1. Preface

1.1. Report Description

1.1.1. Purpose of the Report

1.1.2. Target Audience

1.1.3. USP and Key Offerings

1.2. Research Scope

1.3. Market Introduction

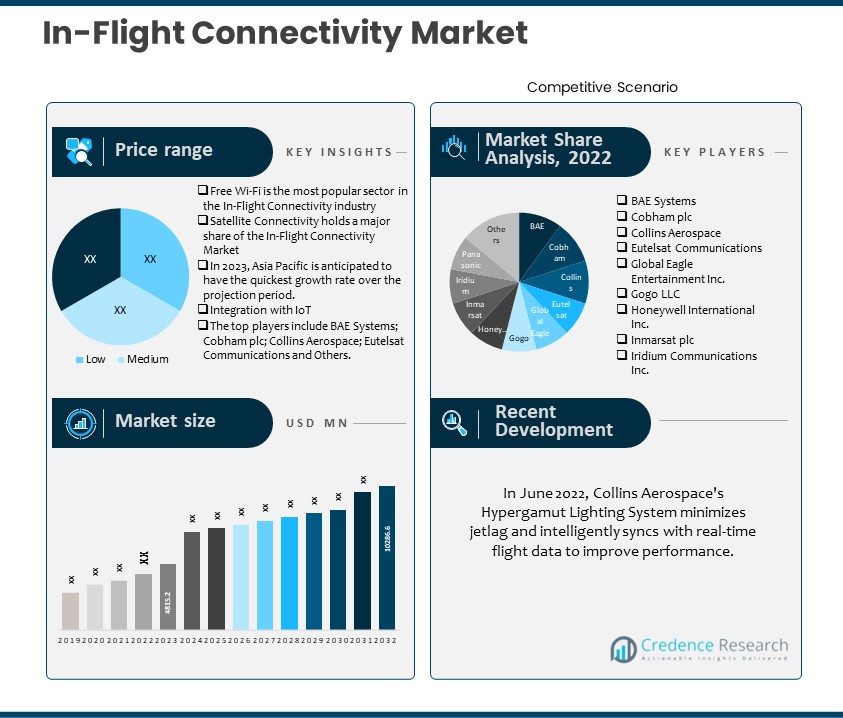

2. Executive Summary

2.1. Market Snapshot: Global In-Flight Connectivity Market

2.1.1. Global In-Flight Connectivity Market, By Technology Type

2.1.2. Global In-Flight Connectivity Market, By Service Model

2.1.3. Global In-Flight Connectivity Market, By Connectivity Speed and Quality

2.1.4. Global In-Flight Connectivity Market, By Aircraft Type

2.1.5. Global In-Flight Connectivity Market, By Region

2.2. Insights from Primary Respondents

3. Market Dynamics & Factors Analysis

3.1. Introduction

3.1.1. Global In-Flight Connectivity Market Value, 2019-2032, (US$ Mn)

3.1.2. Y-o-Y Growth Trend Analysis

3.2. Market Dynamics

3.2.1. In-Flight Connectivity Market Drivers

3.2.2. In-Flight Connectivity Market Restraints

3.2.3. In-Flight Connectivity Market Opportunities

3.2.4. Major In-Flight Connectivity Industry Challenges

3.3. Growth and Development Patterns

3.4. Investment Feasibility Analysis

3.5. Market Opportunity Analysis

3.5.1. Technology Type

3.5.2. Service Model

3.5.3. Connectivity Speed and Quality

3.5.4. Aircraft Type

3.5.5. Geography

4. Market Competitive Landscape Analysis

4.1. Company Market Share Analysis, 2023

4.1.1. Global In-Flight Connectivity Market: Company Market Share, Value 2023

4.1.2. Global In-Flight Connectivity Market: Top 6 Company Market Share, Value 2023

4.1.3. Global In-Flight Connectivity Market: Top 3 Company Market Share, Value 2023

4.2. Global In-Flight Connectivity Market: Company Revenue Share Analysis, 2023

4.3. Company Assessment Metrics, 2023

4.3.1. Stars

4.3.2. Emerging Leaders

4.3.3. Pervasive Players

4.3.4. Participants

4.4. Startups/ SMEs Assessment Metrics, 2023

4.4.1. Progressive Companies

4.4.2. Responsive Companies

4.4.3. Dynamic Companies

4.4.4. Starting Blocks

4.5. Strategic Development

4.5.1. Acquisition and Mergers

4.5.2. New Technology Type Launch

4.5.3. Regional Expansion

4.5.4. Partnerships

4.6. Key Player Technology Type Matrix

4.7. Potential for New Players in the Global In-Flight Connectivity Market

5. Premium Insights

5.1. STAR (Situation, Task, Action, Results) Analysis

5.2. Porter’s Five Forces Analysis

5.2.1. Threat of New Entrants

5.2.2. Bargaining Power of Buyers/Consumers

5.2.3. Bargaining Power of Suppliers

5.2.4. Threat of Substitute Types

5.2.5. Intensity of Competitive Rivalry

5.3. PESTEL Analysis

5.3.1. Political Factors

5.3.2. Economic Factors

5.3.3. Social Factors

5.3.4. Technological Factors

5.3.5. Environmental Factors

5.3.6. Legal Factors

5.4. Key Market Trends

5.4.1. Demand Side Trends

5.4.2. Supply Side Trends

5.5. Value Chain Analysis

5.6. Aircraft Type Analysis

5.6.1. Standard Connectivity in the global market

5.6.2. Patent Analysis

5.6.3. Emerging technologies and their potential disruption to the market

5.7. Consumer Behaviour Analysis

5.7.1. Consumer Preferences and Expectations

5.7.2. Factors Influencing Consumer Buying Decisions

5.7.2.1. North America

5.7.2.2. Europe

5.7.2.3. Asia Pacific

5.7.2.4. Latin America

5.7.2.5. Middle East and Africa

5.7.3. Consumer Pain Points

5.8. Analysis and Recommendations

5.9. Adjacent Market Analysis

6. Market Positioning of Key Players, 2023

