| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| U.S. Soy-Based Chemicals Market Size 2024 |

USD 8,462.98 Million |

| U.S. Soy-Based Chemicals Market , CAGR |

7.69% |

| U.S. Soy-Based Chemicals Market Size 2032 |

USD 15,313.75 Million |

Market Overview

The U.S. Soy-Based Chemicals Market is projected to grow from USD 8,462.98 million in 2024 to an estimated USD 15,313.75 million by 2032, with a compound annual growth rate (CAGR) of 7.69% from 2025 to 2032. This growth is driven by the increasing adoption of sustainable and renewable resources across various industries.

Key drivers of this market include the rising demand for bio-based and sustainable alternatives, technological advancements in soy-based product development, and government incentives promoting renewable resources. Additionally, the versatility of soy-based chemicals in applications such as biodiesel, bioplastics, and personal care products further fuels market expansion.

Geographically, North America leads the soy-based chemicals market, with the United States being a significant contributor due to its robust soybean production and processing capabilities. Key players in the U.S. market include Cargill, Archer Daniels Midland Company, Bunge Limited, and Elevance Renewable Sciences, Inc., who are actively engaged in research and development to introduce sustainable and eco-friendly soy-based chemicals across various industries.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The U.S. Soy-Based Chemicals Market is projected to grow from USD 8,462.98 million in 2024 to USD 15,313.75 million by 2032, with a CAGR of 7.69% from 2025 to 2032.

- The Global Soy-Based Chemicals Market is projected to grow from USD 28,996.80 million in 2024 to USD 52,069.72 million by 2032, with a CAGR of 7.59% from 2025 to 2032.

- Rising demand for sustainable and renewable resources, technological advancements, and government incentives for bio-based products are key drivers of market growth.

- Soy-based chemicals offer eco-friendly alternatives to petroleum-based products, helping reduce carbon emissions and support environmental preservation.

- Challenges include the relatively high cost of soy-based chemicals compared to traditional alternatives and the volatility of raw material prices.

- The versatility of soy-based chemicals is fueling their adoption across various industries, including biodiesel, bioplastics, personal care, and industrial chemicals.

- North America leads the market, driven by the U.S.’s strong soybean production and processing capabilities, with a focus on sustainable chemical innovations.

- Cargill, Archer Daniels Midland Company, and Elevance Renewable Sciences, Inc. are among the prominent players pushing research and development in soy-based chemicals.

Market Drivers

Rising Demand for Sustainable and Renewable Alternatives

The increasing global emphasis on sustainability and environmental responsibility is a primary driver for the U.S. soy-based chemicals market. Consumers, industries, and governments are increasingly seeking eco-friendly alternatives to petroleum-based chemicals. Soy-based chemicals, derived from renewable agricultural resources, offer a biodegradable and lower-carbon footprint option compared to traditional petrochemicals. This shift aligns with the growing consumer preference for natural and sustainable products, further propelling the demand for soy-based chemicals across various applications, including personal care, paints, coatings, and packaging materials.

Supportive Government Policies and Incentives

U.S. federal and state policies are instrumental in promoting the adoption of bio-based chemicals. Programs like the USDA’s BioPreferred initiative provide incentives and recognition for companies manufacturing and using renewable materials. These policies encourage the development of sustainable products and help companies meet regulatory requirements and sustainability goals. For instance, the USDA BioPreferred program has certified thousands of products, which has contributed to a significant increase in federal procurement of biobased products. Government support for research and development in green chemistry fosters innovation, leading to the creation of advanced soy-based chemical products with enhanced performance characteristics.

Technological Advancements in Soy Processing

Advancements in biotechnology and chemical engineering have significantly improved the efficiency and cost-effectiveness of producing soy-based chemicals. Innovations in extraction and processing technologies enable the development of high-performance soy-derived products that meet the stringent requirements of various industries. For instance, ZeaKal’s PhotoSeed technology has improved the oil and protein content of soybeans, enhancing their nutritional composition and profitability. These technological improvements enhance the competitiveness of soy-based chemicals, making them more attractive alternatives to traditional petrochemical products. Additionally, technologies like GPS and satellite mapping help farmers optimize land use, contributing to more sustainable soybean production.

