Market Overview

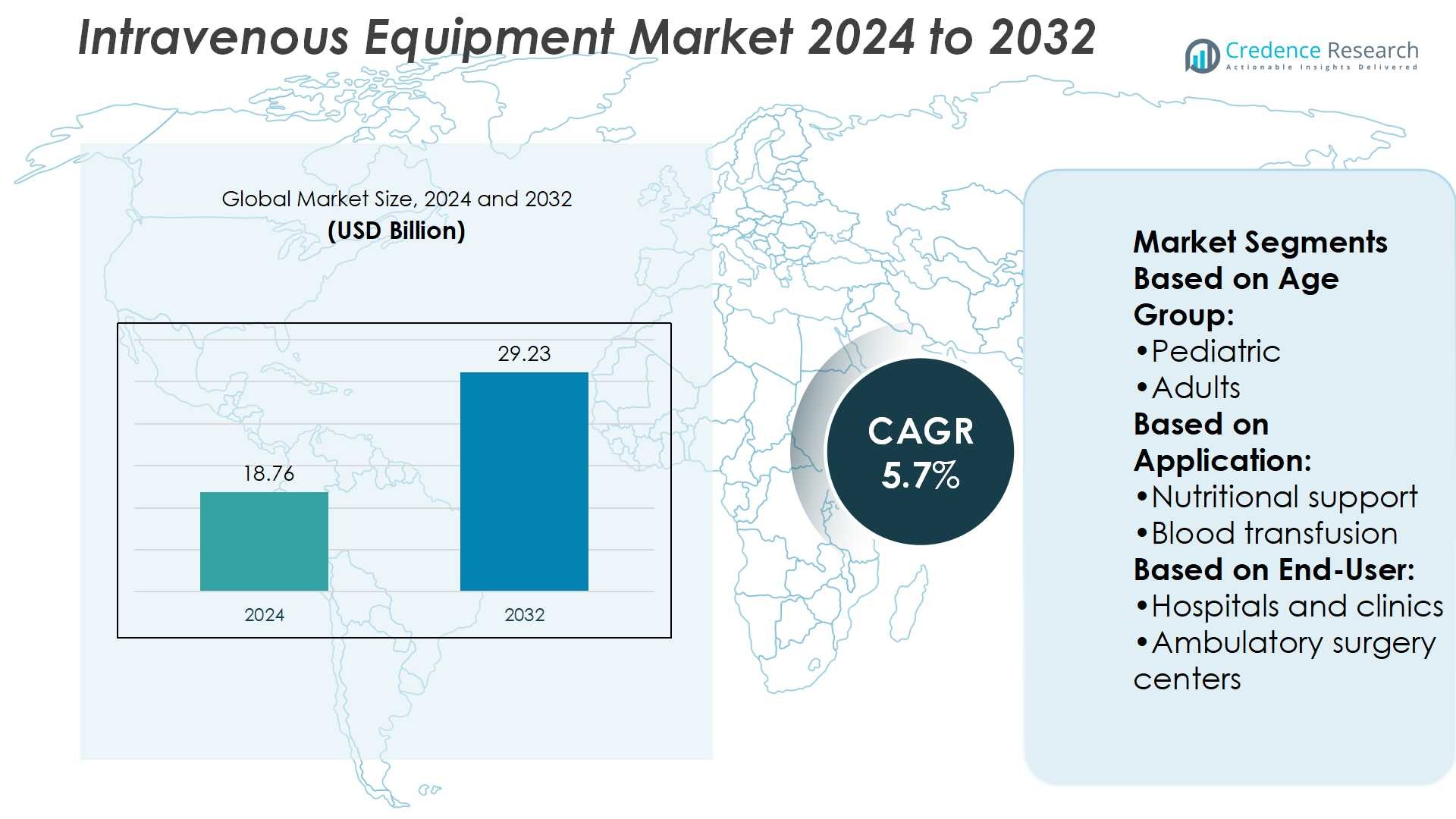

Intravenous Equipment Market size was valued at USD 18.76 billion in 2024 and is anticipated to reach USD 29.23 billion by 2032, at a CAGR of 5.7% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Intravenous Equipment Market Size 2024 |