6.1. Company market share of key players, 2023

6.2. Competitive Benchmarking

6.3. Market Positioning of Key Vendors

6.4. Geographical Presence Analysis

6.5. Major Strategies Adopted by Key Players

6.5.1. Key Strategies Analysis

6.5.2. Mergers and Acquisitions

6.5.3. Partnerships

6.5.4. Technology Type Launch

6.5.5. Geographical Expansion

6.5.6. Paid Wi-Fi

7. Impact Analysis of COVID 19 and Russia – Ukraine War on In-Flight Connectivity Market

7.1. Ukraine-Russia War Impact

7.1.1. Uncertainty and Economic Instability

7.1.2. Supply chain disruptions

7.1.3. Regional market shifts

7.1.4. Shift in government priorities

7.2. COVID-19 Impact Analysis

7.2.1. Supply Chain Disruptions

7.2.2. Demand Fluctuations

7.2.3. Shift in Technology Type Mix

7.2.4. Reduced Industrial Activity

7.2.5. Regional Impact Analysis

7.2.5.1. North America

7.2.5.2. Europe

7.2.5.3. Asia Pacific

7.2.5.4. Latin America

7.2.5.5. Middle East and Africa

8. Global In-Flight Connectivity Market, By Technology Type

8.1. Global In-Flight Connectivity Market Overview, By Technology Type

8.1.1. Global In-Flight Connectivity Market Revenue Share, By Technology Type, 2023 Vs 2032 (in %)

8.2. Satellite Connectivity

8.2.1. Global In-Flight Connectivity Market, By SATELLITE CONNECTIVITY, By Region, 2019-2032 (US$ Mn)

8.2.2. Market Dynamics for SATELLITE CONNECTIVITY

8.2.2.1. Drivers

8.2.2.2. Restraints

8.2.2.3. Opportunities

8.2.2.4. Trends

8.3. Air-to-Ground (ATG) Connectivity

8.3.1. Global In-Flight Connectivity Market, By AIR-TO-GROUND (ATG) CONNECTIVITY, By Region, 2019-2032 (US$ Mn)

8.3.2. Market Dynamics for AIR-TO-GROUND (ATG) CONNECTIVITY

8.3.2.1. Drivers

8.3.2.2. Restraints

8.3.2.3. Opportunities

8.3.2.4. Trends

8.4. Hybrid Connectivity

8.4.1. Global In-Flight Connectivity Market, By Hybrid Connectivity, By Region, 2019-2032 (US$ Mn)

8.4.2. Market Dynamics for Hybrid Connectivity

8.4.2.1. Drivers

8.4.2.2. Restraints

8.4.2.3. Opportunities

8.4.2.4. Trends

9. Global In-Flight Connectivity Market, By Service Model

9.1. Global In-Flight Connectivity Market Overview, By Service Model

9.1.1. Global In-Flight Connectivity Market Revenue Share, By Service Model, 2023 Vs 2032 (in %)

9.2. Free Wi-Fi

9.2.1. Global In-Flight Connectivity Market, By Free Wi-Fi, By Region, 2019-2032 (US$ Mn)

9.2.2. Market Dynamics for Free Wi-Fi

9.2.2.1. Drivers

9.2.2.2. Restraints

9.2.2.3. Opportunities

9.2.2.4. Trends

9.3. Paid Wi-Fi

9.3.1. Global In-Flight Connectivity Market, By Paid Wi-Fi, By Region, 2019-2032 (US$ Mn)

9.3.2. Market Dynamics for Paid Wi-Fi

9.3.2.1. Drivers

9.3.2.2. Restraints

9.3.2.3. Opportunities

9.3.2.4. Trends

9.4. Freemium Model

9.4.1. Global In-Flight Connectivity Market, By Freemium Model, By Region, 2019-2032 (US$ Mn)

9.4.2. Market Dynamics for Freemium Model

9.4.2.1. Drivers

9.4.2.2. Restraints

9.4.2.3. Opportunities

9.4.2.4. Trends

10. Global In-Flight Connectivity Market, By Connectivity Speed and Quality

10.1. Global In-Flight Connectivity Market Overview, By Connectivity Speed and Quality

10.1.1. Global In-Flight Connectivity Market Revenue Share, By Connectivity Speed and Quality, 2023 Vs 2032 (in %)

10.2. High-Speed Connectivity

10.2.1. Global In-Flight Connectivity Market, By High-Speed Connectivity, By Region, 2019-2032 (US$ Mn)

10.2.2. Market Dynamics for High-Speed Connectivity

10.2.2.1. Drivers

10.2.2.2. Restraints