Expanding Applications Across Diverse Industries

The versatility of soy-based chemicals contributes to their growing adoption across multiple sectors. In the automotive industry, soy-based foams are increasingly used in vehicle seating, while in the construction sector, soy-derived polyols are utilized in the production of eco-friendly insulation materials. The food and beverage industry benefits from soy-based emulsifiers and thickeners, and the cosmetics sector incorporates soy-derived ingredients for their moisturizing properties. This broadening of applications not only drives market growth but also positions soy-based chemicals as integral components in the transition toward a more sustainable and circular economy.

Market Trends

Advancements in Soy-Based Polyols for Sustainable Applications

Soy-based polyols are gaining prominence in the production of polyurethanes, which are utilized in various applications such as foams, adhesives, and coatings. These polyols offer a renewable alternative to traditional petrochemical-based polyols, aligning with the growing demand for sustainable materials. The adoption of soy-based polyols is driven by their biodegradability, reduced environmental impact, and compliance with stringent environmental regulations. Industries are increasingly incorporating these polyols to meet sustainability goals and consumer preferences for eco-friendly products.

Expansion of Soy-Based Biodiesel Production

The U.S. is witnessing a significant expansion in soy-based biodiesel production, driven by favorable government policies such as the Renewable Fuel Standard, which mandates the blending of renewable fuels into the nation’s fuel supply. For instance, Soybean oil is the primary feedstock for biodiesel, with U.S. biodiesel production reaching 1.7 billion gallons in 2023. In December 2020 alone, 744 million pounds of soybean oil were consumed for biodiesel production, making it the largest feedstock used that month. Biodiesel consumption in the 2017/2018 period required 3.24 million metric tons of soybean oil, equivalent to the oil from 667.44 million soybean bushels. This expansion underscores the nation’s commitment to cleaner energy alternatives and reduced reliance on fossil fuels.

Integration of Soy-Based Chemicals in Consumer Goods

There is a notable shift toward integrating soy-based chemicals in consumer goods, including personal care products, packaging materials, and textiles. Companies such as Cargill and ADM have established themselves as leading producers, leveraging their extensive manufacturing capabilities and research investments to supply a wide range of soy-derived ingredients to manufacturers in the U.S. Manufacturers are increasingly reformulating products to incorporate soy-based components, responding to consumer demand for products with natural origin, non-toxicity, and biodegradability. For instance, soy-based emulsifiers, thickeners, and functional ingredients are now widely used in processed and packaged foods, while soy-derived chemicals are also found in deodorants, perfumes, and cleaning products. The integration of soy-based chemicals reflects a broader industry movement toward sustainable, eco-friendly alternatives in everyday products, supported by ongoing advancements in processing technologies and supply chain efficiency.

Strategic Collaborations and Investments in Soy-Based Innovations

Key industry players are increasingly engaging in strategic collaborations and investments to drive innovation in soy-based chemicals. Partnerships between agricultural producers, chemical manufacturers, and research institutions are fostering the development of advanced soy-derived products with enhanced performance characteristics. These collaborations aim to overcome existing challenges related to cost, scalability, and product efficacy, thereby accelerating the commercialization of soy-based solutions across various sectors. Such initiatives are pivotal in establishing a sustainable and competitive soy-based chemicals industry.

Market Challenges

High Production Costs and Price Volatility

One of the significant challenges faced by the U.S. soy-based chemicals market is the relatively high production costs and price volatility of raw materials. Soybeans, the primary feedstock for soy-based chemicals, are subject to fluctuations in price due to various factors, including weather conditions, crop yields, and global supply-demand dynamics. For instance, soybean oil futures contracts have seen significant price fluctuations, reflecting the volatility in the market. The agricultural nature of soy production makes it vulnerable to price swings, which can directly impact the cost-effectiveness of producing soy-based chemicals. Additionally, the cost of processing soybeans into chemical-grade products requires substantial investment in technology and infrastructure. These challenges often lead to higher product costs compared to conventional petrochemical-based alternatives, potentially hindering the widespread adoption of soy-based chemicals across industries, especially for cost-sensitive applications. To mitigate these challenges, companies must invest in innovative processing technologies and supply chain management strategies to stabilize prices and improve profitability. Despite the growing demand for sustainable alternatives, the price volatility and cost structure of soy-based chemicals remain a significant hurdle.

