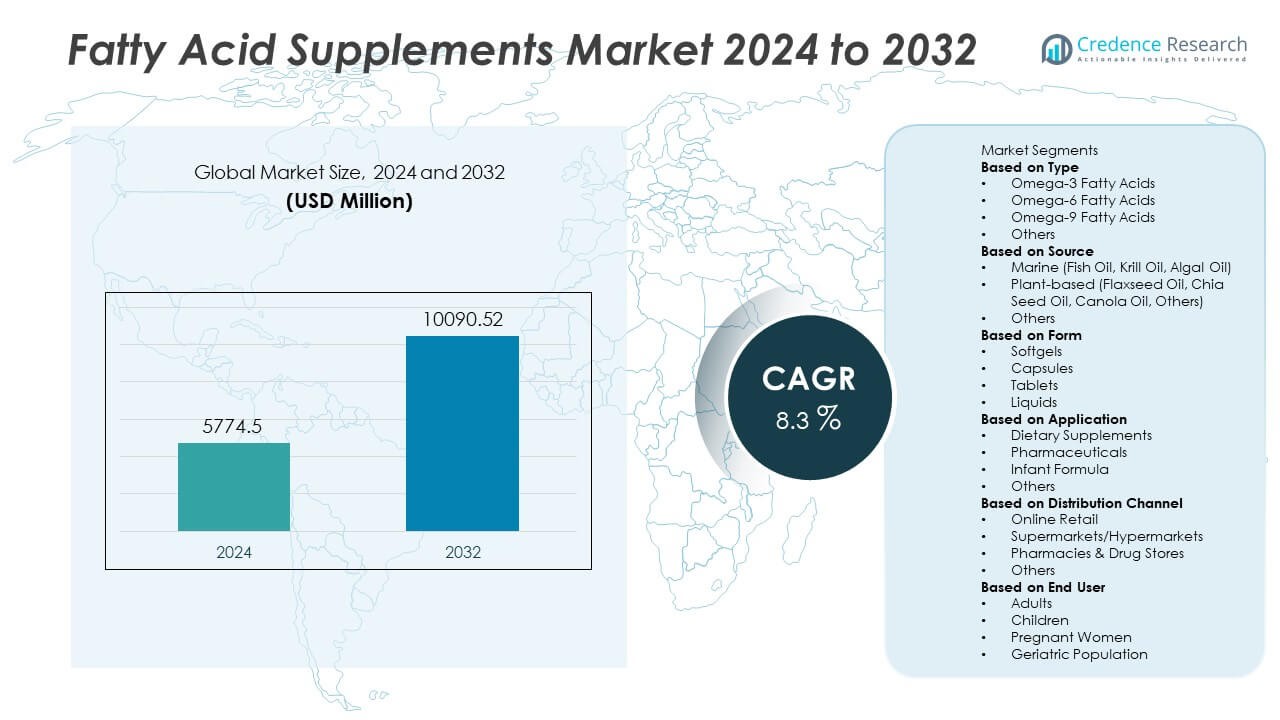

Market Overview

Facial Implants Market size was valued USD 3164.5 million in 2024 and is anticipated to reach USD 4930.66 million by 2032, at a CAGR of 5.7% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Facial Implants Market Size 2024 |

USD 3164.5 Million |

| Facial Implants Market, CAGR |

5.7% |

| Facial Implants Market Size 2032 |

USD 4930.66 Million |

The Facial Implants Market features strong competition among leading companies such as Stryker Corporation, Johnson & Johnson, Medartis AG, KLS Martin Group, Xilloc, Sientra Inc., OsteoMed, EUROS, Hanson Medical, Inc., and AART Inc. These firms drive market growth through continuous innovation in 3D-printed implants, biocompatible materials, and patient-specific reconstruction solutions. Strategic partnerships with healthcare institutions and investments in digital surgical planning tools enhance clinical precision and outcomes. North America dominates the global market, holding a 38% share, supported by advanced healthcare infrastructure, high adoption of cosmetic and reconstructive surgeries, and strong regulatory compliance. This regional leadership is further reinforced by continuous product development and widespread surgeon training initiatives.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Facial Implants Market size was valued at USD 3164.5 million in 2024 and is projected to reach USD 4930.66 million by 2032, registering a CAGR of 5.7% during the forecast period.

