Market Overview

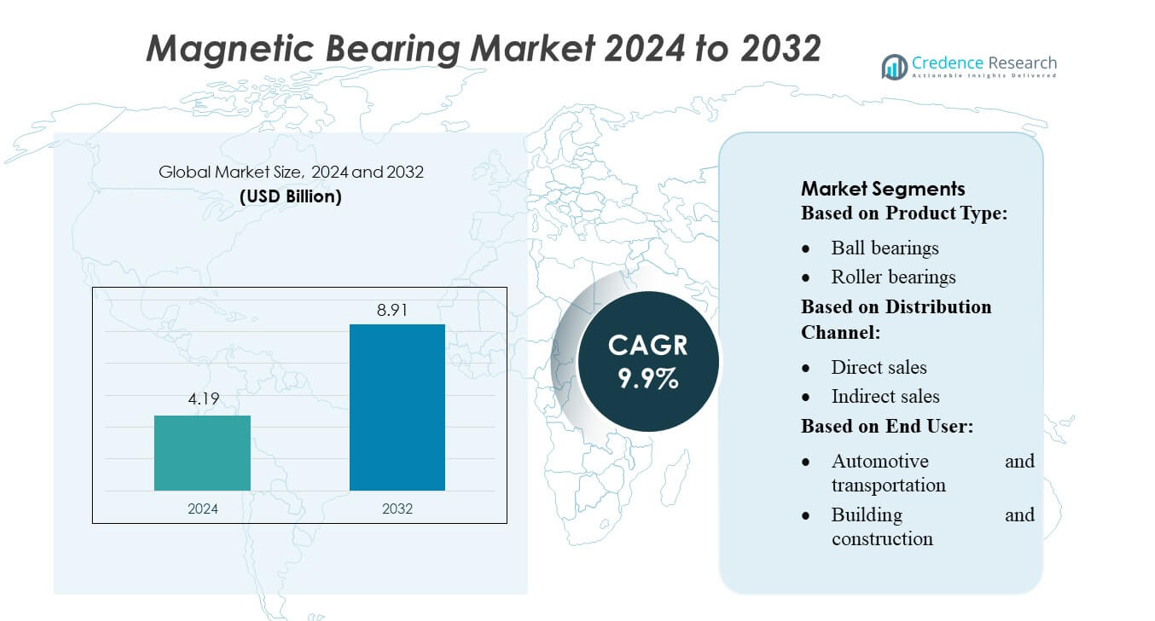

Magnetic Bearing Market size was valued USD 4.19 billion in 2024 and is anticipated to reach USD 8.91 billion by 2032, at a CAGR of 9.9% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Magnetic Bearing Market Size 2024 |

USD 4.19 billion |

| Magnetic Bearing Market, CAGR |

9.9% |

| Magnetic Bearing Market Size 2032 |

USD 8.91 billion |

The magnetic bearing market is dominated by leading players such as Rexnord Corporation, Brammer PLC, RBC Bearings Inc., NTN Corporation, NSK Global, HKT Bearings Ltd., JTEKT Corporation, RHP Bearings, NBI Bearings Europe, and Harbin Bearing Manufacturing Co., Ltd. These companies focus on technological innovation, energy-efficient solutions, and high-speed, low-maintenance bearing systems across industries including aerospace, power generation, and oil & gas. They leverage research and development, strategic partnerships, and regional expansions to maintain competitive advantages and address evolving customer demands. Asia Pacific emerges as the leading region in the market, accounting for approximately 38% of the global share, driven by rapid industrialization, infrastructure growth, and rising demand for advanced machinery in countries such as China, India, Japan, and South Korea. The region’s investment in renewable energy and industrial modernization is expected to sustain its leadership in the coming years.

Market Insights

- The magnetic bearing market size was valued at USD 4.19 billion in 2024 and is expected to reach USD 8.91 billion by 2032, growing at a CAGR of 9.9% during the forecast period.

- Market growth is driven by increasing adoption of energy-efficient, low-maintenance, and high-speed bearing systems in aerospace, power generation, oil & gas, and industrial machinery.

- Key trends include advancements in active magnetic bearing control systems, integration with predictive maintenance and IoT technologies, and growing investments in renewable energy and industrial modernization.

- Competitive analysis shows that major players such as Rexnord Corporation, Brammer PLC, RBC Bearings Inc., NTN Corporation, NSK Global, HKT Bearings Ltd., JTEKT Corporation, RHP Bearings, NBI Bearings Europe, and Harbin Bearing Manufacturing Co., Ltd. focus on R&D, partnerships, and regional expansions to maintain market leadership.