Limited Consumer Awareness and Market Education

While the benefits of soy-based chemicals are becoming more recognized, limited consumer awareness and a lack of widespread understanding about the advantages of using soy-based products continue to pose challenges. Many industries, particularly in sectors such as automotive, packaging, and textiles, have historically relied on petrochemical-based materials due to their well-established supply chains and lower costs. Transitioning to soy-based alternatives requires substantial education and marketing efforts to demonstrate the benefits of these products, such as their sustainability, biodegradability, and renewability. This lack of consumer awareness may delay the adoption of soy-based chemicals, as businesses remain hesitant to switch from conventional materials to newer, less familiar alternatives. Overcoming this challenge will require greater collaboration between manufacturers, industry leaders, and policymakers to promote the environmental and performance advantages of soy-based chemicals and to develop initiatives that encourage both business and consumer engagement with these products.

Market Opportunities

Growing Demand for Bio-Based Products in the Consumer Goods Sector

The increasing consumer preference for eco-friendly and sustainable products presents a significant market opportunity for the U.S. soy-based chemicals market. As more consumers seek out natural, biodegradable, and non-toxic products, industries like personal care, packaging, and textiles are turning to soy-based chemicals as viable alternatives to petroleum-derived options. The versatility of soy-based ingredients, including emulsifiers, surfactants, and polymers, allows them to be integrated into a wide range of consumer goods, from biodegradable packaging to eco-friendly personal care formulations. This shift towards sustainability, supported by rising environmental consciousness, creates a strong growth opportunity for soy-based chemicals across diverse consumer sectors. Furthermore, as regulatory pressure for greener products increases, companies are incentivized to innovate and adopt bio-based chemicals, further expanding the market potential.

Expansion of the Soy-Based Biodiesel Industry

Another key opportunity lies in the expansion of the soy-based biodiesel industry, driven by the increasing global focus on renewable energy sources. Soybean oil is a crucial feedstock for biodiesel production, and as governments push for cleaner energy solutions, the demand for biodiesel is expected to grow. The U.S., being one of the largest producers of soybeans, is well-positioned to capitalize on this opportunity. The expansion of biodiesel production not only supports the biofuel industry but also contributes to reducing greenhouse gas emissions and promoting energy independence. With favorable policies, technological advancements, and growing support for renewable energy initiatives, the U.S. soy-based chemicals market stands to benefit significantly from the continued rise of the biodiesel sector, providing a sustainable avenue for growth and innovation in the market.