- Market growth is driven by rising demand for facial reconstructive and aesthetic surgeries, supported by technological advancements in 3D printing and biocompatible implant materials.

- The market is witnessing a trend toward personalized implant design, digital surgical planning, and minimally invasive techniques that improve patient outcomes and recovery times.

- Strong competition among major players focuses on innovation, mergers, and product differentiation, while high procedural costs and regulatory requirements act as key restraints.

- North America leads with a 38% market share, followed by Europe and Asia-Pacific, while chin and mandibular implants represent the dominant product segment due to their widespread use in reconstructive and cosmetic procedures.

Market Segmentation Analysis:

By Product

The injectables segment dominates the facial implants market, accounting for over 40% share in 2024. Their popularity stems from minimal invasiveness, quick recovery, and wide use in aesthetic enhancements. Products such as hyaluronic acid and botulinum toxin-based injectables are widely adopted for wrinkle reduction and facial contouring. Continuous advancements in filler longevity and safety drive growth. The rising acceptance of non-surgical cosmetic procedures and personalized treatments further strengthens the injectable segment’s dominance among both male and female consumers.

- For instance, Johnson & Johnson MedTech’s MONOVISC® injection, manufactured by Anika Therapeutics, delivers a high molecular weight hyaluronan dose of 88 mg in 4 mL per injection.

By Material

Polymer-based implants lead the market with a 35% share, driven by their flexibility, biocompatibility, and cost-effectiveness. Materials like silicone and polyethylene are commonly used in chin, cheek, and nasal augmentations. These materials provide natural aesthetics and long-term stability with low complication rates. Advancements in 3D printing and customized polymer implant manufacturing have enhanced precision and patient outcomes. Increasing surgeon preference for lightweight and moldable materials continues to propel the polymer segment forward in cosmetic and reconstructive applications.

- For instance, Extrusion-based 3D printing of poly(ε-caprolactone) (PCL) implants has been used by various researchers to achieve sustained drug release profiles. The ability to precisely control the implant’s internal geometry, including strut width and channel diameter, is a known method for controlling drug diffusion rates in biomedical research.

By Procedure

The rhinoplasty segment holds the largest share of over 38%, making it the dominant procedure in the facial implants market. The growing demand for nose reshaping for both cosmetic and corrective purposes fuels its leadership. Technological improvements in 3D imaging and computer-assisted modeling have refined surgical accuracy and patient satisfaction. Rising social media influence and awareness about facial harmony further increase rhinoplasty adoption. The combination of aesthetic enhancement with functional correction continues to make rhinoplasty a preferred procedure among both men and women globally.

Key Growth Drivers

Rising Demand for Aesthetic Enhancement

The growing preference for facial aesthetics among millennials and middle-aged consumers drives market expansion. Increasing social media influence and the desire for youthful appearances are pushing demand for facial implants, particularly chin and cheek augmentations. The availability of minimally invasive techniques and shorter recovery times enhances adoption. Cosmetic clinics and medical tourism in regions like North America and Asia-Pacific further support market growth, creating strong demand for both permanent and temporary facial implant solutions.

- For instance, Hanson Medical holds FDA 510(k) clearance for its MONARCH Nasal Implant (K071018) as an internal nasal prosthesis.

Their website states they manufacture “soft-solid silicone implants” ready for immediate shipment, with custom orders built to “exact specifications” down to durometer (firmness) grade.

Technological Advancements in Implant Design

Continuous innovation in implant materials and manufacturing methods significantly boosts market performance. The use of 3D imaging, computer-aided design, and patient-specific implants enables higher precision and better aesthetic outcomes. Lightweight, biocompatible polymers and porous metals reduce surgical risks and improve tissue integration. Companies are investing in advanced modeling software and customized implant production, helping surgeons achieve natural facial symmetry. These developments enhance patient satisfaction and expand the clinical applications of facial implants in both reconstructive and cosmetic surgeries.

- For instance, Sientra publishes long-term clinical data showing complication rates from its 10-year core study, which involved 1,788 patients (3,506 implants). The study reported a rupture-free rate of 91.4% by patient, while the capsular contracture (Baker Grade III/IV) incidence was 13.5%.

