Market Overviews

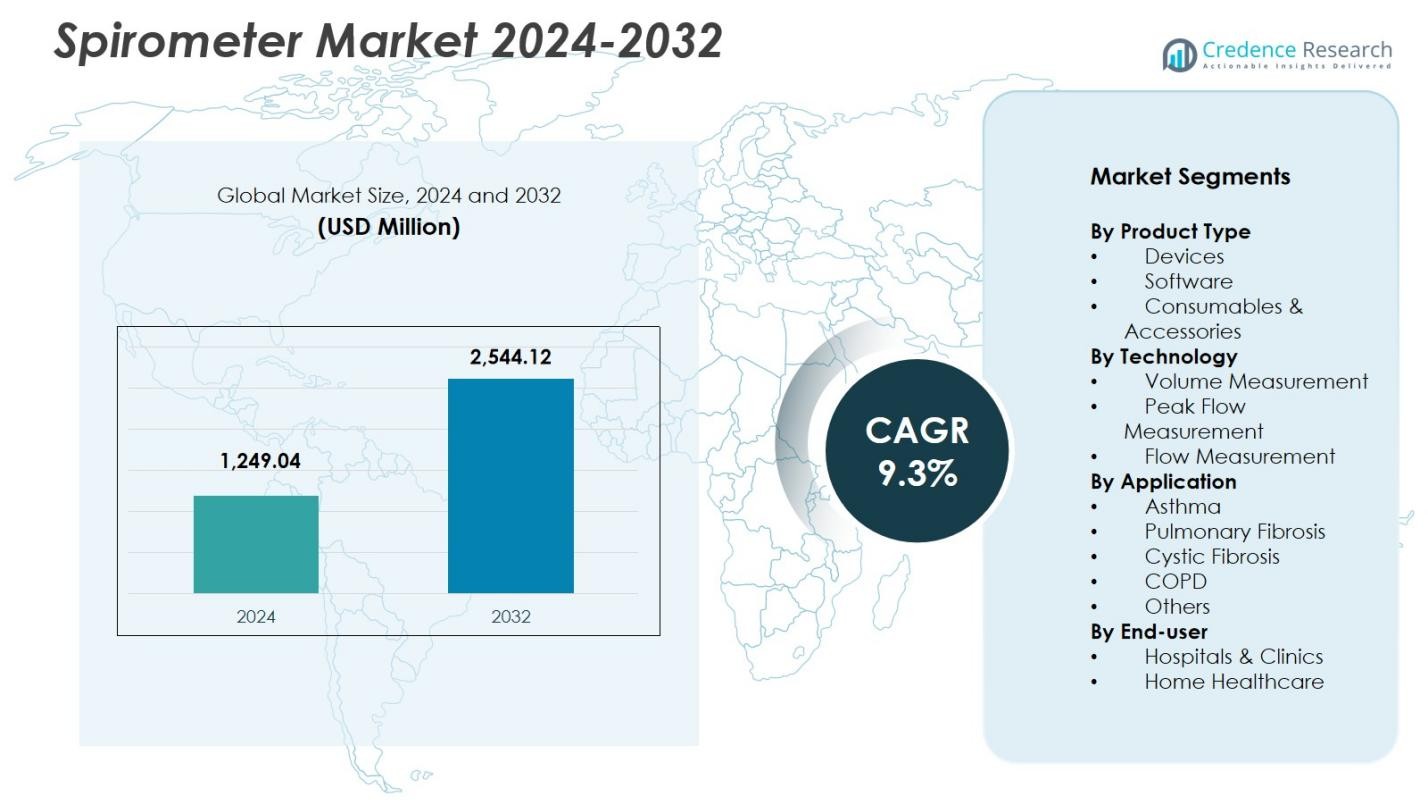

Spirometer Market size was valued at USD 1,249.04 million in 2024 and is anticipated to reach USD 2,544.12 million by 2032, at a CAGR of 9.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Spirometer Market Size 2024 |

USD 1,249.04 Million |

| Spirometer Market, CAGR |

9.3% |

| Spirometer Market Size 2032 |

USD 2,544.12 Million |

Spirometer Market features leading players such as MGC Diagnostics Corporation, NDD Medical Technologies, Koninklijke Philips N.V., Vitalograph Ltd., COSMED srl, Schiller AG, Midmark Corporation, Baxter International (Hill-Rom), Teleflex Incorporated, and MIR (Medical International Research), all of which focus on enhancing diagnostic accuracy, portability, and digital integration. These companies continue to expand their product portfolios with wireless, AI-enabled, and software-supported spirometry systems tailored for clinical and homecare use. Regionally, North America led the market with 34.2% share in 2024, driven by strong healthcare infrastructure and early respiratory screening initiatives, followed by Europe and Asia-Pacific with rising adoption across hospitals, pulmonary centers, and remote monitoring programs.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Spirometer Market was valued at USD 1,249.04 million in 2024 and is projected to reach USD 2,544.12 million by 2032, registering a CAGR of 9.3% during the forecast period.

