| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Hydrocephalus Shunt Market Size 2024 |

USD 497.73 Million |

| Hydrocephalus Shunt Market, CAGR |

3.14% |

| Hydrocephalus Shunt Market Size 2032 |

USD 648.94 Million |

Market Overview

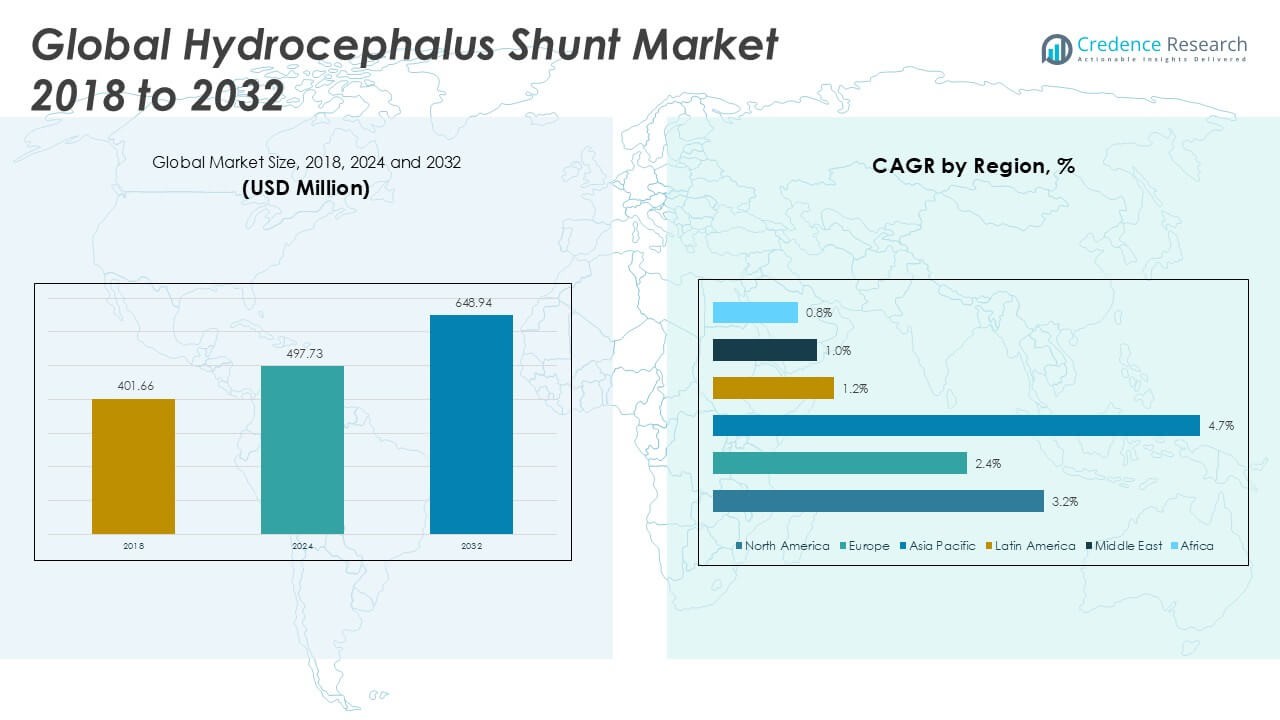

The Hydrocephalus Shunt Market size was valued at USD 401.66 million in 2018, increased to USD 497.73 million in 2024, and is anticipated to reach USD 648.94 million by 2032, at a CAGR of 3.14% during the forecast period.

The Hydrocephalus Shunt Market is driven by the rising incidence of hydrocephalus across all age groups, particularly among infants and the elderly. Increasing awareness, early diagnosis, and improved access to neurosurgical care are contributing to higher treatment rates. Technological advancements, including programmable shunt valves and antimicrobial catheters, are enhancing treatment efficacy and reducing complications, which supports market adoption. Moreover, the growing healthcare expenditure and government initiatives to improve neurological care infrastructure are boosting demand globally. Trends indicate a shift toward minimally invasive procedures and smart shunt systems capable of remote monitoring and pressure adjustments, aligning with broader digital health innovations. Market players are increasingly focused on R&D collaborations and strategic partnerships to introduce advanced, patient-specific solutions. Although shunt-related complications remain a clinical challenge, ongoing innovations aimed at reducing infection rates and revision surgeries are shaping the future of hydrocephalus management, sustaining market growth over the forecast period.

