Market Overview

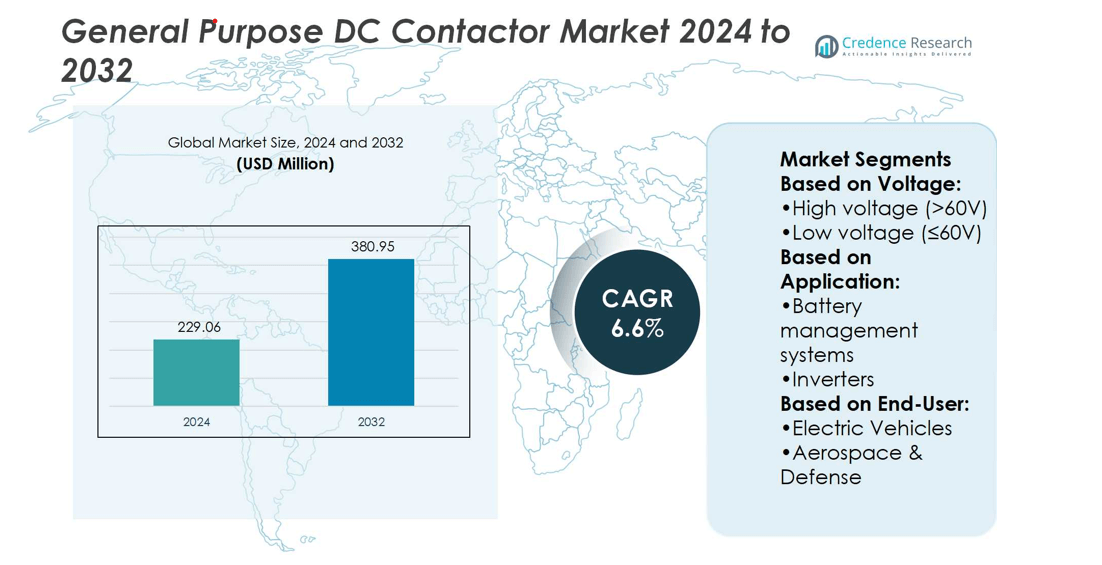

General Purpose DC Contactor Market size was valued at USD 229.06 million in 2024 and is anticipated to reach USD 380.95 million by 2032, at a CAGR of 6.6% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| General Purpose DC Contactor Market Size 2024 |

USD 229.06 million |

| General Purpose DC Contactor Market, CAGR |

6.6% |

| General Purpose DC Contactor Market Size 2032 |

USD 380.95 million |

The General Purpose DC Contactor Market grows through strong demand from electric vehicles, renewable energy systems, and industrial automation. Rising EV adoption drives the need for high-voltage contactors in battery management and charging infrastructure, while renewable projects rely on them for safe circuit isolation and power flow stability. Industrial sectors expand usage to enhance efficiency and safety in automation and heavy machinery. Key trends include the integration of IoT-enabled monitoring, predictive maintenance, and compact lightweight designs. Growing focus on smart grids, digitalized power systems, and sustainable energy projects further strengthens the market’s role in modern energy and mobility ecosystems.

The General Purpose DC Contactor Market shows strong geographical presence with Asia Pacific holding the largest share, driven by EV adoption and renewable energy growth. North America follows with advanced infrastructure and strong industrial automation, while Europe records steady demand supported by strict emission regulations and electrification targets. Latin America and the Middle East & Africa show gradual growth through renewable projects and industrial expansion. Key players driving competition include ABB, Eaton Corporation, Mitsubishi Electric Corporation, LS ELECTRIC, and Fuji Electric.

Market Insights

- The General Purpose DC Contactor Market size was valued at USD 229.06 million in 2024 and is anticipated to reach USD 380.95 million by 2032, at a CAGR of 6.6%.

- Rising demand from electric vehicles, renewable energy systems, and industrial automation drives steady growth.

- Key trends include IoT-enabled monitoring, predictive maintenance, and the adoption of compact lightweight designs.

- Competition remains strong with global and regional players focusing on innovation, pricing, and customization.

