Market Overview

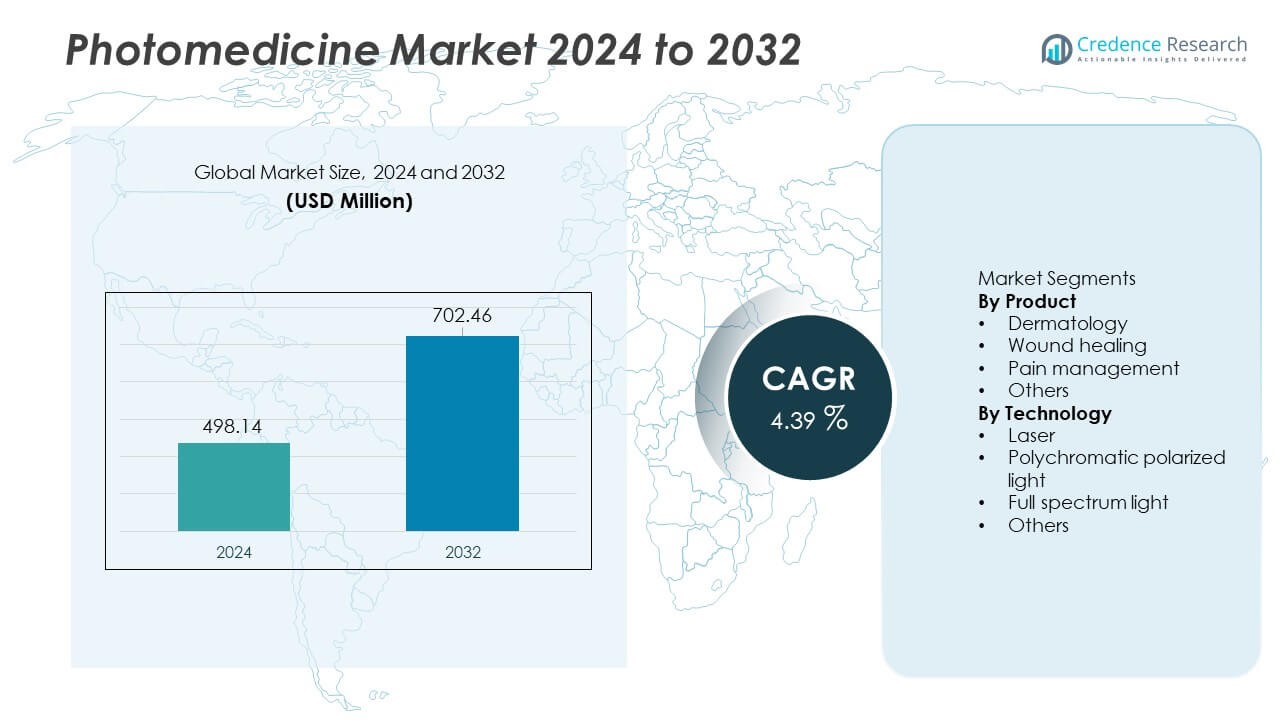

The Photomedicine Market was valued at USD 498.14 million in 2024 and is projected to reach USD 702.46 million by 2032, expanding at a CAGR of 4.39% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Photomedicine Market Size 2024 |

USD 498.14 Million |

| Photomedicine Market, CAGR |

4.39% |

| Photomedicine Market Size 2032 |

USD 702.46 Million |

Top players in the Photomedicine market, including Alma Lasers Ltd., Lumenis, Galderma, AngioDynamics, THOR Photomedicine Ltd, IRIDEX Corporation, PhotoMedex, QBMI Photomedicine, Spectranetics, and Syneron Medical Ltd., continue to advance laser technologies, polarized-light systems, and LED-based therapeutic devices. These companies strengthen clinical adoption through innovations in dermatology, wound care, and pain-management applications. North America leads the market with 39% share, driven by strong aesthetic-medicine demand and high investment in advanced laser platforms. Europe follows with 31% share due to well-established clinical infrastructure and rising adoption of non-invasive phototherapies. Asia Pacific holds 23% share, supported by growing medical-aesthetic procedures and expanding healthcare access, positioning the region as a fast-growing market for leading photomedicine brands.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Photomedicine market reached USD 498.14 million in 2024 and will grow at a CAGR of 4.39% through 2032.