The Hydrocephalus Shunt Market exhibits strong regional presence across North America, Europe, and Asia Pacific, with each region showing unique growth drivers. North America leads due to well-established healthcare systems, advanced neurosurgical infrastructure, and rapid adoption of programmable shunt systems. Europe maintains stable demand supported by high diagnosis rates and government-backed neurological care in countries like Germany, France, and the UK. Asia Pacific is emerging as a high-growth region driven by rising pediatric cases, expanding surgical access, and increasing healthcare investments in China, India, and Japan. Latin America, the Middle East, and Africa show slower growth but present long-term opportunities through public health initiatives and cost-sensitive product innovations. Key players operating in the Hydrocephalus Shunt Market include Medtronic, which offers a comprehensive neurosurgical portfolio; Integra LifeSciences, known for shunt systems and catheters; CHRISTOPH MIETHKE GMBH & CO. KG, focused on advanced valve technologies; and Sophysa, specializing in programmable valves and pediatric shunt systems.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Hydrocephalus Shunt Market was valued at USD 497.73 million in 2024 and is projected to reach USD 648.94 million by 2032, registering a CAGR of 3.14% during the forecast period.

- Increasing prevalence of hydrocephalus, especially among infants and the elderly, continues to drive demand for surgical interventions supported by advanced shunt systems.

- Adoption of programmable valves and smart shunt systems with remote monitoring features is reshaping treatment approaches and improving patient outcomes.

- Major players such as Medtronic, Integra LifeSciences, and Sophysa are investing in R&D, expanding product portfolios, and forming strategic partnerships to maintain market presence.

- High revision rates due to shunt malfunctions, infections, and limited long-term reliability present challenges to consistent clinical outcomes and patient satisfaction.

- North America leads the market with a 39.3% share, followed by Europe at 29.4% and Asia Pacific at 24.5%, with Asia Pacific showing the fastest CAGR of 4.7%.

- Access limitations in regions such as Latin America, the Middle East, and Africa hinder market expansion, but infrastructure development and cost-effective solutions offer future growth potential.

Market Drivers

Rising Prevalence of Hydrocephalus Across Pediatric and Geriatric Populations

The Hydrocephalus Shunt Market benefits significantly from the growing prevalence of hydrocephalus, especially in infants and elderly individuals. Congenital hydrocephalus cases in newborns and age-related cerebrospinal fluid (CSF) circulation disorders among older adults are creating consistent clinical demand. Early diagnosis through advanced imaging and wider screening programs in neonatal care units have increased case detection. It drives the need for timely surgical intervention, which relies on shunt systems for long-term cerebrospinal fluid drainage. Emerging economies are seeing a steady rise in hydrocephalus cases due to expanding birth cohorts and longer life expectancies. The growing patient base ensures steady product utilization and procedure volumes across hospitals and specialty clinics.

- For instance, Medtronic reported over 70,000 programmable valve implants globally across both pediatric and adult populations as of its most recent device performance summary.

Continuous Technological Advancements in Shunt Design and Functionality

The market gains traction from ongoing advancements in shunt technology, such as programmable valves and anti-siphon devices. These innovations help reduce complications like overdrainage, infection, and shunt failure. Manufacturers focus on producing more durable, biocompatible materials to extend device lifespan and reduce revision surgeries. Smart shunt systems equipped with telemetry and pressure adjustment features are gaining adoption in developed markets. It enables clinicians to monitor intracranial pressure without repeated surgical interventions. The push for personalized medical devices further supports product differentiation and premium pricing.

- For instance, CHRISTOPH MIETHKE GMBH & CO. KG has developed over 15 variants of programmable valves, including the M.blue® valve, which features integrated telemetry and has been implanted in more than 30,000 patients worldwide.

