Market Overview

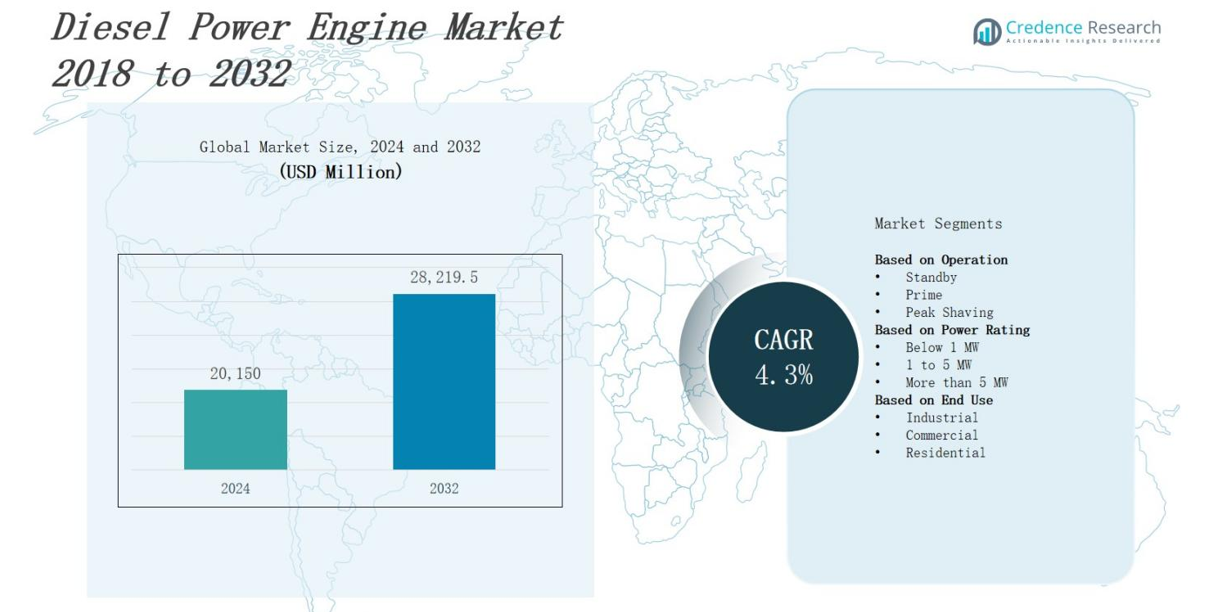

The diesel power engine market is projected to grow from USD 20,150 million in 2024 to USD 28,219.5 million by 2032, at a CAGR of 4.3%.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Diesel Power Engine Market Size 2024 |

USD 20,150 million |

| Diesel Power Engine Market, CAGR |

4.3% |

| Diesel Power Engine Market Size 2032 |

USD 28,219.5 million |

The diesel power engine market is driven by rising demand for reliable backup power across industrial, commercial, and residential sectors, particularly in regions with unstable grid infrastructure. Growth in construction, mining, and agriculture industries also fuels engine adoption due to their high power output and durability. Increasing investment in infrastructure and logistics further supports market expansion. Key trends include the integration of advanced fuel injection systems, electronic engine controls, and emission reduction technologies to comply with stringent environmental regulations. Manufacturers are also focusing on hybrid diesel solutions and enhanced fuel efficiency to meet evolving customer expectations and sustainability goals.

The diesel power engine market spans North America, Asia Pacific, Europe, Latin America, the Middle East, and Africa. Asia Pacific holds the largest share due to high demand across construction and industrial sectors, while North America leads in standby applications. Europe emphasizes emission-compliant technologies, and the Rest of the World offers growth potential through infrastructure expansion. Key players include Wärtsilä Corp., Hyundai Heavy Industries, MAN SE, Doosan, Mitsubishi Heavy Industries, Rolls-Royce Holdings, Volvo Penta, Cummins Inc., and Caterpillar Inc., all competing through innovation, reliability, and regional partnerships.