USD 18.76 Billion |

| Intravenous Equipment Market, CAGR |

5.7% |

| Intravenous Equipment Market Size 2032 |

USD 29.23 Billion |

The Intravenous Equipment Market is driven by rising demand for advanced infusion therapies, growing prevalence of chronic and infectious diseases, and increasing surgical procedures requiring precise fluid and drug administration. It gains momentum from technological advancements in smart infusion systems that improve accuracy, safety, and integration with digital healthcare platforms. Expanding homecare and ambulatory services also boost adoption, supported by insurance coverage and patient preference for convenient treatment. Trends such as the growing use of biologics, rising demand for portable and wearable devices, and focus on sustainability in product design are shaping the market’s evolution and long-term growth prospects.

The Intravenous Equipment Market shows strong regional presence, with North America leading due to advanced healthcare systems, followed by Europe with strict regulatory standards, and Asia-Pacific emerging as the fastest-growing region driven by healthcare investments and large patient populations. Latin America and the Middle East & Africa contribute steadily with gradual adoption of modern infusion technologies. Key players shaping the market include Abbott, BD, Baxter, B. Braun Melsungen AG, 3M, Terumo Corporation, Teleflex Incorporated, Smiths Medical, Henry Schein, Inc., and Ascor S.A.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Intravenous Equipment Market was valued at USD 18.76 billion in 2024 and will reach USD 29.23 billion by 2032, growing at a CAGR of 5.7%.

- Rising demand for advanced infusion therapies and increasing surgical procedures drive strong market growth.

- Growing prevalence of chronic and infectious diseases strengthens the need for reliable intravenous systems.

- Technological advancements in smart infusion pumps enhance accuracy, safety, and digital integration.

- High costs of advanced devices and risk of infections remain key restraints in adoption.

- North America leads the market, Europe holds the second-largest share, while Asia-Pacific shows the fastest growth.

- Leading players focus on innovation, global expansion, and sustainable product design to strengthen competitiveness.

Market Drivers

Rising Demand for Advanced Infusion Therapies Across Healthcare Settings

The Intravenous Equipment Market is expanding due to the growing need for safe and precise infusion therapies in hospitals, clinics, and ambulatory care centers. Increasing prevalence of chronic conditions such as cancer, diabetes, and cardiovascular diseases drives continuous adoption of IV devices. It supports treatment protocols requiring controlled drug administration, fluid therapy, and nutritional support. Growing surgical procedures also elevate usage, as IV systems remain essential for anesthesia and perioperative care. Market growth benefits from continuous integration of smart pumps and advanced monitoring systems. These innovations improve accuracy, reduce errors, and enhance patient safety, making intravenous solutions indispensable in modern healthcare.

- For instance, Abbott’s HeartMate 3 heart pump, in the MOMENTUM 3 trial involving more than 1,000 patients, showed that the five-year survival rate was 58.4%, compared to 43.7% in the control arm with HeartMate II.

Rising Burden of Chronic and Infectious Diseases Driving Adoption

The Intravenous Equipment Market benefits from increasing incidence of infectious and chronic diseases that demand long-term infusion therapy. Cancer patients often require chemotherapy through IV delivery, while diabetic patients rely on intravenous drugs in complex cases. It strengthens the role of IV systems in hospitals and homecare settings alike. Infectious diseases, including sepsis, further heighten the demand for rapid fluid replacement and antibiotic infusion. The growing aging population also fuels demand, as elderly patients frequently require hydration and medication through IV routes. Expanding use of biologics and specialty drugs enhances reliance on precise infusion equipment.

- For instance, Henry Schein’s Blood Control IV Catheter 20-Gauge has a 1-inch beveled tip and comes 50 units per box, 4 boxes per case, ensuring standardization and ease of supply chain handling.

