Market Overview

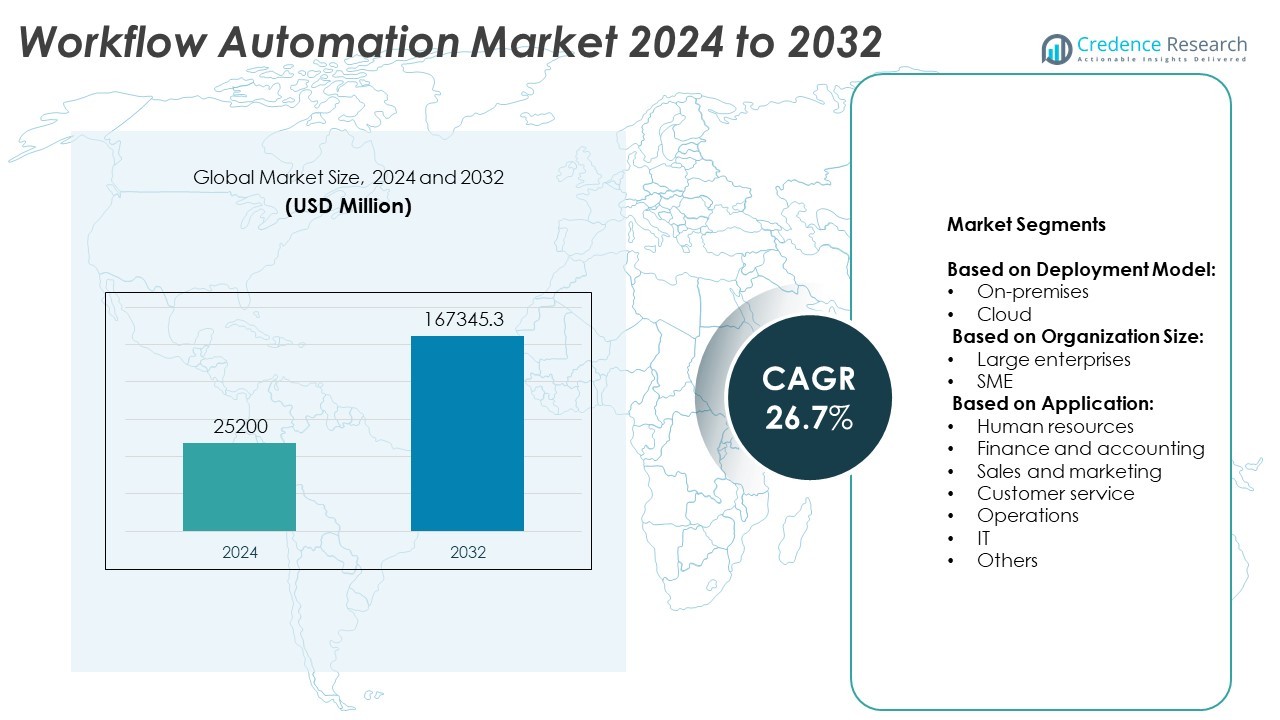

Workflow Automation Market size was valued at USD 25,200 million in 2024 and is anticipated to reach USD 167,345.3 million by 2032, at a CAGR of 26.7% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Workflow Automation Market Size 2024 |

USD 25,200 Million |

| Workflow Automation Market, CAGR |

26.7% |

| Workflow Automation Market Size 2032 |

USD 167,345.3 Million |

The Workflow Automation market advances on the strength of rising demand for operational efficiency, cloud adoption, and digital transformation across enterprises. Organizations implement automation to streamline tasks, reduce errors, and enhance decision-making speed. Trends such as the rise of low-code platforms, integration of AI and machine learning, and growing use of robotic process automation shape the market’s evolution. Businesses seek scalable, real-time solutions that adapt to complex workflows and support hybrid environments

The Workflow Automation market shows strong geographical presence across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America leads adoption due to mature digital infrastructure and enterprise readiness, while Europe emphasizes compliance-driven automation across industries. Asia-Pacific grows rapidly with cloud adoption and digital-first initiatives in emerging economies. Latin America and the Middle East show increasing momentum through public and private digitization programs. Key players driving innovation and expansion across regions include Microsoft Corporation, Pegasystems Inc., IBM Corporation, and SAP SE, each offering integrated, scalable solutions tailored to enterprise and industry-specific need.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Workflow Automation market was valued at USD 25,200 million in 2024 and is projected to reach USD 167,345.3 million by 2032, growing at a CAGR of 26.7%.