- High cost pressures, raw material volatility, and strict regulatory compliance act as restraints.

- Asia Pacific holds the largest share with EV and renewable expansion, followed by North America and Europe, while Latin America and Middle East & Africa show gradual progress.

- Leading players such as ABB, Eaton Corporation, Mitsubishi Electric Corporation, LS ELECTRIC, and Fuji Electric drive market advancements through product innovation and strategic partnerships.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Demand for Electric Vehicles and Sustainable Mobility Solutions

The General Purpose DC Contactor Market gains momentum from the rapid shift toward electric vehicles. Manufacturers integrate advanced contactors to ensure safe switching of high-voltage circuits in battery systems. Growth in EV adoption drives higher demand for efficient, compact, and durable DC contactors. It supports energy transfer between charging infrastructure and vehicles, ensuring reliability. Government incentives for e-mobility further strengthen this demand, making contactors central to vehicle safety and performance. The trend aligns with global decarbonization efforts, supporting consistent market expansion.

- For instance, LS ELECTRIC developed the GPR-H500-A high-voltage DC relay, which is rated for 1,500VDC and 500 Amps. These types of components, designed for switching high-voltage DC power, are suitable for applications such as electric bus battery systems and Energy Storage Systems (ESS).

Expanding Renewable Energy Installations and Energy Storage Systems

Wider deployment of renewable energy projects fuels steady demand for DC contactors. Solar and wind farms use them for isolating and protecting circuits under varying load conditions. It ensures system stability and smooth integration into grids. Energy storage systems, particularly lithium-ion based, also rely on contactors for safety and performance. Rising investments in grid modernization expand opportunities for advanced solutions. This adoption supports both utility-scale and distributed renewable installations, boosting the General Purpose DC Contactor Market significantly.

- For instance, Mitsubishi Electric delivered a high-capacity energy-storage system (50MW output and 300MWh rated capacity) to Kyushu Electric Power Co. for a pilot project in Japan.The project used an energy management system to help balance supply and demand when using renewable energy sources.

Industrial Automation and Electrification of Heavy Machinery

Growth in industrial automation creates sustained demand for reliable switching solutions. The General Purpose DC Contactor Market benefits from automation in sectors such as manufacturing, logistics, and mining. It enables safe circuit control under heavy loads, supporting operational efficiency. Electrification of construction and mining equipment further raises usage across rugged environments. Contactors ensure reliable operation of motors, drives, and auxiliary systems. Increasing adoption of robotics and automated machinery expands market penetration across diverse industries.

Advancements in Power Electronics and Smart Grid Technologies

Continuous advancements in power electronics drive innovation in contactor design and performance. Smart grids require robust switching devices to handle bidirectional energy flows. It enables integration of distributed generation, storage, and demand-side management. Digital control, IoT connectivity, and predictive monitoring enhance the role of modern DC contactors. Growing focus on safety standards and regulatory compliance accelerates technology upgrades. These factors reinforce the relevance of the General Purpose DC Contactor Market in modern energy ecosystems.

Market Trends

Growing Integration of DC Contactors in Electric Mobility Platforms

The General Purpose DC Contactor Market reflects a strong trend toward integration in electric mobility platforms. EV manufacturers require high-performance contactors to manage battery safety and power transfer. It supports fast-charging infrastructure, where reliability and efficiency are critical. Lightweight and compact designs enable easier placement in limited spaces within vehicles. Adoption in electric buses, trucks, and two-wheelers extends market opportunities. This trend aligns with global mobility transformation and rising investments in sustainable transport solutions.

- For instance, LOVATO Electric offers its BFD80T4E230 four-pole contactor with AC/DC coil for 100-250V control voltage, with thermal current rating Ith of 160A, and capable of handling DC1 current of 80A at 1000V when using four poles in series.

Rising Role of Contactors in Renewable Energy and Storage Projects

Renewable energy projects increasingly depend on DC contactors for safe operation. Solar farms, wind projects, and hybrid systems integrate them to protect circuits and manage load changes. It ensures energy transfer efficiency and protects equipment from faults. Energy storage units, especially lithium-ion systems, rely heavily on advanced DC contactors. Expansion of residential and commercial storage boosts this trend further. The General Purpose DC Contactor Market benefits directly from ongoing investments in decentralized and utility-scale clean energy systems.