Technological Advancements in Smart Infusion Systems Enhancing Safety

The Intravenous Equipment Market gains momentum from ongoing technological upgrades in infusion pumps, catheters, and accessories. Advanced systems incorporate wireless connectivity, real-time data tracking, and safety alarms that prevent medication errors. It allows healthcare providers to achieve precise dosing and monitor treatment compliance remotely. Integration with hospital information systems strengthens clinical decision-making and efficiency. Increasing investment in automation and IoT-enabled devices reflects the shift toward smart healthcare infrastructure. Regulatory focus on patient safety also drives innovation in design, material quality, and usability of intravenous devices.

Expanding Homecare and Ambulatory Care Services Boosting Equipment Demand

The Intravenous Equipment Market benefits from growing preference for treatment in homecare and ambulatory settings. Rising healthcare costs and patient preference for convenience encourage adoption of portable IV equipment. It enables safe delivery of antibiotics, chemotherapy, and hydration therapy outside traditional hospitals. Technological improvements in compact pumps and disposable IV sets support this transition. Healthcare providers increasingly recommend home infusion services to reduce hospital stays and associated costs. Insurance coverage for home-based treatments further strengthens market growth, expanding opportunities across developed and emerging regions.

Market Trends

Growing Integration of Smart and Connected Infusion Technologies

The Intravenous Equipment Market is witnessing strong momentum with the adoption of smart and connected devices. Infusion pumps with wireless connectivity and remote monitoring features are becoming standard across advanced healthcare systems. It allows real-time tracking of dosage and enhances safety by minimizing manual errors. Integration with electronic health records ensures seamless data flow between patients and clinicians. Healthcare providers are increasingly investing in connected systems to support efficiency and compliance. This trend reflects the broader move toward digital healthcare ecosystems where automation improves outcomes and reduces risks.

- For instance, Terumo’s MEDISAFE WITH patch pump’s main unit dimensions are 77.9 mm x 40.1 mm x 18.9 mm, weight is 34 g. Also, its remote control measures 136.2 mm x 75.0 mm x 14.3 mm, weighs 152 g with 2 AAA batteries.

Rising Demand for Portable and Wearable Infusion Devices in Homecare

The Intravenous Equipment Market is benefiting from growing demand for compact and wearable devices designed for homecare. Patients with chronic diseases prefer treatment at home to avoid extended hospital stays. It drives adoption of lightweight infusion pumps that offer safety and ease of use. The trend supports the expansion of ambulatory services, particularly in developed regions with high healthcare costs. Portable devices also enable continuous therapy for patients who require mobility during treatment. The shift toward decentralized care makes portable intravenous equipment a critical growth factor.

- For instance, Ascor S.A.’s AP31 volumetric infusion pump handles infusion volumes from 9 ml to 999 ml, adjustable in 0.1 ml increments. The flow rate range is programmable from 1 ml/h to 1000 ml/h, with a user-selectable drug library and the ability to store up to 500 events in real time or as XML files.

Increased Use of Biologics and Specialty Drugs Requiring Intravenous Delivery

The Intravenous Equipment Market is expanding due to the rising use of biologics and specialty drugs that require infusion delivery. Oncology, immunology, and rare disease treatments often rely on intravenous administration for effectiveness. It reinforces the need for precision-engineered equipment capable of handling complex formulations. Growing approvals of monoclonal antibodies and cell-based therapies amplify this trend. Pharmaceutical companies are collaborating with device manufacturers to ensure compatibility with advanced drugs. The demand for reliable intravenous systems aligns with expanding pipelines of high-value therapies.

Focus on Sustainability and Eco-Friendly Intravenous Device Solutions

The Intravenous Equipment Market is shaped by the increasing focus on sustainability in healthcare practices. Manufacturers are developing recyclable materials and reducing plastic waste in disposable IV sets. It addresses environmental concerns and aligns with global sustainability goals. Hospitals and clinics prefer vendors that provide eco-friendly alternatives without compromising safety or quality. Regulatory authorities also support sustainable initiatives by encouraging green manufacturing practices. This trend highlights the growing balance between technological innovation and environmental responsibility in intravenous equipment design.