Increasing Reconstructive Surgeries Post-Trauma

The rising number of facial injuries caused by accidents and sports activities is fueling demand for reconstructive facial implants. Hospitals and trauma centers increasingly rely on implants for bone reconstruction and facial alignment. Surgeons use advanced biomaterials that mimic natural bone and promote faster healing. Government support for healthcare infrastructure and insurance coverage for trauma-related surgeries further boosts adoption. The expansion of reconstructive applications beyond aesthetics contributes significantly to overall market growth.

Key Trends & Opportunities

Shift Toward Minimally Invasive and Injectable Solutions

The market is witnessing a strong transition toward injectable fillers and minimally invasive procedures. Patients prefer non-surgical options for facial enhancement due to reduced downtime and lower risks. Advanced dermal fillers, such as hyaluronic acid and collagen-based injectables, offer flexible and customizable results. Manufacturers are focusing on long-lasting formulations and improved product safety. This trend opens new opportunities for aesthetic professionals to offer hybrid treatments combining surgical and non-surgical solutions for enhanced outcomes.

- For instance, KLS Martin claims more than 16,000 variants of surgical instruments across disciplines (craniomaxillofacial, dental, general surgery) with stringent quality controls in metallurgy, finishing, and final inspection.

Personalization and 3D Printing Integration

Personalized facial implants created through 3D printing technology are reshaping surgical planning and patient care. Surgeons can now design implants based on individual anatomy using digital scans, ensuring precise fitting and aesthetic balance. 3D-printed implants minimize complications and reduce surgical time. This trend is gaining momentum in reconstructive and cosmetic applications, as demand for custom, patient-specific solutions grows. The integration of artificial intelligence and imaging tools further enhances accuracy and innovation in implant manufacturing.

- For instance, OsteoMed offers the Mincro™ system, which employs screws of 1.2 mm and 1.6 mm diameters and matching instrumentation for precise bone graft fixation.

Key Challenges

High Cost of Facial Implant Procedures

The significant cost associated with facial implant surgeries limits accessibility for many consumers, especially in developing regions. Expenses include surgical fees, hospital charges, and post-operative care, making such procedures affordable mainly to high-income groups. Limited reimbursement policies further constrain adoption. Although technological advancements improve outcomes, they also raise overall treatment costs. This financial barrier continues to restrict market penetration among middle-class consumers despite growing aesthetic awareness.

Risk of Complications and Regulatory Barriers

Facial implant procedures involve risks such as infection, nerve damage, and asymmetry, which affect patient confidence. Stringent regulatory requirements for material approval and surgical standards delay new product launches. Manufacturers must invest heavily in clinical trials to ensure safety and compliance. These challenges slow innovation and increase operational costs. Maintaining consistent quality and minimizing adverse outcomes remain critical concerns for industry players aiming to expand their presence in global markets.

Regional Analysis

North America

North America dominates the facial implants market with a 38% share, driven by strong demand for cosmetic procedures and advanced surgical infrastructure. The United States leads regional growth, supported by the presence of skilled surgeons and high consumer spending on aesthetic treatments. Technological innovations in 3D-printed implants and customized surgical solutions strengthen market competitiveness. Rising awareness of facial symmetry and minimally invasive enhancement options further supports adoption. Additionally, the growing influence of media-driven beauty standards continues to propel both surgical and injectable facial procedures across the region.

Europe

Europe holds a 27% market share, supported by growing acceptance of facial reconstructive and cosmetic surgeries. Countries such as Germany, France, and the United Kingdom drive regional demand through robust healthcare systems and established aesthetic clinics. The adoption of biocompatible materials and innovative implant technologies enhances patient safety and treatment precision. Increasing popularity of facial contouring procedures, coupled with medical tourism in Southern Europe, supports consistent market expansion. Regulatory compliance with stringent CE marking standards ensures high-quality implant offerings, further strengthening patient trust and procedural adoption.

Asia-Pacific

Asia-Pacific accounts for a 24% share and is the fastest-growing region in the facial implants market. Rising disposable income, urbanization, and a growing middle-class population fuel cosmetic enhancement demand, especially in China, South Korea, and Japan. The region benefits from affordable treatment options and increasing investments in medical aesthetics infrastructure. Expanding awareness of non-surgical facial treatments and advancements in implant customization contribute to the market’s rapid evolution. South Korea leads innovation in minimally invasive facial procedures, while India’s growing cosmetic surgery industry strengthens regional market penetration.

