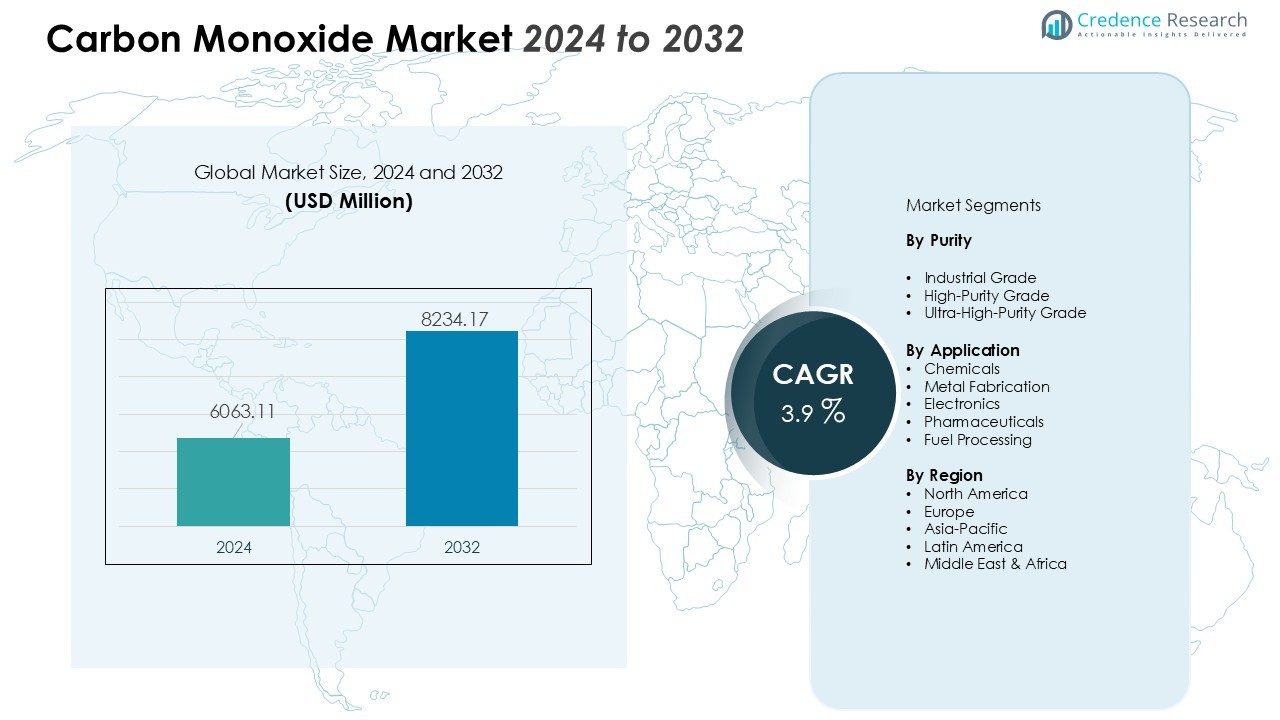

The carbon monoxide market size was valued at USD 6063.11 million in 2024 and is anticipated to reach USD 8234.17 million by 2032, at a CAGR of 3.9% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Carbon Monoxide Market Size 2024 |

USD 6063.11 Million |

| Carbon Monoxide Market, CAGR |

3.9% |

| Carbon Monoxide Market Size 2032 |

USD 8234.17 Million |

Key market drivers include rising utilization of carbon monoxide in metal fabrication, hydroformylation processes, and bulk chemical synthesis. Industries such as pharmaceuticals, polymers, and electronics rely on CO-based intermediates for catalyst regeneration, reductive processing, and fine chemical production. The increasing shift toward clean-energy feedstocks, along with the growing adoption of CO in fuel-cell technologies and emerging carbon-recycling systems, also contributes to demand expansion. Expanding manufacturing footprints in developing economies and continuous innovation in gas handling, storage, and distribution systems reinforce market momentum.

Regionally, North America and Europe maintain strong demand due to mature industrial gas networks, advanced chemical manufacturing capabilities, and ongoing R&D activities. Asia-Pacific is expected to register the fastest growth, supported by rapid industrialization, rising steel production, and expanding chemical synthesis sectors across China, India, South Korea, and Southeast Asia. Emerging markets in Latin America and the Middle East further enhance growth opportunities as industrial infrastructure accelerates and investments in gas-based processing intensify.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The carbon monoxide market is valued at USD 6063.11 million in 2024 and is projected to reach USD 8234.17 million by 2032, supported by a CAGR of 3.9% during the forecast period.