- Demand rises as dermatology devices lead the product segment with 46% share, driven by strong use in aesthetic treatments, wound care, and skin-rejuvenation procedures across clinical settings.

- Trends strengthen around advanced laser systems, polarized-light platforms, and LED-based therapies as companies innovate to meet rising needs for non-invasive and precision-based treatments.

- Competition intensifies as major players expand global distribution, enhance regulatory compliance, and invest in energy-efficient devices while facing restraints linked to high device costs and specialized training requirements.

- North America leads with 39% share, Europe follows with 31%, and Asia Pacific holds 23%, supported by expanding clinical adoption and growing demand for aesthetic and therapeutic photomedicine solutions across key regions.

Market Segmentation Analysis:

Market Segmentation Analysis:

By Product

Dermatology leads the product segment with 46% share, driven by rising demand for non-invasive treatments for acne, pigmentation, psoriasis, and skin rejuvenation. Clinics and dermatology centers adopt photomedicine devices due to their precision, minimal downtime, and improved patient outcomes. Wound healing applications grow as photobiomodulation gains clinical acceptance for faster tissue repair and reduced inflammation. Pain management solutions expand steadily as providers use light-based therapies for musculoskeletal and neuropathic pain relief. The dominance of dermatology continues as aesthetic procedures increase globally and technology advancements improve treatment efficiency and safety.

- For instance, Alma Lasers improved its Harmony XL Pro platform with enhanced power delivery and advanced cooling, which enhances treatment speed for pigmentation and vascular lesions.

By Technology

Laser-based systems dominate the technology segment with 52% share, supported by their strong clinical efficacy, high precision, and suitability for a wide range of medical and aesthetic applications. Dermatology, ophthalmology, and pain therapy providers rely on lasers for targeted energy delivery and predictable results. Polychromatic polarized light grows due to rising adoption in wound healing and inflammatory skin conditions. Full-spectrum light gains traction for broad therapeutic applications, including seasonal affective disorder and skin rejuvenation. Laser leadership strengthens as manufacturers develop compact, high-intensity, and versatile devices with improved energy control and safety features.

- For instance, AngioDynamics enhanced its NanoKnife system with a pulse-field energy delivery of up to 3,000 volts for precise soft-tissue ablation.

Key Growth Drivers

Rising Demand for Non-Invasive and Aesthetic Treatments

The shift toward non-invasive therapies drives strong adoption of photomedicine across dermatology and cosmetic care. Patients prefer light-based treatments for acne, pigmentation, hair removal, and skin rejuvenation due to shorter recovery times and reduced procedural risks. Clinics expand their offerings as phototherapy delivers consistent, high-quality results with improved comfort. Growing awareness of aesthetic wellness and rising disposable incomes further strengthen demand. As technology advances with safer, energy-efficient devices, photomedicine becomes a preferred option for both medical and cosmetic applications, accelerating market growth.

- For instance, Lumenis enhanced its LightSheer DESIRE diode platform with a peak power output of 1,600 watts, enabling faster hair removal with reduced discomfort.

Increasing Use of Photobiomodulation in Wound Healing and Pain Management

Photobiomodulation gains momentum as healthcare providers adopt light-based therapies for enhanced tissue repair and inflammation control. Hospitals and rehabilitation centers use these systems to accelerate wound healing, reduce pain, and improve mobility in patients with chronic or acute injuries. Evidence supporting improved cell regeneration and reduced oxidative stress boosts clinical acceptance. Rising cases of diabetic ulcers and musculoskeletal disorders further increase adoption. As demand for non-pharmacological treatment options grows, photobiomodulation strengthens its role in modern therapeutic care.

- For instance, THOR Photomedicine validated its PBM technology, demonstrating faster tissue repair in clinical studies.

