Smart Bathroom Products Market Overview:

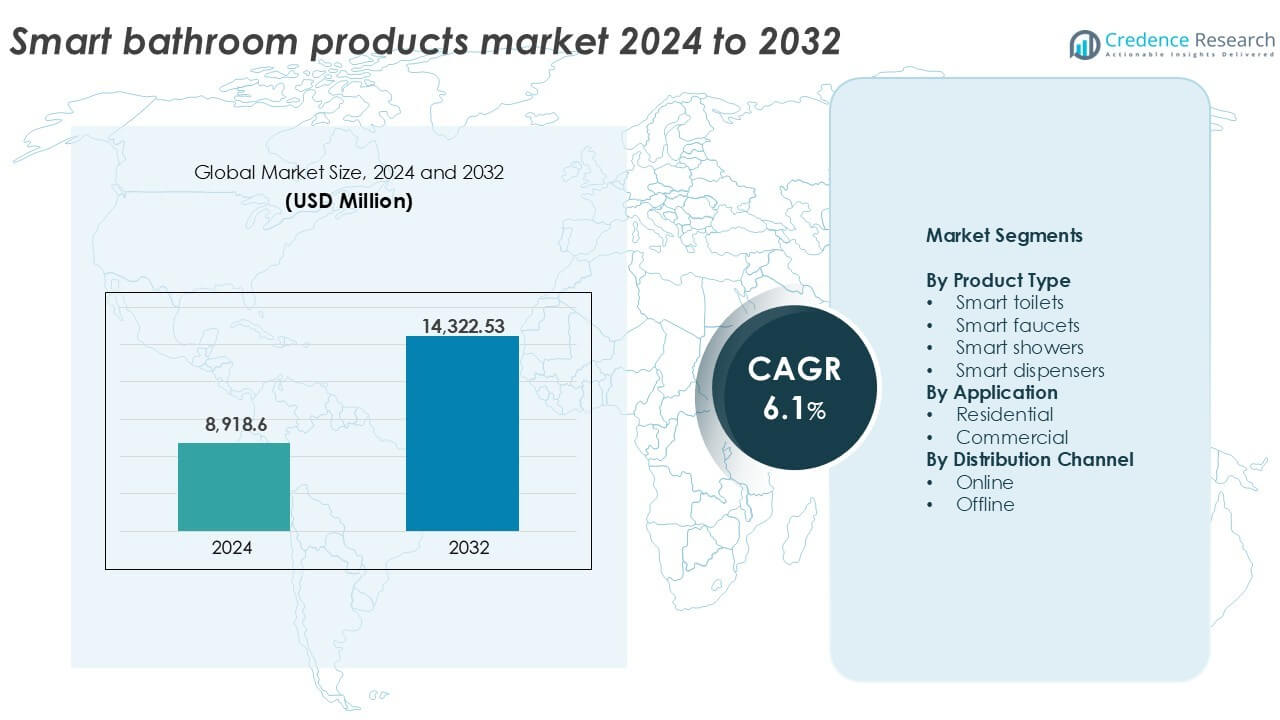

The smart bathroom products market size was valued at USD 8,918.6 million in 2024 and is anticipated to reach USD 14,322.53 million by 2032, at a CAGR of 6.1% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Smart Bathroom Products Market Size 2024 |

USD 8,918.6 million |

| Smart Bathroom Products Market, CAGR |

6.1% |

| Smart Bathroom Products Market Size 2032 |

USD 14,322.53 million |

Top players in the smart bathroom products market include Kohler Co., Toto Ltd., Roca Sanitario, S.A., Moen Incorporated, and American Standard Brands. These companies lead through advanced product features such as touchless control, integrated water-saving systems, and smart connectivity. Their strong R&D capabilities, global brand presence, and wide product portfolios support consistent market performance. North America dominates the market with a 34% share in 2024, driven by high smart home adoption, strong consumer spending, and regulatory support for water efficiency. Europe follows with 28% market share, led by eco-conscious consumers and strict energy standards.

Smart Bathroom Products Market Insights

- The smart bathroom products market was valued at USD 8,918.6 million in 2024 and is projected to reach USD 14,322.53 million by 2032, growing at a CAGR of 6.1%.

- Rising demand for hygiene-focused, touchless solutions and smart home integration drives adoption across residential and commercial sectors.

- Key trends include the use of IoT-enabled fixtures, voice controls, and wellness-focused features such as temperature control and UV sanitation.

