Deli Food Container Market Overview:

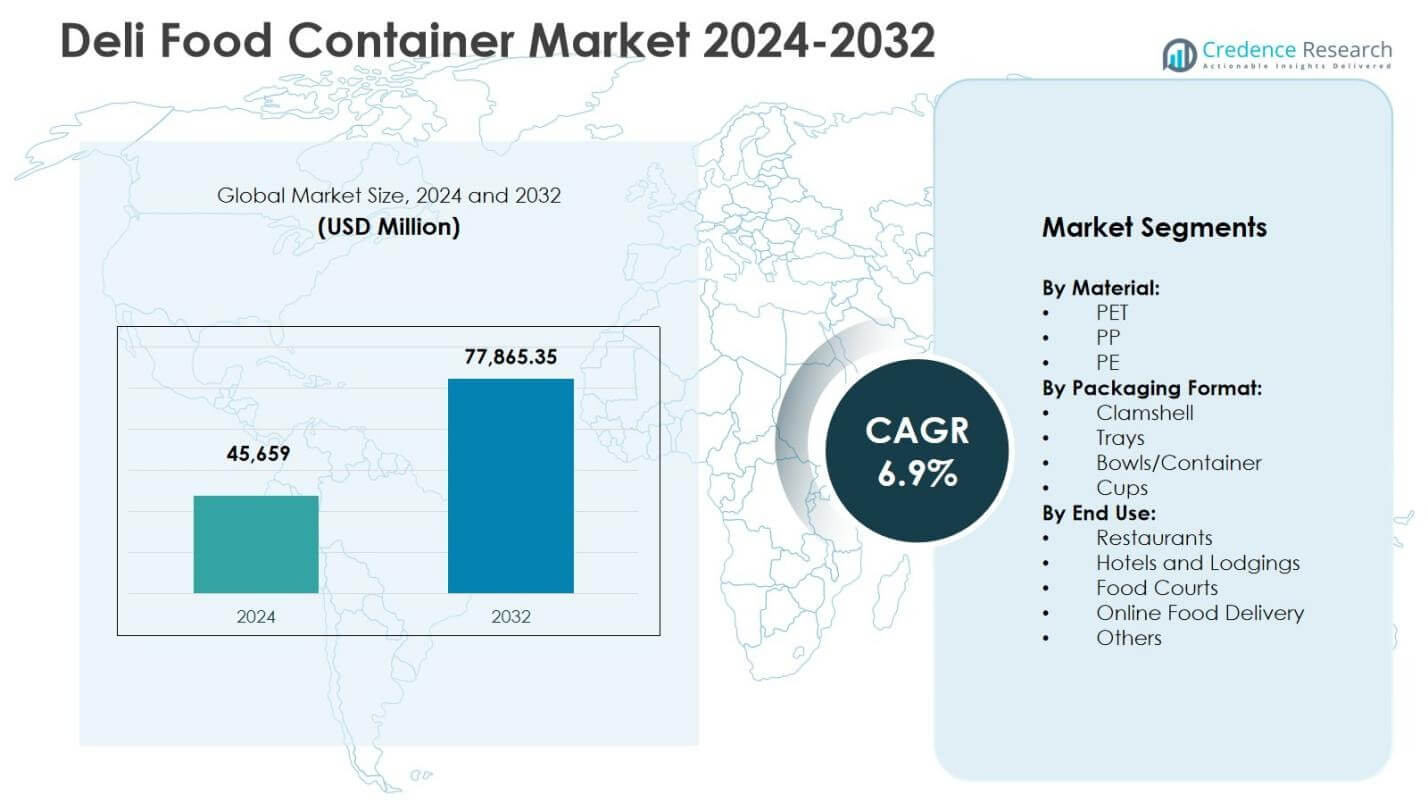

Deli Food Container Market size was valued USD 45,659 Million in 2024 and is anticipated to reach USD 77,865.35 Million by 2032, at a CAGR of 6.9% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Deli Food Container Market Size 2024 |

USD 45,659 million |

| Deli Food Container Market, CAGR |

6.9% |

| Deli Food Container Market Size 2032 |

USD 77,865.35 million |

Deli Food Container Market Insights

- The market grows as demand rises for ready-to-eat meals, takeaway formats, and hygienic PET and PP containers, with restaurants and online food delivery driving higher adoption across rigid bowls, clamshells, and multi-compartment containers.

- The market trends toward recyclable and lightweight packaging, tamper-evident closures, microwave-safe designs, and premium high-clarity containers, with PET leading the material segment with a 48.6 percent share in 2024.

- Key players expand portfolios through sustainable materials, lightweight engineering, and stackable formats, strengthening partnerships with supermarkets, delis, and food-service chains while enhancing supply networks and product performance.