- Rising COPD and asthma cases, along with increased emphasis on early respiratory screening, continue to drive demand for spirometry devices, with the devices segment holding a 62.7% share in 2024.

- Key trends include rapid adoption of portable, wireless, and AI-enabled spirometers that support remote monitoring and digital integration across clinical workflows.

- Leading players such as Philips, Teleflex, Vitalograph, and COSMED expand their portfolios through product innovation and software-driven respiratory diagnostics, strengthening their market presence across healthcare settings.

- Regionally, North America led with 34.2% share in 2024, followed by Europe at 29.6% and Asia-Pacific at 25.8%, while Latin America and Middle East & Africa continue to grow through improved healthcare access and rising respiratory disease awareness.

Market Segmentation Analysis:

By Product Type:

The Spirometer Market by product type is led by devices, which captured 62.7% market share in 2024, driven by rising respiratory disease prevalence and widespread adoption of portable and handheld spirometers in clinical and homecare settings. Devices remain essential for diagnostic accuracy, routine monitoring, and early detection of lung function decline. Software accounted for a growing share as digital platforms support real-time analytics and remote pulmonary assessment. Consumables and accessories, holding the remaining share, continue to benefit from recurring demand for mouthpieces, filters, and calibration tools essential for infection control and test reliability.

- For instance, ndd Medical Technologies’ EasyOne Air offers a portable ultrasound-based spirometer with TrueFlow technology, featuring a color touch screen for real-time graphs and Bluetooth connectivity for over 100 tests per battery charge without calibration.

By Technology:

Within the technology segment, flow measurement spirometers dominated with 48.3% market share in 2024, supported by high precision, rapid response time, and suitability for both clinical and diagnostic laboratories. Their accuracy in measuring airflow patterns makes them integral for COPD and asthma evaluations. Volume measurement systems held a significant portion due to their established use in pulmonary function testing, while peak flow measurement devices maintained steady adoption, particularly in home monitoring programs, driven by increasing patient awareness and the need for continuous respiratory status evaluation.

- For instance, Vitalograph’s Pneumotrac spirometer uses Fleisch pneumotachograph technology for flow detection, measuring flow rates up to ±16 L/s with volume accuracy within ±2.5% and flow accuracy from ±10% to ±5% across its range.

By Application:

By application, COPD emerged as the leading segment with 41.6% market share in 2024, propelled by rising global COPD cases, early screening initiatives, and expanding use of spirometry as a primary diagnostic tool. Asthma followed, supported by growing pediatric and adult patient populations requiring routine lung function monitoring. Pulmonary fibrosis and cystic fibrosis applications demonstrated consistent adoption as healthcare providers increasingly rely on spirometry for disease progression tracking. The “others” category captured the remaining share, driven by its use in occupational health checkups and preoperative pulmonary assessments across healthcare systems.

Key Growth Drivers

Rising Burden of Chronic Respiratory Diseases

The growing prevalence of COPD, asthma, and other chronic respiratory conditions remains a primary driver for the Spirometer Market. Increasing exposure to air pollution, tobacco use, and occupational hazards continues to elevate diagnostic needs across hospitals, clinics, and homecare environments. Governments and healthcare agencies actively promote early screening programs, boosting the adoption of spirometry as a frontline assessment tool. This expanding patient base, combined with heightened clinical awareness, significantly accelerates demand for advanced, portable, and high-accuracy spirometry systems.

- For instance, Briota Technologies’ SpiroPRO, India’s first CDSCO-approved indigenous digital handheld spirometer, supports the government-backed SAVE program under the National Health Mission.

Expansion of Homecare and Remote Patient Monitoring

The shift toward decentralized healthcare strongly supports spirometer adoption in homecare settings. Patients increasingly rely on portable and Bluetooth-enabled devices for continuous respiratory monitoring, improving disease management and reducing hospital visits. Integration with telehealth platforms enables real-time data sharing, remote evaluations, and early detection of lung function deterioration. This trend aligns with payer and provider initiatives focused on lowering healthcare costs, enhancing convenience, and improving long-term patient outcomes, thereby driving sustained market growth.

- For instance, MIR’s Spirobank Smart uses Bluetooth connectivity for app-based spirometry on iOS and Android devices, supporting remote patient monitoring in homecare. Patients perform coached tests at home via video link with clinicians, sending PDF reports instantly for evaluation.

