Market Overview

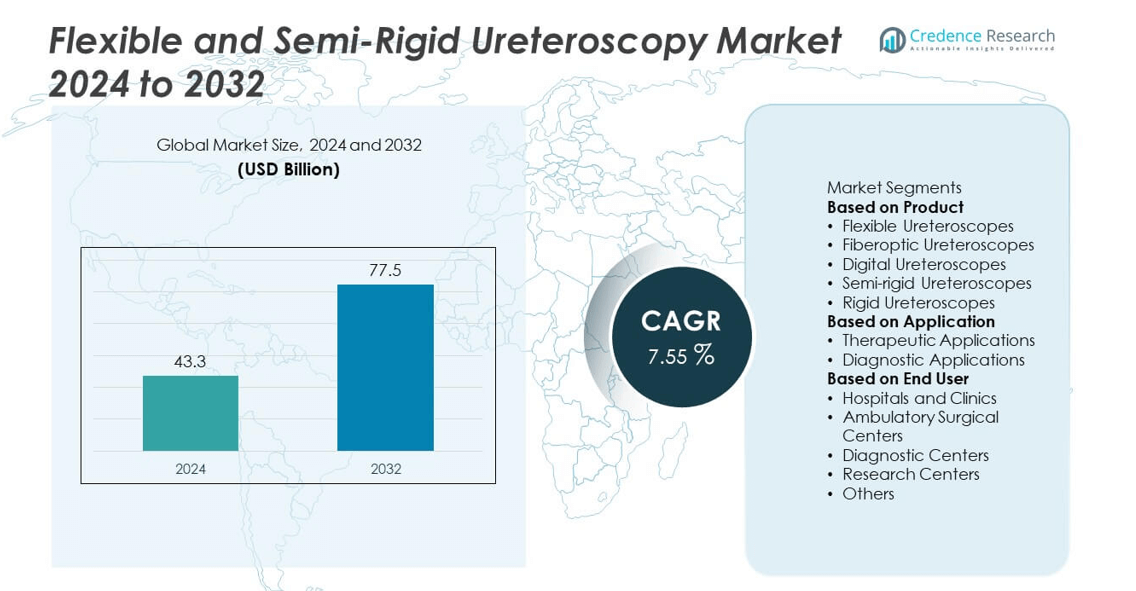

The Flexible and Semi-Rigid Ureteroscopy Market was valued at USD 43.3 billion in 2024 and is projected to reach USD 77.5 billion by 2032, expanding at a CAGR of 7.55% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Flexible and Semi-Rigid Ureteroscopy Market Size 2024 |

USD 43.3 Billion |

| Flexible and Semi-Rigid Ureteroscopy Market , CAGR |

7.55% |

| Flexible and Semi-Rigid Ureteroscopy Market Size 2032 |

USD 77.5 Billion |

The Flexible and Semi-Rigid Ureteroscopy Market grows with rising prevalence of kidney stones, urinary tract disorders, and urological cancers that require minimally invasive treatments. Increasing patient preference for faster recovery and reduced hospital stays fuels demand for ureteroscopic procedures.

The Flexible and Semi-Rigid Ureteroscopy Market demonstrates wide geographic presence, supported by advanced healthcare adoption in developed regions and rapid growth in emerging economies. North America leads with strong infrastructure, skilled professionals, and high demand for minimally invasive procedures, while Europe shows robust uptake driven by technological innovation and an aging population requiring urological care. Asia-Pacific emerges as the fastest-growing region, fueled by rising kidney stone prevalence, expanding healthcare investments, and growing awareness of patient-friendly treatments in China, India, and Japan. Latin America and the Middle East & Africa gradually strengthen adoption with improvements in hospital infrastructure and urban healthcare access. Key players shaping this market include Stryker, Olympus Corporation, Boston Scientific, and KARL STORZ. These companies focus on developing advanced flexible and semi-rigid ureteroscopes, integrating imaging and laser technologies, and expanding their product portfolios to address the rising global demand for precise, safe, and cost-effective urology procedures.

Market Insights

- The Flexible and Semi-Rigid Ureteroscopy Market was valued at USD 43.3 billion in 2024 and is projected to reach USD 77.5 billion by 2032, expanding at a CAGR of 7.55% during the forecast period.

- Rising prevalence of kidney stones, urinary tract disorders, and urological cancers drives strong demand for minimally invasive ureteroscopic procedures that ensure reduced recovery times and improved patient outcomes.

- Technological advancements, including digital ureteroscopes, high-definition imaging, laser lithotripsy integration, and disposable single-use devices, create innovation momentum and expand the scope of clinical applications.