Advancements in Laser and Light-Based Technologies

Technological innovation enhances the precision, versatility, and safety of photomedicine devices, fueling market expansion. New-generation lasers offer improved wavelength control, energy delivery, and tissue selectivity, making them suitable for complex dermatology and surgical applications. Portable and compact systems expand accessibility to clinics and home-care settings. Enhanced user interfaces and automated treatment modes reduce operator dependency and improve outcomes. Continuous R&D investment supports new therapeutic indications, strengthening the value of photomedicine across medical specialties.

Key Trends & Opportunities

Expansion of Home-Use Phototherapy Devices

The market sees growing demand for home-use light therapy devices as consumers seek convenient solutions for skin disorders, pain relief, and mood improvement. Advances in LEDs enable safe, low-energy devices that deliver clinically proven benefits. Dermatology and wellness brands expand product lines focused on acne reduction, anti-aging, and light-based pain management. Remote-care models and digital platforms further support at-home treatments. This trend opens significant opportunities for manufacturers targeting direct-to-consumer channels with affordable, user-friendly devices.

- For instance, Galderma has been involved in research and development of acne treatments, including studies on light-based therapies. Clinical studies have shown that a combination of blue and red light phototherapy is effective for treating mild to moderate acne vulgaris.

Rising Integration of AI and Digital Monitoring in Photomedicine

AI-driven platforms and digital monitoring tools enhance treatment precision, personalization, and safety in photomedicine. Smart devices adjust energy levels based on skin type, lesion depth, or therapeutic response, reducing risk and improving outcomes. Clinics adopt digital imaging and analytics to track patient progress and optimize protocols. These technologies create opportunities for data-driven care, automated workflows, and improved treatment planning. Integration with teledermatology expands reach, strengthening future adoption of intelligent phototherapy systems.

- For instance, Spectranetics deployed advanced laser technology in its medical lasers, allowing for highly precise pulse delivery measured in an extremely short duration for precision in vascular treatments.

Key Challenges

High Equipment Costs and Limited Access in Developing Regions

Photomedicine devices, especially advanced lasers, require significant investment, limiting adoption among small clinics and providers in cost-sensitive markets. Maintenance, training, and replacement parts add to operational expenses. Limited reimbursement further restricts adoption for medical treatments such as wound healing or chronic pain therapy. These financial barriers slow market penetration in emerging regions. Companies must address cost-efficiency and develop more affordable systems to expand global accessibility.

Regulatory and Safety Concerns Related to Energy-Based Devices

Photomedicine systems must meet strict safety, clinical validation, and regulatory standards to ensure patient protection. Variability in global regulations creates complexity for manufacturers seeking approval across multiple markets. Improper use of high-intensity devices can cause burns, pigmentation changes, or ineffective outcomes, increasing scrutiny. Training gaps and inconsistent operator expertise heighten safety risks. Ensuring compliance, certification, and clinical evidence remains a key challenge that influences product availability and adoption.

Regional Analysis

North America

North America leads the Photomedicine market with 38% share, driven by strong adoption of laser systems, advanced dermatology treatments, and photobiomodulation therapies. High demand for non-invasive aesthetic procedures, coupled with rising cases of chronic wounds and pain disorders, supports market expansion. The region benefits from a well-established healthcare infrastructure, strong reimbursement for select phototherapy applications, and rapid technological upgrades by leading manufacturers. Dermatology clinics and ambulatory centers invest heavily in energy-based devices, while growing consumer interest in home-use systems strengthens demand. Continuous R&D activity and regulatory approvals further reinforce the region’s leadership.

Europe

Europe holds 29% share, supported by widespread acceptance of phototherapy for dermatology, wound management, and pain treatment. The region’s strong clinical research landscape drives early adoption of advanced laser technologies and photobiomodulation systems. Dermatology centers across Germany, France, and the U.K. expand their service portfolios as demand rises for cosmetic laser treatments and light-based therapies. Aging populations increase the need for chronic wound solutions, strengthening market growth. Strict regulatory standards enhance product safety and quality, encouraging broader clinical use. Investments in portable and home-based photomedicine devices further support Europe’s steady expansion.