Market Insights

- The diesel power engine market is expected to grow from USD 20,150 million in 2024 to USD 28,219.5 million by 2032, registering a CAGR of 4.3%.

- High demand for reliable backup power in hospitals, data centers, and telecom drives widespread diesel engine adoption across industrial and commercial sectors.

- Asia Pacific leads with 37% market share, supported by strong infrastructure growth and limited grid access in China, India, and Southeast Asia.

- North America holds 26% share, driven by backup power needs in commercial buildings and strict emission-compliant engine deployment in the U.S.

- Advanced engine technologies such as SCR, DPF, and hybrid-ready systems support compliance with Tier 4 and Stage V regulations.

- Diesel engines remain preferred over alternatives due to their fuel efficiency, high torque, and performance in heavy-duty and off-grid applications.

- Key players include Wärtsilä Corp., Hyundai Heavy Industries, MAN SE, Doosan, Mitsubishi Heavy Industries, Rolls-Royce, Volvo Penta, Cummins, and Caterpillar.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Growing Demand for Backup and Standby Power Across Critical Sectors

The diesel power engine market continues to expand due to rising demand for backup power solutions in industrial, commercial, and residential sectors. Hospitals, data centers, and manufacturing facilities rely on diesel engines for uninterrupted operations during grid failures. Its reliability and rapid startup time make it ideal for critical infrastructure. Governments and private entities prioritize energy security, driving investments in robust standby power systems. Frequent power outages in emerging economies further accelerate adoption of diesel engines.

- For instance, Cummins has supplied 2,500kW diesel generators to data centers, enabling Tier III and Tier IV sites to comply with continuous uptime requirements, supporting uninterrupted data operations when grid power is lost.

Infrastructure Expansion and Industrialization in Emerging Markets

Rapid urbanization and infrastructure development projects across Asia Pacific, Africa, and Latin America boost the diesel power engine market. It serves essential roles in powering construction machinery, irrigation systems, and transport fleets in areas with limited grid access. Industrialization and public infrastructure upgrades demand high-performance, off-grid power sources. Construction equipment manufacturers increasingly integrate diesel engines into mobile machinery. Economic growth in these regions strengthens market prospects and expands diesel engine installations across sectors.

- For instance, China’s extensive construction industry and manufacturing sector drive strong demand for diesel power engines as part of its ambitious infrastructure plans and refinery expansions to ensure stable diesel supply.

High Efficiency and Fuel Economy Favor Diesel Over Alternatives

The diesel power engine market benefits from the technology’s superior thermal efficiency and fuel economy compared to gasoline or gas engines. It delivers higher torque output, making it suitable for heavy-duty applications. Diesel engines operate longer with lower fuel consumption, which appeals to cost-sensitive users in transportation and agriculture. These advantages ensure continued preference in off-road and stationary equipment. Manufacturers continue optimizing engine performance to enhance durability and operating efficiency across all power classes.

Advancements in Emission Control and Engine Technologies

Ongoing technological improvements strengthen the competitiveness of the diesel power engine market. It incorporates selective catalytic reduction (SCR), diesel particulate filters (DPF), and electronic engine controls to meet global emission norms. Compliance with Tier 4 and Stage V standards improves environmental performance without compromising power. OEMs invest in cleaner combustion technologies to extend product viability. The push toward hybrid diesel systems also enables better fuel flexibility and lower emissions in future-ready engines.

Market Trends

Integration of Smart Control Systems and Remote Monitoring Technologies

The diesel power engine market is witnessing increased adoption of smart control systems and IoT-enabled monitoring solutions. It allows users to track engine performance, fuel consumption, and maintenance schedules in real time. These features improve operational efficiency and reduce downtime. Remote diagnostics help operators detect faults early and schedule repairs proactively. The shift toward predictive maintenance lowers total cost of ownership. Fleet operators and utilities are prioritizing digital connectivity across diesel engine assets to enhance productivity.