10.2.2.3. Opportunities

10.2.2.4. Trends

10.3. Standard Connectivity

10.3.1. Global In-Flight Connectivity Market, By Standard Connectivity, By Region, 2019-2032 (US$ Mn)

10.3.2. Market Dynamics for Standard Connectivity

10.3.2.1. Drivers

10.3.2.2. Restraints

10.3.2.3. Opportunities

10.3.2.4. Trends

10.4. Low-Bandwidth Connectivity

10.4.1. Global In-Flight Connectivity Market, By Low-Bandwidth Connectivity, By Region, 2019-2032 (US$ Mn)

10.4.2. Market Dynamics for Low-Bandwidth Connectivity

10.4.2.1. Drivers

10.4.2.2. Restraints

10.4.2.3. Opportunities

10.4.2.4. Trends

11. Global In-Flight Connectivity Market, By Aircraft Type

11.1. Global In-Flight Connectivity Market Overview, by Aircraft Type

11.1.1. Global In-Flight Connectivity Market Revenue Share, By Aircraft Type, 2023 Vs 2032 (in %)

11.2. Narrow-Body Aircraft

11.2.1. Global In-Flight Connectivity Market, By Narrow-Body Aircraft, By Region, 2019-2032 (US$ Mn)

11.2.2. Market Dynamics for Narrow-Body Aircraft

11.2.2.1. Drivers

11.2.2.2. Restraints

11.2.2.3. Opportunities

11.2.2.4. Trends

11.3. Wide-Body Aircraft

11.3.1. Global In-Flight Connectivity Market, By Wide-Body Aircraft, By Region, 2019-2032 (US$ Mn)

11.3.2. Market Dynamics for Wide-Body Aircraft

11.3.2.1. Drivers

11.3.2.2. Restraints

11.3.2.3. Opportunities

11.3.2.4. Trends

11.4. Regional Aircraft

11.4.1. Global In-Flight Connectivity Market, By Regional Aircraft, By Region, 2019-2032 (US$ Mn)

11.4.2. Market Dynamics for Regional Aircraft

11.4.2.1. Drivers

11.4.2.2. Restraints

11.4.2.3. Opportunities

11.4.2.4. Trends

12. Global In-Flight Connectivity Market, By Region

12.1. Global In-Flight Connectivity Market Overview, by Region

12.1.1. Global In-Flight Connectivity Market, By Region, 2023 vs 2032 (in%)

12.2. Technology Type

12.2.1. Global In-Flight Connectivity Market, By Technology Type, 2019-2032 (US$ Mn)

12.3. Service Model

12.3.1. Global In-Flight Connectivity Market, By Service Model, 2019-2032 (US$ Mn)

12.4. Connectivity Speed and Quality

12.4.1. Global In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2032 (US$ Mn)

12.5. Aircraft Type

12.5.1. Global In-Flight Connectivity Market, By Aircraft Type, 2019-2032 (US$ Mn)

13. North America In-Flight Connectivity Market Analysis

13.1. Overview

13.1.1. Market Dynamics for North America

13.1.1.1. Drivers

13.1.1.2. Restraints

13.1.1.3. Opportunities

13.1.1.4. Trends

13.2. North America In-Flight Connectivity Market, By Technology Type, 2019-2032(US$ Mn)

13.2.1. Overview

13.2.2. SRC Analysis

13.3. North America In-Flight Connectivity Market, By Service Model, 2019-2032(US$ Mn)

13.3.1. Overview

13.3.2. SRC Analysis

13.4. North America In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2032(US$ Mn)

13.4.1. Overview

13.4.2. SRC Analysis

13.5. North America In-Flight Connectivity Market, By Aircraft Type, 2019-2032(US$ Mn)

13.5.1. Overview

13.5.2. SRC Analysis

13.6. North America In-Flight Connectivity Market, by Country, 2019-2032(US$ Mn)

13.6.1. North America In-Flight Connectivity Market, by Country, 2023 Vs 2032 (in%)

13.6.2. U.S.

13.6.3. Canada

13.6.4. Mexico

14. Europe In-Flight Connectivity Market Analysis

14.1. Overview

14.1.1. Market Dynamics for North America

14.1.1.1. Drivers

14.1.1.2. Restraints

14.1.1.3. Opportunities

14.1.1.4. Trends

14.2. Europe In-Flight Connectivity Market, By Technology Type, 2019-2032(US$ Mn)