Asia Pacific

Asia Pacific accounts for 24% share and remains the fastest-growing region due to rising healthcare spending, expanding dermatology markets, and increasing demand for aesthetic treatments. Large populations in China, India, and Southeast Asia drive strong interest in laser-based procedures for pigmentation, acne, and skin rejuvenation. Hospitals adopt photobiomodulation for pain and wound care as awareness of non-invasive therapies increases. Local device manufacturers accelerate market penetration with affordable systems. Growing medical tourism in South Korea, Thailand, and Singapore strengthens adoption of high-end photomedicine technologies. Government support for modernization of healthcare infrastructure further boosts regional growth.

Latin America

Latin America holds 6% share, driven by increasing demand for dermatology and aesthetic laser procedures in Brazil, Mexico, and Argentina. Urban clinics adopt photomedicine solutions for pigmentation correction, hair removal, and scar treatment as patient awareness rises. Economic constraints slow high-end device adoption, yet mid-range and portable systems gain traction. Hospitals expand use of phototherapy for chronic wounds and pain management as incidence rates rise. Growth is supported by expanding cosmetic markets, strong influence of social media aesthetics, and rising preference for non-invasive treatments across the region.

Middle East & Africa

Middle East & Africa account for 3% share, supported by rising investment in advanced medical technologies and growing demand for aesthetic care in Gulf countries. The UAE and Saudi Arabia lead adoption due to strong dermatology and cosmetic clinic networks. Photobiomodulation gains attention for pain relief and wound management in hospitals. African nations show gradual growth as healthcare modernization improves access to energy-based therapies, though affordability remains a barrier. Increasing medical tourism and expansion of specialty clinics strengthen long-term market potential. Continued investment in high-quality laser systems supports steady adoption across the region.

Market Segmentations:

By Product

- Dermatology

- Wound healing

- Pain management

- Others

By Technology

- Laser

- Polychromatic polarized light

- Full spectrum light

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The Photomedicine market is shaped by major players including Alma Lasers Ltd., Lumenis, THOR Photomedicine Ltd, Galderma, AngioDynamics, PhotoMedex, Inc., IRIDEX Corporation, QBMI Photomedicine, Spectranetics, and Syneron Medical Ltd. These companies compete by expanding their portfolios in dermatology lasers, wound-healing systems, and pain-management phototherapy devices. Firms invest heavily in R&D to enhance precision, energy efficiency, and treatment depth across clinical and aesthetic applications. Strategic partnerships with dermatology clinics, hospitals, and research institutions strengthen technology adoption. Many players focus on FDA-cleared and CE-marked systems to meet rising regulatory expectations and build market credibility. As demand grows for minimally invasive and light-based therapies, companies emphasize innovation in laser platforms, LED systems, and polarized-light devices to gain differentiation. Competition intensifies as manufacturers target emerging markets and broaden therapeutic indications to capture wider patient populations.

Key Player Analysis

- Alma Lasers Ltd.

- Spectranetics

- QBMI Photomedicine

- Syneron Medical Ltd.

- PhotoMedex, Inc.

- AngioDynamics

- Lumenis

- THOR Photomedicine Ltd

- IRIDEX Corporation

- Galderma

Recent Developments

- In June 2025, Alma Lasers Ltd. launched the next-gen Alma Harmony Platform in India, aiming to redefine aesthetic care there.

- In March 2025, Alma Lasers Ltd. rolled out a new version of its aesthetic platform called Alma Harmony.

- In 2024, THOR Photomedicine Ltd was similarly listed as a key photomedicine-device player, indicating its continued relevance in the industry.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Product, Technology and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for non-invasive aesthetic and therapeutic treatments will continue to increase.

- Laser platforms will advance with higher precision, faster cooling, and improved safety features.

- LED and low-level light therapies will gain wider acceptance in home-care and clinical use.

- Dermatology applications will expand as photomedicine becomes central to skin-rejuvenation procedures.

- Wound-healing technologies will improve through enhanced light-delivery systems and optimized wavelengths.

- Pain-management phototherapy will grow as providers seek drug-free treatment options.

- Companies will invest more in portable and wearable phototherapy devices to support remote care.

- AI-enabled platforms will support personalized treatment settings and improved clinical outcomes.

- Regulatory approvals will shape market expansion as manufacturers enhance compliance and safety.

- Emerging markets will adopt photomedicine faster due to growing aesthetic awareness and better healthcare access.