Latin America

Latin America captures a 7% share, led by Brazil and Mexico, where aesthetic surgery is deeply ingrained in cultural trends. Increasing availability of affordable cosmetic treatments and trained plastic surgeons drives the region’s growth. Government initiatives promoting medical tourism enhance international patient inflow. The adoption of advanced facial implants and minimally invasive techniques continues to expand, especially in urban centers. However, limited access to advanced technologies in smaller markets poses a challenge. Continued infrastructure development and awareness campaigns are expected to support steady market growth across the region.

Middle East & Africa

The Middle East & Africa region holds a 4% market share, with rapid growth in countries such as the UAE, Saudi Arabia, and South Africa. Increasing demand for aesthetic improvements among younger populations and rising disposable incomes drive regional expansion. Advanced cosmetic centers in Dubai and Riyadh are adopting state-of-the-art implant technologies and procedures. Government investments in healthcare modernization and medical tourism further support growth. However, limited local manufacturing capabilities and dependency on imports restrain market development. The region’s growing preference for facial reconstruction post-trauma presents emerging opportunities for market players.

Market Segmentations:

By Product:

By Material:

By Procedure:

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The Facial Implants Market is highly competitive, with key players including Medartis AG, Johnson & Johnson, AART Inc., Hanson Medical, Inc., Xilloc, Sientra Inc., Stryker Corporation, KLS Martin Group, EUROS, and OsteoMed. The Facial Implants Market is characterized by strong competition and continuous innovation driven by technological advancements and aesthetic demand. Companies are investing heavily in research and development to design biocompatible materials, 3D-printed implants, and patient-specific solutions that enhance surgical precision and recovery outcomes. The adoption of advanced imaging and computer-aided design (CAD) technologies supports customized implant production, improving fit and reducing complication risks. Strategic collaborations between medical device manufacturers and healthcare providers further expand product accessibility and clinical expertise. Moreover, growing awareness of facial reconstructive procedures, coupled with rising disposable income and improved healthcare infrastructure, continues to create growth opportunities across both developed and emerging markets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Medartis AG

- Johnson & Johnson

- AART Inc.

- Hanson Medical, Inc.

- Xilloc

- Sientra Inc

- Stryker Corporation

- KLS Martin Group

- EUROS

- OsteoMed

Recent Developments

- In May 2025, Meta announced a feature internally referred to as “super sensing.” In super sensing mode, the glasses’ built-in cameras and sensors will remain on and recording throughout the wearer’s day.

- In July 2024, American Exchange Group acquired Indie Lee, a leading clean beauty brand known for its plant-based skincare products. The acquisition enhances American Exchange Group’s position in the premium, sustainable beauty market.

- In June 2024, Google, a leading software company, is testing the facial tracking system for the corporate campus with the help of Google’s Security and Resilience Services (GSRS) team; the test is currently taking place in Kirkland, Washington.

- In July 2023, Sakra World Hospital inaugurated an advanced Facial Palsy Care Centre, incorporating technology and an expert cohort of highly qualified surgeons. Through the integration of innovative technological infrastructure and a proficient multidisciplinary team of surgeons and allied healthcare professionals, the center aimed to redefine treatment paradigms, enhancing overall therapeutic outcomes, and substantially elevating the quality of life for individuals having facial palsy.

Report Coverage

The research report offers an in-depth analysis based on Product, Material, Procedure and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The demand for customized 3D-printed facial implants will continue to rise globally.

- Technological integration in implant design will enhance surgical accuracy and patient outcomes.

- Growing acceptance of minimally invasive facial reconstruction will boost product innovation.

- Advancements in biomaterials will improve implant durability and biocompatibility.

- The aesthetic surgery segment will expand with increasing consumer focus on facial enhancement.

- Strategic collaborations between medical device firms and hospitals will strengthen market presence.

- Regulatory approvals for advanced implant materials will accelerate new product launches.

- Emerging economies will witness higher adoption due to improving healthcare infrastructure.

- Digital planning and AI-assisted surgical tools will redefine implant customization processes.

- Sustainability initiatives in production and packaging will gain importance among manufacturers.