Market Overview:

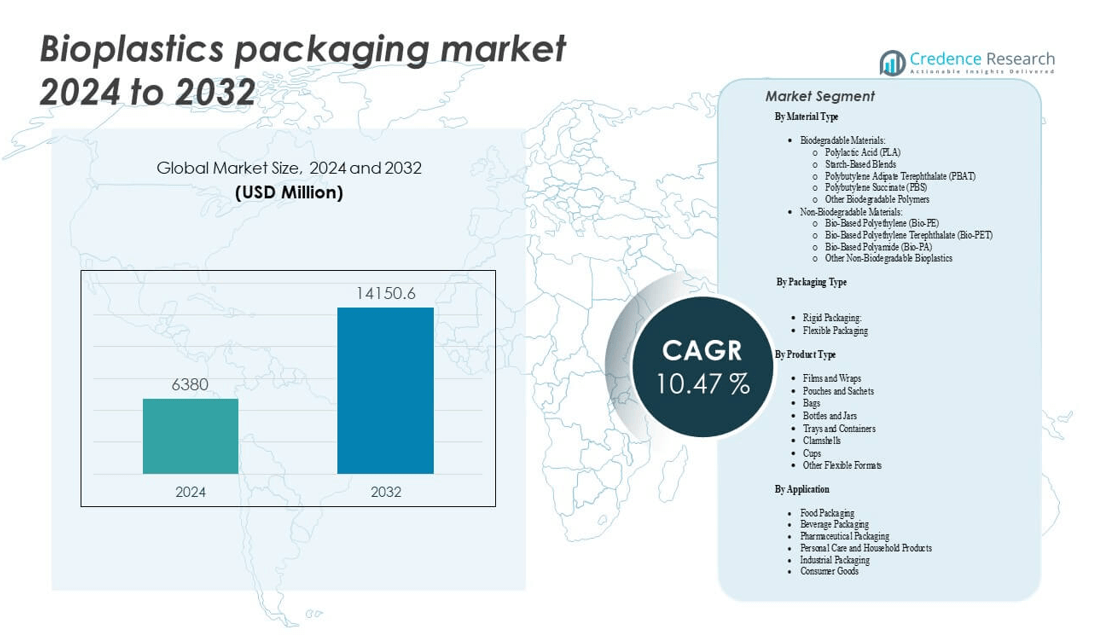

The Bioplastics packaging market is projected to grow from USD 6,380 million in 2024 to an estimated USD 14,150.6 million by 2032, with a compound annual growth rate (CAGR) of 10.47% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Bioplastics Packaging Market Size 2024 |

USD 6,380 million |

| Bioplastics Packaging Market, CAGR |

10.47% |

| Bioplastics Packaging Market Size 2032 |

USD 14,150.6 million |

The market growth is primarily driven by increasing consumer demand for sustainable and environmentally friendly packaging solutions. Regulatory bans on single-use plastics across various countries have accelerated the adoption of bioplastics in packaging. Industries such as food and beverage, personal care, and consumer goods are integrating bioplastics to reduce carbon footprints and appeal to eco-conscious consumers. Technological advancements in biodegradable polymers and improving cost-efficiency are further enhancing market competitiveness and scalability.

Regionally, Europe leads the bioplastics packaging market due to strong environmental regulations, government incentives, and widespread awareness of sustainability. Countries like Germany, France, and the Netherlands are at the forefront of adopting bioplastic materials in various packaging formats. North America follows, driven by corporate sustainability goals and innovative packaging startups. Meanwhile, the Asia Pacific region is emerging rapidly, with countries such as China, India, and Japan expanding their bioplastics production and consumption, supported by growing industrialization, consumer awareness, and policy support.

Market Insights:

- The Bioplastics packaging market was valued at USD 6,380 million in 2024 and is projected to reach USD 14,150.6 million by 2032, growing at a CAGR of 10.47%.

- Rising regulatory bans on single-use plastics are accelerating the shift to biodegradable and compostable packaging solutions.

- Consumer demand for eco-friendly packaging in food, beverage, and personal care industries is driving large-scale adoption.

