Market Overview:

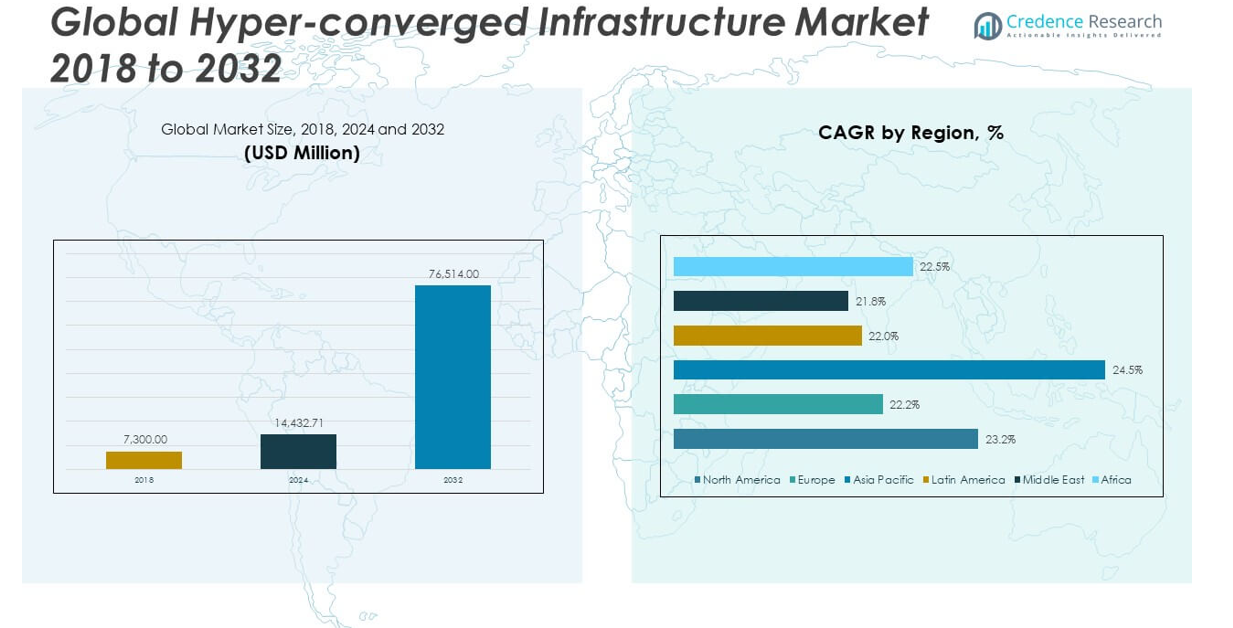

The Hyper-Converged Infrastructure Market size was valued at USD 7,300.00 million in 2018 to USD 14,432.71 million in 2024 and is anticipated to reach USD 76,514.00 million by 2032, at a CAGR of 23.23% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Hyper-Converged Infrastructure Market Size 2024 |

USD 14,432.71 million |

| Hyper-Converged Infrastructure Market, CAGR |

23.23% |

| Hyper-Converged Infrastructure Market Size 2032 |

USD 76,514.00 million |

One of the key growth drivers for the HCI market is the rising demand for data center consolidation and virtualization. Enterprises are increasingly shifting toward unified, software-defined architectures to eliminate the complexity and high costs associated with traditional hardware-based infrastructure. Hyper-converged systems enable organizations to deploy virtualized environments rapidly and scale them effortlessly, making them ideal for modern workloads including virtual desktop infrastructure (VDI), databases, and backup solutions. Additionally, the ongoing migration toward hybrid and multi-cloud ecosystems is propelling HCI adoption, as it seamlessly bridges on-premise and cloud resources. The rising need for disaster recovery, business continuity, and improved operational resilience is also encouraging businesses to opt for HCI solutions that offer integrated data protection and replication capabilities.