- For instance, GEYA offers its GDCR7 series of high-voltage DC contactor relays, which includes models like the GDCR7-250 capable of handling operational currents of up to 250A. GEYA also offers the GYHC series of modular contactors. While the GYHC-25 model has a 25A rating for its main circuit, it’s designed for lower-voltage household applications (up to 250V for DC) rather than being a high-voltage DC contactor.

Increasing Adoption of Digital and Smart Contactor Technologies

The market shows a clear shift toward digitalized contactors with advanced features. Smart designs integrate IoT connectivity, predictive monitoring, and automated control functions. It improves safety, reduces downtime, and enhances lifecycle management. Manufacturers develop solutions with diagnostic capabilities to support modern industrial operations. Such trends align with Industry 4.0 initiatives and intelligent grid requirements. The General Purpose DC Contactor Market evolves with these smart technologies, creating value for both industrial and energy applications.

Strong Demand Across Industrial and Heavy-Duty Applications

Industrial automation continues to shape demand for general purpose DC contactors. Manufacturing plants and logistics operations use them for safe load management and circuit protection. It supports efficient performance of motors, conveyors, and automated machinery. Heavy-duty applications in mining, construction, and marine sectors adopt ruggedized versions to withstand harsh environments. Robotics and advanced automation systems further expand deployment. The General Purpose DC Contactor Market grows steadily through consistent use in diverse industrial and heavy machinery applications.

Market Challenges Analysis

High Cost Pressures and Performance Limitations in Advanced Applications

The General Purpose DC Contactor Market faces significant challenges from cost pressures and technical limitations. Advanced applications in EVs and renewable systems demand compact, lightweight, and high-capacity contactors, raising production costs. It restricts adoption among small manufacturers and price-sensitive regions. Performance limitations such as overheating, contact wear, and reduced durability under heavy loads create operational risks. High maintenance requirements and potential replacement costs further hinder customer acceptance. Balancing affordability with performance remains a major challenge for market players.

Regulatory Compliance, Safety Standards, and Competitive Pressures

Strict regulatory standards and safety certifications present another challenge for manufacturers. It requires continuous investment in testing, material innovation, and product redesign. Compliance delays often slow down product launches, limiting market growth potential. Competitive pressures from regional players offering low-cost alternatives impact margins for established companies. Rising raw material costs and supply chain disruptions further affect stability. The General Purpose DC Contactor Market must address these barriers to maintain reliability, quality, and long-term adoption across industries.

Market Opportunities

Expansion in Electric Mobility, Renewable Energy, and Storage Ecosystems

The General Purpose DC Contactor Market presents strong opportunities through the rapid growth of electric mobility and renewable energy. EV manufacturers require reliable contactors to manage battery packs and charging systems. It also supports grid-tied solar and wind projects where safe circuit control is essential. Rising demand for energy storage systems in residential, commercial, and utility applications further expands potential adoption. Governments worldwide promote clean energy and electrification, creating a favorable environment for growth. These factors open new opportunities for manufacturers to deliver high-performance solutions across diverse sectors.

Advancements in Smart Technologies and Industrial Automation

Ongoing advancements in smart technologies create further prospects for market expansion. The General Purpose DC Contactor Market benefits from IoT-enabled monitoring, predictive maintenance, and advanced safety features. It strengthens adoption in industrial automation, robotics, and heavy-duty machinery. Smart grid integration and digitalized power systems increase the need for intelligent switching solutions. Companies investing in ruggedized and compact designs can address both traditional and emerging industries. This focus on innovation and adaptation drives long-term opportunities across global markets.