- Rising demand for operational efficiency, real-time process visibility, and reduction in manual intervention drives automation adoption across enterprises.

- Key trends include the surge in low-code and no-code platforms, integration of AI for intelligent workflows, and growing use of robotic process automation in hybrid models.

- The competitive landscape includes leading global players offering scalable, AI-enabled platforms, with firms differentiating through industry focus, cloud capabilities, and user-centric design.

- Integration challenges with legacy systems, lack of skilled workforce, and internal resistance to change pose key restraints to widespread deployment.

- North America leads the market in adoption due to enterprise readiness and digital maturity, followed by Europe and Asia-Pacific, where demand grows through compliance and digital expansion.

- Vendors such as Microsoft, Pegasystems, IBM, and SAP invest in intelligent automation, cloud-native solutions, and cross-platform integration to strengthen their position across regions and industries.

Market Drivers

Rising Demand for Operational Efficiency Across Enterprises

Enterprises prioritize workflow automation to reduce manual intervention, minimize errors, and accelerate routine processes. Organizations seek to improve productivity by standardizing workflows and integrating automation tools across departments. The Workflow Automation market benefits from this trend, as companies deploy digital solutions to handle repetitive tasks in finance, HR, and supply chain management. It supports faster approvals, enhanced compliance, and reduced turnaround time. Automation platforms with low-code interfaces further drive adoption among non-technical teams. Businesses implement these solutions to maintain operational agility in competitive markets.

- For instance, Zoho Corporation reported that over 7,500 businesses use Zoho Creator’s low-code automation to reduce process delays by up to 60% in HR and procurement tasks.

Expanding Cloud Infrastructure and Integration Capabilities

The widespread adoption of cloud services accelerates workflow automation across industries. Cloud-native platforms offer scalability, remote access, and real-time synchronization of processes across global teams. The Workflow Automation market aligns with this shift by supporting hybrid environments and seamless integration with enterprise systems such as CRM, ERP, and collaboration tools. It allows businesses to unify processes across fragmented systems, improving visibility and responsiveness. Vendors focus on API-driven platforms to enable customized automation across diverse workflows. Cloud deployment also reduces the burden on internal IT teams by streamlining maintenance and updates.

- For instance, TIBCO Software Inc. integrated its Cloud Integration platform with over 200 APIs, enabling clients to cut workflow execution time by 40% in logistics and inventory operations.

Adoption of AI and Machine Learning in Business Processes

The integration of AI and machine learning enhances the intelligence and adaptability of workflow automation systems. These technologies support predictive analytics, sentiment analysis, and intelligent routing within automated processes. The Workflow Automation market incorporates AI-driven features to help enterprises make data-informed decisions and detect anomalies in workflows. It enables systems to learn from historical data and continuously improve efficiency. Cognitive automation further boosts applications in customer service, document processing, and fraud detection. Organizations adopt AI-infused automation to elevate decision accuracy and process speed.

Growing Emphasis on Digital Transformation and Remote Work

The shift toward digital-first strategies and hybrid work models increases the need for streamlined, automated operations. Enterprises implement automation to sustain business continuity and enable workforce collaboration across geographies. The Workflow Automation market supports this transformation by delivering tools that centralize and automate complex workflows in distributed environments. It eliminates delays caused by siloed communication and manual dependencies. Remote teams benefit from automated notifications, approvals, and document routing, ensuring task completion without physical oversight. Organizations recognize workflow automation as a foundational element of modern digital infrastructure.

Market Trends

Rising Use of No-Code and Low-Code Platforms to Accelerate Adoption

Enterprises increasingly adopt no-code and low-code workflow automation platforms to reduce dependency on IT departments. These platforms empower business users to design, test, and deploy workflows with drag-and-drop simplicity. The Workflow Automation market incorporates such tools to democratize process automation and improve time-to-value. It helps organizations respond quickly to operational changes without lengthy development cycles. This trend also enables faster experimentation and iteration of internal workflows. Vendors continue to enhance their platforms with pre-built templates and intuitive interfaces to support wider adoption.

- For instance, Microsoft Corporation deployed workflow automation across 190 countries through Microsoft Power Automate, enabling over 400 million daily tasks to be executed without manual intervention.

