Electrostatic Discharge Technologies Market Overview:

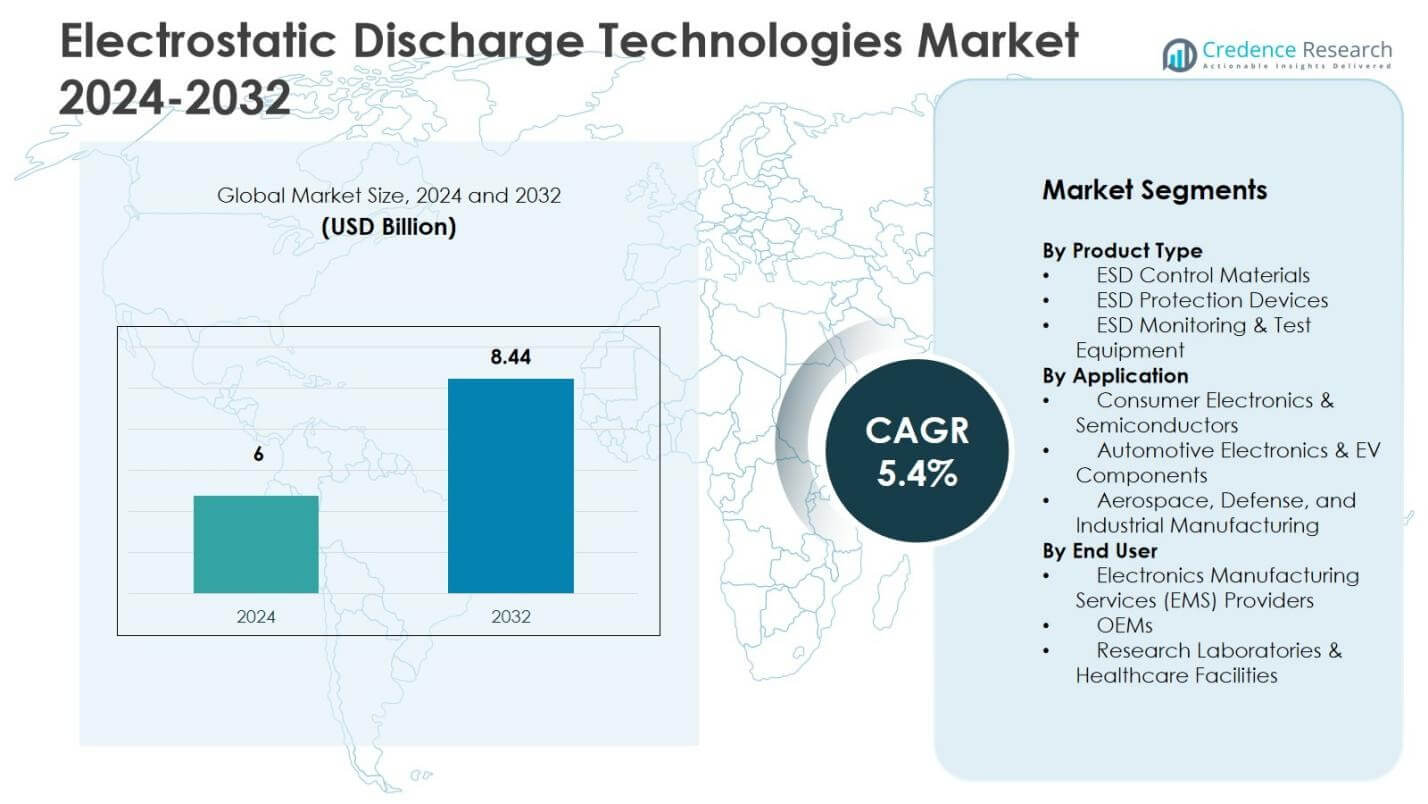

The electrostatic discharge technologies market was valued at $6 billion in 2024 and is anticipated to reach $8.44 billion by 2032, at a CAGR of 5.4% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Electrostatic Discharge Technologies Market Size 2024 |

USD 6 Billion |

| Electrostatic Discharge Technologies Market, CAGR |

5.4% |

| Electrostatic Discharge Technologies Market Size 2032 |

USD 8.44 Billion |

Electrostatic Discharge Technologies Market insights

- The electrostatic discharge technologies market was valued at $6 billion in 2024 and will reach $8.44 billion by 2032 at a CAGR of 5.4%.