Technological Advancements and Digital Integration

Rapid innovation in sensor technology, connectivity, and AI-based analytics enhances the diagnostic accuracy and usability of spirometers. Modern devices offer automated calibration, cloud-based data storage, and advanced interpretation algorithms that support clinical decision-making. Digital spirometry integrated with electronic health records streamlines workflow efficiency for healthcare professionals. These advancements promote greater adoption across high-volume care settings and contribute to standardized, high-quality pulmonary assessments globally, strengthening the overall growth trajectory of the market.

Key Trends & Opportunities

Growing Adoption of Portable and Wireless Spirometers

A major trend shaping the market is the rising preference for portable and wireless spirometers that offer mobility, ease of use, and real-time connectivity. These devices support both clinical and home-based monitoring, expanding access to respiratory diagnostics. Manufacturers continue to develop compact systems with enhanced battery life and app-based reporting, creating opportunities in telemedicine, primary care, and resource-limited regions. This shift toward compact, patient-centric solutions positions portable spirometers as a critical growth avenue.

- For instance, Uscom’s SpiroSonic AIR delivers over 10 hours of usage on a single charge via wireless Qi charging and connects via Bluetooth to Android smartphones and tablets for app-based spirometry.

Integration of AI, Predictive Analytics, and Digital Platforms

AI-enabled spirometry is emerging as a significant opportunity, enabling automated quality checks, pattern recognition, and predictive modeling for early detection of respiratory deterioration. Cloud platforms facilitate long-term lung function tracking, supporting chronic disease management and population-health applications. Healthcare providers benefit from standardized data interpretation and reduced manual errors. As digital transformation accelerates across respiratory care, AI-driven spirometry solutions offer strong potential for differentiation, clinical accuracy, and improved patient engagement.

- For instance, Clario’s partnership with ArtiQ adds instant AI over-reading to spirometry in clinical trials, providing real-time quality feedback to avoid repeat testing and decreasing endpoint variability linked to low data quality and human subjectivity.

Key Challenges

Lack of Standardization and Variability in Test Quality

Despite technological progress, spirometry testing often suffers from inconsistent test quality caused by operator errors, improper patient technique, and variation in device calibration. These inconsistencies can compromise diagnostic reliability, particularly in primary care and decentralized settings. Limited training among healthcare workers further exacerbates the issue, creating a barrier to widespread adoption. Ensuring standardized procedures and improving user competency remain critical challenges for achieving accurate and repeatable results.

High Cost of Advanced Devices and Limited Reimbursement

Advanced spirometers with digital and wireless features remain costly for small clinics, community health centers, and low-income regions. Additionally, reimbursement policies for routine spirometry testing vary significantly across countries, limiting accessibility and slowing adoption in cost-sensitive markets. Budget constraints in healthcare facilities and insufficient coverage for home-based monitoring devices create further barriers. Addressing affordability and establishing robust reimbursement frameworks are essential to expanding market penetration and supporting equitable respiratory care.

Regional Analysis

North America

North America led the Spirometer Market with 34.2% market share in 2024, supported by high diagnostic adoption across hospitals, pulmonary labs, and homecare settings. The region benefits from strong clinical guidelines promoting early detection of COPD and asthma, alongside widespread use of digital and wireless spirometry devices. Technological innovation, favorable reimbursement policies, and strong presence of leading manufacturers further strengthen market penetration. Increasing awareness of lung health, expansion of telehealth services, and rising demand for remote respiratory monitoring continue to accelerate spirometer uptake across the United States and Canada.

Europe

Europe accounted for 29.6% market share in 2024, driven by robust public health initiatives, mandatory workplace respiratory assessments, and growing emphasis on early detection of chronic respiratory diseases. Countries such as Germany, the UK, and Italy showcase high spirometry utilization due to advanced healthcare infrastructure and adoption of standardized pulmonary function testing protocols. The region’s increasing preference for portable and AI-integrated spirometers supports market expansion. Rising pollution-linked respiratory issues, aging populations, and continuous investments in digital health solutions further contribute to sustained spirometer demand across European healthcare systems.

Asia-Pacific

Asia-Pacific captured 25.8% market share in 2024, propelled by expanding healthcare access, rising COPD and asthma prevalence, and large-scale government screening programs, particularly in China and India. The region experiences strong demand for cost-effective handheld spirometers and mobile-integrated respiratory diagnostics. Growing investments in hospital infrastructure, increasing use of telemedicine, and heightened awareness of early lung health monitoring fuel adoption. Rapid urbanization and pollution escalation continue to elevate the need for spirometry testing. As digital health ecosystems mature, Asia-Pacific is positioned as the fastest-growing regional market for advanced pulmonary assessment technologies.