- North America leads the market with a 32.4 percent share in 2024, followed by Europe at 27.8 percent and Asia-Pacific at 24.6 percent, while Latin America and the Middle East and Africa collectively expand demand through growing quick-service restaurant and retail deli networks.

Deli Food Container Market Segmentation Analysis:

By Material

The Deli Food Container Market by material is led by PET, which accounted for 48.6% share in 2024, driven by its clarity, durability, and strong barrier properties that support fresh food visibility and extended shelf life. PET’s recyclability and compliance with evolving sustainability regulations further strengthen its adoption across retail and food-service applications. PP holds a significant secondary share due to its heat resistance and suitability for microwaveable packaging, while PE remains preferred for flexible and cost-efficient formats. The growing emphasis on hygienic storage, lightweight packaging, and circular-economy initiatives continues to reinforce PET’s dominant position in the market.

- For instance, Berry Global expanded its CLCLEAR™ PET range for clear deli tubs, emphasizing PCR (post-consumer recycled) content and lightweight formats.

By Packaging Format

Across packaging formats, Bowls/Containers emerged as the dominant sub-segment with a 36.2% market share in 2024, supported by their versatility, leak-resistant design, and suitability for salads, ready meals, and deli assortments. Their compatibility with tamper-evident lids and stackable formats enhances transport efficiency for retail and takeaway channels. Clamshell packaging follows closely, benefiting from convenience and product visibility for bakery and cold-cut items, while trays and cups serve portion-controlled and single-serve applications. The rise of prepared food consumption, grab-and-go offerings, and premium presentation standards continues to drive demand for bowls and multi-compartment deli containers.

- For instance, Pactiv Evergreen’s hinged paperboard clamshells, measuring 4.79 x 4.81 x 2.75 inches, provide grease resistance and suit hot/cold grab-and-go bakery items like pastries, with a large area for product stickers.

By End Use

By end use, Restaurants represented the leading sub-segment with a 41.7% share in 2024, driven by expanding takeaway meals, quick-service formats, and increasing reliance on hygienic, durable packaging for on-the-go consumption. The growth of meal customization and portion packaging strengthens restaurant adoption of rigid deli containers. Online Food Delivery is the fastest-growing user group, supported by delivery-led dining behavior and tamper-secure packaging needs, while hotels, food courts, and institutional catering contribute to steady volume demand. Rising urban dining frequency, convenience trends, and standardized packaging requirements reinforce the dominance of restaurant-led usage in the market.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Key Growth Drivers

Rising Demand for Convenient and Ready-to-Eat Foods

The Deli Food Container Market grows strongly as urban lifestyles, busy work schedules, and expanding quick-service formats accelerate the consumption of ready-to-eat meals, salads, snacks, and takeaway foods. Food retailers and delis increasingly rely on durable, leak-resistant, and hygienic packaging to ensure product safety, visual appeal, and portion control. Growing consumer preference for grab-and-go formats, coupled with the expansion of supermarket deli counters and prepared-meal sections, further strengthens container adoption. The shift toward portable meal solutions across urban and suburban markets continues to position deli containers as a critical enabler of convenience-driven food consumption.

- For instance, Dart’s Solo MicroGourmet line includes 8 oz. and 16 oz. clear polypropylene deli containers that are microwave-safe, freezer-safe, and recyclable, designed for pasta salads, soups, and pre-cut fruits in delis or carry-out settings.

Expansion of Foodservice, Delivery, and Cloud Kitchen Ecosystems

The rapid growth of online food delivery platforms, cloud kitchens, and quick-commerce services significantly boosts demand for reliable deli food containers designed for transport efficiency and tamper-proof safety. Restaurants, cafés, and food courts increasingly adopt rigid plastic containers, bowls, and clamshells to preserve product integrity during transit while maintaining temperature, freshness, and presentation quality. The rise of subscription meal services and delivery-led dining formats further intensifies packaging usage. As delivery ecosystems expand to tier-2 and tier-3 cities, foodservice operators continue to increase container procurement to support operational scalability and consistent customer experience.

- For instance, Zomato introduced “Zomato Safely Sealed” tamper-proof packaging in 2019, featuring 50-micron single-polymer seals for boxes that can only be opened by cutting the top strip.

Shift Toward Sustainable and Recyclable Packaging Materials

Sustainability-focused regulations, corporate ESG commitments, and growing consumer awareness accelerate the adoption of recyclable PET, PP, and bio-based deli food containers. Food brands and retailers increasingly transition from single-use, non-recyclable plastics to eco-responsible alternatives to meet circular-economy goals and reduce landfill impact. Advances in material engineering, lightweight container design, and post-consumer resin integration strengthen product viability across premium and mass-market applications. The demand for packaging with lower carbon footprint and compliance with waste-management policies continues to drive innovation, enabling manufacturers to differentiate through sustainable performance, product safety, and environmental transparency.