- For instance, an IoT-based system developed for diesel generators uses multiple sensors (temperature, fuel level, oil pressure, vibrations) connected to an Arduino microcontroller, which transfers data to a cloud platform like ThingSpeak, enabling early anomaly detection and preventing unnecessary shutdowns.

Growing Demand for Hybrid Diesel Systems in Off-Grid Applications

The transition toward hybrid energy systems is reshaping the diesel power engine market. It supports the integration of diesel generators with solar panels, batteries, and energy storage units. Hybrid systems reduce fuel usage and lower emissions without compromising reliability. Off-grid industrial sites and telecom towers are early adopters of such configurations. It addresses power needs in remote areas while meeting regulatory and environmental targets. Manufacturers are optimizing hybrid-ready engines for seamless performance across load conditions.

- For instance, Elum Energy’s off-grid solar-diesel hybrid systems deployed in remote industrial and telecom locations feature energy management controls that optimize fuel use, significantly lowering diesel consumption while ensuring continuous power supply.

Expansion of Rental and Leasing Services Across Construction Sector

The diesel power engine market is experiencing a growing shift toward rental and leasing models, especially in construction, mining, and infrastructure sectors. It enables short-term access to high-capacity engines without heavy capital investments. Demand from small contractors and event organizers continues to rise. Rental providers maintain modern, compliant equipment fleets to meet evolving emissions standards. It enhances flexibility for end-users dealing with seasonal or project-based requirements. OEMs and service companies are expanding their rental footprints globally.

Focus on Cleaner Combustion and Regulatory Compliance Innovations

Emissions regulations are driving innovation within the diesel power engine market. It prompts manufacturers to invest in cleaner combustion technologies, exhaust aftertreatment systems, and advanced fuel injection techniques. Tier 4 and Stage V regulations in North America and Europe raise the bar for engine performance and sustainability. Compliance ensures continued market access and customer trust. Companies are redesigning engine platforms to accommodate low-sulfur fuels and alternative biofuels. Environmental compliance now plays a central role in product development strategies.

Market Challenges Analysis

Stringent Emission Regulations and Environmental Compliance Costs

The diesel power engine market faces rising pressure from global emission standards aimed at reducing air pollution and carbon footprint. It must comply with evolving regulations such as EPA Tier 4 and EU Stage V, which mandate advanced emission control technologies. These requirements significantly increase development and production costs. Small and mid-sized manufacturers often struggle to meet these standards without compromising profit margins. End-users face higher purchase prices and maintenance complexity due to integrated emission systems. Regulatory uncertainty in some regions further complicates long-term planning for OEMs and distributors.

Rising Competition from Cleaner and Renewable Alternatives

The diesel power engine market encounters growing competition from electric motors, gas-powered engines, and renewable energy systems. It risks displacement in segments where zero-emission solutions gain policy and financial support. Governments and industries are investing heavily in battery storage, hydrogen fuel cells, and solar-diesel hybrids. This trend reduces diesel engine deployment in urban infrastructure and transportation sectors. Public perception around pollution and sustainability drives preferences away from traditional diesel solutions. Market players must innovate to retain relevance in environmentally conscious industries.

Market Opportunities

Expansion in Emerging Economies with Weak Grid Infrastructure

The diesel power engine market holds strong potential in emerging economies where electricity access remains inconsistent. It plays a vital role in supporting construction, agriculture, telecom, and healthcare sectors across rural and semi-urban areas. Countries in Asia, Africa, and Latin America continue to invest in infrastructure, increasing demand for reliable off-grid power. Diesel engines offer dependable performance in harsh operating environments. Governments and private players seek backup solutions to bridge grid reliability gaps. This sustained infrastructure push presents long-term growth opportunities for diesel engine suppliers.