- Demand strengthens due to rising use of CO in bulk chemical synthesis, including oxo-alcohols, acetic acid, and phosgene derivatives that rely on high-efficiency carbonylation and hydroformylation processes.

- Metal fabrication and metallurgy fuel market expansion as CO remains essential for ore reduction, blast furnace operations, sintering, annealing, and steel-refining activities.

- High-purity CO adoption grows rapidly in semiconductor and electronics manufacturing, where it enables controlled deposition, fine etching, and advanced material engineering.

- Clean-energy innovations and carbon-recycling technologies increasingly use CO for fuel cells, synthetic fuels, and CO₂-conversion systems, supporting circular-carbon pathways.

- Market challenges arise from stringent safety regulations, high handling risks, costly purification systems, and infrastructure limitations that restrict large-volume transport and storage.

- Regional growth is led by strong industrial gas networks in North America and Europe, while Asia-Pacific registers the fastest expansion driven by rapid industrialization, steel output, and increasing semiconductor and chemical production.

Market Drivers:

Rising Use of CO in Bulk Chemical and Intermediate Production

The carbon monoxide market benefits from strong uptake across large-scale chemical synthesis. Industries produce oxo-alcohols, acetic acid, and phosgene derivatives through CO-based pathways that support high output efficiency. It enables manufacturers to maintain consistent purity levels that strengthen downstream product performance. Demand remains stable due to its critical role in hydroformylation and reductive reactions across diverse chemical chains.

- For instance, Celanese Corporation industrially produces acetic acid via carbonylation of methanol with CO using a rhodium catalyst, producing over 3 million metric tons annually with purity levels exceeding 99.9%, meeting strict chemical manufacturing standards.

Growing Dependence on CO in Metallurgy and Metal Fabrication Processes

Rising steel and metal production strengthens demand for CO as a reducing agent in blast furnaces and metal refining systems. It supports efficient removal of oxygen from metal ores and enhances furnace productivity. The carbon monoxide market benefits from expanding applications in sintering, annealing, and surface treatment. Rapid industrial growth in developing economies pushes metal processors to secure reliable CO supplies.

- For Instance, ArcelorMittal’s steel mills produce blast furnace gas as a by-product during the iron-making process, which typically has a carbon monoxide (CO) content of around 20-25%.

Increasing Need for High-Purity CO in Electronics and Semiconductor Manufacturing

High-purity grades of CO gain traction in semiconductor fabrication, where it supports controlled deposition and etching processes. It helps manufacturers achieve precise material characteristics required for advanced electronic devices. The carbon monoxide market grows due to rising demand for specialty gases in integrated circuit and display panel production. Strong focus on microelectronics innovation encourages investments in advanced gas purification systems.

Expansion of Clean Energy Technologies and Carbon Recycling Platforms

Emerging clean-energy systems adopt CO for fuel-cell applications and synthetic fuel development. It also supports carbon-capture and conversion platforms that convert CO₂ into value-added chemicals. The carbon monoxide market benefits from growing interest in low-carbon manufacturing routes and circular chemical processes. Ongoing research promotes novel pathways where CO enables sustainable industrial transformation.

Market Trends:

Growing Adoption of High-Purity and Specialty CO Grades Across Advanced Manufacturing

The carbon monoxide market observes a shift toward high-purity and specialty gas grades that support precision-driven industries. Semiconductor fabrication, fiber optics, and specialty chemical producers rely on refined CO supply to maintain strict process uniformity. It improves reaction selectivity and strengthens quality control in highly sensitive manufacturing lines. Growing demand for microelectronics and advanced materials pushes suppliers to invest in purification technologies. Rising emphasis on stable supply chains encourages long-term contracts with gas distributors. Increased deployment of automated gas delivery systems elevates operational efficiency and safety in production environments.

- For instance, Linde implemented pressure swing adsorption systems, reducing impurities to parts-per-billion for CVD applications in chip production.

Expansion of CO Utilization in Sustainable Industrial Pathways and Low-Carbon Technologies

Global industries integrate CO into emerging clean-energy and circular-chemistry platforms that target emission reduction. It contributes to synthetic fuel production, carbon-capture conversion, and next-generation catalyst development. The carbon monoxide market aligns with rising interest in carbon-recycling routes that transform CO₂ into industrial feedstocks. Strong policy support for decarbonization encourages research partnerships across energy, chemical, and engineering sectors. Commercialization of solid oxide fuel cells and gasification technologies increases CO consumption in pilot and industrial-scale units. Growing attention to energy-efficient syngas systems supports wider industrial adoption and strengthens long-term market prospects.