Regionally, North America dominates the hyper-converged infrastructure market, accounting for the largest revenue share due to early technology adoption, mature IT ecosystems, and strong investment in digital transformation initiatives. The United States plays a leading role, with widespread deployment of HCI across data centers, government agencies, and enterprises. Europe follows closely, driven by steady adoption in countries like Germany, the United Kingdom, and France, where hybrid cloud strategies and regulatory compliance are pushing the need for integrated infrastructure. However, the Asia Pacific region is expected to register the fastest growth during the forecast period, fueled by increasing digitalization, rapid expansion of data centers, and growing adoption of cloud services across India, China, Japan, and Southeast Asia. Emerging markets in Latin America and the Middle East & Africa are also witnessing growing interest in HCI, particularly in sectors such as healthcare, BFSI, and telecom, where operational efficiency and infrastructure scalability are key priorities.

Market Insights:

- The Hyper-Converged Infrastructure Market was valued at USD 14,432.71 million in 2024 and is projected to reach USD 76,514.00 million by 2032, growing at a CAGR of 23.23%.

- Rising demand for data center consolidation and virtualization is driving enterprises toward software-defined architectures that reduce complexity and cost.

- SMEs are emerging as key adopters due to HCI’s simplicity, lower IT requirements, and reduced operational footprint.

- Organizations seek robust disaster recovery and business continuity, and HCI delivers with integrated data protection and replication capabilities.

- Hybrid and multi-cloud adoption is accelerating demand for infrastructure that can bridge on-premise and cloud platforms seamlessly.

- Challenges such as high initial capital cost, integration with legacy systems, and limited workload customization remain key barriers.

- North America leads the market due to mature IT ecosystems, while Asia Pacific is witnessing the fastest growth, fueled by digital transformation and rapid data center expansion.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Growing Need for Simplified IT Management and Infrastructure Consolidation

Organizations increasingly seek to reduce the complexity of traditional IT infrastructure by unifying computing, storage, and networking into a single software-defined system. The Hyper-Converged Infrastructure Market is gaining traction because it eliminates the need for separate management tools and legacy hardware components. Businesses benefit from reduced operational costs, fewer compatibility issues, and a centralized management interface. It streamlines deployment and enhances control across data centers, improving scalability without sacrificing performance. Enterprises value the flexibility to start with a small deployment and scale out incrementally based on needs. This architecture aligns well with current demands for agile and efficient IT operations.

- For example, Nutanix, a leader in hyper-converged infrastructure (HCI), reports that its Enterprise Cloud Platformconsolidates compute, storage, and networking into a single, centrally managed solution—reducing the number of distinct management tools required by up to 90% compared to legacy three-tier architectures, as detailed in their 2024 ESG economic validation study.

Shift Toward Cloud-Ready Solutions and Hybrid Environments

Enterprises are rapidly transitioning to hybrid and multi-cloud strategies, prompting demand for infrastructure that supports seamless integration between on-premise and cloud platforms. Hyper-converged systems are designed to facilitate this shift by offering cloud-like scalability and simplified workload mobility. The market benefits from businesses prioritizing interoperability, resource optimization, and faster application delivery. It allows enterprises to manage distributed workloads with consistency and control, bridging private data centers with public cloud services. Vendors are expanding features like built-in backup, disaster recovery, and multi-cloud compatibility to meet enterprise requirements. These capabilities position hyper-converged infrastructure as an enabler of digital transformation strategies.

Rising Adoption Across Small and Medium Enterprises for Cost Efficiency

Small and medium enterprises (SMEs) are increasingly investing in hyper-converged solutions due to their compact design, ease of deployment, and predictable cost structure. These businesses often lack the resources to manage complex IT ecosystems and prefer infrastructure that minimizes hardware dependency. The Hyper-converged Infrastructure Market addresses these concerns by delivering integrated systems that are pre-configured, pre-tested, and scalable. It supports essential applications such as file storage, remote desktop services, and virtualized workloads without requiring specialized IT staff. By offering a reduced footprint and energy savings, HCI solutions appeal to SMEs with limited budgets. This trend continues to expand the market’s customer base across diverse sectors.

- For example, Dell VxRailnow offers flexible pay-as-you-grow licensing and a 3-node starter configuration at under $25,000 detailed in Dell’s 2024 SMB solution brief with pre-integrated, factory-tested hardware reducing deployment to under 2 hours.