Integration of Robotic Process Automation with Workflow Engines

Companies integrate robotic process automation (RPA) with workflow automation systems to streamline both structured and unstructured tasks. RPA bots perform high-volume, rule-based activities while workflow platforms manage end-to-end process orchestration. The Workflow Automation market evolves to support this hybrid approach, allowing businesses to automate complex workflows across legacy and modern systems. It improves operational efficiency by reducing manual handoffs and optimizing task allocation. This combination enhances employee productivity and system scalability. Businesses apply it across functions such as finance, compliance, and customer service.

- For instance, Blue Prism Group plc deployed automation across over 60 end-to-end processes, returning more than 94,000 work hours back to businesses annually—demonstrating significant operational efficiency within sectors including finance, purchasing, HR, manufacturing, marketing, and IT

Shift Toward AI-Powered Decision Making in Workflows

AI-driven insights increasingly influence decision points within automated workflows. Organizations embed machine learning models to automate dynamic tasks, such as credit scoring, lead prioritization, and demand forecasting. The Workflow Automation market integrates intelligent capabilities to support continuous learning and context-aware actions. It enables workflows to adapt to real-time data and improve over time through feedback loops. Natural language processing also enhances user interaction with automation systems. This trend elevates workflow intelligence and allows systems to manage both routine and exception-based tasks.

Focus on End-to-End Process Visibility and Governance

Businesses prioritize transparency and compliance across their automated workflows. End-to-end visibility helps monitor process performance, identify inefficiencies, and ensure regulatory alignment. The Workflow Automation market addresses these needs by offering dashboards, audit trails, and role-based access controls. It supports organizations in tracking approvals, detecting anomalies, and securing sensitive information. This trend gains momentum in sectors with stringent compliance mandates, such as healthcare, banking, and government. Companies view visibility and control as essential to scaling automation responsibly.

Market Challenges Analysis

Complex Integration with Legacy Systems Limits Scalability

Many enterprises operate on outdated IT infrastructures that lack compatibility with modern automation platforms. Legacy systems often require custom connectors or middleware to function with workflow automation tools, increasing deployment complexity. The Workflow Automation market faces resistance in such environments where integration costs and security risks create implementation barriers. It must address these issues through scalable, API-based architectures that ensure seamless interoperability. Without reliable integration, automation efforts remain isolated and fail to deliver full process optimization. Organizations also encounter delays in standardizing data formats across disparate systems, further restricting efficiency.

Workforce Resistance and Skill Gaps Impact Adoption

Automation initiatives often face internal resistance due to concerns over job displacement and changes in work routines. Employees may lack the technical expertise to manage or adapt to workflow automation tools, especially in non-technical departments. The Workflow Automation market must respond to this challenge by providing training programs, user-friendly interfaces, and change management support. It depends on executive alignment and clear communication to foster acceptance and involvement across teams. Failure to build organizational readiness can stall deployment and reduce return on investment. Companies need to align cultural transformation with technological advancement to ensure sustained adoption.

Market Opportunities

Expansion of Automation in Small and Medium Enterprises (SMEs)

Small and medium enterprises increasingly recognize the value of automation to reduce costs and improve operational control. Cloud-based workflow platforms offer SMEs affordable and scalable solutions without requiring extensive infrastructure. The Workflow Automation market has a strong opportunity to serve this segment with simplified deployment models and subscription-based pricing. It supports SMEs in digitizing core functions such as invoicing, onboarding, and customer service. Vendors that tailor their offerings for ease of use and fast implementation can capture substantial demand. As digital maturity increases among SMEs, demand for automation expands across sectors including retail, logistics, and professional services.

Growth of Industry-Specific Workflow Solutions

Organizations seek automation platforms tailored to the unique compliance, reporting, and operational needs of their industries. The Workflow Automation market can capitalize on this trend by developing sector-specific modules for healthcare, finance, manufacturing, and government. It allows providers to offer pre-configured workflows aligned with regulatory standards and industry best practices. These specialized solutions reduce configuration time and improve adoption rates by addressing domain-specific challenges. Enterprises prefer automation tools that integrate easily with their vertical applications and support audit-readiness. This targeted approach helps vendors differentiate their offerings in a competitive landscape.

Market Segmentation Analysis:

By Deployment Model:

The cloud segment leads adoption due to its flexibility, lower upfront costs, and ease of integration with third-party systems. Businesses favor cloud-based workflow platforms for their scalability and ability to support remote operations. The Workflow Automation market benefits from growing investments in cloud-native applications across industries. It enables organizations to deploy, update, and manage workflows without extensive internal infrastructure. On-premises deployment continues to serve sectors with stringent data security and regulatory requirements, including healthcare, government, and finance. These organizations prioritize control and data residency, which sustains demand for on-premise models in specific markets.