Adoption of Advanced Diesel Technologies for Industrial Applications

The diesel power engine market can capitalize on advancements in engine design, fuel injection, and exhaust treatment systems. It enables high-performance output while meeting current environmental standards. Industries such as oil and gas, marine, and mining still rely on diesel for its high torque and operational flexibility. The development of hybrid diesel systems further expands application in remote and mobile setups. Demand for compact, efficient, and low-emission engines continues to rise. Manufacturers that deliver technologically advanced solutions can access new market segments and secure competitive advantage.

Market Segmentation Analysis:

By Operation

The diesel power engine market segments by operation into standby, prime, and peak shaving applications. Standby engines dominate the market due to high demand across hospitals, data centers, and commercial buildings where power reliability is critical. Prime power engines serve continuous-use applications in remote or off-grid areas, particularly in mining and oilfield operations. Peak shaving units help industrial users reduce electricity costs during high-demand periods. Each operation mode serves distinct user needs and influences engine design and performance expectations.

- For instance, MAN diesel standby engines operate typically around 50 hours per year but deliver essential emergency power ranging from 396 kW to 1,117 kW during outages.

By Power Rating

The diesel power engine market includes engines rated below 1 MW, between 1 to 5 MW, and above 5 MW. Engines below 1 MW hold a large share due to widespread use in residential and light commercial applications. The 1 to 5 MW segment caters to mid-sized industrial facilities, commercial complexes, and critical infrastructure. Engines above 5 MW support heavy industries, large-scale utilities, and marine operations. It reflects growing demand for high-output systems that ensure uninterrupted operations in energy-intensive sectors.

- For instance, engines below 0.5 MW hold about 40% market share, widely used in small commercial enterprises and backup power systems because of their compact and affordable design.

By End Use

The diesel power engine market segments by end use into industrial, commercial, and residential categories. Industrial users account for the largest share, driven by consistent need across manufacturing, construction, and mining operations. The commercial sector uses diesel engines in retail outlets, offices, hospitals, and telecom infrastructure where continuous backup is essential. Residential usage grows in regions with poor grid connectivity or frequent power cuts. It remains vital across all sectors for its reliability, scalability, and adaptability.

Segments:

Based on Operation

- Standby

- Prime

- Peak Shaving

Based on Power Rating

- Below 1 MW

- 1 to 5 MW

- More than 5 MW

Based on End Use

- Industrial

- Commercial

- Residential

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America holds 26% share of the global diesel power engine market, driven by demand from industrial, commercial, and data center sectors. It benefits from strict backup power requirements across hospitals, government facilities, and telecom networks. The United States dominates regional demand, supported by grid resilience initiatives and construction activity. Diesel engines are preferred for their reliability and ease of integration into emergency systems. It continues to attract investments in advanced emission-compliant engines. Manufacturers focus on hybrid models to align with environmental goals without sacrificing power capacity.

Asia Pacific

Asia Pacific leads the diesel power engine market with a 37% share, fueled by large-scale infrastructure development and limited grid access in rural areas. China, India, and Southeast Asian countries use diesel engines extensively across construction, agriculture, and manufacturing. Rapid urbanization and industrial expansion create strong demand for both standby and prime power applications. It supports telecom towers, water pumps, and temporary construction facilities in remote zones. Governments prioritize energy access, creating consistent growth opportunities for engine suppliers. Domestic and international manufacturers compete for volume-driven contracts and rental fleet partnerships.

Europe

Europe accounts for 18% of the diesel power engine market, supported by robust demand in marine, manufacturing, and public infrastructure. Germany, the UK, and France lead installations due to their industrial base and stringent power continuity requirements. It experiences moderate growth due to the region’s strong focus on emission reduction and adoption of clean energy alternatives. Diesel engine use remains relevant in backup and off-grid scenarios, especially in Eastern Europe. Manufacturers adapt by developing low-emission engines to comply with EU Stage V norms. Retrofit and replacement demand drives aftermarket revenue streams.