- Leading companies like Kohler Co., Toto Ltd., and Roca Sanitario, S.A. focus on innovation and premium product offerings to maintain competitive edge.

- North America holds the largest regional share at 34%, followed by Europe at 28% and Asia-Pacific at 24%, with smart toilets dominating the product segment with over 40% share due to high adoption in both households and hospitality projects.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Smart Bathroom Products Market Segmentation Analysis:

By Product Type

Smart toilets lead the smart bathroom products market by product type, holding over 40% of the market share in 2024. Their dominance is driven by rising demand for hygiene-focused, water-efficient solutions with features such as automatic flushing, heated seats, and self-cleaning nozzles. Aging populations and growing awareness of hygiene standards boost adoption in both developed and emerging markets. Smart faucets and showers also gain momentum, supported by touchless control, temperature regulation, and water-saving functionalities. Smart dispensers see slower uptake but are increasingly used in commercial restrooms for hygiene automation.

- For instance, TOTO has installed more than 70 million WASHLET smart toilets globally, equipped with heated seats, bidet cleansing, and ewater+ self-cleaning technology.

By Application

The residential segment dominates the smart bathroom products market with more than 60% share in 2024. Rising disposable income, urbanization, and smart home integration trends drive adoption of connected bathroom fixtures in homes. Consumers prioritize comfort, health, and energy efficiency, pushing demand for smart toilets and showers. High-end housing developments and renovations in North America, Europe, and parts of Asia-Pacific contribute to strong growth. The commercial segment, though smaller, shows rising demand in hospitality, healthcare, and corporate sectors where hygiene, automation, and maintenance cost reduction are key.

- For instance, Xiaomi sells app-connected smart toilet seats integrated with its Mi Home ecosystem, supporting millions of active smart home users in China.

By Distribution Channel

Offline channels dominate the smart bathroom products market with a share exceeding 55% in 2024. Customers prefer to experience product features physically before purchase, especially for premium fixtures like smart toilets and showers. Retail showrooms, dealer networks, and specialty outlets support offline sales through expert consultation and installation support. However, online sales are growing rapidly due to the convenience of e-commerce platforms, easy comparison, and bundled smart home offerings. Leading brands expand digital presence and offer virtual demos to support direct-to-consumer online strategies.

Key Growth Drivers

Rising Adoption of Smart Home Technologies

The growing penetration of smart home ecosystems significantly fuels the demand for smart bathroom products. Consumers are increasingly integrating connected devices across their homes to enhance comfort, efficiency, and hygiene. Voice-activated controls, app-based management, and IoT connectivity enable seamless integration of smart toilets, showers, and faucets with home assistants like Alexa and Google Home. The ability to monitor water usage, adjust temperature, and schedule features appeals to tech-savvy homeowners. Furthermore, smart bathrooms align with the broader trend of energy and water conservation, enabling users to track consumption and reduce utility bills. Smart home installations, particularly in North America, Europe, and parts of Asia-Pacific, act as strong enablers of adoption. Builders and real estate developers are also embedding smart solutions into new residential projects, making these products a default part of modern homes.

- For instance, Kohler integrates smart toilets and showers with Amazon Alexa and Google Assistant across its Konnect platform, which supports thousands of connected devices globally.

Emphasis on Hygiene, Health, and Wellness

Health and hygiene have become critical purchasing factors, particularly since the COVID-19 pandemic, and smart bathroom products cater directly to these priorities. Touchless technology, self-cleaning functions, and temperature-adjustable features enhance personal hygiene and user safety. Smart toilets with automatic lids, UV sanitation, and bidet functionality reduce germ transmission risks. Wellness-centric innovations, such as aromatherapy showers and water temperature control for stress relief, align with consumer preferences for health-supportive environments. In commercial settings like hospitals and offices, demand grows for smart dispensers and faucets that minimize contact. These features not only support infection control but also appeal to aging populations and individuals with mobility constraints, reinforcing the value proposition of smart bathrooms across all age groups and user profiles.

- For instance, Grohe’s SmartControl shower systems allow precise temperature and flow regulation to support user comfort and stress reduction.

Government Support for Water Conservation

Water conservation initiatives from governments and environmental agencies bolster the demand for smart bathroom fixtures. Regulatory bodies across regions mandate the use of low-flow or sensor-based water fixtures in new buildings. Smart faucets and showers with flow restrictors and automatic shut-off functions help meet these guidelines. For example, the U.S. EPA’s WaterSense program certifies water-efficient bathroom products, encouraging both manufacturers and consumers to prioritize sustainable solutions. These policies also lead to growing awareness among residential users, commercial facility managers, and property developers. Utility rebates and green certification schemes provide further incentives for adoption. The smart bathroom segment, with its advanced control systems and resource optimization features, aligns perfectly with these environmental mandates, driving continued market growth.

