MS Polymers Market Overview:

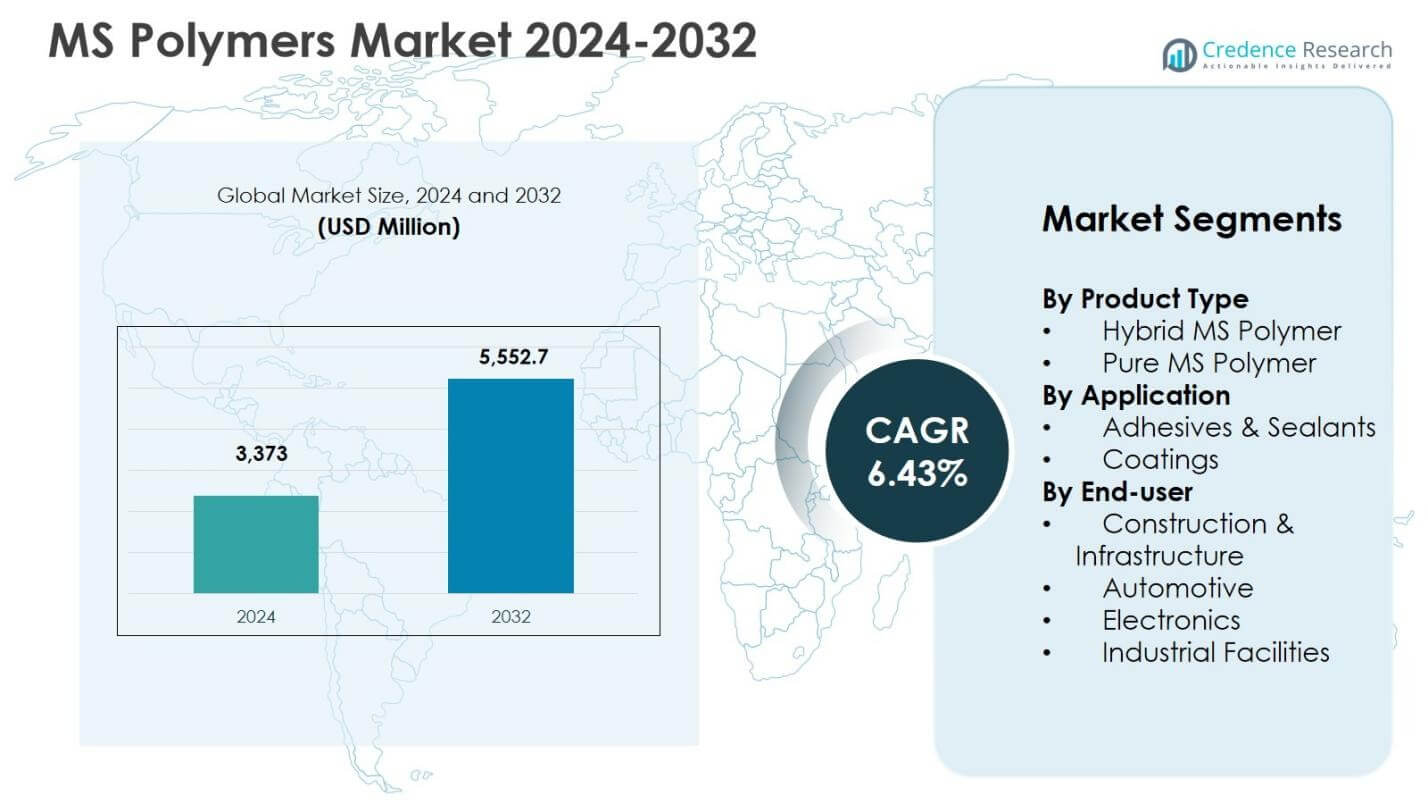

MS Polymers Market size was valued at USD 3,373 million in 2024 and is anticipated to reach USD 5,552.7 million by 2032, at a CAGR of 6.43% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| MS Polymers Market Size 2024 |

USD 3,373 million |

| MS Polymers Market, CAGR |

6.43% |

| MS Polymers Market Size 2032 |

USD 5,552.7 million |

MS Polymers Market Insights

- Market growth is driven by rising adoption of low-VOC and solvent-free materials, with Hybrid MS Polymer leading the product segment at a 64.8% share in 2024 due to cost efficiency, balanced performance, and broad application compatibility.

