Market Overview

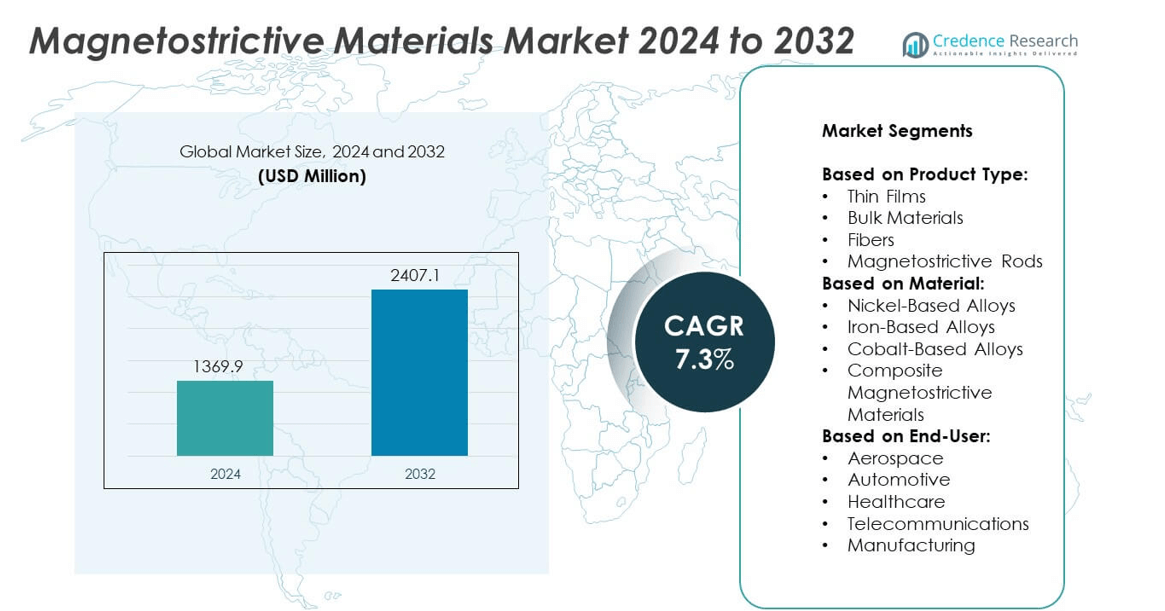

The Magnetostrictive Materials Market size was valued at USD 1369.9 million in 2024 and is anticipated to reach USD 2407.1 million by 2032, growing at a CAGR of 7.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Magnetostrictive Materials Market Size 2024 |

USD 1369.9 million |

| Magnetostrictive Materials Market, CAGR |

7.3% |

| Magnetostrictive Materials Market Size 2032 |

USD 2407.1 million |

The Magnetostrictive Materials market advances through rising demand in industrial automation, defense systems, and precision medical devices. It supports high-performance sensing and actuation across harsh environments where durability and responsiveness are critical. Key drivers include the expansion of smart infrastructure, increased use in sonar and aerospace applications, and adoption in minimally invasive surgical tools. Market trends highlight integration into compact mechatronic systems, hybrid actuator technologies, and wireless energy harvesting.

The Magnetostrictive Materials market demonstrates strong growth across North America, Europe, and Asia-Pacific, supported by industrial automation, defense modernization, and advanced manufacturing. North America leads in technology development and military applications, while Europe emphasizes automotive innovation and precision engineering. Asia-Pacific shows rapid adoption due to expanding infrastructure and electronics manufacturing. Key players shaping this market include TDK Corporation, known for its precision components; Metglas, Inc., a specialist in magnetostrictive alloys; and KYOCERA Corporation, which offers integrated material solutions. LORD Corporation also contributes through vibration control and sensing systems, enhancing the material’s industrial and aerospace applications.

Market Insights

- The Magnetostrictive Materials market was valued at USD 1369.9 million in 2024 and is projected to reach USD 2407.1 million by 2032, growing at a CAGR of 7.3% during the forecast period.