Key Trends & Opportunities

Integration of AI and Predictive Maintenance Technologies

A key trend in the smart bathroom products market is the integration of artificial intelligence and predictive maintenance. Modern systems collect data on usage patterns and deliver insights to users via connected apps. AI-driven features can alert users about potential leakages, worn-out parts, or excessive water consumption, enabling proactive maintenance. This not only enhances the product lifespan but also saves money and prevents water damage. In commercial facilities, predictive analytics support large-scale maintenance planning and service automation. Such innovations improve product value and differentiate offerings in a competitive market. As connectivity standards improve, these intelligent features are expected to become standard across mid- to high-end product ranges.

- For instance, LIXIL deploys remote monitoring for smart fixtures across hotels in Japan, enabling maintenance scheduling based on real usage cycles.

Expansion into Commercial and Hospitality Sectors

The commercial sector presents major growth opportunities for smart bathroom products, especially in hospitality, healthcare, and office settings. Hotels increasingly adopt smart toilets and showers to enhance guest experiences, while hospitals and clinics value touchless systems for hygiene control. Corporate offices invest in smart dispensers and faucets to align with sustainability goals and promote employee well-being. Growing awareness of resource efficiency and long-term cost savings further supports commercial sector investments. As businesses upgrade facilities to meet green building certifications and wellness standards, smart bathroom products are positioned as essential upgrades. Suppliers expanding B2B product lines and service models will benefit from this emerging demand.

Key Challenges

High Initial Costs and Retrofit Challenges

The high upfront cost of smart bathroom products poses a barrier, especially in price-sensitive markets. Smart toilets, touchless faucets, and sensor-enabled dispensers carry significantly higher prices than traditional alternatives. Integration often requires plumbing and electrical upgrades, further increasing installation costs. These expenses deter homeowners, small businesses, and low-budget commercial projects. Retrofitting older buildings adds complexity and may demand structural changes or smart hub installations. Consumers often delay purchases unless bundled with broader renovations or supported by subsidies. This limits market penetration in emerging economies and among middle-income households. Affordability and flexible financing will be critical to expanding adoption.

Privacy and Cybersecurity Concerns

As smart bathroom products become more connected, concerns over data privacy and cybersecurity rise. Devices that track usage patterns, water consumption, and environmental settings often store data on cloud-based platforms. Consumers and facility managers worry about unauthorized access, data breaches, and misuse of personal information. Vulnerabilities in app-based controls or smart home integrations pose risks to privacy and safety. Commercial facilities, in particular, demand robust data protection features to comply with regulations. Manufacturers must prioritize secure data encryption, firmware updates, and transparent privacy policies to build trust and comply with evolving standards. Failing to address these risks can hinder adoption and damage brand reputation.

Regional Analysis

North America

North America holds the largest share in the smart bathroom products market, accounting for around 34% in 2024. High smart home penetration, early technology adoption, and strong purchasing power drive regional dominance. Consumers prioritize hygiene, energy efficiency, and convenience, boosting sales of smart toilets, showers, and faucets. The United States leads the region due to aggressive marketing by global brands, rising residential remodeling, and government incentives for water-saving fixtures. Canada follows with growing adoption in premium housing and commercial spaces. The presence of tech-focused manufacturers and a mature e-commerce ecosystem also support sustained growth across the region.

Europe

Europe represents approximately 28% of the global smart bathroom products market in 2024, driven by stringent environmental regulations and widespread acceptance of home automation. Countries such as Germany, the UK, and France lead the region in product adoption. Consumers in this region show strong interest in energy- and water-saving technologies, aligning with EU mandates. Smart toilets and faucets are gaining traction in both residential and commercial sectors. Growth is further supported by government-led smart building initiatives and renovations across urban areas. European manufacturers invest in advanced sensor technologies and hygiene features, strengthening their global competitiveness.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the smart bathroom products market, with a share of about 24% in 2024. Rapid urbanization, rising disposable income, and smart city initiatives across China, Japan, South Korea, and India fuel adoption. Japan leads in smart toilet technology, supported by innovation and widespread cultural acceptance. China experiences robust growth due to expanding middle-class housing and increasing awareness of hygiene standards. India’s market shows strong potential due to real estate development and rising health consciousness. Regional manufacturers increasingly offer locally tailored, affordable smart bathroom solutions, boosting market accessibility in emerging economies.