Growing Healthcare Infrastructure and Surgical Capacity in Developing Regions

Expanding neurosurgical infrastructure across developing countries is accelerating access to hydrocephalus treatment. Increased public and private investments in hospital equipment and training are closing care gaps, especially in Southeast Asia, Latin America, and parts of Africa. Governments and NGOs promote pediatric neurological health, encouraging early diagnosis and timely shunt placement. Rising insurance coverage and universal healthcare initiatives are easing the cost burden for families. It supports volume growth in both urban and semi-urban healthcare centers. The Hydrocephalus Shunt Market is leveraging these structural improvements to expand market penetration beyond traditional high-income regions.

Rising Focus on Reducing Complications and Improving Long-Term Outcomes

Shunt-related infections, blockages, and failures remain critical concerns for clinicians and patients. The market responds by investing in antimicrobial coatings and low-profile valve systems to reduce risks during and after implantation. Hospitals adopt stringent surgical protocols and post-operative monitoring to manage complications proactively. Research institutions collaborate with medical device companies to develop next-generation materials and designs. It improves patient outcomes and enhances procedural confidence among surgeons. The Hydrocephalus Shunt Market is increasingly shaped by clinical outcomes and safety benchmarks that influence purchasing decisions and reimbursement policies.

Market Trends

Integration of Smart and Programmable Shunt Systems into Standard Treatment

The Hydrocephalus Shunt Market is witnessing a growing preference for programmable and smart shunt systems that allow non-invasive pressure adjustments. These devices help clinicians tailor cerebrospinal fluid drainage to patient-specific needs without surgical revisions. Telemetry features and remote monitoring capabilities are being incorporated to track intracranial pressure and device performance in real time. It enhances clinical decision-making and reduces hospital visits. Programmable valves are gaining approval across multiple geographies, reflecting regulatory support for next-generation solutions. Their adoption is strongest in developed markets but is gradually extending to emerging regions with rising neurosurgical capacity.

- For instance, Sophysa’s Polaris® programmable valve, used in over 40,000 procedures globally, enables external pressure readjustments without magnetic interference risks and is CE-marked across Europe and select APAC markets.

Shifting Preference Toward Minimally Invasive Surgical Techniques

Surgeons and healthcare facilities are moving toward minimally invasive procedures for shunt placement to reduce trauma, infection risk, and recovery time. Advances in imaging and navigation systems support precision in shunt positioning. This shift aligns with the broader healthcare trend of optimizing patient outcomes through less invasive techniques. It increases procedure volumes by lowering the threshold for surgical intervention. The Hydrocephalus Shunt Market benefits from this trend by aligning product innovation with evolving clinical practice standards. Device manufacturers are responding by designing low-profile and flexible shunt systems suited for smaller incisions and quicker deployment.

- For instance, Integra LifeSciences offers the NPH Low Profile Valve System, which has shown a 23% reduction in incision length and improved procedural efficiency in over 12,000 recorded uses since its introduction.

Focus on Pediatric Care and Specialized Shunt Designs

Pediatric patients represent a significant portion of the hydrocephalus population, prompting increased focus on age-specific shunt solutions. The market is seeing a rise in demand for shunts designed for neonatal and infant cranial anatomies. These products often include anti-siphon features and flow control mechanisms tailored for pediatric physiology. It supports long-term treatment success and reduces the need for frequent revisions. The Hydrocephalus Shunt Market is evolving to support developmental and growth considerations through modular and upgradeable systems. Pediatric neurosurgical centers continue to influence design and procurement trends globally.

Increased Emphasis on Post-Surgical Monitoring and Long-Term Care

Long-term care and post-surgical monitoring are becoming central to treatment protocols. Hospitals and neurosurgeons are adopting advanced diagnostic tools and monitoring equipment to detect early signs of shunt malfunction or infection. Home-based care solutions and wearable monitoring systems are in development to support outpatient management. It improves patient outcomes and reduces the economic burden of emergency readmissions. The Hydrocephalus Shunt Market is responding with integrated solutions that combine hardware, software, and data analytics. This trend supports a more comprehensive and value-based approach to hydrocephalus care.