- Increasing demand for high-precision actuators and sensors in robotics, aerospace, and industrial automation is a key driver boosting the adoption of magnetostrictive materials.

- Integration of hybrid actuation systems, miniaturized sensor components, and wireless energy harvesting technologies are shaping the ongoing market trends.

- Manufacturers such as TDK Corporation, KYOCERA Corporation, Metglas, Inc., and LORD Corporation focus on product innovation and strategic collaborations to strengthen their market presence.

- High production costs and dependence on rare-earth elements such as terbium and dysprosium act as major restraints, limiting large-scale adoption in cost-sensitive applications.

- North America leads the global market due to strong investments in defense, healthcare, and automation, followed by Europe with rising demand from the automotive and industrial sectors.

- Asia-Pacific continues to emerge as a high-potential region with expanding infrastructure, defense upgrades, and electronics manufacturing driving magnetostrictive material consumption.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Growing Use in Advanced Sensors for Industrial Automation and Robotics

The Magnetostrictive Materials market benefits from rising demand for high-precision sensors in manufacturing and process automation. Industries rely on these materials for their ability to convert magnetic energy into mechanical motion with exceptional responsiveness. It supports critical functions such as position sensing, torque measurement, and force detection in robotic systems and CNC machinery. Industrial automation trends require sensor solutions that offer durability in harsh environments, which magnetostrictive materials fulfill efficiently. Increasing investments in smart factories further accelerate sensor adoption. The market continues to gain from this push toward intelligent monitoring and motion control.

- For instance, TDK’s TAS8240 angle sensor achieves an accuracy of ±1.0° across a −40 °C to +150 °C range in a compact 3 × 3 mm² package.

Rising Adoption in Defense and Aerospace Applications for Precision Control

Defense and aerospace sectors increasingly incorporate magnetostrictive materials to achieve superior control and stability in actuators and vibration damping systems. It enables adaptive control in aircraft wings, missile guidance systems, and naval sonar equipment. Military-grade requirements for high-reliability and rugged materials favor magnetostrictive alloys such as Terfenol-D. Governments support research on advanced defense technologies that improve real-time response and noise suppression. These materials also meet size and weight constraints in aerospace components without compromising performance. The Magnetostrictive Materials market gains long-term growth momentum from strategic defense investments.

- For instance, Terfenol-D, a giant magnetostrictive alloy, can undergo a shape change of approximately 2,000 microstrains when subjected to a magnetic field of 160 kA/m, according to materials science publications. This large deformation in response to a magnetic field is a key property of Terfenol-D and makes it useful in various applications.

Expanding Demand from Healthcare Sector for High-Performance Medical Devices

Medical equipment manufacturers use magnetostrictive materials in surgical tools, ultrasound transducers, and implantable devices requiring micro-motion precision. It offers excellent response speed, miniaturization capability, and biocompatibility in certain formulations. With aging populations and rising healthcare expenditure, demand for high-resolution diagnostics and minimally invasive procedures is growing. Magnetostrictive actuators ensure repeatable motion control in robotic surgery platforms and diagnostic imaging. Hospitals and research institutions prioritize equipment with higher accuracy and longer service life. The Magnetostrictive Materials market remains vital to innovation in next-generation healthcare solutions.

Integration in Energy Harvesting and Structural Health Monitoring Systems

Energy infrastructure and civil engineering projects increasingly deploy magnetostrictive materials for condition monitoring and energy harvesting. It plays a role in transforming ambient vibrations into usable energy and capturing data on stress or fatigue in bridges, turbines, and pipelines. Magnetostrictive sensors improve asset safety and operational efficiency by detecting early signs of structural degradation. Power plants and transportation networks use these systems to avoid costly downtimes. Smart infrastructure initiatives rely on self-powered sensor networks, where magnetostrictive components reduce maintenance needs. The Magnetostrictive Materials market supports the shift toward predictive maintenance and sustainable infrastructure design.