- The primary market driver is rising adoption of ESD protection across semiconductor fabrication, consumer electronics and automotive electronics, with the consumer electronics and semiconductors segment holding a 52.8% share in 2024 due to high-volume PCB assembly and chip manufacturing.

- Market trends include rapid deployment of smart ESD monitoring systems, IoT-enabled grounding solutions and advanced ESD materials that support cleanroom manufacturing and reliability-focused production environments across EMS operations and OEM facilities.

- Competitive analysis shows a strong presence of global players focusing on innovation in ESD flooring, coatings, packaging and protection devices, along with strategic investments in automation, compliance-certified solutions and expansion across high-growth electronics manufacturing hubs.

- North America holds a 34.6% share, Asia-Pacific accounts for a 29.8% share and Europe represents a 27.3% share in 2024, supported by semiconductor capacity expansion, EV electronics production, aerospace manufacturing and industrial automation initiatives.

Electrostatic Discharge Technologies Market segmentation analysis

By product type

The electrostatic discharge technologies market by product type is led by ESD control materials, which accounted for a 46.2% share in 2024, making it the dominant sub-segment. This category includes ESD flooring, packaging and coatings that support large-scale manufacturing environments. Its growth is driven by expanding semiconductor fabrication, stricter quality-control protocols and rising deployment of cleanroom infrastructure across electronics and automotive facilities. ESD protection devices and ESD monitoring and test equipment collectively hold the remaining market share, supported by increasing use of sensitive microelectronic components and the need for real-time static charge measurement in production lines.

- Sherwin-Williams provides electrostatic dissipative flooring systems for semiconductor manufacturing facilities, offering chemical resistance and protection against static damage in cleanrooms and fabrication areas.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By application

Consumer electronics and semiconductors emerged as the dominant application segment, securing a 52.8% share in 2024. The segment’s leadership is driven by rising production of smartphones, wearables, advanced chips and PCB assemblies that require stringent ESD control during design and assembly. Increasing wafer miniaturization and higher circuit density further strengthen demand for robust ESD protection systems. Automotive electronics and EV components and aerospace, defense and industrial manufacturing together account for the remaining share, supported by electrification trends, safety standards and reliability-critical electronic systems.

- Nexperia launched a high-surge ESD diode in a wafer-level chip-scale package in 2024 for wearables. The compact design enhances board efficiency in devices with USB-C charging and sensors.

By end user

Electronics manufacturing services providers dominate the market with a 41.6% share in 2024, driven by large-volume electronic assembly operations and contract manufacturing for global OEMs. The segment benefits from rising outsourcing of PCB assembly, surface-mount technology lines and semiconductor packaging activities that require consistent static-safe environments. OEMs represent the second-largest share as they integrate in-house quality protection processes, while research laboratories and healthcare facilities contribute the remaining share, driven by precision instrumentation, medical device manufacturing and controlled laboratory environments where ESD-induced failures must be prevented.

Electrostatic Discharge Technologies Market Key Growth Drivers

Rapid expansion of semiconductor and electronics manufacturing

The electrostatic discharge technologies market grows significantly due to the accelerating expansion of semiconductor fabrication, PCB assembly and microelectronics manufacturing worldwide. Increasing wafer miniaturization, higher transistor density and advanced packaging technologies heighten the sensitivity of components to electrostatic failures, driving large-scale adoption of ESD flooring, coatings, protective packaging and grounding systems. The surge in smartphone production, wearable devices, data-center electronics and consumer Internet of Things products further strengthens demand. Governments and manufacturing clusters in Asia-Pacific and North America invest heavily in semiconductor capacity expansion, reinforcing the need for robust ESD control infrastructure across cleanrooms and high-precision assembly environments.