- For instance, Northwestern University researchers developed a process achieving 70% Faradaic efficiency in converting captured \(CO_{2}\) to \(CO\) at room temperature, which operates at an energy intensity of 35 gigajoules per ton of CO produced. This significantly lowers energy consumption compared to older methods, which required more than 59 gigajoules per ton.

Market Challenges Analysis:

Stringent Safety Regulations and Operational Risks in CO Handling

The carbon monoxide market faces significant challenges due to strict safety norms and high operational risks. CO’s toxic nature requires advanced monitoring systems, airtight storage, and controlled transport procedures. It increases compliance costs for chemical plants, metal processors, and semiconductor facilities. Frequent regulatory updates demand continuous investment in training and safety upgrades. Limited tolerance for leaks or exposure incidents forces operators to adopt specialized equipment. Heightened scrutiny from environmental and occupational safety agencies increases operational complexity.

High Production Costs and Infrastructure Constraints Across Key Industries

Producers encounter rising costs linked to purification, separation, and distribution of CO across industrial clusters. The carbon monoxide market struggles with limited pipeline networks that restrict efficient large-volume transport. It also faces infrastructure gaps in emerging economies where industrial gas supply chains remain underdeveloped. High capital requirements slow expansion plans for small and mid-sized manufacturers. Volatile raw material availability affects production stability for syngas-derived CO. Supply disruptions and logistical barriers create uncertainty for industries that depend on consistent high-purity CO delivery.

Market Opportunities:

Expansion of CO Applications in Sustainable Chemicals and Low-Carbon Technologies

The carbon monoxide market gains strong opportunities from rising interest in sustainable chemical pathways and circular-carbon systems. It supports new routes for synthetic fuels, green methanol, and advanced intermediates that align with global decarbonization goals. Emerging carbon-capture and conversion platforms create fresh demand for CO-based reactions that convert CO₂ into valuable products. Strong research activity in catalysis strengthens commercialization potential for next-generation processes. Investment flows from energy transition programs encourage industrial pilots across major economies. Adoption of clean-energy gasification units broadens market access for producers that supply high-purity CO.

Growth Potential Across High-Precision Manufacturing and Specialty Gas Applications

Rising demand for high-performance electronics, engineered materials, and fine chemicals opens new revenue avenues. The carbon monoxide market benefits from the need for ultra-high-purity gases in semiconductor fabrication, OLED production, and specialty coatings. It enhances process accuracy and enables manufacturers to meet strict quality benchmarks in advanced industries. Expansion of microelectronics clusters in Asia and North America raises CO consumption in deposition and reduction steps. Strong interest in automated gas supply systems increases opportunities for gas suppliers offering integrated delivery solutions. Broader industrial digitization supports new service models built around remote monitoring and predictive maintenance for CO infrastructure.

Market Segmentation Analysis:

By Purity

The carbon monoxide market categorizes purity levels into industrial grade, high-purity grade, and ultra-high-purity grade, each serving distinct end-use requirements. Industrial-grade CO secures strong demand from metallurgy, bulk chemicals, and syngas-based operations that prioritize volume and cost efficiency. High-purity CO gains traction in pharmaceutical intermediates and advanced chemical synthesis where controlled reactions require consistent gas quality. Ultra-high-purity CO records rapid growth due to its critical role in semiconductor manufacturing, microelectronics processing, and precision material deposition. It enables producers to meet strict purity standards and helps maintain uniformity in sensitive production environments. Rising focus on stringent quality benchmarks drives investment in refined purification and distribution systems.

- For instance, Air Liquide supplies industrial-grade oxygen to steel producers like ArcelorMittal, enabling efficient blast furnace operations and improved energy performance.

By Application

Application segments include chemicals, metal fabrication, electronics, pharmaceuticals, and fuel processing, each contributing to diverse revenue streams. The carbon monoxide market maintains strong penetration in chemical synthesis, where CO supports production of acetic acid, oxo-alcohols, and other high-volume intermediates. Metal fabrication units depend on CO for reduction processes that improve furnace efficiency and material performance. It strengthens demand in the electronics sector through its role in deposition, etching, and specialty gas applications. Pharmaceutical industries adopt CO-based intermediates to support complex synthesis pathways. Emerging fuel production and carbon-conversion technologies create new application avenues for CO in low-carbon industrial platforms.