- Competitive activity remains strong, with key players such as Stryker, Olympus Corporation, Boston Scientific, and KARL STORZ focusing on expanding product portfolios, investing in R&D, and targeting both developed and emerging healthcare markets.

- High equipment costs, recurring maintenance expenses, and technical limitations such as reduced durability of flexible scopes act as restraints, particularly in cost-sensitive healthcare settings and smaller medical facilities.

- North America demonstrates strong adoption supported by advanced healthcare infrastructure and favorable reimbursement, while Europe shows robust uptake driven by technological innovation and aging demographics.

- Asia-Pacific emerges as the fastest-growing region with rising healthcare investments in China, India, and Japan, while Latin America and the Middle East & Africa gradually expand adoption through improving hospital infrastructure and urban healthcare access.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Prevalence of Urological Disorders and Kidney Stones

The Flexible and Semi-Rigid Ureteroscopy Market benefits from the rising incidence of kidney stones, urinary tract disorders, and urological cancers. Changing dietary habits, sedentary lifestyles, and dehydration-related conditions increase the burden of kidney stone cases worldwide. Hospitals and clinics report growing demand for minimally invasive procedures to manage these conditions effectively. It supports adoption of ureteroscopes as they provide precise visualization and access to affected areas. Physicians prefer these devices for reduced patient trauma and shorter recovery periods. Rising patient awareness about advanced treatment options further strengthens the growth trajectory.

- For instance, Boston Scientific’s LithoVue Elite single-use digital flexible ureteroscope, introduced real-time intrarenal pressure monitoring with a 270° deflection range and compatibility with laser fibers up to 365 μm, ensuring safer kidney stone management.

Advancements in Visualization and Imaging Technologies

Technological progress in digital imaging and high-definition visualization drives the growth of the Flexible and Semi-Rigid Ureteroscopy Market. Advanced ureteroscopes provide clearer views of renal anatomy, improving diagnostic accuracy and procedural efficiency. Integration of fiber optics, narrow-band imaging, and enhanced light transmission expands treatment potential. It allows urologists to perform complex interventions with greater precision and safety. The development of smaller, more maneuverable scopes improves access to difficult areas within the urinary tract. Growing investment in R&D ensures continuous upgrades in visualization systems, reinforcing device adoption.

- For instance, Olympus received FDA clearance for its RenaFlex single-use flexible ureteroscope, featuring a 9.5 Fr outer diameter, 3.6 Fr working channel, and a 120° field of view with 270° articulation, delivering enhanced visualization for complex urological procedures.

Shift Toward Minimally Invasive Procedures and Patient-Centric Care

The Flexible and Semi-Rigid Ureteroscopy Market gains momentum through the global preference for minimally invasive surgeries. Patients increasingly demand procedures that minimize hospital stays, reduce postoperative pain, and improve recovery times. Ureteroscopic interventions align with this trend by offering safe and effective alternatives to open surgeries. It enhances patient satisfaction and strengthens confidence in advanced urological care. Healthcare providers emphasize solutions that balance treatment outcomes with improved quality of life. Rising focus on patient-centered approaches continues to drive acceptance of ureteroscopic devices across medical facilities.

Growing Adoption of Disposable and Cost-Efficient Devices

Adoption of single-use ureteroscopes creates strong opportunities for the Flexible and Semi-Rigid Ureteroscopy Market. Disposable devices reduce risks of cross-contamination and minimize costs linked to sterilization and repair. Hospitals and ambulatory centers increasingly recognize the value of these innovations in improving procedural safety. It supports wider adoption, particularly in high-volume healthcare settings. Manufacturers invest in cost-efficient designs without compromising on performance or visualization quality. Growing demand for affordable yet effective solutions ensures sustainable growth across developed and emerging regions.

Market Trends

Rising Adoption of Digital and Disposable Ureteroscopes

The Flexible and Semi-Rigid Ureteroscopy Market experiences significant growth from the introduction of digital and single-use ureteroscopes. Digital scopes deliver high-resolution imaging, improving diagnostic precision and treatment outcomes. Disposable variants address infection control concerns and reduce costs tied to reprocessing and repairs. It encourages adoption among hospitals and ambulatory centers handling high patient volumes. The convenience and safety of these devices strengthen their role in modern urology. Rising demand for cost-efficient, infection-free solutions continues to fuel this trend.

- For instance, KARL STORZ introduced the FLEX-XC1 single-use video ureteroscope, featuring an 8.5 Fr sheath, a 3.5 Fr working channel, and a 70 cm working length with 270° bidirectional deflection, ensuring high-definition visualization.