Market Segmentation Analysis

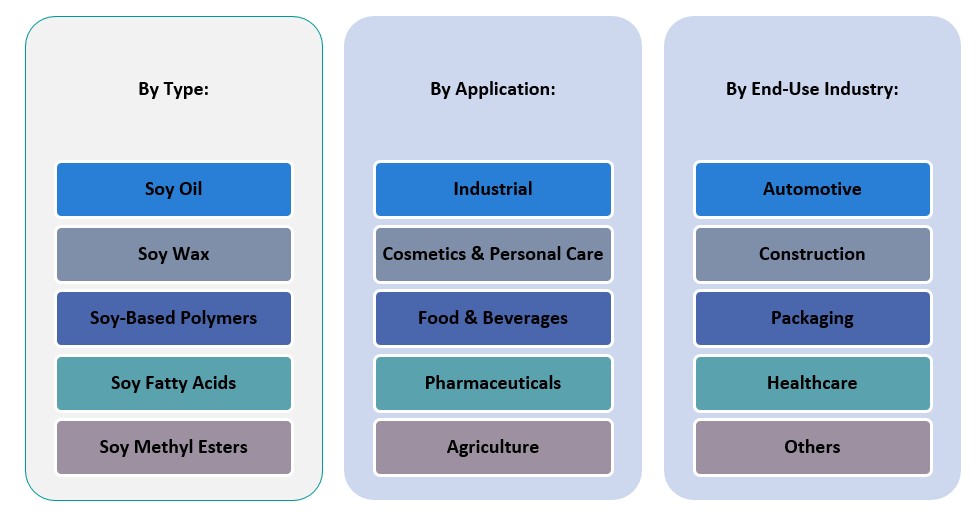

By Type

Soy oil is a widely used product derived from soybeans, serving as a key feedstock for various applications such as biodiesel production, food products, and industrial chemicals. Its versatility positions soy oil as an essential ingredient in renewable energy solutions, especially in biodiesel production. As a biodegradable and renewable material, soy wax is predominantly used in candle manufacturing. The growing demand for eco-friendly products has led to increased adoption of soy wax in consumer goods, especially those focused on sustainability. Soy-based polymers are increasingly used in biodegradable plastics and coatings, gaining traction as an alternative to petroleum-based plastics. The rising demand for sustainable materials is pushing industries to adopt soy-based polymers to reduce environmental impact. Soy fatty acids are utilized in the production of surfactants, soaps, and lubricants. The demand for bio-based materials in industrial applications is driving the growth of this segment, contributing to greener alternatives in manufacturing processes. Soy Methyl Esters primarily used in biodiesel production, soy methyl esters are in growing demand due to the increasing emphasis on renewable energy sources. This shift helps reduce dependency on fossil fuels while supporting sustainable energy solutions.

By Application

Soy-based chemicals play a significant role in industrial applications, particularly in lubricants and surfactants. Their renewable and biodegradable nature makes them an attractive alternative to conventional chemicals in various industrial sectors. Soy-based ingredients such as soy wax, soy oil, and soy fatty acids are increasingly used in cosmetics and personal care products. These ingredients offer moisturizing, emollient, and conditioning properties, aligning with the industry’s shift towards natural and sustainable formulations. In the food industry, soy-based chemicals like emulsifiers and soy lecithin are vital for stabilizing and enhancing the texture of food products. These soy-derived ingredients are increasingly preferred for their natural and functional properties. Soy-derived ingredients are used in pharmaceuticals as excipients, stabilizers, and emulsifiers. Their role in drug formulations is crucial for developing more sustainable and bio-based medical products. In agriculture, soy-based chemicals are used for crop protection, fertilizers, and soil conditioners. These bio-based alternatives offer an environmentally friendly option compared to traditional synthetic chemicals, supporting sustainable farming practices.

Segments

Based on Type

- Soy Oil

- Soy Wax

- Soy-Based Polymers

- Soy Fatty Acids

- Soy Methyl Esters

Based on Application

- Industrial

- Cosmetics & Personal Care

- Food & Beverages

- Pharmaceuticals

- Agriculture

Based on End Use Industry

- Automotive

- Construction

- Packaging

- Healthcare

- Others

Based on Region

- Midwest Region

- South Region

- West Region

- Northeast Region

Regional Analysis

Midwest Region (55%)

The Midwest is the leading region in the U.S. Soy-Based Chemicals Market, holding approximately 55% of the market share. This is due to the region’s prominence in soybean production, as the Midwest is home to the majority of U.S. soybean farms, including states like Illinois, Iowa, and Nebraska. The abundance of soybeans in this region makes it the primary source for soy-based chemical production. Additionally, the Midwest has a well-developed infrastructure for processing and manufacturing, which supports the growth of soy-derived products such as soy oil, soy-based polymers, and biodiesel. The region also benefits from strong government support for agricultural sustainability, which further drives the adoption of bio-based chemicals.

South Region (25%)

The South region accounts for around 25% of the market share in the U.S. soy-based chemicals market. Key states in this region, such as Texas, Arkansas, and Louisiana, are significant producers of soybeans, contributing to the availability of raw materials. The South’s robust industrial sector, including manufacturing, agriculture, and energy, is increasingly adopting soy-based chemicals as part of their sustainability efforts. The region also plays a significant role in the biodiesel industry, where soy methyl esters are used as a major feedstock. As industries in the South shift towards renewable energy solutions, soy-based chemicals are gaining traction in various applications.

Key players

- Archer Daniels Midland Company

- Cargill, Incorporated

- Renewable Lubricants, Inc.

- Soy Technologies LLC

- VertecBio

- Elevance Renewable Sciences, Inc.

- Dow Inc.

- Calgene, Inc.

- BioBased Technologies LLC

- Green Plains Inc.