Market Challenges Analysis

High Revision Rates and Risk of Post-Surgical Complications Remain Persistent Issues

The Hydrocephalus Shunt Market faces a major challenge from the high incidence of shunt malfunctions, infections, and blockages, often requiring multiple surgical revisions. These complications lead to increased healthcare costs, extended hospital stays, and patient discomfort. It raises concerns about long-term reliability and safety, especially in pediatric and elderly patients. Clinical outcomes heavily depend on surgical expertise, postoperative care, and timely diagnosis of device failure. Despite innovations in shunt design, no device offers a guaranteed long-term solution, creating uncertainty among healthcare providers. The ongoing need for improvements in material durability and infection control technologies continues to drive clinical demand but also exposes gaps in current product performance.

Limited Access to Neurosurgical Care and Economic Constraints in Developing Regions

Access to timely diagnosis and treatment remains limited in low- and middle-income countries due to inadequate neurosurgical infrastructure and workforce shortages. The Hydrocephalus Shunt Market struggles to penetrate these regions fully, despite a growing disease burden. High device costs and the lack of insurance coverage often make shunt implantation unaffordable for many patients. It restricts equitable access and delays intervention, worsening clinical outcomes. Regulatory and logistical hurdles in importing advanced medical devices also slow down availability. Without sustained investment in healthcare systems and local manufacturing capacity, market expansion into these underserved areas remains a critical challenge.

Market Opportunities

Advancements in Smart Shunt Technology and Remote Monitoring Solutions

The development of smart hydrocephalus shunt systems with pressure sensors, telemetry, and wireless monitoring opens new avenues for market growth. These innovations allow real-time tracking of cerebrospinal fluid dynamics and help detect early signs of shunt failure. It reduces the need for emergency interventions and enhances post-operative care. Integration with digital health platforms and AI-driven diagnostics supports personalized treatment planning and long-term management. The Hydrocephalus Shunt Market can leverage this trend to offer value-based solutions aligned with modern healthcare delivery models. Collaborations between medtech companies and software developers present strong potential for commercializing intelligent shunt systems.

Expansion Opportunities in Emerging Economies Through Infrastructure Development

Healthcare infrastructure upgrades in emerging regions present a significant opportunity to expand the reach of hydrocephalus treatment. Governments and global health organizations are investing in neurosurgery training, diagnostic tools, and surgical equipment to improve care access. It creates favorable conditions for introducing cost-effective and scalable shunt solutions. The Hydrocephalus Shunt Market can grow by forming partnerships with public health institutions and local distributors. Tailoring product lines for affordability and low-maintenance use supports adoption in rural and resource-constrained settings. Long-term market potential lies in addressing unmet needs through inclusive and context-sensitive product strategies.

Market Segmentation Analysis:

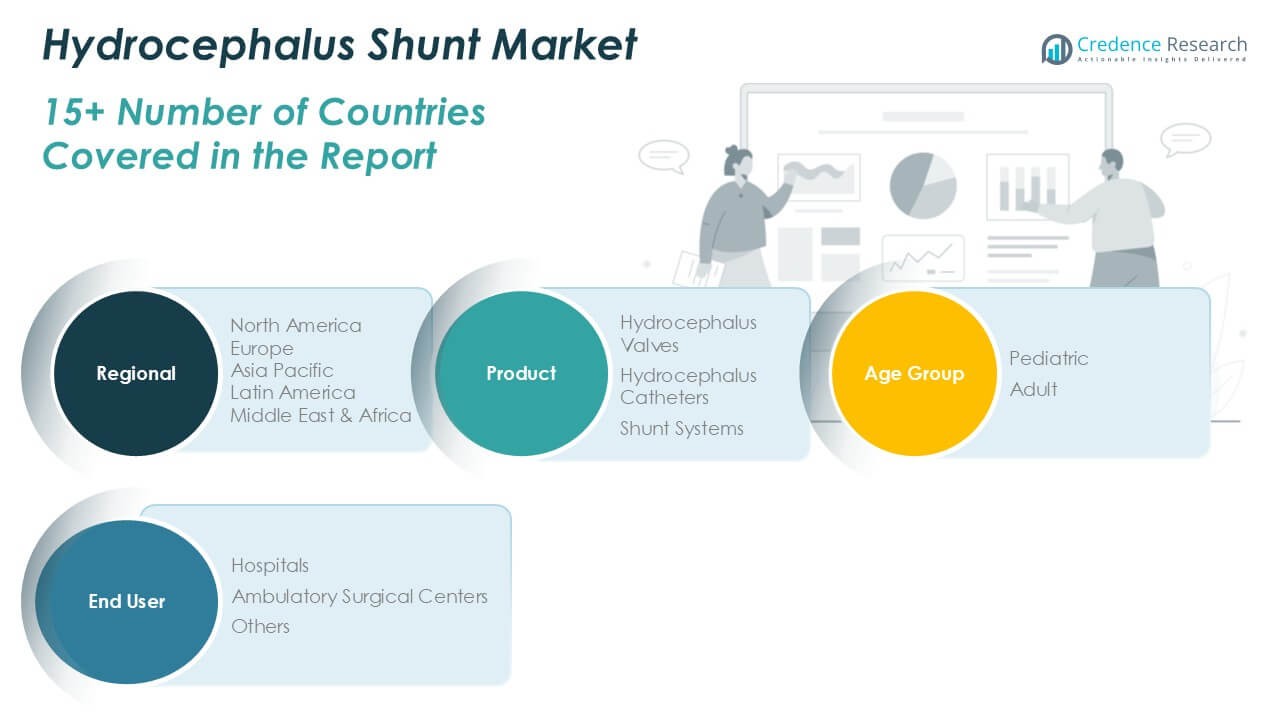

By Product:

The Hydrocephalus Shunt Market is segmented by product into hydrocephalus valves, hydrocephalus catheters, and shunt systems. Shunt systems hold the largest share due to their critical role in maintaining cerebrospinal fluid drainage and pressure regulation. These systems are widely adopted across age groups for managing both congenital and acquired hydrocephalus. Hydrocephalus valves contribute significantly to market revenue, driven by demand for programmable and pressure-adjustable models that improve clinical outcomes. Hydrocephalus catheters, though standard components, face ongoing innovation in materials to reduce infection and blockage risks. It continues to see product upgrades aligned with minimally invasive and long-term use requirements.

- For instance, Spiegelberg GmbH & Co. KG has deployed more than 25,000 antibacterial catheters globally since launching its silver-ion embedded catheter line, with post-market surveillance indicating a 40% reduction in infection incidence.

By Age Group:

The Hydrocephalus Shunt Market includes pediatric and adult segments. Pediatric patients account for a higher volume of shunt procedures due to the early onset of congenital hydrocephalus. This segment drives demand for age-specific shunt systems designed for growing cranial structures and sensitive physiology. Pediatric care also sees higher revision rates, contributing to recurring device use. The adult segment is expanding due to an aging population and rising cases of normal pressure hydrocephalus. It benefits from improved diagnostic capabilities and increasing awareness among clinicians and caregivers. Both segments demand durable, low-complication devices tailored to patient-specific needs.

- For instance, Bicakcilar has reported more than 18,000 pediatric shunt system installations over the last five years, with dedicated models optimized for variable skull growth and pressure fluctuation resistance.

By End-User:

The market is segmented by end user into hospitals, ambulatory surgical centers, and others. Hospitals dominate the Hydrocephalus Shunt Market due to their advanced neurosurgical infrastructure and capacity to handle complex procedures. They manage the majority of pediatric and adult shunt implantations, revisions, and emergency care. Ambulatory surgical centers are gaining traction, particularly in urban areas with access to specialized neurosurgeons and support technology. These centers offer cost-effective and time-efficient treatment for selected cases. The “others” segment includes specialty clinics and rehabilitation centers, which play a growing role in post-operative management and long-term patient follow-up. It supports ongoing demand through continued care and monitoring solutions.

Segments:

Based on Product:

- Hydrocephalus Valves

- Hydrocephalus Catheters

- Shunt Systems

Based on Age Group:

Based on End-User:

- Hospitals

- Ambulatory Surgical Centers

- Others

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America Hydrocephalus Shunt Market

North America Hydrocephalus Shunt Market grew from USD 159.64 million in 2018 to USD 195.57 million in 2024 and is projected to reach USD 255.76 million by 2032, reflecting a compound annual growth rate (CAGR) of 3.2%. North America is holding a 39% market share. The region benefits from strong healthcare infrastructure, advanced neurosurgical capabilities, and widespread awareness. The United States leads market demand, supported by high diagnosis rates, insurance coverage, and adoption of programmable shunt systems. Canada also contributes significantly, with increasing investment in pediatric neurological care. Strong presence of key market players and early adoption of smart shunt technologies support continued regional growth.