- Asia Pacific is the leading region with approximately 38% of the global share, followed by North America and Europe, reflecting high demand for advanced machinery and infrastructure development.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Product Type:

In the Magnetic Bearing Market, ball bearings dominate the product type segment, accounting for the largest market share due to their precision, low friction, and suitability for high-speed operations. These bearings are widely adopted in applications requiring reduced mechanical wear and maintenance, such as turbines and compressors. Roller bearings and other specialized bearings hold smaller shares, primarily serving niche industrial applications. Growth in the ball bearings sub-segment is driven by advancements in magnetic levitation technologies and increasing adoption in high-performance machinery, which demand improved efficiency and longer operational lifespans.

- For instance, Rexnord’s Link‑Belt 200‑series unmounted ball bearing (bore 2 15/16″) offers a dynamic load rating of 15,080 lb and a static load rating of 11,100 lb — providing robust support under heavy loads while maintaining smooth operation at speeds up to 3,300 RPM.

By Distribution Channel:

Direct sales represent the dominant distribution channel, capturing the majority market share as manufacturers increasingly supply magnetic bearings directly to large industrial and OEM clients. This approach ensures customized solutions, streamlined integration, and after-sales support, enhancing client satisfaction. Indirect sales through distributors and resellers account for a smaller portion of the market, primarily serving small-to-medium enterprises or regional clients. The growth of the direct sales channel is propelled by increasing demand for tailored magnetic bearing systems in critical applications such as aerospace, energy, and industrial machinery sectors.

- For instance, Brammer PLC the company maintains more than 3.5 million individual product lines in its inventory, with over 350,000 items in stock at any given time — enabling rapid fulfillment and on‑time delivery even for specialized bearing requirements.

By End User:

The industrial machinery sector leads the end-user segment with the highest market share, driven by widespread adoption of magnetic bearings in turbines, pumps, and high-speed machinery for reduced maintenance and energy efficiency. The automotive and transportation sector is also growing steadily, particularly in high-speed rail and electric vehicle applications. Aerospace and defense, energy and power, building and construction, and electrical and electronics collectively contribute to the remaining share. The industrial machinery sub-segment’s growth is fueled by increased investment in automation, high-speed processing, and precision equipment requiring low-friction and vibration-free operations.

Key Growth Drivers

Rising Demand for High-Speed and Precision Machinery

The increasing adoption of high-speed turbines, compressors, and industrial machinery is driving demand for magnetic bearings. These bearings reduce friction, vibration, and maintenance requirements while enhancing operational efficiency. Industries such as energy, aerospace, and industrial manufacturing rely on magnetic bearings to achieve precision performance and prolonged equipment life. The shift toward automation and high-performance equipment further accelerates adoption, making this demand a primary growth driver for the market.

- For instance, NTN introduced a “Deep Groove Ball Bearing for High-Speed Servo Motors” designed for machine-tool servo motors — this bearing achieves a dmn value of 1.9 million, representing a ~40% performance boost over prior-generation bearings, and reduces vibration by approximately 50%.

Energy Efficiency and Maintenance Cost Reduction

Magnetic bearings contribute significantly to energy savings and lower lifecycle costs. Unlike conventional bearings, they eliminate mechanical contact, reducing energy losses and minimizing maintenance frequency. This efficiency is particularly valuable in sectors like power generation and industrial machinery, where operational uptime and energy optimization are critical. Rising awareness of energy-efficient solutions and cost-reduction strategies encourages companies to invest in magnetic bearings, fueling sustained market growth.

- For instance, NSK had created “high-efficiency motor bearings” that reduce energy loss: for bearings with pressed steel cages, NSK claimed a 60% reduction in energy loss compared to conventional bearings; with plastic cages, up to 80% reduction in energy loss.

Technological Advancements and Innovation

Continuous innovation in magnetic bearing designs, including hybrid and active magnetic systems, is expanding their application potential. Advances in control systems, materials, and manufacturing processes improve performance, reliability, and adaptability across sectors. Such technological progress enables integration into complex applications like high-speed motors, aerospace systems, and medical equipment, attracting investment and adoption. The emphasis on R&D and product customization remains a key growth driver, supporting broader market penetration and enhanced operational efficiency.