Market Segmentation Analysis:

By Voltage

The General Purpose DC Contactor Market divides into high voltage (>60V) and low voltage (≤60V) segments. High-voltage contactors dominate demand in applications requiring stable switching under heavy loads. It is critical for EV powertrains, renewable energy integration, and large-scale industrial machinery. Low-voltage contactors hold steady adoption across HVAC, consumer equipment, and small-scale battery systems. Their cost-effectiveness and flexibility make them suitable for distributed applications. Growing investments in electrification expand opportunities across both voltage categories.

- For instance, a model in their low-voltage DILM series, such as the DILM50, is rated for DC-1 operation and can handle 50A at 110V DC, while for high-voltage DC applications, their AVD series contactors can manage significantly higher voltages and currents.

By Application

Key applications include battery management systems, inverters, HVAC, and charging systems. Battery management systems lead demand with rising EV adoption and storage deployment. It ensures safe isolation and reliable energy transfer. Inverters use contactors to regulate power conversion in renewable energy and industrial settings. HVAC applications integrate contactors for efficiency and circuit protection. Charging systems represent a fast-growing segment, driven by expansion of fast-charging infrastructure worldwide. Each application area strengthens the market’s foundation across energy and mobility ecosystems.

- For instance, ABB offers its GF contactor range to support inverters in solar PV systems. The GF 875 model, which can carry a high thermal current of 875, is specifically rated for 210A at 1500V DC for DC-PV3 utilization. In contrast, for HVAC systems.

By End User

End users span electric vehicles, aerospace and defense, industrial machinery, and renewable energy. The General Purpose DC Contactor Market records maximum growth in electric vehicles, where safety and reliability are critical. Aerospace and defense applications adopt advanced contactors to ensure performance under extreme conditions. It supports avionics, satellites, and defense-grade systems with stringent reliability requirements. Industrial machinery leverages contactors for motor control, automation, and heavy-duty operations. Renewable energy remains a vital end-user sector, requiring contactors for safe grid integration and storage deployment. These end-user segments highlight the versatility and wide adoption potential of DC contactors.

Segments:

Based on Voltage:

- High voltage (>60V)

- Low voltage (≤60V)

Based on Application:

- Battery management systems

- Inverters

Based on End-User:

- Electric Vehicles

- Aerospace & Defense

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America accounts for 32% share of the General Purpose DC Contactor Market, driven by strong adoption across electric vehicles, renewable energy, and industrial automation. The region benefits from advanced automotive manufacturing hubs in the United States, where EV adoption continues to expand under federal incentives and state-level regulations. It supports demand for high-voltage DC contactors in battery management and charging infrastructure. Canada plays an important role in renewable energy integration, particularly in wind and hydro-based projects where safety and reliability are crucial. Mexico strengthens regional demand through industrial machinery and automotive component manufacturing, adding to growth momentum. The region maintains a leadership position due to continuous innovation, large-scale R&D, and strong supplier presence that ensures robust market performance.

Europe

Europe holds 27% share of the General Purpose DC Contactor Market, supported by stringent regulations on emissions and growing adoption of sustainable energy. Germany leads the regional market with a strong automotive sector and rapid EV transition, requiring high-performance contactors for both passenger and commercial vehicles. France and the UK drive adoption through renewable energy and smart grid projects that depend on reliable switching components. It also gains momentum in industrial automation, where advanced contactor solutions improve efficiency and safety. Aerospace and defense applications remain significant, with demand for durable and compact contactors in avionics and military systems. The presence of global manufacturers, coupled with government-backed electrification targets, positions Europe as a dynamic contributor to overall market expansion.

Asia Pacific

Asia Pacific captures the largest share at 34%, reflecting its role as the leading hub for electric vehicle production, renewable energy deployment, and industrial manufacturing. China dominates demand with large-scale EV adoption, supported by nationwide infrastructure expansion and government subsidies. Japan and South Korea contribute through advanced technology integration, with major players focusing on compact and high-efficiency contactors for EVs and industrial systems. India records rising adoption in renewable energy, particularly solar projects, where safe and cost-effective contactors play a critical role. It also benefits from industrial automation growth across manufacturing hubs in Southeast Asia. The region’s high production capacity, competitive costs, and rising domestic demand make Asia Pacific a critical driver of long-term market leadership.