Miniaturization of Devices and Expanding Clinical Applications

Continuous miniaturization of ureteroscopes creates new opportunities across urology. The Flexible and Semi-Rigid Ureteroscopy Market benefits from smaller, highly flexible scopes that reach deeper into the urinary tract. Miniaturized devices reduce patient trauma, enabling quicker recovery and improved comfort. It supports expansion into pediatric urology and complex renal procedures once limited by scope size. Surgeons gain improved maneuverability without sacrificing visualization quality. Growing demand for devices that address challenging cases reinforces this market trend.

- For instance, HugeMed launched its 6.3 Fr ultra-slim single-use flexible ureteroscope at AUA 2025, designed for enhanced maneuverability in narrow anatomy while maintaining image quality, marking one of the thinnest commercialized digital ureteroscopes available.

Integration of Advanced Imaging and Laser Technologies

The Flexible and Semi-Rigid Ureteroscopy Market grows with integration of laser lithotripsy systems and advanced imaging tools. High-powered laser systems improve stone fragmentation efficiency and reduce procedure times. Enhanced imaging techniques, such as narrow-band imaging, support better visualization of tissue and vascular structures. It allows urologists to achieve higher success rates with minimal complications. Combining ureteroscopes with laser technologies creates comprehensive solutions for kidney stone management. This integration strengthens clinical outcomes and expands treatment adoption.

Expanding Role of Outpatient and Ambulatory Surgical Centers

The rise of ambulatory care significantly influences the Flexible and Semi-Rigid Ureteroscopy Market. Ambulatory surgical centers adopt these devices to meet growing demand for minimally invasive urological procedures. Shorter recovery times and lower hospitalization costs attract both patients and providers to outpatient settings. It reinforces the shift from traditional hospital-based care to more accessible treatment models. Device manufacturers increasingly target this segment with cost-effective and portable ureteroscopes. The expanding role of outpatient facilities highlights a lasting trend shaping future demand.

Market Challenges Analysis

High Equipment Costs and Maintenance Burden for Healthcare Providers

The Flexible and Semi-Rigid Ureteroscopy Market faces significant challenges due to high equipment costs and recurring expenses for maintenance. Advanced digital ureteroscopes and laser systems require substantial investment, making adoption difficult for smaller hospitals and clinics. Frequent repairs, sterilization processes, and scope damage during procedures add financial strain. It creates barriers for healthcare facilities in cost-sensitive markets and limits widespread adoption. Budgetary pressures force providers to balance between innovation and affordability, often delaying procurement of advanced devices. These financial constraints restrict market penetration, particularly in developing economies.

Technical Limitations and Shortage of Skilled Professionals

Clinical adoption of ureteroscopes also encounters hurdles linked to technical limitations and workforce shortages. The Flexible and Semi-Rigid Ureteroscopy Market struggles with challenges such as limited durability of flexible scopes, risk of breakage, and reduced lifespan under high patient volumes. Shortage of skilled urologists trained in advanced ureteroscopic procedures compounds the problem. It results in uneven access to high-quality care, especially in rural and low-resource regions. Complex procedures demand expertise in handling laser systems and digital scopes, further raising training requirements. These limitations reduce efficiency and slow the pace of global market expansion.

Market Opportunities

Rising Demand for Minimally Invasive Urological Procedures in Emerging Markets

The Flexible and Semi-Rigid Ureteroscopy Market presents strong opportunities in emerging economies where the burden of kidney stones and urological disorders is increasing. Growing healthcare investments in countries such as China, India, and Brazil expand access to advanced medical devices. Rising patient awareness about minimally invasive options fuels acceptance of ureteroscopic procedures. It creates demand for both flexible and semi-rigid scopes in hospitals and ambulatory care centers. Affordability-focused solutions introduced by manufacturers align with the needs of cost-sensitive regions. Expansion into these markets supports long-term growth and widens the global footprint of ureteroscopic technologies.

Integration of Digital Platforms and Disposable Scope Innovations

Opportunities emerge from the integration of digital health platforms and innovations in disposable ureteroscopes. The Flexible and Semi-Rigid Ureteroscopy Market benefits from single-use devices that address infection risks and reduce reprocessing costs. Hospitals increasingly adopt these solutions to enhance safety and streamline operations. It creates pathways for manufacturers to develop value-driven products targeting high-volume facilities. Incorporating real-time data monitoring and digital connectivity into ureteroscopes also enhances procedural efficiency. Strategic collaborations between device makers and healthcare providers will accelerate adoption of these innovative technologies, creating strong growth potential across global markets.