- High production costs and limited industrial composting infrastructure continue to restrict market scalability in developing regions.

- Europe leads the market with a 36.4% share due to strong environmental policies and early technology adoption.

- North America follows with 29.7%, supported by brand-led sustainability initiatives and growing use in e-commerce packaging.

- Asia Pacific, holding 24.5% share, is emerging rapidly with growing manufacturing capacity and policy-driven domestic production.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Regulatory Pressure to Phase Out Conventional Plastics

Governments worldwide are enforcing strict regulations against single-use plastics, prompting industries to adopt sustainable alternatives. The growing legislative support, including bans and extended producer responsibility schemes, has increased the urgency to replace conventional polymers. Regulatory frameworks in the EU, North America, and parts of Asia are specifically targeting plastic waste reduction. These policies create a favorable environment for the Bioplastics packaging market to grow. The packaging sector, being a major consumer of plastic, is under high pressure to transition. Stakeholders are investing in R&D to meet new compliance standards. Businesses adopting bioplastics can benefit from regulatory incentives. The global push toward a circular economy further reinforces the regulatory-driven demand for bioplastics.

- For example, the European Union’s Single-Use Plastics Directive has eliminated items like plastic straws and cutlery across 27 countries, directly impacting industries to the tune of reducing over 3.4million tons of plastic waste annually.

Surging Consumer Awareness and Environmental Consciousness

Rising awareness about the environmental impact of petroleum-based plastics is shifting consumer preferences toward sustainable options. Increasing eco-consciousness influences purchasing behavior, especially among younger demographics. Brands are under pressure to align with sustainability values, prompting packaging redesigns using bio-based materials. The Bioplastics packaging market benefits from this behavioral transformation, especially in food, personal care, and e-commerce segments. Environmentally friendly packaging has become a key differentiator in competitive markets. Public campaigns and media coverage accelerate the awareness of biodegradable and compostable materials. Consumer-driven demand creates bottom-up pressure on brands and suppliers. The momentum is further strengthened by global sustainability initiatives and certifications.

Corporate Sustainability Goals Driving Product Innovation

Large corporations have set ambitious ESG and net-zero targets, requiring a shift in packaging materials. The transition from fossil-based packaging to bio-based options aligns with decarbonization objectives. The Bioplastics packaging market is gaining traction from these strategic shifts. Multinational brands in food, beverage, and cosmetics are leading the way by integrating bioplastics into their supply chains. Companies are also investing in innovation to improve product functionality while maintaining environmental credentials. Partnerships between manufacturers and bio-polymer producers are becoming common. These collaborations enhance scale, reduce costs, and promote product standardization. The market is also witnessing growing interest in closed-loop packaging systems using bio-based materials.

Technological Advancements in Bioplastic Formulations and Performance

Continuous improvements in bioplastic processing and polymer science are boosting material properties. Newer formulations offer better strength, durability, and barrier protection, meeting industry requirements. These innovations expand the applicability of bioplastics across various packaging types, from rigid containers to flexible films. The Bioplastics packaging market benefits from enhanced processability and compatibility with existing manufacturing equipment. Advancements in compostability and biodegradation further strengthen its environmental value. Technologies enabling multilayer bioplastic structures improve shelf-life for perishable goods. Research institutions and startups are actively developing bio-based additives for enhanced functionality.

- For example, PLA derived from corn starch now achieves tensile strengths between 50 and 70 MPa, making it mechanically comparable to conventional PET in terms of stiffness and strength.

Market Trends:

Integration of Bioplastics into Luxury and Premium Packaging Segments

The luxury packaging segment is increasingly adopting bio-based materials to appeal to eco-conscious high-end consumers. Brands in cosmetics, fashion, and fine beverages are turning to bioplastics for sustainability and aesthetics. This shift is driven by rising demand for premium, sustainable brand experiences. Custom-designed bioplastic containers and finishes are replacing traditional fossil-based plastics. The Bioplastics packaging market is witnessing increased interest from luxury labels seeking differentiation through environmental responsibility. Designers are experimenting with bioplastics that mimic the tactile and visual appeal of conventional polymers. Demand is growing for transparent, glossy, and customizable bioplastic solutions.