Demand for Improved Data Protection, Resilience, and Edge Computing Capabilities

Organizations are placing greater emphasis on infrastructure resilience and data protection in response to rising cybersecurity threats and operational risks. Hyper-converged systems support these priorities through built-in encryption, high availability, and automated failover mechanisms. The market is further strengthened by the demand for edge computing, where enterprises deploy infrastructure closer to end users and data sources. It delivers low-latency performance, localized processing, and remote management—features essential for industries like healthcare, manufacturing, and telecom. The ability to operate in harsh or space-constrained environments increases the relevance of hyper-converged solutions in distributed IT settings. These capabilities collectively drive sustained investment in the market.

Market Trends:

Integration of Artificial Intelligence and Machine Learning into Infrastructure Management

Vendors are embedding artificial intelligence (AI) and machine learning (ML) capabilities into hyper-converged platforms to automate performance tuning and predictive maintenance. These technologies help IT teams anticipate hardware failures, optimize resource allocation, and manage workloads more effectively. The Hyper-Converged Infrastructure Market is witnessing increased demand for self-optimizing systems that reduce manual intervention. AI-driven analytics also support data-driven decision-making by delivering real-time insights into application performance and infrastructure usage. It enhances operational efficiency while reducing downtime. Enterprises are adopting intelligent platforms to manage complex workloads across hybrid environments with greater precision.

- For example, Hewlett Packard Enterprise (HPE)leverages AI-driven predictive analytics through its HPE InfoSight platform, which analyzes infrastructure telemetry from over 100,000 systems worldwide.

Expansion of Software-Defined Infrastructure in Core and Edge Deployments

Software-defined infrastructure is gaining traction in core data centers and remote edge environments, aligning with the market’s shift toward flexibility and agility. The Hyper-Converged Infrastructure Market is moving toward fully software-driven control planes that decouple hardware from system management. It enables organizations to deploy infrastructure across geographically distributed sites without compromising control. Enterprises can standardize operations through unified software platforms while maintaining scalability. Vendors are focusing on delivering modular, software-centric architectures that support dynamic provisioning and configuration. This shift supports rapid deployment of applications in sectors such as retail, logistics, and energy.

Growth in Vertical-Specific Customization and Use Case Adaptability

Vendors are tailoring hyper-converged solutions to meet the specific needs of industries such as healthcare, education, defense, and financial services. The Hyper-converged Infrastructure Market is expanding due to demand for application-ready systems that align with regulatory, security, and operational requirements. It supports customized features such as HIPAA compliance, real-time analytics, or high-performance computing for sector-specific workloads. Industry players are designing pre-configured solutions that reduce deployment time and enhance ROI. This trend enables organizations to adopt infrastructure that fits their business model and technology roadmap. It reinforces the relevance of HCI in specialized and high-demand environments.

- For instance, integrated Nutanix HCI platforms come with FIPS 140-2 certification and built-in data-at-rest encryption for government and healthcare deployments, and are pre-configured for HIPAA and PCI DSS compliance requirements.

Emphasis on Subscription-Based Pricing and Infrastructure-as-a-Service Models

Enterprise buyers are increasingly seeking flexible purchasing options that align infrastructure costs with usage and business growth. The Hyper-Converged Infrastructure Market is adapting to this shift through subscription-based pricing, pay-as-you-grow models, and Infrastructure-as-a-Service (IaaS) offerings. It allows organizations to avoid large upfront capital investments while maintaining access to enterprise-grade infrastructure. Vendors are introducing consumption-based billing structures and managed services to attract customers with limited internal IT resources. This financial model supports scalability and cost control, especially in uncertain economic environments. It reflects a broader move toward service-oriented infrastructure delivery across the IT landscape.