- STMicroelectronics deploys ESD protection devices like the BPF8089-01SC6, which safeguards GNSS receiver chipsets such as the STA8089GA against eight-kilovolt ESD-HBM transients while maintaining downstream voltage thresholds.

Rising deployment of automotive electronics and electric vehicles

The increasing integration of electronic control units, power electronics, battery-management systems and infotainment modules in modern vehicles acts as a major growth catalyst. Electric vehicles and hybrid systems require highly reliable semiconductor components, where static discharge failures can affect safety, efficiency and operational integrity. Automotive OEMs and Tier-1 suppliers adopt advanced ESD-safe materials, test equipment and protection devices across manufacturing, assembly and repair environments. Growing regulatory emphasis on reliability, combined with expansion of ADAS, autonomous systems and smart mobility platforms, fuels sustained investment in standardized ESD-protection frameworks across automotive production ecosystems.

- Bosch mandates ESD-safe and anti-static materials in all tape-and-reel packaging for automotive electronics, supporting baking up to 40 degrees Celsius for 79 days per J-STD-033 norms without mechanical alterations.

Stringent quality-control standards and compliance mandates

Global manufacturing environments increasingly operate under strict quality-assurance regulations and industry standards such as ANSI/ESD S20.20 and IEC-61340, which reinforce adoption of structured ESD-control programs. Electronics producers, EMS providers, aerospace contractors and medical device manufacturers deploy certified ESD technologies to minimize warranty costs, product recalls and latent defect risks. Corporate quality programs now integrate continuous monitoring, ESD audits and operator-safety protocols, encouraging widespread use of grounded workstations, conductive materials and real-time charge measurement solutions. The growing importance of zero-defect manufacturing, combined with customer-driven reliability benchmarks, strengthens long-term demand for compliant and audit-ready ESD-protection systems.

Electrostatic Discharge Technologies Market Key trends and opportunities

Shift toward smart, connected and AI-enabled ESD monitoring systems

A major trend shaping the market is the transition from manual ESD inspection toward intelligent, sensor-driven and network-connected monitoring platforms. Manufacturers increasingly deploy IoT-enabled wrist-strap testers, smart grounding modules and cloud-based analytics dashboards that track static charge levels in real time across workstations and production lines. Integration with manufacturing execution systems and quality-management systems enables predictive alerts, automated compliance reporting and data-driven risk prevention. Vendors are also exploring AI-powered anomaly detection and digital-twin environments to optimize ESD-control performance. This evolution opens significant opportunities for software-centric ESD ecosystems, subscription-based monitoring services and Industry 4.0-aligned production environments.

- Transforming Technologies offers the WST200, a portable wrist strap tester that measures resistance between the operator, wrist strap and ground cord using nine-volt DC, indicating high, low or OK status via LED and audible alarm with factory-set parameters of 800K to 10M ohms.

Growing adoption of ESD solutions in healthcare, aerospace and high-reliability sectors

New growth opportunities are emerging from sectors where operational safety and reliability are mission-critical. Medical device assembly, diagnostic instrumentation, aerospace avionics and defense electronics increasingly rely on precision circuits vulnerable to static discharge damage. As these industries scale production and modernize facilities, they invest in static-safe materials, conductive flooring, ESD-certified workbenches and contamination-controlled environments. The rise of digital healthcare equipment, implantable devices and space-grade electronics further expands the application scope, positioning ESD technologies as strategic enablers of product longevity, safety compliance and performance assurance across specialized manufacturing domains.

- Bosch Rexroth provides ESD-interlinked manual workstations designed for medical engineering assembly lines, featuring electrostatically conductive or dissipative components that meet DIN EN 61340-5-1 standards for protecting sensitive devices.