Market Segmentation Analysis:

By Product

The Flexible and Semi-Rigid Ureteroscopy Market is segmented into flexible ureteroscopes and semi-rigid ureteroscopes. Flexible scopes dominate demand due to their advanced maneuverability, enhanced imaging quality, and suitability for complex renal procedures. Hospitals prefer flexible scopes for accessing hard-to-reach areas of the urinary tract with minimal patient trauma. Semi-rigid ureteroscopes maintain relevance in routine procedures due to lower cost and robust performance. It creates balance in adoption, with flexible scopes driving innovation while semi-rigid variants provide affordability in resource-limited settings. Growth in digital and disposable flexible scopes further reinforces their leadership within this segment.

- For instance, ProSurg announced the launch of its NAVIUS system in March 2025, offering real-time 3D navigation and imaging overlays during ureteroscopy to enhance surgeon precision and procedural outcomes.

By Application

Applications define the growing scope of the Flexible and Semi-Rigid Ureteroscopy Market across urological treatments. Kidney stone management accounts for the largest share, supported by increasing cases linked to lifestyle changes and dehydration risks. Ureteroscopes are also widely used in diagnosing and treating urinary tract disorders, strictures, and urological cancers. Flexible devices enable access to challenging renal anatomy, expanding treatment possibilities. It enhances their adoption for advanced procedures that demand precision and reduced invasiveness. Rising demand for efficient tools in both diagnosis and therapeutic interventions secures long-term opportunities across applications.

- For instance, ELMED’s robotic Avicenna Roboflex system centers on flexible ureteroscopy for renal stones, offering robotic precision that supports urologists in therapeutic procedures—particularly in anatomically challenging cases.

By End User

Hospitals, ambulatory surgical centers, and specialty clinics form the core end-user categories of the Flexible and Semi-Rigid Ureteroscopy Market. Hospitals lead adoption due to their capacity to handle complex procedures, large patient volumes, and access to advanced imaging technologies. Ambulatory surgical centers record rapid growth as minimally invasive urological procedures shift toward outpatient care for cost efficiency and faster recovery. Specialty clinics contribute by offering targeted care in urban regions with rising urology patient loads. It reflects a diverse end-user base where adoption is driven by efficiency, safety, and patient demand for less invasive procedures. Expanding infrastructure across emerging economies further strengthens adoption across all end-user categories.

Segments:

Based on Product

- Flexible Ureteroscopes

- Fiberoptic Ureteroscopes

- Digital Ureteroscopes

- Semi-rigid Ureteroscopes

- Rigid Ureteroscopes

Based on Application

- Therapeutic Applications

- Diagnostic Applications

Based on End User

- Hospitals and Clinics

- Ambulatory Surgical Centers

- Diagnostic Centers

- Research Centers

- Others

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the largest share of the Flexible and Semi-Rigid Ureteroscopy Market at 39% in 2024. The region benefits from advanced healthcare infrastructure, early adoption of innovative technologies, and a high prevalence of kidney stone disease. The United States dominates regional demand, supported by widespread availability of flexible digital ureteroscopes and access to laser lithotripsy systems. It also benefits from favorable reimbursement policies that encourage adoption of minimally invasive procedures across hospitals and ambulatory surgical centers. Canada contributes steadily, with increasing government investment in urology care and growing awareness of advanced treatments. The presence of leading medical device manufacturers further accelerates product availability and supports continuous technological advancement. The region’s emphasis on training programs and skilled workforce enhances procedure outcomes, ensuring strong long-term growth.

Europe

Europe accounts for 28% of the Flexible and Semi-Rigid Ureteroscopy Market in 2024, making it the second-largest region. Rising prevalence of urinary tract disorders and kidney stones drives strong demand across countries such as Germany, France, the United Kingdom, and Italy. Germany leads with advanced healthcare facilities and strong medical device manufacturing capabilities. The United Kingdom emphasizes clinical research and rapid adoption of minimally invasive technologies, while France invests heavily in expanding access to outpatient procedures. It benefits from supportive healthcare policies promoting patient-centered care and wider access to urological treatments. The region also shows strong focus on reducing infection risks, which accelerates adoption of disposable ureteroscopes. Europe’s aging population and growing burden of chronic diseases further reinforce reliance on ureteroscopic procedures.