- Key market trends include increased use of MS polymers in adhesives and sealants, which dominated applications with a 71.6% share in 2024, alongside growing focus on high-performance hybrid formulations and sustainable construction materials.

- Market restraints include higher costs compared to conventional adhesive technologies and limited technical awareness in developing regions, which can slow adoption despite performance and durability advantages.

- Regionally, Europe led the market with a 31.6% share in 2024, followed by North America at 28.4% and Asia Pacific at 26.9%, while Construction & Infrastructure remained the largest end-user segment with a 58.9% share.

MS Polymers Market Segmentation Analysis:

By Product Type:

The MS Polymers market by product type is led by Hybrid MS Polymer, which accounted for 64.8% market share in 2024, driven by its balanced performance characteristics, cost efficiency, and broad compatibility with fillers, plasticizers, and additives. Hybrid variants offer improved adhesion, elasticity, and weather resistance, making them suitable for construction and industrial sealing applications. Pure MS Polymer held 35.2% share, supported by demand for solvent-free, low-VOC, and high-durability solutions in premium applications. Growth across both segments is driven by tightening environmental regulations and rising adoption of sustainable polymer technologies.

- For instance, Kaneka MS Polymer, an isocyanate-free STPE base resin, delivers high durability, good weatherability, and paint compatibility for building joints and tile bonding.

By Application:

In terms of application, Adhesives & Sealants dominated the MS Polymers market with a 71.6% share in 2024, supported by extensive use in bonding, sealing, and gap-filling across construction, automotive, and industrial assemblies. Strong adhesion to diverse substrates, flexibility, and resistance to moisture and UV exposure drive demand in this segment. Coatings accounted for 28.4% share, benefiting from growing use in protective and decorative surfaces requiring elasticity and chemical resistance. Increasing infrastructure activity and replacement of solvent-based chemistries continue to strengthen application-level demand.

- For instance, Sika’s Sikaflex®-127 hybrid sealant bonds window and door frames to concrete, masonry, and metals, providing elastic, moisture-curing performance for interior and exterior connection joints.

By End-user:

The Construction & Infrastructure segment led the MS Polymers market with a 58.9% share in 2024, driven by large-scale use in sealants, flooring, glazing, and façade systems. Rising urbanization and green building adoption support sustained demand. Automotive held 21.7% share, supported by lightweight bonding, vibration damping, and interior applications. Industrial Facilities accounted for 12.4%, driven by maintenance and equipment sealing needs, while Electronics captured 7.0%, supported by precision bonding and insulation requirements. Performance durability and regulatory compliance remain key end-user drivers.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Key Growth Drivers

Rising Demand for Sustainable and Low-VOC Materials

The MS Polymers market is strongly driven by the increasing adoption of sustainable, solvent-free, and low-VOC materials across construction, automotive, and industrial sectors. MS polymers meet stringent environmental and workplace safety regulations while delivering strong adhesion, elasticity, and weather resistance. Growing emphasis on green building certifications and environmentally responsible manufacturing practices is accelerating the shift away from solvent-based adhesives and sealants. Additionally, rising awareness of indoor air quality and long-term material durability is reinforcing demand, particularly in residential, commercial, and infrastructure applications where regulatory compliance and performance consistency are critical.

- For instance, SABA applies Sabatack® MS polymers to bond and seal cabins, trailers, windows, side panels, and sandwich panels in trucks, buses, and railway cars. The adhesives provide elastic bonds with high weather resistance, outperforming traditional systems in vibration-heavy environments.

Expansion of Global Construction and Infrastructure Development

Rapid urbanization and large-scale infrastructure development are key drivers supporting MS polymer consumption. These materials are extensively used in sealing, bonding, glazing, flooring, and façade applications due to their flexibility, moisture resistance, and long service life. Investments in smart cities, transportation networks, and energy-efficient buildings are increasing product penetration. MS polymers’ ability to adhere to multiple substrates and perform reliably under varying climatic conditions enhances their suitability for complex construction environments, strengthening their role as preferred materials in modern infrastructure projects.

- For instance, 3M deploys advanced MS polymers in building construction. These provide superior adhesion and chemical resistance for applications like window installation and joint sealing, ensuring durability in exterior joinery under varying weather.