Market Challenges Analysis

High Risk of Infections and Device-Related Complications Limiting Wider Adoption

The Intravenous Equipment Market faces challenges linked to hospital-acquired infections and device-related complications. Catheter-associated bloodstream infections remain a critical concern for healthcare providers worldwide. It raises the need for stringent sterilization protocols and advanced material innovations. Repeated needle insertion and long-term use increase risks of thrombosis, leakage, and patient discomfort. These complications can lead to extended hospital stays and higher treatment costs, discouraging broader usage in certain settings. Regulatory authorities continue to push for safer device designs, but achieving consistent compliance remains difficult across emerging markets.

High Costs, Training Needs, and Stringent Regulatory Barriers Slowing Growth

The Intravenous Equipment Market is also challenged by the high costs of advanced devices and the training required for proper operation. Smart infusion pumps and connected systems, while effective, remain expensive for hospitals with limited budgets. It creates disparities in adoption between developed and developing regions. Complex equipment demands skilled staff, and lack of adequate training may lead to dosing errors and misuse. Stringent regulatory requirements for product approval and quality assurance also extend timelines and raise development costs. These barriers limit innovation speed and slow the expansion of new intravenous technologies.

Market Opportunities

Expanding Role of Homecare and Ambulatory Infusion Services Creating Growth Potential

The Intravenous Equipment Market holds strong opportunities with the rising shift toward homecare and ambulatory services. Patients prefer receiving treatment at home to reduce hospital visits and healthcare costs. It drives demand for portable, user-friendly, and safe infusion systems that support chronic disease management. Insurance coverage for home infusion therapies is expanding, further boosting adoption. Emerging economies are also investing in outpatient and day-care centers, creating new growth avenues. Manufacturers that develop compact, reliable devices tailored for non-hospital settings can capture a significant share of this opportunity.

Growing Demand for Smart Devices and Biologics Supporting Future Expansion

The Intravenous Equipment Market is set to benefit from increasing reliance on biologics and the adoption of smart infusion systems. Advanced therapies such as monoclonal antibodies and cell-based treatments require accurate and controlled delivery. It creates an opportunity for manufacturers to innovate devices with precision dosing and digital connectivity. Integration of IoT and AI into infusion pumps enhances monitoring, reduces errors, and improves patient outcomes. Healthcare systems are prioritizing technologies that combine safety with efficiency, opening doors for digital-enabled intravenous solutions. Rising pharmaceutical investments in specialty drugs will further expand opportunities for IV equipment providers.

Market Segmentation Analysis:

By Age Group

The Intravenous Equipment Market demonstrates strong usage across pediatric, adult, and geriatric populations. Pediatric patients require specialized devices with smaller dimensions to ensure safe administration. Adults represent the largest share, driven by high prevalence of chronic diseases and rising surgical procedures. It supports growing demand for accurate infusion therapy in oncology, cardiology, and infectious disease treatments. The geriatric segment is expanding rapidly due to an aging global population that often requires long-term infusion therapies. Rising incidence of dehydration, nutritional deficiencies, and multiple comorbidities in elderly patients reinforces the need for advanced intravenous solutions.

- For instance, BD’s primary IV administration sets for pediatric use often feature microbore tubing under 2 mm internal diameter, which minimizes priming volume and suits low-volume infusions.

By Application

The market is segmented into nutritional support, blood transfusion, fluid and electrolyte balance, and other applications. Nutritional support holds significant demand, particularly for patients unable to consume food orally or those undergoing cancer treatment. Blood transfusion represents a steady segment, supported by rising cases of trauma, surgeries, and blood disorders. It remains essential in emergency care and chronic anemia management. Fluid and electrolyte balance dominates applications, as IV systems are critical for rehydration and maintaining stability in critical care. Other applications, including chemotherapy and drug administration, continue to expand alongside pharmaceutical advancements.