Europe Hydrocephalus Shunt Market

Europe Hydrocephalus Shunt Market grew from USD 126.66 million in 2018 to USD 151.87 million in 2024 and is projected to reach USD 187.62 million by 2032, reflecting a CAGR of 2.4%. Europe holds a 29% market share. Countries such as Germany, the United Kingdom, and France drive demand through publicly funded healthcare and expanding geriatric populations. It benefits from early-stage interventions and availability of specialized pediatric and adult neurosurgical centers. Rising focus on patient safety and clinical outcomes encourages the use of programmable valves and antimicrobial shunt components. The region’s steady growth reflects mature healthcare systems and gradual technology upgrades.

Asia Pacific Hydrocephalus Shunt Market

Asia Pacific Hydrocephalus Shunt Market grew from USD 80.68 million in 2018 to USD 108.01 million in 2024 and is projected to reach USD 158.76 million by 2032, reflecting a CAGR of 4.7%. Asia Pacific accounts for 25% of the global market. China, India, and Japan are the key contributors, driven by large patient populations and expanding neurosurgical capacity. Government investment in pediatric care and rural healthcare delivery supports early diagnosis and treatment. It benefits from the rising penetration of international medical device manufacturers. Rapid urbanization and awareness campaigns are increasing demand for safe and effective shunt implants.

Latin America Hydrocephalus Shunt Market

Latin America Hydrocephalus Shunt Market grew from USD 15.39 million in 2018 to USD 18.77 million in 2024 and is projected to reach USD 21.00 million by 2032, reflecting a CAGR of 1.2%. Latin America holds a 3% market share. Brazil and Mexico dominate due to improving hospital infrastructure and public health initiatives targeting pediatric neurological conditions. It faces limitations in reimbursement frameworks and surgical capacity in rural areas. Market players are focusing on cost-effective solutions to expand reach. Although growth is moderate, the need for reliable hydrocephalus treatment continues to sustain demand.

Middle East Hydrocephalus Shunt Market

Middle East Hydrocephalus Shunt Market grew from USD 11.47 million in 2018 to USD 13.01 million in 2024 and is projected to reach USD 14.37 million by 2032, reflecting a CAGR of 1.0%. The region accounts for 2% of the global market share. Saudi Arabia and the United Arab Emirates lead the market, supported by national health reforms and infrastructure investment. It benefits from growing partnerships with international device suppliers and training programs for neurosurgeons. Limited access in low-income countries continues to restrict overall market expansion. Despite slower growth, high-income Gulf countries maintain steady procedural volumes.

Africa Hydrocephalus Shunt Market

Africa Hydrocephalus Shunt Market grew from USD 7.83 million in 2018 to USD 10.51 million in 2024 and is projected to reach USD 11.44 million by 2032, reflecting a CAGR of 0.8%. Africa holds a 2% market share. South Africa, Nigeria, and Egypt represent key growth centers, although access to treatment remains a challenge in many regions. It relies heavily on imported devices and NGO-supported medical missions to deliver hydrocephalus care. Resource limitations, delayed diagnosis, and surgical workforce shortages impact treatment rates. Growth remains slow, but international partnerships and healthcare investment may create new opportunities over time.

Key Player Analysis

- Medtronic

- Sophysa

- CHRISTOPH MIETHKE GMBH & CO. KG

- Integra LifeSciences

- Bicakcilar

- Spiegelberg GmbH & Co. KG

- Hpbio

- Aesculap, Inc.