- For instance, chemical manufacturers like Celanese and INEOS utilize CO in their chemical synthesis processes, producing millions of tons of acetic acid annually using advanced CO-based carbonylation technology

Segmentations:

By Purity

- Industrial Grade

- High-Purity Grade

- Ultra-High-Purity Grade

By Application

- Chemicals

- Metal Fabrication

- Electronics

- Pharmaceuticals

- Fuel Processing

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Regional Analysis:

Strong Market Presence Across North America Driven by Advanced Industrial Infrastructure

North America holds a significant share due to its mature chemical manufacturing base, robust metal processing capacity, and well-developed industrial gas networks. The carbon monoxide market benefits from strong demand in hydroformylation, acetic acid production, and semiconductor fabrication facilities across the U.S. and Canada. It supports high adoption levels in refineries and syngas plants where operational efficiency and steady gas supply remain priorities. Growth in specialty chemicals and advanced materials strengthens long-term consumption. Expanding investments in microelectronics manufacturing stimulate demand for ultra-high-purity CO. Strong regulatory frameworks and investments in safety technologies reinforce market stability.

Consistent Expansion Across Europe Supported by Technological and Environmental Advancements

Europe records steady growth driven by its strong chemical clusters, advanced metallurgical operations, and rising focus on sustainable industrial pathways. The carbon monoxide market gains support from European initiatives that promote low-carbon chemicals and circular-carbon technologies. It sees rising uptake in synthetic fuel development, carbon-conversion platforms, and precision manufacturing. Demand in Germany, France, and the UK remains stable due to established industrial gas infrastructure and high standards for purity control. Strengthening semiconductor and specialty materials production drives interest in high-purity CO. Rising emphasis on emission control and energy-efficient gasification technologies supports regional momentum.

Rapid Growth Across Asia-Pacific Driven by Industrialization and Manufacturing Expansion

Asia-Pacific emerges as the fastest-growing regional segment, supported by large-scale industrialization, expanding chemical production, and strong steel output. The carbon monoxide market benefits from increasing consumption across China, India, South Korea, and Southeast Asia. It plays a vital role in electronics manufacturing, where high-purity CO supports deposition, etching, and specialty gas applications. Rising investments in semiconductor fabs, fine chemicals, and engineered materials strengthen regional opportunities. Expanding syngas projects and clean-energy initiatives improve access to CO supply. Strong government support for industrial modernization accelerates adoption across multiple sectors.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Celanese Corporation

- Linde plc

- ATCO Atmospheric And Speciality Gases Private Limited

- Middlesex Gases & Technologies, Inc.

- Air Liquide

- Air Products and Chemicals, Inc.

- Axcel Gases

- Sipchem Company

- American Gas Products

- Messer

Competitive Analysis:

The carbon monoxide market features an established competitive landscape dominated by global industrial gas producers and specialized chemical manufacturers. Key participants such as Celanese Corporation, Linde plc, ATCO Atmospheric And Speciality Gases Private Limited, and Middlesex Gases & Technologies, Inc. strengthen market structure through broad distribution networks and advanced gas-handling capabilities. It benefits leading players that invest in purification technologies, high-purity gas production, and integrated supply solutions. Companies focus on long-term supply contracts to support semiconductor fabrication, metal processing, and bulk chemical operations. Strategic expansions into emerging economies help suppliers address rising demand from industrial clusters. Strong emphasis on safety compliance, product quality, and technological innovation shapes competitive differentiation across the industry.

Recent Developments:

- In July 2025, Linde announced major U.S. investments to support the commercial space sector, including two new long-term agreements for bulk industrial gases for rocket launches and construction of a new air separation unit in Brownsville, Texas, expected online in Q1 2026.

- In February 2025, Air Products announced exiting three U.S.-based projects including sustainable aviation fuel expansion in California, green liquid hydrogen in New York, and carbon monoxide project in Texas, recording a pre-tax charge of up to $3.1 billion to streamline its portfolio and focus on core industrial gas business.

Report Coverage:

The research report offers an in-depth analysis based on Purity, Application and Region. It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- Rising demand for high-purity CO in semiconductor and microelectronics manufacturing strengthens long-term growth potential.

- Expansion of gasification projects increases CO availability for chemicals, fuels, and advanced materials.

- Growing interest in carbon-conversion technologies positions CO as a key intermediate in low-carbon industrial pathways.

- It supports wider adoption of circular-chemistry models that convert CO₂ into value-added products.

- Investments in specialty gas infrastructure improve supply reliability across high-precision manufacturing sectors.

- Strengthening environmental regulations accelerate development of cleaner CO production methods.

- R&D activity in catalyst optimization enhances efficiency of CO-based reactions across chemical processing routes.

- Emerging industrial clusters in Asia-Pacific drive strong demand across steel, chemicals, and electronics industries.

- Automation of gas handling, monitoring, and delivery systems enhances operational efficiency for end users.

- Global focus on energy transition expands opportunities for CO use in synthetic fuels and next-generation energy platforms.