- For instance, B. Braun’s Gravity Blood Administration Set with hand pump and 1 CARESITE® Injection Site features a priming volume of 75 mL, length 89 inches, 170-micron filter, 10 drops per mL drip rate.

By End User

The market includes hospitals and clinics and ambulatory surgery centers as key end users. Hospitals and clinics represent the largest segment due to the concentration of advanced treatment facilities and high patient inflow. It accounts for strong adoption of both basic IV sets and advanced smart pumps. Ambulatory surgery centers are growing steadily as outpatient procedures rise and patients seek cost-effective treatment alternatives. These centers require efficient and portable intravenous devices to support short-stay treatments. The expansion of outpatient care models ensures strong opportunities for IV equipment adoption outside traditional hospital environments.

Segments:

Based on Age Group:

Based on Application:

- Nutritional support

- Blood transfusion

Based on End-User:

- Hospitals and clinics

- Ambulatory surgery centers

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America holds the largest share of the Intravenous Equipment Market, accounting for 37.2% in 2024. The region benefits from advanced healthcare infrastructure, strong regulatory standards, and high adoption of smart infusion systems. It is supported by rising cases of chronic diseases, including cancer, diabetes, and cardiovascular disorders, which require regular intravenous therapies. The United States dominates regional demand, driven by significant healthcare spending, technological adoption, and well-established hospital networks. Canada contributes steadily, supported by government investment in public healthcare and growing home infusion services. The presence of leading manufacturers and continuous product innovation further secures North America’s position as the largest regional market. Rising focus on automation, integration of IoT-enabled devices, and increasing emphasis on patient safety will continue to support the region’s leadership in the forecast period.

Europe

Europe represents 28.6% of the Intravenous Equipment Market in 2024, holding the second-largest share. The region’s market is driven by an aging population, high prevalence of chronic diseases, and growing demand for advanced infusion therapies. It benefits from strong regulatory frameworks that emphasize patient safety, particularly in infusion pump design and IV set quality. Germany, France, and the United Kingdom are leading contributors, supported by advanced healthcare systems and growing research in infusion technology. Southern and Eastern Europe also show rising adoption due to investments in healthcare modernization. The increasing shift toward homecare infusion services, along with government-funded healthcare access, strengthens demand across the region. Europe’s emphasis on sustainability and eco-friendly medical devices is influencing the development of recyclable and safer intravenous equipment, reinforcing steady growth prospects.

Asia-Pacific

Asia-Pacific holds 21.4% of the Intravenous Equipment Market in 2024, emerging as the fastest-growing region. The market expansion is fueled by rising healthcare investments, expanding hospital infrastructure, and a large patient base. China, Japan, and India represent the largest contributors, with increasing demand for IV systems in oncology, critical care, and infectious disease management. It benefits from rapid growth in medical tourism, particularly in India and Southeast Asia, which boosts demand for advanced infusion solutions. The rise in chronic illnesses, coupled with expanding health insurance coverage, encourages higher spending on intravenous therapies. Local manufacturers are entering the market with cost-effective devices, while global companies are expanding operations to capture regional opportunities. Strong growth in homecare infusion adoption is expected to further accelerate market share in Asia-Pacific.

Latin America

Latin America accounts for 7.5% of the Intravenous Equipment Market in 2024, reflecting steady but limited adoption compared to larger regions. Brazil and Mexico lead the regional demand, supported by improving hospital infrastructure and growing awareness of advanced infusion therapies. It is influenced by rising healthcare spending, particularly in urban centers where modern hospitals are concentrated. Challenges such as uneven healthcare access and budget limitations in rural areas slow overall growth. Nonetheless, increasing adoption of intravenous systems for critical care, oncology, and emergency treatments supports steady expansion. Government initiatives to improve public health services and rising investments from private healthcare providers contribute to market opportunities. Latin America is expected to benefit from gradual expansion of ambulatory and homecare services in the coming years.