14.2.1. Overview

14.2.2. SRC Analysis

14.3. Europe In-Flight Connectivity Market, By Service Model, 2019-2032(US$ Mn)

14.3.1. Overview

14.3.2. SRC Analysis

14.4. Europe In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2032(US$ Mn)

14.4.1. Overview

14.4.2. SRC Analysis

14.5. Europe In-Flight Connectivity Market, By Aircraft Type, 2019-2032(US$ Mn)

14.5.1. Overview

14.5.2. SRC Analysis

14.6. Europe In-Flight Connectivity Market, by Country, 2019-2032 (US$ Mn)

14.6.1. Europe In-Flight Connectivity Market, by Country, 2023 Vs 2032 (in%)

14.6.2. UK

14.6.3. France

14.6.4. Germany

14.6.5. Italy

14.6.6. Spain

14.6.7. Benelux

14.6.8. Russia

14.6.9. Rest of Europe

15. Asia Pacific In-Flight Connectivity Market Analysis

15.1. Overview

15.1.1. Market Dynamics for North America

15.1.1.1. Drivers

15.1.1.2. Restraints

15.1.1.3. Opportunities

15.1.1.4. Trends

15.2. Asia Pacific In-Flight Connectivity Market, By Technology Type, 2019-2032(US$ Mn)

15.2.1. Overview

15.2.2. SRC Analysis

15.3. Asia Pacific In-Flight Connectivity Market, By Service Model, 2019-2032(US$ Mn)

15.3.1. Overview

15.3.2. SRC Analysis

15.4. Asia Pacific In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2032(US$ Mn)

15.4.1. Overview

15.4.2. SRC Analysis

15.5. Asia Pacific In-Flight Connectivity Market, By Aircraft Type, 2019-2032(US$ Mn)

15.5.1. Overview

15.5.2. SRC Analysis

15.6. Asia Pacific In-Flight Connectivity Market, by Country, 2019-2032 (US$ Mn)

15.6.1. Asia Pacific In-Flight Connectivity Market, by Country, 2023 Vs 2032 (in%)

15.6.2. China

15.6.3. Japan

15.6.4. India

15.6.5. South Korea

15.6.6. South East Asia

15.6.7. Rest of Asia Pacific

16. Latin America In-Flight Connectivity Market Analysis

16.1. Overview

16.1.1. Market Dynamics for North America

16.1.1.1. Drivers

16.1.1.2. Restraints

16.1.1.3. Opportunities

16.1.1.4. Trends

16.2. Latin America In-Flight Connectivity Market, By Technology Type, 2019-2032(US$ Mn)

16.2.1. Overview

16.2.2. SRC Analysis

16.3. Latin America In-Flight Connectivity Market, By Service Model, 2019-2032(US$ Mn)

16.3.1. Overview

16.3.2. SRC Analysis

16.4. Latin America In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2032(US$ Mn)

16.4.1. Overview

16.4.2. SRC Analysis

16.5. Latin America In-Flight Connectivity Market, By Aircraft Type, 2019-2032(US$ Mn)

16.5.1. Overview

16.5.2. SRC Analysis

16.6. Latin America In-Flight Connectivity Market, by Country, 2019-2032 (US$ Mn)

16.6.1. Latin America In-Flight Connectivity Market, by Country, 2023 Vs 2032 (in%)

16.6.2. Brazil

16.6.3. Argentina

16.6.4. Rest of Latin America

17. Middle East In-Flight Connectivity Market Analysis

17.1. Overview

17.1.1. Market Dynamics for North America

17.1.1.1. Drivers

17.1.1.2. Restraints

17.1.1.3. Opportunities

17.1.1.4. Trends

17.2. Middle East In-Flight Connectivity Market, By Technology Type, 2019-2032(US$ Mn)

17.2.1. Overview

17.2.2. SRC Analysis

17.3. Middle East In-Flight Connectivity Market, By Service Model, 2019-2032(US$ Mn)

17.3.1. Overview

17.3.2. SRC Analysis

17.4. Middle East In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2032(US$ Mn)

17.4.1. Overview

17.4.2. SRC Analysis

17.5. Middle East In-Flight Connectivity Market, By Aircraft Type, 2019-2032(US$ Mn)

17.5.1. Overview

17.5.2. SRC Analysis

17.6. Middle East In-Flight Connectivity Market, by Country, 2019-2032 (US$ Mn)