Growing Automotive Lightweighting and Advanced Assembly Needs

The automotive industry’s focus on lightweighting, durability, and improved assembly efficiency is accelerating the adoption of MS polymers. These materials enable strong bonding of dissimilar substrates, reduce reliance on mechanical fasteners, and enhance vibration damping and corrosion protection. Increasing production of electric vehicles further supports demand, as manufacturers seek advanced adhesive and sealing solutions to improve energy efficiency and structural integrity. MS polymers also contribute to improved vehicle aesthetics and long-term reliability, reinforcing their importance in next-generation automotive design and manufacturing.

Key Trends & Opportunities

Shift Toward High-Performance and Hybrid MS Polymer Formulations

A prominent trend in the MS Polymers market is the development of high-performance hybrid formulations that balance cost efficiency with enhanced mechanical and chemical properties. Manufacturers are focusing on faster curing, improved adhesion strength, and greater resistance to temperature fluctuations and chemicals. These advancements support broader adoption across industrial maintenance, transportation, and prefabricated construction. Product differentiation through customized formulations tailored to specific applications and environmental conditions presents significant growth opportunities for suppliers targeting premium and specialized end-use segments.

- For instance, Kaneka’s SAX500 series MS Polymers provide faster curing and quick strength build-up alongside excellent adhesion to plastics, metals, and woods. These formulations enable lower modulus for tougher performance without brittleness, supporting applications in transportation and construction.

Rising Adoption in Emerging and Non-Traditional Applications

MS polymers are gaining traction in emerging applications such as renewable energy installations, modular construction systems, and advanced electronics assembly. Their resistance to UV exposure, moisture, and thermal stress makes them suitable for solar panel sealing, wind energy components, and electronic encapsulation. Industrial facilities increasingly adopt MS polymer-based solutions for maintenance and repair due to ease of application and durability. This expanding application scope creates new revenue streams and supports long-term market diversification beyond traditional construction and automotive uses.

- For instance, Henkel’s TEROSON MS 930, a silane-modified polymer sealant, provides primerless adhesion and excellent UV/weather resistance for solar panel assemblies and exterior sealing.

Key Challenges

Higher Cost Compared to Conventional Adhesive Technologies

One of the primary challenges facing the MS Polymers market is the higher cost of MS polymer formulations compared to conventional polyurethane, silicone, and acrylic-based alternatives. Price sensitivity among small and mid-scale manufacturers, particularly in emerging economies, can limit adoption despite superior performance benefits. Cost pressures in large construction and industrial projects may encourage continued use of lower-priced materials, slowing penetration. Addressing this challenge requires economies of scale, formulation optimization, and clearer communication of lifecycle cost advantages.

Limited Awareness and Technical Familiarity in Developing Markets

Limited awareness and technical familiarity with MS polymer technology remain challenges in several developing regions. End users and applicators often rely on traditional materials due to established usage practices and limited technical training. Inadequate knowledge regarding application techniques, curing behavior, and long-term performance can hinder adoption. Market players must invest in education, training programs, and demonstration projects to improve acceptance. Strengthening distribution networks and technical support capabilities is essential to overcoming this barrier and unlocking growth potential in underserved markets.

Regional Analysis

North America

North America accounted for 28.4% of the MS Polymers market share in 2024, driven by strong demand from construction, automotive, and industrial maintenance applications. The region benefits from strict VOC regulations and widespread adoption of sustainable building materials, supporting the replacement of solvent-based adhesives and sealants. High renovation activity, commercial infrastructure upgrades, and advanced automotive manufacturing further strengthen demand. The presence of established manufacturers, robust distribution networks, and strong technical awareness among end users contributes to stable market growth. Increasing use of MS polymers in electric vehicles and green construction projects continues to support regional expansion.

Europe

Europe held 31.6% market share in 2024, making it the leading regional market for MS polymers. Growth is driven by stringent environmental regulations, strong emphasis on green construction, and high adoption of low-emission materials. Countries across Western and Northern Europe extensively use MS polymers in façade systems, flooring, and glazing applications. Automotive lightweighting initiatives and industrial sustainability targets further reinforce demand. The region’s mature construction standards, combined with continuous product innovation and strong regulatory compliance, support consistent market penetration across both residential and industrial end-use sectors.

Asia Pacific

Asia Pacific captured 26.9% of the MS Polymers market share in 2024, supported by rapid urbanization, infrastructure development, and expanding manufacturing activity. Strong construction growth in residential, commercial, and transportation infrastructure drives high consumption of adhesives and sealants. Rising automotive production and increasing awareness of low-VOC materials further support market growth. While cost sensitivity remains a factor, improving regulatory frameworks and growing adoption of sustainable materials are accelerating MS polymer penetration. Expanding industrial facilities and rising investments in smart cities strengthen long-term growth prospects across the region.