Key Trends & Opportunities

Expansion in Aerospace and Defense Applications

The aerospace and defense sector increasingly utilizes magnetic bearings for high-speed, precision-critical components. Their ability to operate without lubrication in extreme conditions presents significant advantages. This trend opens opportunities for market growth, particularly in advanced aircraft, satellites, and defense machinery. Continuous innovation and performance optimization in this sector offer manufacturers a chance to expand their portfolios and secure long-term contracts, reinforcing magnetic bearings’ strategic relevance.

- For instance, JTEKT also built a magnetic-bearing evaluation rig that reliably tests rotor speeds up to 45,000 min⁻¹ (dmn ≈ 2.7 million) and supports rapid acceleration rates up to 15,000 min⁻¹/s, enabling validation under extreme dynamic profiles required for aircraft and space components.

Integration with Renewable Energy Systems

Magnetic bearings are gaining traction in renewable energy applications, including wind turbines and hydropower generators. Their low-friction design enhances energy efficiency and reliability, critical for sustainable power generation. As governments and industries focus on renewable adoption, magnetic bearings present a valuable opportunity for deployment in high-performance, low-maintenance energy systems. Manufacturers can leverage this trend to innovate energy-specific solutions, catering to the growing demand for environmentally friendly and durable bearing technologies.

- For instance, NBI Bearings Europe Oquendo (Spain) plant with CNC grinders and an Aichelin heat-treatment line across a 2,500 m² production area (5,500 m² total site), supporting in-house metallography and metrology labs.

Adoption in Electric Vehicles and Transportation

The rising focus on electric and high-speed transportation is creating new applications for magnetic bearings. In electric motors and high-speed rail systems, they reduce mechanical wear and improve efficiency. This trend is expected to expand as automakers prioritize lightweight, low-maintenance, and high-performance components, providing manufacturers with a growing market opportunity to develop specialized magnetic bearing solutions.

Key Challenges

High Initial Investment and Implementation Costs

Magnetic bearings require significant upfront investment in advanced materials, control systems, and integration processes. High costs can deter small and medium enterprises from adopting these solutions, limiting widespread deployment. While long-term benefits include maintenance reduction and energy savings, the initial expenditure remains a barrier, especially in cost-sensitive industries. Manufacturers must develop cost-effective designs and financing options to overcome this challenge and expand market adoption.

Complex System Integration and Technical Expertise Requirements

Implementing magnetic bearings demands specialized knowledge in design, control systems, and monitoring. Integration into existing machinery can be technically challenging, requiring skilled personnel and advanced infrastructure. Limited technical expertise in certain regions and industries may slow adoption, particularly for small-scale applications. Addressing this challenge involves training, technical support, and standardized solutions to ensure smooth integration and reliable performance, critical for broader market acceptance.

Regional Analysis

North America

North America holds approximately 35% of the global magnetic bearing market, making it a key region for industry growth. The market is driven by advanced industrial infrastructure, the presence of leading manufacturers, and high adoption in aerospace, oil & gas, and power generation sectors. Companies in the U.S. and Canada are focusing on high-speed compressors, turbines, and renewable energy applications, leveraging magnetic bearings for their energy efficiency, low maintenance, and reduced downtime. Technological innovation, such as integration with advanced control systems and real-time monitoring, further strengthens regional demand, positioning North America as both a market leader and technology innovator.

Asia Pacific

Asia Pacific accounts for around 38% of the global magnetic bearing market and is the fastest-growing region. Growth is fueled by rapid industrialization, expansion of power generation, and rising demand in automotive, heavy machinery, and renewable energy sectors in countries such as China, India, Japan, and South Korea. Leading manufacturers are investing heavily in local production and R&D to cater to rising energy efficiency requirements and high-speed machinery applications. The region’s focus on infrastructure development and modernization, combined with large-scale adoption of advanced turbomachinery, is expected to sustain strong growth and gradually increase market share over the next decade.

Europe

Europe represents about 26% of the global magnetic bearing market, supported by well-established industrial and energy sectors. Strict environmental regulations and the push for energy-efficient technologies have accelerated adoption in power generation, industrial automation, and manufacturing processes. Key European countries, including Germany, France, and the U.K., are investing in high-speed machinery that requires low-maintenance, high-performance magnetic bearings. The market benefits from strong technological innovation, including active magnetic bearing control systems and integration with predictive maintenance tools. Europe’s strategic focus on sustainability and reliability ensures steady demand and positions the region as a major hub for advanced bearing solutions.