Competitive Analysis

The U.S. soy-based chemicals market is highly competitive, with major players actively investing in innovation, sustainability, and product diversification. Archer Daniels Midland Company and Cargill, Incorporated dominate the market due to their extensive soybean processing capabilities and large-scale production of soy-based chemicals. Elevance Renewable Sciences, Inc. and Dow Inc. also play a significant role, focusing on the development of high-performance, bio-based chemicals for industrial applications. Renewable Lubricants, Inc. and BioBased Technologies LLC specialize in providing eco-friendly solutions for lubricants and other industrial chemicals, catering to the growing demand for sustainable alternatives. Smaller companies such as Soy Technologies LLC and VertecBio™ contribute to niche markets by offering specialized soy-based products. The competitive landscape is characterized by continuous innovation, with companies seeking to meet regulatory requirements and consumer preferences for environmentally sustainable products.

Recent Developments

- On October 7, 2024, Evonik and BASF agreed on the first delivery of biomass-balanced ammonia, achieving a product carbon footprint reduction of over 65%. This collaboration supports Evonik’s sustainable product lines like VESTAMIN IPD eCO and VESTAMID eCO.

- On February 26, 2025, Arkema announced a 15% expansion of its polyvinylidene fluoride (PVDF) production capacity at its Calvert City, Kentucky plant. This $20 million investment aims to meet the growing demand for high-performance resins in electric vehicles and energy storage systems.

- On February 25, 2025, AkzoNobel offered to acquire powder coatings assets and the International Research Center from its subsidiary in India. This move is part of the company’s strategy to focus more on liquid paints and coatings in the Indian market.

- In February 2025, Perstorp Holding AB began ester production at its Amsterdam plant, marking a significant step in expanding its product offerings in the sustainable chemicals sector.

Market Concentration and Characteristics

The U.S. Soy-Based Chemicals Market exhibits moderate concentration, with a few large players, such as Archer Daniels Midland Company, Cargill, and Dow Inc., holding significant market share due to their extensive production capacities and established distribution networks. However, the market also features a growing number of smaller, specialized companies, such as Renewable Lubricants, Inc. and BioBased Technologies LLC, that focus on niche segments like eco-friendly lubricants and sustainable chemical products. This competitive landscape is characterized by a blend of large-scale corporations driving innovation and research in sustainable products, alongside smaller companies pushing advancements in specific applications. The market is marked by increasing collaboration, technological innovation, and a strong emphasis on environmental sustainability, as both large and small players work to meet the rising demand for renewable, bio-based chemicals across various industries.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Type, Application, End Use Industry and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The U.S. soy-based chemicals market is poised for growth as demand for eco-friendly and sustainable products continues to rise across industries. Consumers and businesses alike are prioritizing renewable materials to reduce environmental footprints.

- Advancements in soy processing technologies will improve efficiency and lower production costs, making soy-based chemicals more competitive compared to petroleum-based alternatives. Innovations in biotechnology and chemical engineering are key drivers of this trend.

- U. S. government policies and incentives promoting renewable energy and bio-based products will further support the growth of the soy-based chemicals market. Initiatives such as the USDA’s BioPreferred program will continue to play a critical role.

- Soy-based chemicals are expanding their footprint in industrial applications such as lubricants, coatings, and adhesives. Their renewable nature and low environmental impact position them as viable alternatives to traditional petrochemicals.

- The biodiesel industry will continue to be a significant growth area for soy-based chemicals. Soy methyl esters are gaining popularity as a renewable feedstock for biodiesel production, driven by the push for cleaner energy sources.

- The personal care industry is increasingly incorporating soy-based ingredients in skincare, haircare, and cosmetics products. These bio-based components align with the growing consumer demand for natural and non-toxic formulations.

- The development of soy-based polymers for applications in packaging, automotive, and textiles will drive market growth. These polymers offer biodegradable and sustainable alternatives to traditional plastics, appealing to environmentally conscious consumers.

- The growing focus on reducing plastic waste is expected to fuel the adoption of soy-based chemicals in packaging materials. Companies are increasingly adopting bio-based plastics and coatings derived from soy to meet sustainability goals.

- Continued investment in R&D will lead to the creation of new, high-performance soy-based chemicals. Companies will focus on improving product formulations, scalability, and cost-efficiency to expand their market reach.

- While the U.S. market remains dominant, the adoption of soy-based chemicals is expanding globally, particularly in emerging economies where sustainability initiatives are gaining traction. This global expansion will provide new growth opportunities for U.S.-based producers.