Electrostatic Discharge Technologies Market Key challenges

High implementation costs and complexity of ESD program integration

One of the key challenges for the market is the high initial cost associated with implementing comprehensive ESD-control programs. Large-scale deployments require facility upgrades, specialized materials, staff training, certification audits and ongoing maintenance investments, which may slow adoption among small and midsize manufacturers. Integrating ESD systems into legacy production environments can be technically complex, requiring workflow redesign and operational downtime. Organizations without dedicated quality-engineering teams often struggle to maintain continuous compliance, leading to partial or inconsistent implementation. This cost-complexity barrier limits penetration across cost-sensitive markets and emerging-economy manufacturing ecosystems.

Lack of awareness and inconsistent compliance practices across industries

Despite technological advancement, many organizations still underestimate the operational and financial risks associated with ESD-induced failures, particularly in developing manufacturing ecosystems. Limited technical awareness, absence of standardized enforcement and fragmented training programs result in inconsistent adherence to global ESD standards. Some industries continue to rely on basic grounding practices instead of structured, audited ESD-control systems, increasing defect probability and reliability concerns. Addressing this challenge requires wider industry education, certification-driven adoption models and stronger collaboration between ESD solution providers, regulatory bodies and manufacturing quality leaders.

Regional analysis

North America

North America holds a strong position in the electrostatic discharge technologies market, accounting for a 34.6% market share in 2024, driven by advanced semiconductor fabrication, aerospace electronics and high-reliability manufacturing environments. The United States leads regional demand due to the presence of major EMS providers, automotive electronics plants and defense technology manufacturers that require stringent ESD-control compliance. Investments in cleanroom infrastructure, quality-assurance programs and electronics R&D further strengthen adoption. Growing EV production, coupled with strong enforcement of ANSI/ESD standards, supports sustained market growth across healthcare devices, industrial automation and precision electronic assemblies.

Europe

Europe captured a 27.3% market share in 2024, supported by advanced automotive manufacturing, aerospace engineering hubs and strong electronics quality-compliance frameworks. Germany, France and the United Kingdom drive demand through high-value electronics assembly, avionics production and laboratory instrumentation manufacturing that rely on certified ESD environments. The region benefits from strict regulatory alignment with IEC-61340 standards and growing investments in semiconductor packaging ecosystems. Expansion of electric mobility platforms, industrial automation programs and renewable-energy control electronics further enhances the need for ESD-safe materials, monitoring systems and protection devices.

Asia-Pacific

Asia-Pacific represents the largest growth-driven region, securing a 29.8% market share in 2024, fueled by massive semiconductor fabrication, consumer electronics assembly and contract manufacturing operations across China, South Korea, Taiwan, Japan and India. Rapid expansion of PCB production, smartphone manufacturing, EV electronics and chip-packaging facilities increases reliance on static-safe flooring, coatings, packaging and grounding solutions. Government-backed industrial corridors, electronics export clusters and rising OEM outsourcing further accelerate adoption. Increasing penetration of smart factories and Industry 4.0 initiatives strengthens demand for automated ESD monitoring systems and compliance-certified production environments.

Latin America

Latin America accounted for a 5.4% market share in 2024, supported by expanding electronics assembly, automotive component manufacturing and industrial equipment production across Mexico and Brazil. The region experiences rising adoption of ESD-safe workstations, conductive packaging and testing equipment as multinational EMS providers strengthen regional manufacturing footprints. Growth is influenced by increasing investments in automotive electronics, consumer device assembly and medical equipment production that require reliability-controlled environments. Efforts to align with global quality-assurance standards and gradual modernization of industrial infrastructure continue to create steady opportunities for ESD technology deployment.

Middle East and Africa

The Middle East and Africa region held a 2.9% market share in 2024, driven by emerging investments in industrial electronics, defense equipment assembly and healthcare technology manufacturing across Gulf economies. Growth is supported by the establishment of specialized manufacturing parks, electronics refurbishment facilities and laboratory research environments that require controlled static-protection measures. Increasing government-led industrial diversification programs encourage the adoption of ESD flooring, monitoring devices and certified protective materials. Rising participation in high-reliability manufacturing sectors is expected to strengthen future market penetration.