Key Trends & Opportunities

Adoption of Tamper-Evident, Smart, and Functional Packaging Designs

A major trend shaping the Deli Food Container Market is the integration of tamper-evident closures, secure sealing systems, and smart functional features that enhance food safety and customer trust, especially in delivery-centric environments. Retailers and foodservice operators increasingly prefer stackable, space-efficient containers that optimize storage and logistics while improving shelf presentation. Innovations such as anti-fog lids, multi-compartment formats, and microwave-safe structures expand usage across meal-prep, salad, and protein packaging applications. The opportunity for manufacturers lies in combining safety, convenience, and performance attributes with value-added design, strengthening brand positioning across modern retail and quick-service channels.

- For instance, SystemPAK offers tamper-evident plastic containers that are microwave-safe and freezer-safe down to -40°C for freezer-grade models, ideal for liquids, dried foods, and semi-dry items like takeaway curries in deli applications.

Premiumization of Packaging for Fresh, Healthy, and Gourmet Offerings

The growing consumer shift toward premium deli assortments, gourmet salads, protein bowls, and high-quality prepared foods drives demand for visually appealing, high-clarity packaging that enhances product visibility and perceived freshness. Retailers increasingly leverage upscale deli containers to support brand differentiation, attract health-conscious shoppers, and justify premium pricing across fresh-food categories. The trend toward portion-controlled nutrition, clean-label ingredients, and elevated in-store presentation creates opportunities for advanced PET and PP container formats. Manufacturers benefit from developing aesthetic, durable, and retail-ready packaging solutions that align with evolving lifestyle and premium food-consumption trends.

- For instance, Sealed Air Corporation introduced its Cryovac® Darfresh® vacuum skin packaging, which offers enhanced product visibility and extended freshness for premium proteins and ready-to-eat meals.

Key Challenges

Environmental Regulations and Pressure to Reduce Plastic Waste

The market faces challenges due to tightening global regulations on single-use plastics, landfill restrictions, and extended producer-responsibility frameworks. Manufacturers and foodservice operators must balance durability and safety requirements with sustainability targets and recycling infrastructure limitations. Transitioning to eco-friendly materials increases production and procurement costs for many stakeholders, especially in cost-sensitive regions. Variations in waste-collection systems and end-of-life material recovery further complicate large-scale adoption. Companies must invest in recyclable material innovation, closed-loop systems, and compliance-driven packaging redesign to mitigate regulatory risks and maintain long-term market competitiveness.

Volatility in Raw Material Prices and Supply Chain Disruptions

Fluctuations in polymer prices, resin availability, and global petrochemical supply chains pose significant challenges for deli container manufacturers and distributors. Rising input costs directly affect packaging margins and pricing models for foodservice and retail customers. Logistics constraints, transportation delays, and geopolitical uncertainties further disrupt procurement cycles and production planning. Smaller suppliers face increased cost pressures compared to integrated packaging companies with stronger sourcing capabilities. To address these challenges, market participants must strengthen supplier partnerships, diversify raw-material sourcing, and adopt operational resilience strategies to stabilize production reliability and cost structures.

Regional Analysis

North America

North America held a leading position in the Deli Food Container Market with a 32.4% share in 2024, supported by strong demand from supermarkets, convenience stores, and quick-service restaurants across the United States and Canada. The region benefits from high consumption of ready-to-eat meals, premium salads, and packaged deli assortments, which drives adoption of PET and PP rigid containers with tamper-evident and microwave-safe features. Growth in online food delivery, meal-kit services, and sustainability-focused packaging initiatives further strengthens market expansion. Continuous investments in recyclable packaging formats and innovation in lightweight container designs reinforce the region’s dominant role.

Europe

Europe accounted for a 27.8% share in 2024, driven by strict packaging sustainability regulations, strong retail penetration, and rising consumer preference for eco-friendly and recyclable deli containers. The market gains momentum from the expansion of premium grocery formats, in-store deli counters, and chilled ready-meal offerings across Western and Northern Europe. Demand for high-clarity PET containers and recyclable PP formats increases as retailers emphasize food safety, quality preservation, and elevated product presentation. Ongoing transition toward circular-economy packaging models and investment in bio-based and post-consumer resin solutions continue to influence product development and adoption trends across the region.

Asia-Pacific

Asia-Pacific represented a 24.6% share in 2024, emerging as the fastest-growing regional market due to rapid urbanization, expanding foodservice infrastructure, and increasing popularity of convenience-driven dining and takeaway formats. Rising disposable incomes, growth in organized retail, and the proliferation of cloud kitchens and delivery platforms significantly boost demand for durable deli containers. Manufacturers benefit from large-scale production capacity in China, India, and Southeast Asia, supporting cost-efficient supply. The shift toward modern food retailing, expanding prepared-food categories, and gradual adoption of sustainable packaging alternatives further strengthen market penetration across both developed and emerging Asia-Pacific economies.