- For instance, Zoho Corporation reports that users have built 1.5 million custom business applications on Zoho Creator over the past decade. This platform, a part of Zoho One, allows users to create web and mobile applications tailored to their specific business needs using a low-code, drag-and-drop interface. The platform is designed for users with minimal or no coding experience and integrates with other Zoho products and third-party applications.

By Organization Size:

Large enterprises dominate the adoption of workflow automation due to their high volume of transactions and complex operational structures. These organizations invest in automation to streamline multi-departmental workflows, reduce manual bottlenecks, and enhance process transparency. The Workflow Automation market also sees strong momentum among SMEs, supported by cost-effective solutions and simplified deployment models. It supports SMEs in managing limited resources while improving customer responsiveness and compliance. Vendors that address the specific needs of small businesses with intuitive interfaces and fast onboarding gain a competitive advantage. Both enterprise tiers contribute to market expansion through unique use cases and automation priorities.

- For instance, Appian achieved the top ranking in “Business Workflow Automation with Integration Use Case” in the 2023 Gartner Critical Capabilities report, scoring 4.78 out of 5 in that category

By Application:

Human resources departments automate repetitive tasks such as recruitment, onboarding, and leave management to enhance employee experience. Finance and accounting teams adopt workflow automation to manage invoice processing, expense approvals, and compliance tracking. Sales and marketing benefit from faster lead routing, campaign approvals, and CRM integration. The Workflow Automation market also enables customer service teams to streamline ticket resolution, escalation management, and feedback collection. Operations teams implement automation to monitor supply chains, manage procurement, and ensure process continuity. IT departments use it to automate incident response, user provisioning, and infrastructure monitoring. Other applications span project management, legal workflows, and compliance auditing across various sectors.

Segments:

Based on Deployment Model:

Based on Organization Size:

Based on Application:

- Human resources

- Finance and accounting

- Sales and marketing

- Customer service

- Operations

- IT

- Others

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the largest share in the Workflow Automation market, accounting for 38% of global revenue. Strong digital infrastructure, widespread enterprise automation, and early adoption of cloud technologies drive demand across the United States and Canada. Businesses in the region prioritize operational efficiency and competitive agility, accelerating the deployment of AI-powered workflow platforms. Sectors such as banking, healthcare, and IT services invest in workflow orchestration to reduce overhead and ensure compliance. Vendors like ServiceNow, IBM, and Salesforce maintain a strong presence, offering scalable solutions to large enterprises and government agencies. The region continues to lead innovation in AI-integrated and low-code automation platforms.

Europe

Europe contributes 27% to the global Workflow Automation market, driven by its emphasis on digital transformation, regulatory compliance, and structured enterprise operations. Countries such as Germany, the UK, and France adopt workflow automation to enhance productivity and adhere to GDPR requirements. Enterprises deploy automation across HR, finance, and procurement functions to streamline cross-border operations. The presence of leading vendors and strong demand from manufacturing, logistics, and public administration sectors sustain regional growth. Cloud-based solutions gain traction as businesses seek scalable and secure automation systems. Initiatives supporting smart industry and digital government further boost market maturity in this region.

Asia-Pacific

Asia-Pacific accounts for 21% of the Workflow Automation market, with rapid adoption across China, India, Japan, and Southeast Asia. Economic digitization, growing startup ecosystems, and increasing cloud infrastructure investment contribute to market expansion. Organizations across industries implement automation to handle high-volume processes and reduce manual dependencies. Demand grows significantly in sectors like e-commerce, IT services, and education where scalability and real-time response are essential. Domestic and international vendors compete for market share by offering cost-effective and customizable solutions. Government programs supporting digital literacy and smart enterprise transformation reinforce regional momentum.

Latin America

Latin America holds 8% of the global Workflow Automation market, with demand emerging steadily across Brazil, Mexico, and Colombia. Enterprises in the region focus on improving internal process efficiency, customer experience, and regulatory compliance. Cloud-based platforms see increased adoption due to cost savings and ease of access. Workflow automation supports functions such as document management, employee onboarding, and customer ticket resolution across mid-sized organizations. The market remains fragmented but shows potential through expanding digital adoption and regional investments in IT modernization. Localized support and regional customization help international vendors establish a foothold.