- For instance, Amcor collaborated with Bulldog in 2025 to produce luxury skincare tubes that achieved a 16.67% reduction in plastic usage per unit by technically optimizing wall thickness while maintaining necessary squeezability, print quality, and leak resistance.

Growth of Bioplastics in E-commerce and Direct-to-Consumer Channels

The exponential rise of e-commerce is creating new demand for lightweight, protective, and sustainable packaging. Bioplastics are gaining preference in secondary and tertiary packaging used in shipping. The Bioplastics packaging market is expanding through e-commerce platforms that prioritize sustainable shipping solutions. Startups and eco-focused brands are integrating compostable bioplastic mailers, wrapping, and cushioning materials. These packaging types enhance unboxing experiences while reducing environmental impact. Online marketplaces are also incorporating green packaging requirements for sellers. Retailers are responding to customer feedback seeking reduced plastic waste. The e-commerce sector presents a scalable opportunity for bioplastics across global markets.

Circular Economy Models Driving Bioplastic Collection and Reuse Systems

The industry is shifting toward closed-loop systems supported by extended producer responsibility and take-back programs. Bioplastics are being integrated into packaging models that support composting and industrial recycling. The Bioplastics packaging market is responding to circularity mandates by developing traceable and recoverable packaging solutions. Brands are labeling products with disposal instructions and compostability certifications. Municipal infrastructure is evolving to accept and process bioplastics efficiently. Innovative pilot programs are testing community compost bins for bioplastic waste collection. This trend is fostering cross-sector collaboration between municipalities, brands, and consumers.

- For instance, the LIFE RESTART project in Sicily established an industrial process that achieves 75-80% reuse of brewery spent grain (550–600 tonnes annually) for biopolymer production, replacing 300 tonnes of fossil fuel-based plastics per year.

Material Innovation Enabling Hybrid and Composite Bioplastic Solutions

Manufacturers are combining different bio-based polymers to create high-performance hybrid materials. These composites improve flexibility, barrier strength, and temperature resistance. The Bioplastics packaging market is embracing material innovation to meet diverse industry needs. Hybrid solutions support wider application in frozen foods, ready meals, and cosmetics. Companies are integrating cellulose, starch, PLA, and PHA to achieve optimal material behavior. These innovations reduce reliance on single-feedstock sources, improving supply chain resilience. The emergence of bio-nanocomposites is adding mechanical strength and lightweight characteristics. Such trends are helping the market transition from niche applications to mainstream packaging formats.

Market Challenges Analysis:

Cost Competitiveness and Economic Viability Remain Major Constraints

Bioplastics continue to face challenges in achieving price parity with conventional plastics. High raw material costs, complex manufacturing processes, and limited economies of scale contribute to elevated prices. The Bioplastics packaging market must address these barriers to gain wider industry acceptance. Many companies hesitate to switch due to budget constraints or uncertain returns on investment. Bioplastic packaging often requires investment in new machinery or adjustments in production lines. Small- and medium-sized enterprises may find it difficult to absorb added costs. Fluctuations in bio-based feedstock supply and pricing also impact long-term viability. Market expansion depends on achieving cost reductions through innovation, partnerships, and government subsidies.

Infrastructure Gaps and End-of-Life Management Complications

End-of-life management for bioplastics remains underdeveloped in many regions. Composting and recycling infrastructure often fails to differentiate or process bioplastic waste effectively. The Bioplastics packaging market faces challenges with consumer disposal behavior, labeling confusion, and inconsistent waste collection systems. Inadequate composting facilities restrict the environmental benefits of biodegradable packaging. Mismanaged disposal can lead to contamination of recycling streams or landfill accumulation. These issues create skepticism among consumers and stakeholders. Developing harmonized standards and robust end-of-life systems is essential for market credibility. Broader collaboration between regulators, waste managers, and producers is required to close infrastructure gaps.