Latin America

Latin America held 6.1% market share in 2024, supported by gradual improvements in respiratory care infrastructure and increasing diagnosis rates of asthma and COPD. Brazil and Mexico represent key contributors due to expanding clinical adoption of spirometry and rising governmental focus on chronic disease management. The market benefits from growing penetration of portable devices suitable for remote and underserved areas. However, budget constraints and inconsistent reimbursement remain challenges. Strengthening healthcare digitization, rising awareness campaigns, and expansion of primary care programs continue to create opportunities for broader spirometer utilization across the region.

Middle East & Africa

The Middle East & Africa region accounted for 4.3% market share in 2024, driven by rising respiratory disorders linked to smoking prevalence, pollution, and occupational exposures. Gulf countries, including Saudi Arabia and the UAE, demonstrate increasing adoption of advanced spirometers supported by investments in modern healthcare infrastructure. In Africa, demand is growing for affordable, portable spirometry devices suitable for community health programs. Limited awareness and resource constraints remain barriers; however, expanding public health initiatives, improving diagnostic capabilities, and rising focus on early disease screening continue to support steady market growth across the region.

Market Segmentations:

By Product Type

- Devices

- Software

- Consumables & Accessories

By Technology

- Volume Measurement

- Peak Flow Measurement

- Flow Measurement

By Application

- Asthma

- Pulmonary Fibrosis

- Cystic Fibrosis

- COPD

- Others

By End-user

- Hospitals & Clinics

- Home Healthcare

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape in the Spirometer Market

features leading players including MGC Diagnostics Corporation, NDD Medical Technologies, Koninklijke Philips N.V., Vitalograph Ltd., COSMED srl, Schiller AG, Midmark Corporation, Baxter International (Hill-Rom), Teleflex Incorporated, and MIR (Medical International Research). These companies focus on expanding digital capabilities, enhancing device portability, and integrating advanced analytics to strengthen their market presence. Product innovation remains central, with manufacturers introducing wireless, AI-enabled, and cloud-connected spirometers that support remote patient monitoring and standardized diagnostic workflows. Strategic initiatives such as partnerships with telehealth providers, licensing of software platforms, and continuous upgrades to measurement accuracy help companies broaden their customer base. Emerging players emphasize cost-effective handheld solutions targeted at developing markets, while established brands invest in R&D to develop high-precision systems used in hospitals and pulmonary laboratories. As demand rises for home-based respiratory assessment, leading companies increasingly prioritize user-friendly interfaces, automated calibration, and seamless data integration with electronic health records to maintain competitiveness.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Teleflex Incorporated (US)

- Vitalograph Ltd. (UK)

- MIR (Medical International Research) (Italy)

- Schiller AG (Switzerland)

- Midmark Corporation (US)

- COSMED srl (Italy)

- MGC Diagnostics Corporation (US)

- NDD Medical Technologies (Switzerland)

- Baxter International (Hill-Rom Services, Inc.) (US)

- Koninklijke Philips N.V. (Netherlands)

Recent Developments

- In January 2025, Martins Industries completed the acquisition of ABC American Balancing Corp, a specialist brand in tyre balancing beads, expanding Martins’ tyre balancing product portfolio and market reach, particularly in motorcycle and diverse tyre balancing segments.

- In January 2025, ARI-Hetra introduced three new heavy-duty wheel balancers with integrated online management consoles, enhancing wheel balancing service capabilities for commercial applications.

- In December 2025, Fastco (under Groupe Touchette) announced the acquisition of the ENVY wheel brand, strengthening its position in the wheel and tyre accessories market (which directly ties into wheel balance products and services).

Report Coverage

The research report offers an in-depth analysis based on Product Type, Technology, Application, End User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The spirometer market will continue to expand as early respiratory screening becomes a global healthcare priority.

- Demand for portable and wireless spirometers will rise with the growth of homecare and remote patient monitoring

- AI-powered diagnostic algorithms will enhance test accuracy and support predictive lung health assessments.

- Integration of spirometry data with electronic health records will streamline clinical workflows and improve decision-making.

- Adoption of cloud-connected spirometers will increase as providers shift toward digital respiratory management.

- Emerging economies will experience strong growth due to rising COPD and asthma cases and improving healthcare infrastructure.

- Manufacturers will focus on developing user-friendly, low-maintenance devices that support self-monitoring.

- Telehealth platforms will increasingly incorporate spirometry to enable continuous respiratory tracking.

- Regulatory emphasis on standardized pulmonary testing will drive upgrades to high-accuracy diagnostic systems.

- Growing awareness of occupational lung health will create additional demand across industrial and workplace screening programs.