Market Challenges Analysis:

High Initial Capital Investment and Integration Complexity in Legacy Environments

Despite long-term cost benefits, many organizations hesitate to adopt hyper-converged systems due to significant upfront capital investment. Licensing fees, hardware upgrades, and training requirements can strain IT budgets, especially for mid-sized firms. The Hyper-converged Infrastructure Market faces resistance from businesses operating legacy systems that are difficult to dismantle or integrate. It often requires rearchitecting workloads and retraining personnel, which slows adoption. Enterprises with deeply embedded traditional infrastructure may find the transition disruptive. Vendor lock-in concerns also arise, as most HCI solutions are bundled and optimized for proprietary ecosystems. These issues create barriers for widespread deployment in cost-sensitive or complex IT environments.

Limited Flexibility in Customization and Performance for Specialized Workloads

While hyper-converged systems perform well across general-purpose applications, they can fall short in handling specialized or high-performance workloads. The Hyper-converged Infrastructure Market must address limitations in customization for industries requiring fine-tuned storage, compute, or networking capabilities. It may not support granular control over hardware configurations, which is often necessary for advanced scientific computing or intensive database operations. Scalability at the component level remains a challenge, as most HCI platforms scale in fixed blocks rather than individual resources. This can lead to inefficiencies and underutilization of assets. Enterprises that demand tailored infrastructure often view HCI as a compromise on control and optimization.

Market Opportunities:

Expansion Potential Across Government and Public Sector Modernization Projects

Government agencies and public sector organizations are actively upgrading their legacy IT infrastructure to meet demands for digital services, cybersecurity, and operational efficiency. The Hyper-Converged Infrastructure Market presents a strong opportunity in this domain due to its ability to simplify management, reduce costs, and improve scalability. It supports secure data processing, rapid deployment, and compliance with regulatory frameworks. Vendors can tailor HCI solutions to align with national digital transformation initiatives. Public cloud alternatives may face regulatory or sovereignty limitations, making on-premise hyper-converged systems a preferred choice. This shift opens avenues for growth in defense, education, healthcare, and municipal service sectors.

Growing Adoption in Developing Economies and Mid-Market Enterprises

Emerging markets in Asia, Latin America, and Africa are accelerating investments in digital infrastructure, creating demand for compact, scalable, and affordable IT solutions. The Hyper-Converged Infrastructure Market has room to grow among small to mid-sized enterprises seeking operational efficiency and simplified deployment. It enables businesses to overcome skill shortages and reduce dependence on complex hardware ecosystems. With improved internet penetration and increasing data workloads, these regions are prioritizing infrastructure modernization. Vendors offering cost-effective, pre-configured HCI systems can capture market share by targeting regional data centers and local service providers. These expanding markets represent a long-term growth path for HCI adoption.

Market Segmentation Analysis:

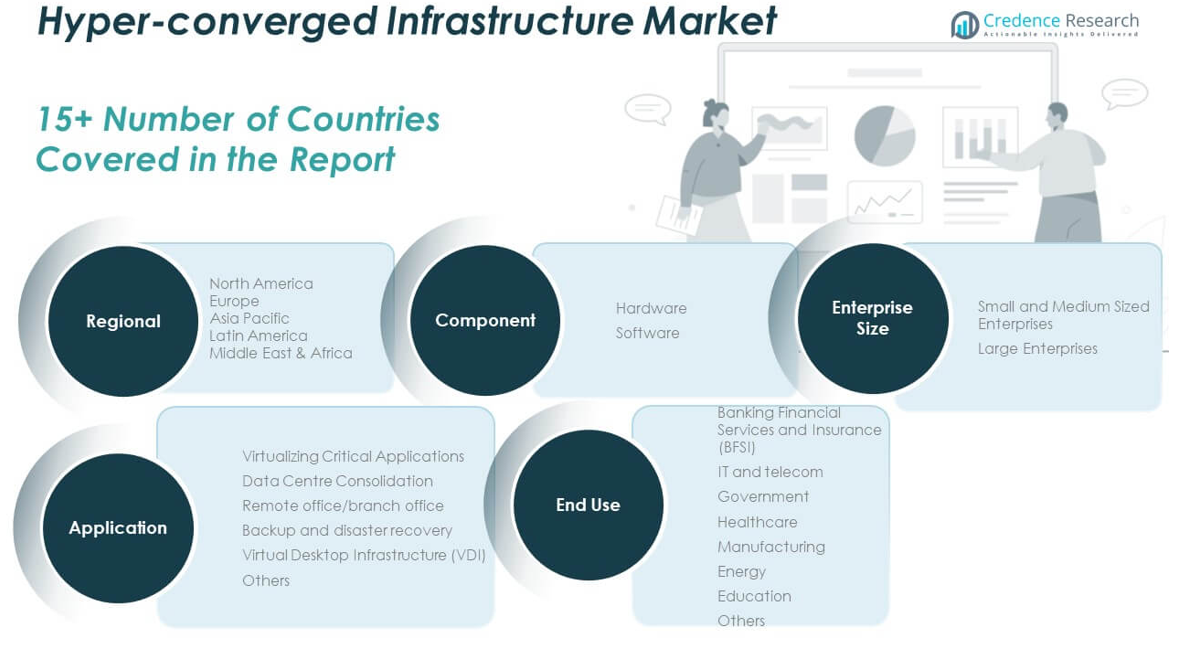

The Hyper-Converged Infrastructure Market is segmented by component, application, end-use, and enterprise size.

By component, hardware accounts for the dominant revenue share due to demand for integrated appliances, while software is gaining momentum with the rise of virtualization and cloud orchestration tools.

- For example, Dell EMC VxRail Appliancesremain the gold standard for integrated, turnkey HCI hardware, with over 170,000 nodes sold globally as of 2024.

By application, virtual desktop infrastructure (VDI), data centre consolidation, and backup and disaster recovery lead adoption, driven by the need for efficient resource use and high availability. Virtualizing critical applications and remote office/branch office deployments are also expanding across distributed enterprises.

- For example, Cisco HyperFlex All-NVMe systems deliver 1.6 million IOPS per node, enabling high-density virtualized workloads with sub-millisecond latency.

By end-use, the IT and telecom sector represents a significant share due to the continuous need for scalable and agile infrastructure. BFSI and government segments rely on hyper-converged systems for secure, compliant operations. Healthcare and manufacturing sectors adopt it to streamline operations and improve data management. The energy and education sectors are gradually integrating these solutions to support evolving digital needs.

By enterprise size, large enterprises dominate the market, leveraging HCI for complex workloads and multi-site infrastructure. However, small and medium-sized enterprises (SMEs) are emerging as a high-growth segment due to the appeal of simplified deployment, lower TCO, and reduced IT overhead.

Segmentation:

By Component Segments

By Application Segments

- Virtualizing Critical Applications

- Data Centre Consolidation

- Remote Office/Branch Office

- Backup and Disaster Recovery

- Virtual Desktop Infrastructure (VDI)

- Others

By End-Use Segments

- Banking, Financial Services and Insurance (BFSI)

- IT and Telecom

- Government

- Healthcare

- Manufacturing

- Energy

- Education

- Others

By Enterprise Size Segments

- Small and Medium-Sized Enterprises (SMEs)

- Large Enterprises

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

The North America Hyper-Converged Infrastructure Market size was valued at USD 2,935.33 million in 2018 to USD 5,739.80 million in 2024 and is anticipated to reach USD 30,337.04 million by 2032, at a CAGR of 23.2% during the forecast period. North America holds the largest share of the Hyper-Converged Infrastructure Market, accounting for nearly 40% of the global revenue. It leads in adoption due to a mature IT ecosystem, high demand for cloud integration, and strong presence of key vendors. The region benefits from early investments in virtualization, software-defined storage, and data center modernization. Enterprises across the U.S. and Canada are deploying hyper-converged solutions to support hybrid cloud strategies and reduce operational complexity. It continues to attract significant investments from public and private sectors seeking resilient, scalable, and cost-effective infrastructure. Demand remains high across industries such as healthcare, BFSI, education, and government.