Asia-Pacific

Asia-Pacific represents 22% of the Flexible and Semi-Rigid Ureteroscopy Market in 2024, emerging as the fastest-growing region. China and Japan are major contributors, with China expanding healthcare infrastructure and Japan advancing innovations in digital and miniaturized ureteroscopes. India shows rapid growth, supported by a rising middle-class population, growing healthcare expenditure, and high prevalence of kidney stone disease. It benefits from cost-effective device production and government initiatives to improve access to advanced care. South Korea and Australia also demonstrate rising adoption of minimally invasive urology procedures. Increasing awareness about patient-friendly treatment methods and strong investments in healthcare technology drive expansion. The region’s large patient base creates substantial opportunities for manufacturers to expand their presence and meet growing demand.

Latin America

Latin America holds 6% of the Flexible and Semi-Rigid Ureteroscopy Market in 2024. Brazil leads the region with strong adoption of minimally invasive treatments and expanding hospital infrastructure. Mexico follows with growing imports of advanced medical devices from North America. It faces challenges such as uneven access to care in rural areas, but urban centers increasingly adopt advanced technologies. Rising prevalence of kidney stone disease and urinary tract disorders boosts procedural demand. Private healthcare providers invest in modern diagnostic and surgical equipment to enhance treatment quality. Efforts to improve training and awareness among urologists support wider device adoption across the region.

Middle East & Africa

The Middle East & Africa account for 5% of the Flexible and Semi-Rigid Ureteroscopy Market in 2024. Gulf countries, led by Saudi Arabia and the United Arab Emirates, drive growth with strong investment in modern hospitals and advanced surgical equipment. South Africa represents a key market within Africa, showing gradual adoption of minimally invasive urology treatments. It benefits from government programs aimed at improving patient access to modern healthcare facilities in urban regions. However, limited infrastructure and affordability issues remain barriers in several African nations. Multinational companies expand their presence to address growing healthcare needs and provide access to disposable and cost-efficient devices. Increasing medical tourism in Gulf countries also creates demand for advanced urological procedures. The region’s focus on improving healthcare delivery ensures steady but gradual growth in the coming years.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Competitive Analysis

Competitive landscape of the Flexible and Semi-Rigid Ureteroscopy Market is shaped by leading players including Stryker, Olympus Corporation, Boston Scientific, Richard Wolf, KARL STORZ, ELMED Medical Systems, Maxer Endoscopy, Rocamed, Vimex Endoscopy, and ProSurg. These companies focus on developing advanced flexible and semi-rigid ureteroscopes with improved imaging capabilities, durability, and maneuverability to address complex urological procedures. Innovation remains a core strategy, with emphasis on digital platforms, laser lithotripsy integration, and disposable single-use scopes that reduce infection risks and operational costs. Strong global presence, extensive distribution networks, and continuous R&D investment enable these players to maintain leadership positions in hospitals and ambulatory surgical centers. The market also demonstrates increasing competition from mid-sized and regional manufacturers introducing cost-effective solutions for emerging economies. Partnerships with healthcare providers and investments in training programs further strengthen adoption rates. The overall competitive environment is defined by rapid technological progress, affordability strategies, and a clear shift toward patient-centric, minimally invasive solutions.

Recent Developments

- In April 2024, Olympus received FDA 510(k) clearance for its RenaFlex single-use flexible ureteroscope, featuring a 9.5 Fr outer diameter, a 3.6 Fr working channel, and 270° active articulation up/down—while offering high-quality visualization with a 120-degree field of view.

- In May 2023, Boston Scientific announced that it was putting $300 million into the expansion of its Galway, Ireland plant expected to add 400 jobs.

- In February 2023, Olympus Corporation also launched their flexible ureteroscope model called EVIS Flex-Q. The scope is designed to be more flexible and easier to manoeuvre than previous models.

- In January 2023, Boston Scientific has just finished its acquiring of Apollo Endosurgery, which has blostered its endoluminal surgery capabilities

Report Coverage

The research report offers an in-depth analysis based on Product, Application, End User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for minimally invasive procedures will continue to expand across global healthcare systems.

- Flexible digital ureteroscopes will gain higher adoption for complex renal interventions.

- Disposable single-use ureteroscopes will grow in demand to reduce infection risks and maintenance costs.

- Integration of laser lithotripsy technologies will improve efficiency and success rates in stone management.

- Advancements in imaging and miniaturization will expand applications into pediatric and complex cases.

- Ambulatory surgical centers will increase their role in driving adoption of ureteroscopes.

- Emerging economies will provide strong growth opportunities through rising healthcare investments.

- Competitive intensity will increase as mid-sized firms introduce affordable and durable devices.

- Training programs for urologists will expand to address shortages in skilled professionals.

- Sustainability initiatives will encourage development of cost-efficient and eco-friendly disposable scopes.