Market Trends

Increasing Integration of Magnetostrictive Actuators in Compact Mechatronic Systems

Miniaturization trends across electronics and electromechanical systems are driving the adoption of compact, high-force actuators based on magnetostrictive materials. It enables efficient displacement and vibration control in confined spaces without mechanical complexity. Consumer electronics, precision tools, and lab automation devices now incorporate these actuators for improved responsiveness and silent operation. The Magnetostrictive Materials market aligns with industries seeking lightweight and compact alternatives to traditional hydraulic or piezoelectric systems. Advancements in material engineering enhance performance under varied environmental conditions. Manufacturers are optimizing design integration for faster, quieter actuation in multifunctional systems.

- For instance, Metglas 2605SC, when in a thin-ribbon form, exhibits a saturation magnetostrictive coefficient of approximately 27 ppm. This material is known for its magnetic softness and high elastic modulus, making it suitable for detecting strain in low magnetic field strengths.

Wider Adoption of Magnetostrictive Sensors in Structural Monitoring of Smart Infrastructure

Infrastructure operators are increasingly embedding magnetostrictive sensors into critical assets such as bridges, tunnels, and dams. It enables real-time monitoring of strain, stress, and fatigue for structural health assessments. The growing shift toward smart cities requires predictive maintenance tools that improve safety and reduce manual inspections. The Magnetostrictive Materials market reflects this trend with expanding use in self-powered sensing systems and wireless monitoring networks. These materials offer long service life, stable output, and immunity to electromagnetic interference. Engineers favor them in inaccessible or safety-critical zones where reliability is essential.

- For instance, a dual‑use magnetostrictive device using a Galfenol rod generated 30.3 mJ in one hour while precisely detecting a bridge’s natural frequency under intermittent traffic loading, enabling structural diagnostics at least once every two days.

Growing Focus on Material Customization for Extreme-Environment Applications

Researchers and manufacturers are tailoring magnetostrictive material compositions to withstand corrosive, high-temperature, and high-pressure environments. It supports use in deep-sea exploration, geothermal drilling, and nuclear instrumentation. Performance enhancements in thermal stability, magneto-mechanical coupling, and fatigue resistance are leading trends. The Magnetostrictive Materials market benefits from demand in sectors where conventional materials fail to deliver consistency. Defense and energy industries continue to test alloy variations like Galfenol and Terfenol-D in extreme scenarios. Material innovation enables niche applications with strong commercial viability.

Emergence of Hybrid Systems Combining Magnetostrictive and Piezoelectric Technologies

Hybrid actuator and sensor systems are gaining attention for their ability to combine the benefits of magnetostrictive and piezoelectric materials. It enhances frequency response, control accuracy, and energy efficiency in complex electromechanical applications. Developers are leveraging magnetostrictive elements for coarse motion and piezo components for fine adjustments. The Magnetostrictive Materials market supports this evolution through component-level integration in advanced robotics, aerospace control systems, and haptic interfaces. Hybrid designs reduce system noise and power losses while enabling compact form factors. This trend is shaping next-generation motion control strategies.

Market Challenges Analysis

High Material Cost and Limited Availability of Rare-Earth Elements

The reliance on rare-earth elements such as terbium and dysprosium significantly increases the production cost of magnetostrictive materials. It restricts large-scale adoption in cost-sensitive applications despite technical advantages. Global supply constraints and geopolitical dependencies impact pricing and raw material accessibility. Manufacturers face difficulty in maintaining stable procurement channels and managing long-term cost efficiency. The Magnetostrictive Materials market encounters procurement delays when raw material exports fluctuate due to trade policies or regional instability. Price-sensitive industries often hesitate to adopt these materials when affordable alternatives are available.

Complex Fabrication Processes and Integration Barriers in Legacy Systems

Magnetostrictive components require precise fabrication methods and controlled processing conditions to achieve consistent performance. It increases the initial investment for manufacturers and deters smaller players from entering the market. Integration challenges arise when adapting magnetostrictive actuators or sensors to existing mechanical or electronic architectures. Legacy systems in industrial and infrastructure settings often lack compatibility with newer materials. The Magnetostrictive Materials market faces resistance where design changes require complete overhauls or significant engineering resources. Adoption slows when integration raises concerns over long-term reliability, calibration complexity, or electromagnetic interference.