Market Opportunities:

Expansion of Bioplastics in Emerging Economies with Growing Packaging Needs

Emerging markets in Asia, Latin America, and Africa are experiencing rapid industrialization and rising consumerism. The Bioplastics packaging market can capitalize on this growth by offering sustainable solutions to address rising packaging demand. Government policies promoting green alternatives and foreign investment in local manufacturing further support expansion. Localized production units can reduce import dependency and enable cost-effective scaling. Educational campaigns can help drive consumer awareness and create demand for eco-packaging.

R&D-Focused Innovation Accelerating Application-Specific Bioplastics

The market is seeing strong R&D investment in creating specialized bioplastics for niche applications such as high-barrier films and thermal-resistant containers. The Bioplastics packaging market stands to benefit from these tailored materials that meet stringent industry requirements. Sectors like healthcare, dairy, and electronics need application-specific performance. Companies exploring bio-based additives and functional coatings are unlocking new use cases. These innovations offer competitive differentiation and support premium market positioning.

Market Segmentation Analysis:

The Bioplastics packaging market is segmented

By material type into biodegradable and non-biodegradable categories. Biodegradable materials, including polylactic acid (PLA), starch-based blends, PBAT, and PBS, dominate due to their compostability and alignment with global sustainability targets. PLA and starch blends are widely used in food and consumer goods packaging. PBAT and PBS offer enhanced flexibility and durability, making them suitable for films and wraps. Non-biodegradable materials such as Bio-PE, Bio-PET, and Bio-PA are preferred where mechanical strength and recyclability are essential, particularly in beverage and industrial packaging.

- For instance, NatureWorks, the world’s largest producer of polylactic acid (PLA), operates the Ingeo biopolymer plant in Blair, Nebraska, with an annual output exceeding 150,000 metric tonnes.

By packaging type, the market includes both rigid and flexible formats. Flexible packaging, such as films, pouches, sachets, and bags, leads in volume due to its cost-efficiency and widespread use in food and personal care products. Rigid formats, including bottles, jars, trays, and clamshells, are growing steadily in applications demanding structural integrity. It supports a wide range of packaging types while promoting circular and sustainable solutions.

- For instance, Novamont’s Mater-Bi™ film grades have been validated for high-barrier performance and compostability, achieving >95% biodegradation in less than 90 days, meeting EN 13432 standards for food-contact applications.

By application, includes food, beverages, pharmaceuticals, personal care, industrial packaging, and consumer goods. Food and beverage segments lead due to high consumption and strict regulatory demands for sustainable packaging. Personal care and household product segments are gaining momentum as brands invest in eco-friendly retail packaging. Pharmaceutical and industrial applications are adopting bio-based options to meet green compliance standards and enhance environmental performance. Each application contributes to the expanding footprint of bioplastics across global supply chains.

Segmentation:

By Material Type

- Biodegradable Materials:

- Polylactic Acid (PLA)

- Starch-Based Blends

- Polybutylene Adipate Terephthalate (PBAT)

- Polybutylene Succinate (PBS)

- Other Biodegradable Polymers

- Non-Biodegradable Materials:

- Bio-Based Polyethylene (Bio-PE)

- Bio-Based Polyethylene Terephthalate (Bio-PET)

- Bio-Based Polyamide (Bio-PA)

- Other Non-Biodegradable Bioplastics

By Packaging Type

- Rigid Packaging:

- Flexible Packaging

By Product Type

- Films and Wraps

- Pouches and Sachets

- Bags

- Bottles and Jars

- Trays and Containers

- Clamshells

- Cups

- Other Flexible Formats

By Application

- Food Packaging

- Beverage Packaging

- Pharmaceutical Packaging

- Personal Care and Household Products

- Industrial Packaging

- Consumer Goods

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

Europe holds the largest share of the Bioplastics packaging market, accounting for 36.4% of the global revenue in 2024. The region leads due to strong regulatory frameworks, widespread consumer awareness, and the early adoption of green packaging solutions. Countries like Germany, France, Italy, and the Netherlands are front-runners in implementing bioplastics across food, personal care, and industrial packaging. Strict EU directives targeting plastic waste and single-use materials are driving the demand for biodegradable alternatives. Public-private partnerships and funding for bio-economy projects support regional innovation and production capacity. Strong infrastructure for composting and waste management further accelerates bioplastics adoption.