Latin America

Latin America captured a 8.9% share in 2024, supported by growing quick-service restaurant expansion, increasing supermarket deli offerings, and rising demand for packaged ready-to-eat meals in urban centers. Countries such as Brazil, Mexico, and Chile contribute strongly through expanding retail modernization and the adoption of takeaway and delivery-oriented food formats. Demand for lightweight and cost-effective plastic containers remains dominant, while sustainability initiatives are gradually shaping product preferences in premium retail channels. The region’s market growth is reinforced by investments in local packaging manufacturing capacity, improving supply networks, and rising consumer inclination toward hygienic and secure food packaging solutions.

Middle East and Africa

The Middle East and Africa accounted for a 6.3% share in 2024, driven by growth in modern retail, expanding hospitality and foodservice sectors, and rising consumption of convenience foods in urban economies. Demand for deli food containers increases across quick-service restaurants, hypermarkets, and institutional catering environments, particularly in Gulf Cooperation Council countries. Investments in tourism, hotel catering, and organized food retail strengthen container usage across premium and takeaway meal segments. While affordability remains a key purchasing driver, gradual shifts toward recyclable and higher-quality packaging solutions support long-term market development across emerging markets in the region.

Deli Food Container Market Segmentations:

By Material:

By Packaging Format:

- Clamshell

- Trays

- Bowls/Container

- Cups

By End Use:

- Restaurants

- Hotels and Lodgings

- Food Courts

- Online Food Delivery

- Others

By Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape in the Deli Food Container Market is characterized by leading players such as Pactiv Evergreen, Berry Global Inc., Amcor plc, Huhtamäki Oyj, Sabert Corporation, Genpak, Display Pack, Eco-Products Inc., Vegware Ltd, and Lollicup USA. The market reflects an intense focus on material innovation, sustainability, and performance-driven packaging solutions, as manufacturers expand portfolios across PET, PP, and recyclable formats to address shifting regulatory and ESG requirements. Companies strengthen their positions through investments in lightweight container engineering, tamper-evident sealing systems, and stackable, logistics-efficient designs tailored for retail, foodservice, and delivery channels. Strategic priorities include capacity expansion, automation upgrades, and collaboration with food retailers to develop customized formats for salads, prepared meals, and premium deli assortments. Increasing emphasis on circular-economy packaging, post-consumer resin integration, and eco-label branding drives product differentiation, while pricing discipline, regional supply networks, and customer service capabilities continue to influence competitive advantage across global and emerging markets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Pactiv Evergreen

- Genpak

- Display Pack

- Vegware Ltd

- Berry Global Inc.

- Sabert Corporation

- Lollicup USA

- Eco-Products Inc.

- Amcor plc

- Huhtamäki Oyj

Recent Developments

- In September 2025, Georgia-Pacific announced an agreement to acquire Anchor Packaging, a major rigid food container and cling film manufacturer, to expand its food-to-go and deli container offerings in the U.S. market.

- In March 2025, Placon launched its new Fresh ‘n Clear Dip Cup container line, designed for hummus, spreads, and dips to meet rising demand for sustainable thermoformed food packaging in the deli segment.

- In July 2025, The Compleat Food Group acquired Freshpak, a producer specializing in chilled food-to-go snacks and deli fillers, to expand capabilities in protein-rich deli products.

- In September 2025, Mama’s Creations acquired Crown from Sysco, a fresh protein manufacturer generating $56 million in FY25 revenue, to bolster deli solutions in poultry and prepared foods.

Report Coverage

The research report offers an in-depth analysis based on Material, Packaging Format, End Use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will witness sustained growth as demand for ready-to-eat meals, takeaway food, and convenience packaging continues to increase across retail and foodservice channels.

- Manufacturers will prioritize recyclable, bio-based, and lightweight materials as sustainability regulations and corporate ESG commitments become stronger worldwide.

- PET and PP containers will retain strong adoption due to durability, clarity, and safety performance, while advanced eco-friendly alternatives will gain faster traction.

- Packaging designs will increasingly focus on tamper-evident closures, leak resistance, and transit protection to support delivery-led food consumption.

- Smart, functional, and premium-presentation container formats will expand as retailers enhance product visibility and consumer experience.

- Automation, precision molding, and material-efficient production technologies will improve cost efficiency and scalability for manufacturers.

- Demand from quick-service restaurants, cloud kitchens, and grocery delis will continue to drive high-volume procurement of rigid food containers.

- Regional manufacturing expansion and localized supply networks will strengthen resilience against raw-material and logistics disruptions.

- Strategic partnerships between packaging suppliers and food retailers will increase to enable customized packaging solutions for prepared foods.

- Market participants will focus on circular-economy alignment, recycling infrastructure collaboration, and closed-loop material integration to enhance long-term competitiveness.