The Europe Hyper-Converged Infrastructure Market size was valued at USD 1,627.90 million in 2018 to USD 3,070.89 million in 2024 and is anticipated to reach USD 15,207.36 million by 2032, at a CAGR of 22.2% during the forecast period. Europe represents a significant portion of the Hyper-Converged Infrastructure Market, with strong uptake in countries like Germany, the United Kingdom, and France. It accounts for roughly 22% of global market share and is driven by a steady shift toward digital transformation, data privacy regulations, and IT modernization efforts. Organizations across the region prioritize integrated systems that support compliance with GDPR and sector-specific mandates. It supports use cases in public services, telecom, and financial institutions that demand operational efficiency and high availability. Vendor partnerships and regional data center expansion support broader market penetration. Edge computing and virtualization continue to gain traction across medium and large enterprises.

The Asia Pacific Hyper-Converged Infrastructure Market size was valued at USD 1,858.58 million in 2018 to USD 3,831.10 million in 2024 and is anticipated to reach USD 22,152.24 million by 2032, at a CAGR of 24.5% during the forecast period. Asia Pacific is the fastest-growing region in the Hyper-Converged Infrastructure Market, projected to account for nearly 26% of global revenue by 2032. It benefits from rapid digital infrastructure development, rising cloud adoption, and expanding enterprise IT budgets across China, India, Japan, and Southeast Asia. Enterprises are turning to hyper-converged systems to address scalability needs, limited IT resources, and growing data workloads. It offers a solution for both urban and remote environments where traditional infrastructure may be infeasible. Government-led digital initiatives and the rise of regional data centers are boosting demand. Small and medium businesses in the region increasingly prefer pre-integrated, low-maintenance platforms.

The Latin America Hyper-Converged Infrastructure Market size was valued at USD 416.10 million in 2018 to USD 813.86 million in 2024 and is anticipated to reach USD 3,968.78 million by 2032, at a CAGR of 22.0% during the forecast period. Latin America is an emerging region in the Hyper-Converged Infrastructure Market, capturing approximately 5% of global share in 2024. Countries such as Brazil, Mexico, and Argentina are investing in next-generation IT infrastructure to support economic growth and digital services. Enterprises are adopting hyper-converged systems to address IT skill shortages, reduce maintenance costs, and support hybrid cloud operations. It is particularly useful in sectors like healthcare, retail, and telecom where deployment speed and scalability are priorities. Demand is supported by increased internet penetration, e-commerce activity, and data localization policies. Vendors targeting the region offer modular and cost-sensitive solutions tailored to local needs.

The Middle East Hyper-Converged Infrastructure Market size was valued at USD 306.60 million in 2018 to USD 571.44 million in 2024 and is anticipated to reach USD 2,762.58 million by 2032, at a CAGR of 21.8% during the forecast period. The Middle East region presents strong growth potential in the Hyper-Converged Infrastructure Market, fueled by ongoing investments in smart cities, digital government, and enterprise modernization. It currently represents just under 4% of the global market but is gaining momentum due to increased IT spending in the UAE, Saudi Arabia, and Qatar. Governments and corporations are adopting HCI to support cloud-native applications, reduce data center footprint, and enhance data security. It provides the scalability and resilience needed for mission-critical operations. Strategic partnerships between vendors and regional telecom providers are facilitating adoption. Vertical-specific demand in energy, finance, and healthcare sectors continues to strengthen the market.

The Africa Hyper-Converged Infrastructure Market size was valued at USD 155.49 million in 2018 to USD 405.62 million in 2024 and is anticipated to reach USD 2,086.00 million by 2032, at a CAGR of 22.5% during the forecast period. Africa is in the early stages of adopting hyper-converged solutions but shows steady potential within the global Hyper-Converged Infrastructure Market. It holds a modest 2.5% market share but is supported by gradual infrastructure development, growing demand for digital services, and regional cloud initiatives. Countries such as South Africa, Nigeria, and Kenya are exploring integrated IT platforms to improve service delivery across public and private sectors. It helps organizations overcome legacy system limitations and deploy flexible, scalable solutions with minimal technical overhead. Vendors offering simplified and cost-effective systems are finding opportunities in local data centers and education networks. With rising digitalization, the region is expected to contribute more significantly in the coming years.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Dell Inc.

- Nutanix

- Cisco Systems, Inc.

- Hewlett Packard Enterprise Development LP (HPE)

- Huawei Technologies Co., Ltd.