Middle East and Africa

The Middle East and Africa collectively hold 5.3% of the Intravenous Equipment Market in 2024, representing the smallest regional share. The Middle East, particularly Saudi Arabia, the United Arab Emirates, and Qatar, demonstrates strong demand due to advanced healthcare infrastructure and high investments in modern medical technology. Africa reflects slower adoption because of limited access to advanced healthcare facilities and high costs of smart infusion systems. It faces challenges such as shortage of skilled healthcare professionals and restricted budgets for advanced equipment procurement. However, rising government focus on healthcare modernization and international collaborations are creating growth potential. Increasing incidence of infectious diseases, coupled with expanding hospital networks in urban regions, supports gradual adoption of IV equipment. Over time, efforts to strengthen healthcare systems are expected to improve market presence in the Middle East and Africa.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Abbott

- Henry Schein, Inc.

- Smiths Medical

- Terumo Corporation

- Ascor S.A.

- BD

- Braun Melsungen AG

- Baxter

- 3M

- Teleflex Incorporated

Competitive Analysis

The Intravenous Equipment Market players including Abbott, BD, Baxter, B. Braun Melsungen AG, 3M, Terumo Corporation, Teleflex Incorporated, Smiths Medical, Henry Schein, Inc., and Ascor S.A. The Intravenous Equipment Market is characterized by strong competition, driven by innovation, product diversification, and global distribution strategies. Companies are focusing on advanced infusion pumps, safety catheters, and eco-friendly IV sets to meet rising demand across hospitals, clinics, and homecare settings. It is shaped by continuous investment in smart technologies, such as connected infusion systems with real-time monitoring, which enhance accuracy and reduce risks. Growing emphasis on sustainability and compliance with stringent regulatory standards also influences product development. Strategic initiatives, including mergers, partnerships, and regional expansions, play a critical role in strengthening market positions. The landscape reflects a balance between innovation-led growth and the need for cost-effective solutions tailored to both developed and emerging markets.

Recent Developments

- In March 2025, beOnd Airlines announced a partnership with The Elixir Clinic to offer passengers exclusive IV Vitamin Drip therapy as an add-on to their flight bookings, enhancing wellness and hydration before or after flights between Dubai, the Maldives, and Zurich.

- In April 2024, Lemer Pax, a global radiation protection leader, partnered with ICU Medical to distribute the Plum 360 infusion pump in France’s nuclear medicine sector, aiming to expand sales across the European market.

- In October 2023, B. Braun Medical Inc. (B. Braun), a leader in smart infusion therapy, launched its new Introcan Safety® 2 IV Catheter with Multi-Access Blood Control. IV access is a critical element of infusion therapy, and needlestick injuries continue to be a serious risk faced by clinicians in their daily routines, potentially exposing them to bloodborne pathogens.

- In April 2023, BD (Becton, Dickinson and Company), a leading global medical technology company, launched a new, easy-to-use advanced ultrasound device with a specialized probe designed to provide clinicians with optimal IV placement.

Report Coverage

The research report offers an in-depth analysis based on Age Group, Application, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will see rising adoption of smart infusion pumps with wireless connectivity.

- Homecare and ambulatory infusion services will expand significantly across regions.

- Demand for portable and wearable IV devices will continue to grow among chronic patients.

- Hospitals will prioritize connected systems that integrate with electronic health records.

- Sustainability will influence product design through recyclable and eco-friendly IV materials.

- Use of biologics and specialty drugs will boost the need for precision infusion systems.

- Emerging markets will invest heavily in modern hospital infrastructure and IV technologies.

- Artificial intelligence and IoT will enhance monitoring and reduce medication errors.

- Regulatory frameworks will push manufacturers toward higher safety and compliance standards.

- Partnerships between pharmaceutical companies and device makers will strengthen product development.