Latin America

Latin America holds a moderate share of around 7% in 2024, with growth led by Brazil, Mexico, and Argentina. Urban expansion, improving infrastructure, and growing awareness of smart home benefits support demand. Smart toilets and showers gain traction among upper-middle-class households and premium hotels. However, high import costs and limited domestic production constrain widespread adoption. Local distributors and online platforms help expand reach, while multinational brands introduce entry-level smart bathroom ranges. As infrastructure improves and smart home ecosystems develop, the region is expected to witness steady growth in adoption of connected bathroom technologies.

Middle East & Africa

The Middle East & Africa region accounts for approximately 7% of the global smart bathroom products market in 2024. Demand is concentrated in the GCC countries, particularly the UAE and Saudi Arabia, due to luxury residential projects and high-end commercial developments. Consumers seek premium bathroom solutions integrated with IoT and voice control. Water scarcity concerns also drive adoption of water-efficient smart fixtures. In Africa, market growth remains limited by affordability and infrastructure challenges, though urban centers such as Johannesburg and Nairobi show rising interest in tech-enabled housing solutions. Government-backed green building codes further support long-term demand.

Market Segmentations:

By Product Type

- Smart toilets

- Smart faucets

- Smart showers

- Smart dispensers

By Application

By Distribution Channel

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The smart bathroom products market is highly competitive, with key players focusing on innovation, strategic partnerships, and smart technology integration to gain market share. Companies such as Kohler Co., Toto Ltd., and Roca Sanitario, S.A. lead the market through continuous advancements in smart toilets, faucets, and showers. These firms invest in product development featuring AI-enabled systems, water-saving technology, and mobile app controls. American Standard Brands, Moen Incorporated, and Delta Faucet Company maintain strong brand recall through wide distribution networks and diversified product portfolios. European players like Villeroy & Boch AG and Duravit AG compete by offering premium designs and energy-efficient fixtures. New entrants and niche players such as WaterHawk and Kraus USA Plumbing innovate in water usage monitoring and eco-friendly solutions. The competitive focus remains on enhancing user convenience, ensuring hygiene, and aligning with smart home trends. Global expansion strategies and sustainability-focused offerings are expected to further intensify market competition.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Kohler Co.

- Roca Sanitario, S.A.

- Toto Ltd.

- Moen Incorporated

- Duravit AG

- Jaquar

- American Standard Brands

- Villeroy & Boch AG

- Delta Faucet Company

- Jacuzzi Brands Ltd.

- Cera Sanitaryware Ltd.

- Bradley Corporation

- Kraus USA Plumbing

- Pfister

- Signature Hardware

- WaterHawk

Recent Developments

- In March 2023, Roca introduced the In-Wash Insignia shower toilet, which incorporates Roca Connect technology to provide unparalleled comfort and hygiene. Through the accompanying mobile app, called In-Wash Insignia, users can conveniently customize and regulate various operational modes and daily functionalities. Additionally, the app provides valuable insights into water usage and toilet utilization, empowering users with informative data.

- In January 2023, Kohler launched the Sprig Shower Infusion System, during the CES 2023 event. This groundbreaking aromatherapy shower infusion system introduces the Sprig Shower Pods, which have the ability to infuse the water stream with an array of delightful scents such as lavender and eucalyptus. These pods also contain skin-friendly ingredients, ensuring a rejuvenating and luxurious spa-like experience that can be enjoyed on a daily basis.

- In January 2023, “Withings” announced its launch of U-Scan, a palm-sized scanner that attaches straight into your toilet’s bowl. Two cartridges will be available to check various stats: a nutrition and metabolic tracker that checks pH, ketone, vitamin C levels, and more; and a second one to help track women’s luteinizing hormone for ovulation cycles.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Application, Distribution Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Smart bathroom products will see wider adoption as smart home ecosystems expand globally.

- Demand will rise for touchless and hygiene-focused fixtures across residential spaces.

- Water-efficient smart faucets and showers will gain stronger regulatory support.

- Smart toilets will remain the leading product category due to comfort and health benefits.

- Integration with voice assistants and mobile applications will improve user experience.

- Commercial adoption will grow in hotels, hospitals, and corporate facilities.

- Manufacturers will focus on affordable models to reach mid-income households.

- Sustainability and water conservation features will influence purchasing decisions.

- Asia-Pacific will register the fastest growth due to urban housing development.

- Competitive intensity will increase through product innovation and strategic partnerships.