17.6.1. Middle East In-Flight Connectivity Market, by Country, 2023 Vs 2032 (in%)

17.6.2. UAE

17.6.3. Saudi Arabia

17.6.4. Rest of Middle East

18. Africa In-Flight Connectivity Market Analysis

18.1. Overview

18.1.1. Market Dynamics for North America

18.1.1.1. Drivers

18.1.1.2. Restraints

18.1.1.3. Opportunities

18.1.1.4. Trends

18.2. Africa In-Flight Connectivity Market, By Technology Type, 2019-2032(US$ Mn)

18.2.1. Overview

18.2.2. SRC Analysis

18.3. Africa In-Flight Connectivity Market, By Service Model, 2019-2032(US$ Mn)

18.3.1. Overview

18.3.2. SRC Analysis

18.4. Africa In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2032(US$ Mn)

18.4.1. Overview

18.4.2. SRC Analysis

18.5. Africa In-Flight Connectivity Market, By Aircraft Type, 2019-2032(US$ Mn)

18.5.1. Overview

18.5.2. SRC Analysis

18.6. Africa In-Flight Connectivity Market, by Country, 2019-2032 (US$ Mn)

18.6.1. Middle East In-Flight Connectivity Market, by Country, 2023 Vs 2032 (in%)

18.6.2. South Africa

18.6.3. Egypt

18.6.4. Rest of Africa

19. Company Profiles

19.1. BAE Systems

19.1.1. Company Overview

19.1.2. Technology Types/Services Portfolio

19.1.3. Geographical Presence

19.1.4. SWOT Analysis

19.1.5. Financial Summary

19.1.5.1. Market Revenue and Net Profit (2019-2023)

19.1.5.2. Business Segment Revenue Analysis

19.1.5.3. Geographical Revenue Analysis

19.2. Cobham plc

19.3. Collins Aerospace

19.4. Eutelsat Communications

19.5. Global Eagle Entertainment Inc.

19.6. Gogo LLC

19.7. Honeywell International Inc.

19.8. Inmarsat plc

19.9. Iridium Communications Inc.

19.10. Panasonic Corp.

19.11. Safran (Zodiac Aerospace SA)

19.12. SITAONAIR

19.13. Thales SA

19.14. ViaSat Inc.

20. Research Methodology

20.1. Research Methodology

20.2. High-Speed Connectivity – Secondary Research

20.3. High-Speed ConnectivityI – Data Modelling

20.3.1. Company Share Analysis Model

20.3.2. Revenue Based Modelling

20.4. High-Speed ConnectivityII – Primary Research

20.5. Research Limitations

20.5.1. Assumptions

List of Figures

FIG. 1 Global In-Flight Connectivity Market: Research Methodology

FIG. 2 Market Size Estimation – Top Down & Bottom up Approach

FIG. 3 Global In-Flight Connectivity Market Segmentation

FIG. 4 Global In-Flight Connectivity Market, By Technology Type, 2023 (US$ Mn)

FIG. 5 Global In-Flight Connectivity Market, By Service Model, 2023 (US$ Mn)

FIG. 6 Global In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023 (US$ Mn)

FIG. 7 Global In-Flight Connectivity Market, by Aircraft Type, 2023 (US$ Mn)

FIG. 8 Global In-Flight Connectivity Market, by Geography, 2023 (US$ Mn)

FIG. 9 Attractive Investment Proposition, By Technology Type, 2023

FIG. 10 Attractive Investment Proposition, By Service Model, 2023

FIG. 11 Attractive Investment Proposition, By Connectivity Speed and Quality, 2023

FIG. 12 Attractive Investment Proposition, By Aircraft Type, 2023

FIG. 13 Attractive Investment Proposition, by Geography, 2023

FIG. 14 Global Market Share Analysis of Key In-Flight Connectivity Market Manufacturers, 2023

FIG. 15 Global Market Positioning of Key In-Flight Connectivity Market Manufacturers, 2023

FIG. 16 Global In-Flight Connectivity Market Value Contribution, By Technology Type, 2023 & 2032 (Value %)

FIG. 17 Global In-Flight Connectivity Market, by Satellite Connectivity, Value, 2019-2032 (US$ Mn)