- NetApp

- Broadcom

- Quantum Corporation

- Scale Computing

- Microsoft

Competitive Analysis:

The Hyper-Converged Infrastructure Market features intense competition, driven by rapid innovation and strong demand for integrated IT solutions. Major players include Nutanix, Dell Technologies, VMware, Cisco Systems, and Hewlett Packard Enterprise. These companies focus on enhancing software capabilities, improving scalability, and offering hybrid cloud integration to gain market share. The market also includes emerging vendors like Scale Computing and Pivot3, which target niche segments and small to mid-sized enterprises. It remains dynamic, with vendors investing in AI integration, edge computing support, and subscription-based models. Strategic partnerships, mergers, and acquisitions continue to shape the competitive landscape. Differentiation hinges on performance, ease of deployment, and adaptability across verticals. The Hyper-converged Infrastructure Market benefits from a broad range of offerings, allowing enterprises to align infrastructure choices with specific workloads and business needs. It creates a landscape where innovation, ecosystem compatibility, and service flexibility are key competitive factors.

Recent Developments:

- In April 2025, Dell Technologies unveiled new infrastructure innovations designed to power modern, AI-ready data centers, with a special focus on evolving its hyper-converged and disaggregated infrastructure strategies. This means businesses can now benefit from the flexibility of scaling compute, networking, and storage independently, while still enjoying the operational simplicity typical of hyper-converged systems.

- In May 2025, HPE launched an advanced private cloud portfolio built on its hyper-converged infrastructure platforms. With the introduction of HPE Morpheus Software for virtualized workloads and HPE Morpheus VM Essentials, enterprises can now reduce virtual machine licensing costs dramatically while benefiting from unified management and flexible, disaggregated hyper-converged architecture.

- In May 2025, Nutanix announced significant new partnerships with technology leaders including Nvidia, Pure Storage, Cisco, and Citrix at its NEXT 2025 conference. These collaborations integrate Nutanix’s VMware alternative into a broader array of partner products and services, strengthening its position in cloud, AI, and storage. A notable highlight was the expansion of Nutanix and Dell’s alliance, allowing Dell servers to ship with Nutanix Cloud Platform pre-installed.

- In June 2025, Cisco introduced major innovations for hyper-converged and AI-ready data centers at Cisco Live. These new technologies aim to simplify, secure, and future-proof data centers by integrating expanded AI PODs, a unified management dashboard, and advanced networking—most notably through collaboration with Nvidia for AI-optimized infrastructure.

Market Concentration & Characteristics:

The Hyper-Converged Infrastructure Market exhibits moderate to high market concentration, with a few dominant players holding significant global shares. It is characterized by rapid technological advancements, vendor-driven innovation, and a strong focus on software-defined architecture. The market favors integrated solutions that combine compute, storage, and networking into a unified platform. It supports a shift toward modular and scalable deployments across enterprise and edge environments. Vendors compete on performance, interoperability, ease of management, and hybrid cloud readiness. The market continues to evolve with trends such as AI integration, consumption-based pricing, and vertical-specific customization. It remains attractive to both large enterprises and mid-market organizations seeking agility and cost efficiency.

Report Coverage:

The research report offers an in-depth analysis based on component, application, end-use, and enterprise size. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Demand for scalable and software-defined infrastructure will continue to drive market expansion across enterprises of all sizes.

- Hybrid and multi-cloud strategies will strengthen the role of HCI in unifying on-premise and cloud operations.

- Integration of AI and automation will enhance system intelligence and reduce manual infrastructure management.

- Edge deployments will accelerate, particularly in sectors like manufacturing, retail, and healthcare.

- Subscription-based and pay-as-you-grow models will see wider adoption among cost-conscious businesses.

- SMEs will emerge as a key growth segment due to the simplicity and efficiency of HCI platforms.

- Vertical-specific HCI solutions will gain traction in industries requiring compliance and specialized workloads.

- Advancements in data protection and disaster recovery will boost appeal in security-sensitive environments.

- Emerging markets in Asia Pacific, Latin America, and Africa will contribute significantly to future demand.

- Vendor competition will intensify, leading to increased innovation, strategic alliances, and product differentiation.