Electrostatic Discharge Technologies Market Segmentations:

By Product Type

- ESD Control Materials

- ESD Protection Devices

- ESD Monitoring & Test Equipment

By Application

- Consumer Electronics & Semiconductors

- Automotive Electronics & EV Components

- Aerospace, Defense, and Industrial Manufacturing

By End User

- Electronics Manufacturing Services (EMS) Providers

- OEMs

- Research Laboratories & Healthcare Facilities

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive landscape

The competitive landscape in the electrostatic discharge technologies market is shaped by leading players such as 3M Co., Desco Industries Inc., PPG Industries Inc., Henkel AG & Co. KGaA, Keyence Corp., Texas Instruments Inc., STMicroelectronics N.V., Microchip Technology Inc., Protektive Pak and Elmech ESD Solutions. The market features a mix of global manufacturers, electronics component suppliers and specialty material providers that focus on reliability, product innovation and compliance-driven ESD protection solutions. Companies emphasize portfolio expansion across ESD flooring, coatings, packaging materials, monitoring systems and protection devices to address diverse end-use environments including semiconductor fabrication, automotive electronics, aerospace and EMS operations. Strategic priorities include technology integration, automation-enabled ESD monitoring and certification-based offerings aligned with ANSI/ESD and IEC standards. Partnerships with OEMs and contract manufacturers, along with regional manufacturing expansions in Asia-Pacific and North America, further strengthen market presence.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key player analysis

- 3M Co.

- Desco Industries Inc.

- PPG Industries Inc.

- Henkel AG & Co. KGaA

- Keyence Corp.

- Texas Instruments Inc.

- STMicroelectronics N.V.

- Microchip Technology Inc.

- Protektive Pak (Botron Company Inc.)

- Elmech ESD Solutions

Recent developments

- In Dec. 2025, Cortec introduced EcoSonic VpCI-125 HP Permanent ESD Stretch Film, offering permanent ESD protection with added corrosion resistance for electronics packaging.

- In March 2025, EOS/ESD Association Services LLC partnered with SRF Technologies to deliver comprehensive ESD and EOS diagnostic, mitigation and testing solutions worldwide.

- In Feb. 2025, Semtech Corp. launched a new ESD protection device, the RClamp10022PWQ, designed for automotive Ethernet applications to support high-speed networks used in ADAS and autonomous driving systems.

- In July 2024, Sweden’s ESD Center acquired Denmark’s ZENITECH.dk to enhance its electrostatic discharge packaging and cleanroom product offerings.

Report coverage

The research report offers an in-depth analysis based on product type, application, end user and geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams and key applications. The report also includes insights into the competitive environment, SWOT analysis, current market trends, and primary drivers and constraints. It examines market dynamics, regulatory scenarios and technological advancements shaping the industry, and provides strategic recommendations for new entrants and established companies.

Future outlook

- The market will witness stronger adoption of advanced ESD monitoring and automation-driven control systems across electronics manufacturing environments.

- Semiconductor miniaturization and high-density chip architectures will continue to accelerate demand for robust ESD protection frameworks.

- Automotive electronics and EV component production will drive sustained investment in certified ESD-safe materials and assembly infrastructure.

- Industry 4.0 integration will enable data-driven ESD risk assessment, predictive maintenance and centralized compliance tracking.

- Healthcare, aerospace and defense manufacturing will emerge as expanding application areas requiring high-reliability ESD solutions.

- Vendors will focus on developing eco-efficient and durable ESD materials that support cleanroom and sustainability standards.

- Outsourced electronics manufacturing and EMS expansion will increase deployment of standardized ESD programs across global production networks.

- Regulatory alignment with international ESD safety and quality standards will strengthen enforcement and program adoption.

- Cloud-connected and AI-enabled ESD analytics platforms will gain traction to support real-time monitoring and reporting.

- Market participants will emphasize training, certification services and lifecycle support to enhance operational reliability and customer value.