FIG. 18 Global In-Flight Connectivity Market, by Air-to-Ground (ATG) Connectivity, Value, 2019-2032 (US$ Mn)

FIG. 19 Global In-Flight Connectivity Market, by Hybrid Connectivity, Value, 2019-2032 (US$ Mn)

FIG. 20 lobal In-Flight Connectivity Market Value Contribution, By Service Model, 2023 & 2032 (Value %)

FIG. 21 Global In-Flight Connectivity Market, by Free Wi-Fi, Value, 2019-2032 (US$ Mn)

FIG. 22 Global In-Flight Connectivity Market, by Paid Wi-Fi, Value, 2019-2032 (US$ Mn)

FIG. 23 Global In-Flight Connectivity Market, by Freemium Model, Value, 2019-2032 (US$ Mn)

FIG. 24 Global In-Flight Connectivity Market Value Contribution, By Connectivity Speed and Quality, 2023 & 2032 (Value %)

FIG. 25 Global In-Flight Connectivity Market, by High-Speed Connectivity, Value, 2019-2032 (US$ Mn)

FIG. 26 Global In-Flight Connectivity Market, by Standard Connectivity, Value, 2019-2032 (US$ Mn)

FIG. 27 Global In-Flight Connectivity Market, by Low-Bandwidth Connectivity, Value, 2019-2032 (US$ Mn)

FIG. 28 Global In-Flight Connectivity Market Value Contribution, By Aircraft Type, 2023 & 2032 (Value %)

FIG. 29 Global In-Flight Connectivity Market, by Narrow-Body Aircraft, Value, 2019-2032 (US$ Mn)

FIG. 30 Global In-Flight Connectivity Market, by Wide-Body Aircraft, Value, 2019-2032 (US$ Mn)

FIG. 31 Global In-Flight Connectivity Market, by Regional Aircraft, Value, 2019-2032 (US$ Mn)

FIG. 32 North America In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 33 U.S. In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 34 Canada In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 35 Mexico In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 36 Europe In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 37 Germany In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 38 France In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 39 U.K. In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 40 Italy In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 41 Spain In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 42 Benelux In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 43 Russia In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 44 Rest of Europe In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 45 Asia Pacific In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 46 China In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 47 Japan In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 48 India In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 49 South Korea In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 50 South-East Asia In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 51 Rest of Asia Pacific In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 52 Latin America In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 53 Brazil In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 54 Argentina In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 55 Rest of Latin America In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 56 Middle East In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 57 UAE In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 58 Saudi Arabia In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 59 Rest of Middle East In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 60 Africa In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 61 South Africa In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 62 Egypt In-Flight Connectivity Market, 2019-2032 (US$ Mn)

FIG. 63 Rest of Africa In-Flight Connectivity Market, 2019-2032 (US$ Mn)

List of Tables

TABLE 1 Market Snapshot: Global In-Flight Connectivity Market

TABLE 2 Global In-Flight Connectivity Market: Drivers Impact Analysis

TABLE 3 Global In-Flight Connectivity Market: Market Restraints Impact Analysis

TABLE 4 Global In-Flight Connectivity Market, by Competitive Benchmarking, 2023

TABLE 5 Global In-Flight Connectivity Market, by Geographical Presence Analysis, 2023

TABLE 6 Global In-Flight Connectivity Market, by Key Strategies Analysis, 2023

TABLE 7 Global In-Flight Connectivity Market, by Satellite Connectivity, By Region, 2019-2023 (US$ Mn)

TABLE 8 Global In-Flight Connectivity Market, by Satellite Connectivity, By Region, 2023-2032 (US$ Mn)

TABLE 9 Global In-Flight Connectivity Market, by Air-to-Ground (ATG) Connectivity, By Region, 2019-2023 (US$ Mn)

TABLE 10 Global In-Flight Connectivity Market, by Air-to-Ground (ATG) Connectivity, By Region, 2023-2032 (US$ Mn)

TABLE 11 Global In-Flight Connectivity Market, by Hybrid Connectivity, By Region, 2019-2023 (US$ Mn)

TABLE 12 Global In-Flight Connectivity Market, by Hybrid Connectivity, By Region, 2023-2032 (US$ Mn)

TABLE 13 Global In-Flight Connectivity Market, by Free Wi-Fi, By Region, 2019-2023 (US$ Mn)

TABLE 14 Global In-Flight Connectivity Market, by Free Wi-Fi, By Region, 2023-2032 (US$ Mn)

TABLE 15 Global In-Flight Connectivity Market, by Paid Wi-Fi, By Region, 2019-2023 (US$ Mn)

TABLE 16 Global In-Flight Connectivity Market, by Paid Wi-Fi, By Region, 2023-2032 (US$ Mn)