Market Opportunities

Emerging Use in Wireless Energy Transfer and Self-Powered Sensing Systems

Advances in wireless energy transfer and self-powered systems open new application avenues for magnetostrictive materials. It supports energy harvesting from mechanical vibrations to power remote sensors and low-energy devices in industrial and infrastructure settings. Developers are exploring magnetostrictive transducers for contactless energy delivery in rotating machinery and sealed environments. The Magnetostrictive Materials market stands to gain from demand in off-grid sensing, condition monitoring, and maintenance-free electronics. These applications require robust materials that operate without external power or frequent maintenance. Research institutions and OEMs are investing in scalable solutions for harsh and remote conditions.

Potential in Automotive Sector for Smart Mobility and Active Noise Control

Automotive manufacturers are examining magnetostrictive materials for applications in active noise and vibration control, adaptive suspension systems, and intelligent braking. It enables fast response times, compact designs, and precision actuation critical to electric and autonomous vehicle platforms. The shift toward smart mobility requires embedded systems capable of real-time adjustment to road and driver conditions. The Magnetostrictive Materials market presents growth potential in components that improve ride comfort, safety, and energy efficiency. Integration in EVs and next-generation vehicle platforms offers long-term scalability. Partnerships between material developers and Tier 1 suppliers continue to expand these opportunities.

Market Segmentation Analysis:

By Product Type:

Thin films lead the adoption in microelectromechanical systems (MEMS), sensors, and actuators due to their compatibility with compact electronics and fast magnetic response. Bulk materials maintain steady demand across heavy-duty applications in industrial automation and defense systems where high force output and durability are essential. Fibers are emerging in lightweight sensing and smart textile applications, offering flexibility and magneto-mechanical efficiency. Magnetostrictive rods dominate in displacement sensing, linear actuators, and energy harvesting devices. The Magnetostrictive Materials market supports a broad range of form factors to address specific mechanical, size, and force requirements across industries.

- For instance, TDK’s compact thin-film xMR sensor measures just 8 × 8 × 5 mm and detects metallic foreign particles under 100 µm in size on manufacturing lines, enhancing contamination control in pharmaceuticals and batteries.

By Material:

Nickel-based alloys offer good magnetostriction properties and corrosion resistance, making them suitable for general-purpose applications in telecommunications and automotive sectors. Iron-based alloys, especially Terfenol-D, deliver high magnetostrictive strain and are preferred in sonar systems, actuators, and vibration control devices. Cobalt-based alloys provide enhanced thermal stability and are used in aerospace and high-temperature environments. Composite magnetostrictive materials combine metal and polymer properties to balance flexibility, responsiveness, and mechanical strength. It enhances customization options for engineers developing next-generation devices with strict performance criteria. The market continues to evolve with improved alloy compositions and hybrid structures.

- For instance, ETREMA Products, Inc.’s Terfenol-D maintains magnetostrictive performance exceeding 1,000 ppm from room temperature up to 200°C due to its high Curie temperature of 380°C. This means that the material’s ability to change shape or size in response to a magnetic field remains strong within this temperature range. The Curie temperature is the point at which a ferromagnetic material loses its permanent magnetic properties and transitions to a paramagnetic state.

By End-User:

Aerospace applications rely on magnetostrictive materials for vibration control, active noise suppression, and precision actuators in flight systems. Automotive manufacturers adopt them for adaptive suspension, engine mount systems, and cabin noise cancellation, especially in electric and autonomous vehicles. Healthcare sector uses them in ultrasonic transducers, surgical tools, and implantable devices requiring micro-motion accuracy. Telecommunications benefit from these materials in RF filters, signal processing, and vibration-sensitive communication systems. The Magnetostrictive Materials market finds strong penetration in the manufacturing sector, where it improves motion control, robotic systems, and non-destructive testing equipment. Each end-user sector demands specific material properties aligned with performance, reliability, and environmental resilience.