Rest of the World

The Rest of the World, including Latin America, the Middle East, and Africa, holds 19% share of the diesel power engine market. It supports essential applications where grid supply is unstable or unavailable. The Middle East leads demand for engines in oil and gas operations, while Africa relies on diesel for power access across remote communities. Latin America uses it in construction, agriculture, and commercial properties. It offers untapped potential due to growing electrification efforts and infrastructure investments. Suppliers target local partnerships and rental solutions to increase regional penetration.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Wärtsilä Corp.

- Hyundai Heavy Industries Co., Ltd.

- MAN SE

- Doosan

- Mitsubishi Heavy Industries, Ltd.

- Rolls-Royce Holdings plc.

- Volvo Penta

- Cummins, Inc.

- Caterpillar Inc.

Competitive Analysis

The diesel power engine market features intense competition among multinational corporations offering advanced, reliable, and efficient engine solutions. Key players include Wärtsilä Corp., Hyundai Heavy Industries Co., Ltd., MAN SE, Doosan, Mitsubishi Heavy Industries, Ltd., Rolls-Royce Holdings plc., Volvo Penta, Cummins, Inc., and Caterpillar Inc. It remains driven by product innovation, emission compliance, and operational efficiency. Companies focus on expanding their global footprint through strategic alliances, distribution networks, and aftermarket services. Leading firms invest in digital technologies, hybrid system integration, and fuel optimization to meet changing regulatory and customer requirements. Competitive differentiation depends on engine performance, cost-effectiveness, and application-specific customization. The market continues to reward companies that balance technological leadership with strong service capabilities and localized manufacturing strategies.

Recent Developments

- In April 2024, Rolls-Royce partnered with ASCO Carbon Dioxide Ltd and Landmark Power Holdings Limited to develop scalable carbon capture solutions for clean power generation using mtu engines.

- In March 2024, Caterpillar collaborated with the Africa Data Centres Association to supply high-density diesel and gas generator sets tailored for continuous, standby, and temporary power at data centers.

- In January 2024, Tata Motors launched its Turbotronn 2.0 diesel engine for trucks in the 19–42 tonne category, aiming to enhance efficiency and reliability in commercial transport.

- In January 2024, Jaguar Land Rover unveiled the new Range Rover Evoque with both diesel and petrol variants, featuring fog lights, air purifiers, wireless charging, and a 48V mild-hybrid system.

Market Concentration & Characteristics

The diesel power engine market shows moderate to high concentration, with a few dominant players controlling significant global share. It includes established firms such as Caterpillar, Cummins, MAN SE, and Mitsubishi Heavy Industries, which maintain strong brand equity, global distribution, and advanced R&D capabilities. The market features high entry barriers due to stringent emission norms, capital-intensive manufacturing, and technological complexity. It serves diverse sectors including construction, mining, manufacturing, marine, and residential backup power, demanding reliability and high torque performance. Product differentiation centers on fuel efficiency, emission compliance, and digital integration. OEMs focus on expanding aftermarket services and rental networks to retain customers and improve margins. The diesel power engine market relies on long-term infrastructure investment cycles, and it remains highly sensitive to fuel regulations and environmental policies. Competitive dynamics are shaped by regional demand patterns, customization needs, and the pace of hybrid and low-emission technology development.

Report Coverage

The research report offers an in-depth analysis based on Operation, Power Rating, End Use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for diesel power engines will remain strong in sectors requiring reliable backup power like healthcare, telecom, and data centers.

- Emerging markets will continue to drive engine sales due to infrastructure expansion and limited grid access.

- Manufacturers will focus on hybrid diesel systems to meet emission targets and improve fuel efficiency.

- Technological innovations will enhance engine durability, remote monitoring, and control capabilities.

- Regulatory pressure will push OEMs to develop engines compliant with evolving emission standards.

- Off-grid and rural applications will boost demand for low-maintenance, high-torque diesel engines.

- Engine rental and leasing services will grow in popularity among construction and mining contractors.

- Integration of digital diagnostics and predictive maintenance tools will increase operational efficiency.

- Local partnerships and service networks will become critical for expanding in developing regions.

- Replacement demand for aging engines will create steady growth in aftermarket and retrofit segments.