TABLE 17 Global In-Flight Connectivity Market, by Freemium Model, By Region, 2019-2023 (US$ Mn)

TABLE 18 Global In-Flight Connectivity Market, by Freemium Model, By Region, 2023-2032 (US$ Mn)

TABLE 19 Global In-Flight Connectivity Market, by High-Speed Connectivity, By Region, 2019-2023 (US$ Mn)

TABLE 20 Global In-Flight Connectivity Market, by High-Speed Connectivity, By Region, 2023-2032 (US$ Mn)

TABLE 21 Global In-Flight Connectivity Market, by Standard Connectivity, By Region, 2019-2023 (US$ Mn)

TABLE 22 Global In-Flight Connectivity Market, by Standard Connectivity, By Region, 2023-2032 (US$ Mn)

TABLE 23 Global In-Flight Connectivity Market, by Low-Bandwidth Connectivity, By Region, 2019-2023 (US$ Mn)

TABLE 24 Global In-Flight Connectivity Market, by Low-Bandwidth Connectivity, By Region, 2023-2032 (US$ Mn)

TABLE 25 Global In-Flight Connectivity Market, by Narrow-Body Aircraft, By Region, 2019-2023 (US$ Mn)

TABLE 26 Global In-Flight Connectivity Market, by Narrow-Body Aircraft, By Region, 2023-2032 (US$ Mn)

TABLE 27 Global In-Flight Connectivity Market, by Wide-Body Aircraft, By Region, 2019-2023 (US$ Mn)

TABLE 28 Global In-Flight Connectivity Market, by Wide-Body Aircraft, By Region, 2023-2032 (US$ Mn)

TABLE 29 Global In-Flight Connectivity Market, by Regional Aircraft, By Region, 2019-2023 (US$ Mn)

TABLE 30 Global In-Flight Connectivity Market, by Regional Aircraft, By Region, 2023-2032 (US$ Mn)

TABLE 31 Global In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 32 Global In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 33 Global In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 34 Global In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 35 Global In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 36 Global In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 37 Global In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 38 Global In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 39 Global In-Flight Connectivity Market, by Region, 2019-2023 (US$ Mn)

TABLE 40 Global In-Flight Connectivity Market, by Region, 2023-2032 (US$ Mn)

TABLE 41 North America In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 42 North America In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 43 North America In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 44 North America In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 45 North America In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 46 North America In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 47 North America In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 48 North America In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 49 North America In-Flight Connectivity Market, by Country, 2019-2023 (US$ Mn)

TABLE 50 North America In-Flight Connectivity Market, by Country, 2023-2032 (US$ Mn)

TABLE 51 United States In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 52 United States In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 53 United States In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 54 United States In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 55 United States In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 56 United States In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 57 United States In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 58 United States In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 59 Canada In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 60 Canada In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 61 Canada In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 62 Canada In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 63 Canada In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 64 Canada In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 65 Canada In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 66 Canada In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 67 Mexico In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 68 Mexico In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 69 Mexico In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 70 Mexico In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 71 Mexico In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 72 Mexico In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 73 Mexico In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 74 Mexico In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 75 Europe In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 76 Europe In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 77 Europe In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 78 Europe In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 79 Europe In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 80 Europe In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 81 Europe In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 82 Europe In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 83 Europe In-Flight Connectivity Market, by Country, 2019-2023 (US$ Mn)

TABLE 84 Europe In-Flight Connectivity Market, by Country, 2023-2032 (US$ Mn)