Latin America

Latin America accounted for 7.4% of the MS Polymers market share in 2024, supported by gradual growth in construction, infrastructure renovation, and industrial maintenance activities. Demand is increasing in commercial buildings, transportation projects, and automotive assembly, particularly in urban centers. Although traditional materials remain prevalent, growing awareness of durability and environmental performance is encouraging adoption of MS polymer-based solutions. Economic recovery initiatives and infrastructure investments are supporting steady market expansion. Improved access to advanced construction materials and rising technical awareness among contractors continue to enhance regional demand.

Middle East & Africa

The Middle East & Africa region represented 5.7% market share in 2024, driven primarily by large-scale infrastructure projects, commercial construction, and industrial development. Demand for MS polymers is supported by their performance under extreme temperature conditions and strong resistance to moisture and UV exposure. Ongoing investments in commercial real estate, transportation infrastructure, and industrial facilities sustain market growth. While adoption remains at an early stage in some countries, increasing focus on durable and low-maintenance materials is gradually expanding the use of MS polymer adhesives and sealants across the region.

MS Polymers Market Segmentations:

By Product Type

- Hybrid MS Polymer

- Pure MS Polymer

By Application

- Adhesives & Sealants

- Coatings

By End-user

- Construction & Infrastructure

- Automotive

- Electronics

- Industrial Facilities

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape analysis of the MS Polymers market is characterized by the presence of Kaneka Corporation, AGC Chemicals Americas Inc., Evonik Industries AG, Momentive Performance Materials, Wacker Chemical Corporation, Covestro AG, Arkema S.A., Sika AG, and Henkel AG & Co. KGaA as leading participants. The market reflects moderate consolidation, with established players leveraging strong R&D capabilities, proprietary formulations, and global distribution networks to maintain competitive positioning. Product innovation focuses on hybrid MS polymer technologies, faster curing systems, and enhanced adhesion performance to meet evolving regulatory and application requirements. Strategic initiatives such as capacity expansion, formulation optimization, and partnerships with construction and automotive OEMs are strengthening market penetration. Players are also emphasizing low-VOC and sustainable product portfolios to align with environmental regulations. Competitive differentiation increasingly depends on technical support, application-specific solutions, and long-term performance reliability rather than price competition alone.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Henkel AG & Co. KGaA

- China Risun Group

- Evonik Industries AG

- Sika AG

- Momentive Performance Materials

- Kaneka Corporation

- Arkema S.A.

- Wacker Chemical Corporation

- AGC Chemicals Americas Inc.

- Covestro AG

Recent Developments

- In December 2025, Henkel AG & Co. KGaA launched Loctite MS 9650, a next-generation MS polymer adhesive and sealant designed for durable and lightweight structural bonding in automotive display applications.

- In August 2025, Bostik (Arkema Group) introduced the VSR 400A conductive seam sealant based on silyl modified polymer (SMP) for heavy-duty trucks in the Americas, showcased at the Automotive Composites Conference & Exhibition (ACCE).

- In July 2024, Mohm Chemical launched x’traseal MS-602, an MS polymer sealant designed for construction applications like sealing joints in prefabricated buildings and expansion joints.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Application, End User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The MS Polymers market will continue to expand driven by increasing adoption of low-VOC and solvent-free materials across construction and industrial applications.

- Growing infrastructure development and renovation activities will sustain long-term demand for MS polymer-based adhesives and sealants.

- Automotive lightweighting and rising electric vehicle production will accelerate the use of MS polymers in bonding and sealing applications.

- Product innovation will focus on high-performance hybrid formulations offering faster curing and improved durability.

- Regulatory pressure on emissions and sustainability will further shift demand away from conventional solvent-based chemistries.

- Asia Pacific will remain a key growth region supported by urbanization and manufacturing expansion.

- Demand from industrial maintenance and repair applications will steadily increase due to reliability and ease of use.

- Adoption in emerging applications such as renewable energy installations and modular construction will create new growth avenues.

- Manufacturers will strengthen technical support and application-specific solutions to enhance customer retention.

- Competitive intensity will increase as new entrants and regional players expand capacity and product portfolios.