Segments:

Based on Product Type:

- Thin Films

- Bulk Materials

- Fibers

- Magnetostrictive Rods

Based on Material:

- Nickel-Based Alloys

- Iron-Based Alloys

- Cobalt-Based Alloys

- Composite Magnetostrictive Materials

Based on End-User:

- Aerospace

- Automotive

- Healthcare

- Telecommunications

- Manufacturing

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America accounts for 33.2% of the global Magnetostrictive Materials market, driven by strong demand across defense, aerospace, and industrial automation sectors. The United States leads regional consumption due to extensive R&D investments in smart materials, military-grade actuators, and energy-efficient systems. Government-funded defense projects and collaborations with private sector innovators have accelerated the deployment of magnetostrictive components in sonar systems, vibration dampers, and missile control systems. Manufacturing companies across the region integrate these materials into robotics, non-destructive testing systems, and industrial sensors to enhance operational precision and durability. The healthcare sector also contributes to market expansion through the development of advanced surgical tools and imaging systems. Canada supports regional growth with investments in aerospace innovation and sensor-based structural monitoring systems in critical infrastructure. The presence of leading research institutions and a robust industrial base further reinforces North America’s leadership in technological adoption and commercialization.

Europe

Europe holds 27.6% of the global market, supported by growing applications in automotive, manufacturing, and renewable energy sectors. Countries such as Germany, France, and the United Kingdom deploy magnetostrictive sensors in automation systems, EV platforms, and active suspension systems to enhance performance and passenger comfort. The region’s strong automotive industry is adopting advanced vibration control technologies to meet noise reduction regulations and improve electric vehicle ride quality. Magnetostrictive actuators and rods are also being integrated into wind turbines and structural health monitoring systems across the energy sector. EU-funded initiatives are supporting material innovation and sustainable industrial design. Research centers across Scandinavia and Central Europe are driving collaboration between academia and private enterprises for smart sensing technologies. It maintains consistent growth due to regulatory support, innovation incentives, and expanding use of adaptive materials in precision systems.

Asia-Pacific

Asia-Pacific captures 24.1% of the Magnetostrictive Materials market, driven by rapid industrialization, infrastructure development, and defense modernization. China leads regional growth with large-scale investments in aerospace, telecommunications, and railway safety systems. Magnetostrictive materials are increasingly used in sensor arrays, structural monitoring of high-speed rail networks, and military-grade actuators. Japan and South Korea contribute through high-performance electronics and precision manufacturing, integrating magnetostrictive components in compact sensors and automation tools. India’s market is growing steadily, supported by defense procurement programs and smart infrastructure projects using sensor-driven monitoring solutions. Regional demand benefits from strong domestic manufacturing bases, low production costs, and a skilled technical workforce. Asia-Pacific remains a dynamic region with substantial potential for new application development and export-oriented material production.

Latin America

Latin America represents 8.4% of the global market, primarily supported by industrial and automotive sector needs in Brazil, Mexico, and Argentina. Regional manufacturers are incorporating magnetostrictive sensors into process automation, powertrain systems, and smart assembly lines to improve efficiency and reduce downtime. The healthcare sector in Brazil is exploring magnetostrictive materials for use in diagnostic tools and therapeutic devices. Telecommunications and energy sectors are investing in sensor-based systems to ensure performance monitoring of remote assets. Despite limited R&D infrastructure, Latin America shows rising interest in adopting magnetostrictive technologies to modernize its industrial base. It offers moderate growth driven by import reliance and gradual integration of advanced materials in high-value sectors.

Middle East & Africa

The Middle East & Africa account for 6.7% of the global Magnetostrictive Materials market, with growing opportunities in oil & gas, infrastructure monitoring, and defense sectors. Countries such as the UAE and Saudi Arabia are deploying smart sensing technologies in energy facilities, pipelines, and high-rise construction projects. Magnetostrictive sensors offer long operational life, resistance to harsh environments, and real-time data output, making them suitable for asset monitoring in remote or extreme locations. South Africa shows potential in mining and industrial automation applications. Defense modernization and investments in advanced materials research are limited but expanding in Gulf countries through international partnerships. While adoption is still in early phases, the region presents niche opportunities in critical infrastructure and energy domains where durability and reliability are essential.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Competitive Analysis