Middle East & Africa

The Middle East & Africa contributes 6% to the Workflow Automation market, supported by rising demand for digital governance, operational modernization, and private sector digitization. GCC countries invest in workflow tools to improve public service delivery and enhance enterprise efficiency. In Africa, adoption accelerates across banking, telecom, and education sectors, where process automation addresses resource constraints. The shift toward hybrid work environments and paperless systems further strengthens market readiness. International vendors partner with regional players to offer scalable cloud-based solutions aligned with local business needs. Adoption remains uneven but gains momentum through public and private digital initiatives.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Pegasystems Inc.

- Zoho Corporation

- IBM Corporation

- TIBCO Software Inc.

- Xerox Corporation

- SAP SE

- Oracle Corporation

- Blue Prism Group plc

- Amazon Web Services (AWS)

- Microsoft Corporation

Competitive Analysis

IBM Corporation, Oracle Corporation, Pegasystems Inc., Amazon Web Services (AWS), Blue Prism Group plc, Microsoft Corporation, SAP SE, TIBCO Software Inc., Xerox Corporation, Zoho CorporationThe workflow automation market remains highly competitive, with leading players differentiating through cloud integration, AI capabilities, and domain specialization. Enterprise vendors focus on embedding automation into existing ecosystems to streamline complex business processes and drive digital transformation. Some emphasize industry-specific solutions, while others offer broad, modular platforms that scale across departments. Vendors with strong cloud infrastructure and AI capabilities enhance their platforms with intelligent routing, data-driven decisioning, and low-code environments to appeal to both technical and business users. Players targeting small and mid-sized enterprises gain traction through cost-effective, easy-to-deploy tools that support rapid implementation. As automation becomes central to operational efficiency, competitive positioning hinges on product adaptability, ecosystem compatibility, and speed of innovation. Leading firms continue to invest in intelligent automation, hybrid deployment models, and generative AI integration to strengthen market share and retain customer loyalty.

Recent Developments

- In 2025, Blue Prism delivered Blue Prism Assistant, an agentic AI embedded within its Next Gen platform that provides natural-language help and smart asset recommendations for workflow automation.

- In July 2024, Zoom launched Workflow Automation, a no-code tool to improve efficiency and cut down on routine tasks. This feature allows users create complex workflows that connect Zoom Workplace with third-party apps. Initially, the new will work with Zoom Team Chat but later will cover the entire Zoom Workplace platform.

- In 2023, CrowdStrike Falcon Fusion is a sophisticated cloud-based security orchestration, automation, and response (SOAR) framework. It seamlessly integrates with the CrowdStrike Falcon platform and is provided to our valued customers at no additional expense. From the convenience of the Falcon console, SOC analysts are empowered to effortlessly create comprehensive automated workflows utilizing a user-friendly interface, pre-designed workflow templates, and personalized scripts to efficiently execute a wide range of actions directly on the endpoint.

Market Concentration & Characteristics

The Workflow Automation market shows moderate concentration, with a mix of global technology leaders and emerging vendors competing across enterprise segments. It features a diverse range of offerings, including cloud-native platforms, AI-driven process engines, and low-code tools tailored to various organizational sizes and industries. Large players dominate the high-end market through deep integrations, multi-cloud support, and scalable orchestration capabilities. Smaller firms differentiate through agility, ease of deployment, and pricing flexibility that appeals to mid-market and SME customers. The market evolves rapidly with innovation centered on AI, integration capabilities, and industry-specific configurations. It reflects characteristics of high technological dynamism, growing user demand for real-time visibility, and a shift toward democratized automation across non-technical functions. Strategic partnerships, product modularity, and user-centric design define the competitive environment and support continued expansion.

Report Coverage

The research report offers an in-depth analysis based on Deployment Model, Organization Size, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Cloud-based workflow platforms will continue to dominate deployment models due to scalability and ease of access.

- AI integration will drive smarter decision-making and adaptive process flows across industries.

- Low-code and no-code tools will expand adoption among non-technical business users.

- Industry-specific automation solutions will gain traction in healthcare, finance, and manufacturing sectors.

- Vendors will focus on improving cross-platform integration and API connectivity to streamline operations.

- Real-time analytics and process visibility features will become standard in enterprise deployments.

- Hybrid automation combining RPA and workflow orchestration will address complex enterprise needs.

- Demand from small and medium enterprises will grow with the availability of cost-effective, modular tools.

- Automation platforms will evolve to support autonomous workflows with minimal human intervention.

- Regulatory compliance and data security will influence platform design and deployment strategies.