- Surgiwear Ltd

Competitive Analysis

The Hydrocephalus Shunt Market is moderately consolidated, with a few key players dominating the global landscape through innovation, global distribution, and specialized neurosurgical portfolios. Leading companies include Medtronic, Integra LifeSciences, Sophysa, CHRISTOPH MIETHKE GMBH & CO. KG, Spiegelberg GmbH & Co. KG, Bicakcilar, Aesculap Inc., Hpbio, and G. Surgiwear Ltd. These players focus on product innovation, regulatory approvals, and geographic expansion to strengthen their market presence. The market sees strong emphasis on research and development to address complications such as infections and shunt malfunctions. Players differentiate themselves through proprietary technologies, precision-engineered devices, and pediatric-specific product lines. Strategic moves such as global distribution agreements, partnerships with neurosurgical centers, and regulatory approvals in high-growth regions contribute to competitive positioning. Innovation in smart shunt systems with telemetry capabilities is emerging as a key area of focus, targeting improved post-surgical care and remote monitoring. Cost-effective solutions tailored for developing markets are also gaining attention, where affordability and access are primary concerns. The competitive environment continues to evolve with increased investment in personalized and digital neurosurgical solutions.

Recent Developments

- In July 2024, The Department of Defense (DOD) awarded a USD 5.6 million grant to Senseer Health Inc. to advance innovative technology for monitoring hydrocephalus shunts. The creation of the MultiSense microsensor by Senseer Health Inc. provides optimism for patients and their families, as it promises to reduce complications and enhance overall quality of life.

- In May 2024, CereVasc Inc. obtained approval from the United States Food and Drug Administration (US FDA) to begin its innovative STRIDE pivotal study, which will evaluate the safety and effectiveness of its new eShunt System for treating patients with Normal Pressure Hydrocephalus, compared to the existing standard of care, the ventriculo-peritoneal (VP) shunt.

- In November 2023, for young patients suffering from hydrocephalus-a neurological disorder that results in an accumulation of cerebral fluid in the interior spaces of the brain which often requires repeated hospital stays-surgeons at Intermountain Primary Children’s Hospital successfully placed a novel brain shunt accessory, becoming the first hospital in the U.S. to accomplish the same.

- In October 2023, through its Blueprint MedTech initiative, the NINDS (National Institute of Neurological Disorders and Stroke) of the National Institutes of Health (NIH) awarded Rhaeos, Inc. a USD 1.5 million grant. With this award, the company will continue to develop its FDA-designated breakthrough medical technology, which aims to revolutionize the treatment of hydrocephalus, a brain disorder that affects more than a million people in the U.S.

- In August 2023, registration for the handheld MRI system-based HOPE PMR Pediatric Hydrocephalus study was completed. The observational multi-site study intended to alter the standard procedure to treat pediatric hydrocephalus with the Swoop system, a brain imaging device that can be used in outpatient, inpatient, and emergency pediatric care settings. This can be accessed at the child’s bedside and emits no ionizing radiation. The portable MRI system was developed by Hyperfine, Inc.

Market Concentration & Characteristics

The Hydrocephalus Shunt Market is moderately concentrated, with a limited number of global manufacturers controlling a significant portion of the market. It is characterized by high entry barriers due to stringent regulatory requirements, complex product development processes, and the need for clinical validation. Companies with strong R&D capabilities and established distribution networks maintain a competitive edge through innovation and consistent product quality. The market emphasizes long-term device reliability, patient safety, and customization for pediatric and adult cases. Demand remains steady due to the chronic nature of hydrocephalus and the lack of alternative long-term treatment options. It operates within a clinically driven framework, where purchasing decisions are heavily influenced by surgeon preference, institutional protocols, and reimbursement conditions. The shift toward programmable and smart shunt systems reflects a move toward more value-based, outcome-oriented care. Emerging markets contribute to future potential, but growth remains dependent on healthcare infrastructure development and cost-sensitive product strategies.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Product, Age Group, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will see increased adoption of programmable and smart shunt systems with integrated monitoring features.

- Demand will grow steadily due to the rising incidence of hydrocephalus in both pediatric and elderly populations.

- Research will focus on reducing shunt-related complications such as infection, blockage, and overdrainage.

- Companies will invest in biocompatible and antimicrobial materials to improve long-term device performance.

- Pediatric-specific shunt systems will gain greater attention due to higher procedural volumes and revision needs.

- Digital health integration will enable remote tracking of intracranial pressure and device function.

- Emerging economies will contribute to future expansion as surgical infrastructure and access improve.

- Strategic partnerships between device manufacturers and healthcare institutions will strengthen global reach.

- Minimally invasive implantation techniques will support quicker recovery and reduced hospital stays.

- Innovation will remain key to market competitiveness, with a strong focus on patient-specific solutions.