The Magnetostrictive Materials market features a concentrated competitive landscape led by TDK Corporation, Metglas, Inc., KYOCERA Corporation, LORD Corporation, Emerson Electric, and Advanced Cerametrics. These companies maintain strong market positions through specialized product lines, technical expertise, and global distribution networks. Each focuses on advancing material performance, optimizing actuation efficiency, and expanding applications across high-growth sectors such as aerospace, medical, and industrial automation. Players prioritize R&D investments to enhance magnetic strain properties, reduce energy losses, and improve thermal stability of magnetostrictive alloys. Strategic collaborations with defense contractors, electronics manufacturers, and research institutions support rapid innovation cycles and broaden end-use reach. Companies actively seek differentiation through proprietary alloy formulations, integration capabilities, and miniaturized sensor technologies. Competitive focus also includes developing solutions for extreme environments and expanding presence in emerging economies. Leading firms align their offerings with evolving customer demands in noise control, precision sensing, and structural health monitoring. Market leaders emphasize high reliability, operational longevity, and compliance with international performance standards to maintain a competitive edge. The industry sees moderate entry barriers due to technical complexity, high raw material costs, and long validation cycles. Competitive dynamics continue to evolve as global players adapt to application-specific needs and advance scalable production capabilities for next-generation magnetostrictive systems.

Recent Developments

- In May 2025, TDK Corporation was selected as an SX Brand 2025 by Japan s Ministry of Economy, Trade and Industry (METI) and the Tokyo Stock Exchange, recognizing its strides in sustainability transformation.

- In December 2024, The Althen sensor and control announced the launch of the latest selection of flow meter and control switch. These new products are designed to increase the accuracy and efficiency of measurement and controlling fluid currents in different industrial applications. The company aims to integrate the state art technology into the offers and address the growing demand for advanced flow measurement.

- In May 2024, NSK Ltd. developed a practical magnetostrictive torque sensor (3rd-generation sensor) for automobiles which provides many benefits like comfortable ride, failure prediction, extension of driving mileage and performance improvement owing to its weight-reducing and space-saving features, while also shortening the development period.

Market Concentration & Characteristics

The Magnetostrictive Materials market displays moderate concentration, with a few established players dominating global supply and technology development. It is characterized by high specialization, driven by technical complexity, proprietary material formulations, and performance-critical end-use requirements. Key manufacturers operate in niche segments such as defense-grade actuators, precision medical tools, and industrial automation systems. The market emphasizes low-volume, high-value production tailored to specific application demands. Entry barriers remain high due to the need for advanced processing capabilities, rare-earth material access, and extensive validation cycles. Product differentiation centers around thermal stability, magnetic strain efficiency, and integration compatibility. Innovation cycles are shaped by end-user collaboration and material performance testing under extreme conditions. Companies prioritize long-term contracts, R&D partnerships, and cross-sector applicability to maintain competitiveness. It evolves steadily with growing interest in hybrid systems, energy harvesting, and compact mechatronic components. The Magnetostrictive Materials market relies on continuous improvements in alloy engineering and system-level integration to meet the changing expectations of aerospace, automotive, and industrial users.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Material, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for magnetostrictive materials will rise with the expansion of industrial automation and precision manufacturing.

- Defense and aerospace sectors will continue to adopt advanced actuators and sensors requiring high magnetic responsiveness.

- Medical device manufacturers will increase usage in surgical tools, diagnostic equipment, and implantable systems.

- Smart infrastructure projects will drive integration of magnetostrictive sensors for real-time structural health monitoring.

- Energy harvesting applications will open new opportunities in remote sensing and low-power electronics.

- Automotive industry will adopt these materials in active noise control, adaptive suspension, and electric vehicle platforms.

- Research will focus on developing cost-effective alloys with reduced reliance on rare-earth elements.

- Miniaturization and integration into hybrid systems will enhance use in compact electronics and robotics.

- Emerging economies will contribute to demand through investments in defense, manufacturing, and smart cities.

- Strategic collaborations between OEMs, material developers, and research institutions will accelerate innovation and scalability.