Latin America

Latin America accounts for roughly 7–8% of the global magnetic bearing market, reflecting a growing but smaller regional presence. Industrial modernization, expanding infrastructure, and rising energy demands are key drivers for adoption in countries such as Brazil and Mexico. Magnetic bearings are increasingly being used in manufacturing, power generation, and industrial machinery to enhance equipment reliability, reduce maintenance costs, and support energy efficiency initiatives. Despite slower adoption compared to North America and Asia Pacific, investment in industrial upgrades and renewable energy projects is expected to create steady growth opportunities, gradually expanding the market share for magnetic bearing solutions in the region.

Middle East & Africa (MEA)

The MEA region holds approximately 6% of the global magnetic bearing market. The demand is primarily driven by oil & gas, petrochemical, and power generation industries, where magnetic bearings offer reliability, reduced maintenance, and improved operational efficiency in harsh environments. Countries such as Saudi Arabia, UAE, and South Africa are investing in industrial and energy infrastructure, creating opportunities for advanced bearing solutions. Additionally, the region is witnessing growing adoption of high-speed machinery and renewable energy projects, which require low-maintenance and energy-efficient solutions. This positions MEA for gradual but steady growth, with an increasing role in the global magnetic bearing market.

Market Segmentations:

By Product Type:

- Ball bearings

- Roller bearings

By Distribution Channel:

- Direct sales

- Indirect sales

By End User:

- Automotive and transportation

- Building and construction

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The magnetic bearing market include Rexnord Corporation, Brammer PLC, RBC Bearings Inc., NTN Corporation, NSK Global, HKT Bearings Ltd., JTEKT Corporation, RHP Bearings, NBI Bearings Europe, and Harbin Bearing Manufacturing Co., Ltd. The magnetic bearing market is highly competitive, driven by continuous technological innovation and increasing demand for energy-efficient, low-maintenance solutions. Companies focus on developing high-speed, contactless bearing systems for industries such as aerospace, power generation, oil & gas, and industrial machinery. Innovation in active magnetic bearing control systems, predictive maintenance, and integration with IoT-enabled monitoring is shaping market dynamics. Strategic initiatives such as partnerships, mergers, and regional expansions are commonly pursued to strengthen market presence. Additionally, emphasis on performance optimization, reliability, and customer support enhances competitiveness. The growing preference for sustainable and high-efficiency machinery encourages players to invest in advanced designs, fostering differentiation and maintaining a dynamic market environment that responds to evolving industrial and regulatory requirements.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Rexnord Corporation

- Brammer PLC

- RBC Bearings Inc.

- NTN Corporation

- NSK Global

- HKT Bearings Ltd.

- JTEKT Corporation

- RHP Bearings

- NBI Bearings Europe

- Harbin Bearing Manufacturing Co., Ltd.

Recent Developments

- In September 2025, Neo Performance Materials (NEO), has initiated production at its sintered rare earth magnet facility in Estonia, with an annual capacity of 2,000 tonnes. This development is expected to strengthen the supply chain and drive growth in the magnetic materials market.

- In May 2025, Schaeffler announced to open a manufacturing plant in Shoolagiri, Tamil Nadu, India. This production facility is inaugurated to develop a wide range of high-tech bearings for end-user industries.

- In October 2024, Arnold Magnetic Technologies opened a new manufacturing facility in Thailand to increase its production of high-reliability magnetic components. This expansion is a strategic move to boost the company’s market position and capitalize on growth in the magnetic materials sector.

- In February 2024, NTN Corporation supplied bearings for the H3 launch vehicle’s engine turbo pumps, which are designed for high-speed rotation in cryogenic conditions. These bearings feature a proprietary solid lubricant for performance at low temperatures and a reinforced fiberglass retainer to handle the high centrifugal forces of the ultra-high speed rotation

Report Coverage

The research report offers an in-depth analysis based on Product Type, Distribution Channel, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Adoption of magnetic bearings is expected to increase in aerospace, power generation, and industrial machinery.

- Demand for energy-efficient and low-maintenance machinery will drive market growth.

- Technological advancements in active magnetic bearing control systems will enhance performance and reliability.

- Integration with IoT and predictive maintenance solutions will gain wider acceptance.

- Expansion in renewable energy projects will create new opportunities for magnetic bearing applications.

- Emerging economies will increasingly invest in industrial modernization, boosting regional demand.

- Growth in high-speed compressors, turbines, and pumps will support market expansion.

- Companies will focus on R&D to develop lightweight, high-performance, and contactless bearing solutions.

- Strategic partnerships, collaborations, and regional expansions will continue to shape the competitive landscape.

- Rising awareness of sustainable and environmentally friendly machinery will reinforce the adoption of magnetic bearings.