TABLE 85 Germany In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 86 Germany In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 87 Germany In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 88 Germany In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 89 Germany In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 90 Germany In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 91 Germany In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 92 Germany In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 93 France In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 94 France In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 95 France In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 96 France In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 97 France In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 98 France In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 99 France In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 100 France In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 101 United Kingdom In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 102 United Kingdom In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 103 United Kingdom In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 104 United Kingdom In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 105 United Kingdom In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 106 United Kingdom In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 107 United Kingdom In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 108 United Kingdom In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 109 Italy In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 110 Italy In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 111 Italy In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 112 Italy In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 113 Italy In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 114 Italy In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 115 Italy In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 116 Italy In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 117 Spain In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 118 Spain In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 119 Spain In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 120 Spain In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 121 Spain In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 122 Spain In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 123 Spain In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 124 Spain In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 125 Benelux In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 126 Benelux In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 127 Benelux In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 128 Benelux In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 129 Benelux In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 130 Benelux In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 131 Benelux In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 132 Benelux In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 133 Russia In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 134 Russia In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 135 Russia In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 136 Russia In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 137 Russia In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 138 Russia In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 139 Russia In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 140 Russia In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 141 Rest of Europe In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 142 Rest of Europe In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 143 Rest of Europe In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 144 Rest of Europe In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 145 Rest of Europe In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 146 Rest of Europe In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 147 Rest of Europe In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 148 Rest of Europe In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 149 Asia Pacific In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 150 Asia Pacific In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 151 Asia Pacific In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 152 Asia Pacific In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 153 Asia Pacific In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 154 Asia Pacific In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 155 Asia Pacific In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 156 Asia Pacific In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 157 China In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 158 China In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 159 China In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 160 China In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 161 China In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 162 China In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 163 China In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 164 China In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 165 Japan In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 166 Japan In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 167 Japan In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 168 Japan In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 169 Japan In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 170 Japan In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 171 Japan In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 172 Japan In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 173 India In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 174 India In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 175 India In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 176 India In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 177 India In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 178 India In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 179 India In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 180 India In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 181 South Korea In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 182 South Korea In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 183 South Korea In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 184 South Korea In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 185 South Korea In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 186 South Korea In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 187 South Korea In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 188 South Korea In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 189 South-East Asia In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 190 South-East Asia In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 191 South-East Asia In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 192 South-East Asia In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 193 South-East Asia In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 194 South-East Asia In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 195 South-East Asia In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 196 South-East Asia In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 197 Rest of Asia Pacific In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 198 Rest of Asia Pacific In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 199 Rest of Asia Pacific In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 200 Rest of Asia Pacific In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 201 Rest of Asia Pacific In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 202 Rest of Asia Pacific In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 203 Rest of Asia Pacific In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 204 Rest of Asia Pacific In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 205 Latin America In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 206 Latin America In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 207 Latin America In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 208 Latin America In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 209 Latin America In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 210 Latin America In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 211 Latin America In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 212 Latin America In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 213 Brazil In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 214 Brazil In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 215 Brazil In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 216 Brazil In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 217 Brazil In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 218 Brazil In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 219 Brazil In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 220 Brazil In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 221 Argentina In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 222 Argentina In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 223 Argentina In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 224 Argentina In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 225 Argentina In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 226 Argentina In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 227 Argentina In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 228 Argentina In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 229 Rest of Latin America In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 230 Rest of Latin America In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 231 Rest of Latin America In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 232 Rest of Latin America In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 233 Rest of Latin America In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 234 Rest of Latin America In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 235 Rest of Latin America In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 236 Rest of Latin America In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 237 Middle East In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 238 Middle East In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 239 Middle East In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 240 Middle East In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 241 Middle East In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 242 Middle East In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 243 Middle East In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 244 Middle East In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 245 UAE In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 246 UAE In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 247 UAE In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 248 UAE In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 249 UAE In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 250 UAE In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 251 UAE In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 252 UAE In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 253 Saudi Arabia In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 254 Saudi Arabia In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 255 Saudi Arabia In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 256 Saudi Arabia In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 257 Saudi Arabia In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 258 Saudi Arabia In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 259 Saudi Arabia In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 260 Saudi Arabia In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 261 Rest of Middle East In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 262 Rest of Middle East In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 263 Rest of Middle East In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 264 Rest of Middle East In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 265 Rest of Middle East In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 266 Rest of Middle East In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 267 Rest of Middle East In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 268 Rest of Middle East In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 269 Africa In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 270 Africa In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 271 Africa In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 272 Africa In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 273 Africa In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 274 Africa In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 275 Africa In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 276 Africa In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 277 South Africa In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 278 South Africa In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 279 South Africa In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 280 South Africa In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 281 South Africa In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 282 South Africa In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 283 South Africa In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 284 South Africa In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 285 Egypt In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 286 Egypt In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 287 Egypt In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 288 Egypt In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 289 Egypt In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 290 Egypt In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 291 Egypt In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 292 Egypt In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)

TABLE 293 Rest of Africa In-Flight Connectivity Market, By Technology Type, 2019-2023 (US$ Mn)

TABLE 294 Rest of Africa In-Flight Connectivity Market, By Technology Type, 2023-2032 (US$ Mn)

TABLE 295 Rest of Africa In-Flight Connectivity Market, By Service Model, 2019-2023 (US$ Mn)

TABLE 296 Rest of Africa In-Flight Connectivity Market, By Service Model, 2023-2032 (US$ Mn)

TABLE 297 Rest of Africa In-Flight Connectivity Market, By Connectivity Speed and Quality, 2019-2023 (US$ Mn)

TABLE 298 Rest of Africa In-Flight Connectivity Market, By Connectivity Speed and Quality, 2023-2032 (US$ Mn)

TABLE 299 Rest of Africa In-Flight Connectivity Market, By Aircraft Type, By Region, 2019-2023 (US$ Mn)

TABLE 300 Rest of Africa In-Flight Connectivity Market, By Aircraft Type, By Region, 2023-2032 (US$ Mn)