Latin America

Latin America represents 4% share of the General Purpose DC Contactor Market, showing gradual but steady progress. Brazil drives demand through renewable energy projects, particularly in wind and solar, where DC contactors safeguard grid stability. Mexico’s automotive sector strengthens market presence, supported by integration of EV components and charging systems. It records further adoption in industrial machinery and logistics operations that require reliable switching solutions. Regional growth faces challenges from limited infrastructure and investment delays, but government-backed renewable projects create new opportunities. The presence of international suppliers entering local markets enhances technology adoption and long-term potential across Latin America.

Middle East & Africa

The Middle East & Africa account for 3% share, supported by emerging applications in renewable energy and industrial development. Gulf countries expand solar and hydrogen projects, requiring reliable DC contactors for system safety and efficiency. South Africa leads regional adoption through industrial machinery and renewable projects, while North Africa records demand growth in grid modernization. It also benefits from rising focus on smart infrastructure and energy diversification across key economies. Market penetration remains limited due to infrastructure gaps and higher costs of advanced systems. However, ongoing investments in energy diversification and industrial automation provide steady opportunities, keeping the region relevant within the global market landscape.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Competitive Analysis

The competitive landscape players such as ABB, Carlo Gavazzi, Eaton Corporation, Fuji Electric, GEYA Electrical Equipment Supply, K.A. Schmersal GmbH & Co. KG, LOVATO Electric S.p.A., LS ELECTRIC, L&T, and Mitsubishi Electric Corporation. The competitive landscape of the General Purpose DC Contactor Market is characterized by continuous innovation, strong regional presence, and growing emphasis on advanced technologies. Companies focus on developing high-performance solutions that address demand from electric vehicles, renewable energy systems, and industrial automation. It reflects a clear trend toward compact, efficient, and durable designs that can withstand high-voltage operations and harsh environments. Manufacturers invest heavily in digital integration, IoT-enabled monitoring, and predictive maintenance to improve safety and lifecycle management. Pricing strategies and customization options play a crucial role in capturing diverse end-user segments. Strategic collaborations, regional expansions, and technological advancements remain central to strengthening market positions and sustaining long-term growth.

Recent Developments

- In March 2025, Siemens strengthened its competitiveness in both its automation and electric vehicle (EV) charging businesses. The company will focus on growth markets and improving customer orientation in automation, while concentrating on fast-charging infrastructure for depots, fleets, and en-route charging in the EV charging sector.

- In January 2025, Schaltbau introduced an upgraded Eddicy C303 contactor with capabilities of managing a continuous current of 500 amps. With this upgrade, Schaltbau achieves another milestone in improving the reliability and efficacy of its DC solutions.

- In June 2024, Sensata Technologies expanded its low-power products with the SGX Series contactors SGX150, SGX250, SGX400. The SGX Series with the new models were designed to provide unmatched dependability and compact efficiency. The new SGX Series offers optimal performance for residential energy storage systems, DC fast-charging infrastructure, industrial electric forklifts, and Automated Guided Vehicles (AGVs).

- In June 2024, Eaton Corporation unveiled a comprehensive suite of safety-focused electrified vehicle (EV) technologies at The Battery Show Europe, showcasing high-voltage EV protection devices, including advanced contactors. These contactors provide exceptionally fast, safe, and reliable protection for high-power battery and inverter systems.

Report Coverage

The research report offers an in-depth analysis based on Voltage, Application, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand with rising adoption of electric vehicles worldwide.

- Demand will grow in renewable energy projects requiring reliable switching solutions.

- Smart grid integration will create opportunities for advanced digitalized contactors.

- Industrial automation will continue to drive steady consumption across sectors.

- Compact and lightweight designs will gain preference in mobility applications.

- Safety compliance and regulatory standards will shape product development priorities.

- IoT-enabled monitoring and predictive maintenance features will increase adoption.

- Emerging economies will contribute significantly through infrastructure and energy investments.

- High-voltage applications will dominate demand in EVs and energy storage systems.

- Continuous innovation will strengthen competition and support long-term market growth.