North America represents 29.7% of the global Bioplastics packaging market in 2024, driven by sustainability commitments from major consumer brands and regulatory developments in states such as California and New York. The market is gaining traction across foodservice, consumer electronics, and pharmaceuticals. Companies in the U.S. and Canada are incorporating bio-based polymers into packaging portfolios to meet ESG goals and appeal to environmentally conscious consumers. It benefits from robust R&D capabilities and growing investment in compostable packaging technologies. Retail chains and e-commerce platforms are also pushing suppliers to transition to sustainable materials. Industrial composting infrastructure remains a challenge in parts of the region but is improving.

Asia Pacific holds a 24.5% share of the Bioplastics packaging market in 2024 and is expected to grow rapidly over the forecast period. China, Japan, India, and South Korea are driving regional growth through rising industrialization, increasing plastic waste concerns, and growing consumer demand for eco-friendly packaging. Government initiatives supporting bio-economy development and green manufacturing are encouraging domestic bioplastics production. Regional startups and multinationals are expanding local operations to meet demand and reduce import dependency. The food and beverage and retail sectors are primary adopters of bioplastic packaging in urban areas. It faces scalability and end-of-life challenges, but innovation and infrastructure investment are gaining momentum.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Amcor plc

- Novamont S.p.A

- NatureWorks LLC

- Mondi plc

- BASF SE

- Braskem S.A.

- Corbion N.V.

- Sealed Air Corporation

- TIPA Corp Ltd.

- Huhtamaki

- ALPLA

- Constantia Flexibles Group GmbH

- Mitsubishi Chemical Corporation

- Arkema S.A.

- Biome Bioplastics Limited

Competitive Analysis:

The Bioplastics packaging market is moderately fragmented, with a mix of global players and regional specialists competing on innovation, pricing, and sustainability credentials. Leading companies such as NatureWorks, BASF SE, Novamont S.p.A., and Total Corbion PLA dominate through strong R&D capabilities and extensive distribution networks. These firms focus on product differentiation by developing compostable and bio-based packaging materials tailored to industry needs. Strategic collaborations between biopolymer producers and packaging converters are enhancing product integration and market reach. Emerging players are introducing niche applications and targeting local markets with cost-effective alternatives. The market rewards players who demonstrate end-to-end sustainability, from sourcing to disposal. Competitive intensity is increasing with rising demand and regulatory pressure. Companies that offer certified, high-performance materials aligned with circular economy principles are capturing a larger customer base.

Recent Developments:

- In July 2025, Amcor plc continued its focus on sustainable packaging by launching a collaborative refill pouch for Nana laundry and cleaning products with Mediacor. This new 2-liter spouted stand-up pouch targets the cleaning product segment and was introduced on July 11, 2025, highlighting Amcor’s commitment to innovative and eco-friendly solutions.

- In June 2024, Novamont S.p.A coordinated the kickoff of the TERRIFIC project, a European Union-funded initiative aimed at developing eight innovative biobased packaging solutions. This €16 million project involves 19 partners and seeks to showcase the full potential of biodegradable materials to improve packaging circularity and resource efficiency in Europe.

- In Feb2025, Mondi plc introduced new office paper brands—IQ ULTRA and MAESTRO expert—expanding their portfolio of sustainable options for the European market. In December 2024, Mondi also announced a paper-based, stand-up pouch for dishwashing tabs in partnership with Proquimia, offering a recyclable, paper-rich alternative to plastic packaging for Spanish and Portuguese consumers

Market Concentration & Characteristics

The Bioplastics packaging market features medium market concentration with several dominant players holding significant share. It exhibits strong innovation cycles, driven by evolving sustainability demands and changing regulatory frameworks. Key characteristics include a high degree of material customization, industry-specific applications, and rapid technological advancements in polymer science. The market is shaped by environmental compliance requirements, cost competitiveness, and the ability to scale sustainable solutions efficiently. End users seek packaging that meets performance standards while aligning with eco-conscious branding. Regional production and sourcing strategies play a vital role in maintaining competitiveness across global supply chains.

Report Coverage:

The research report offers an in-depth analysis based on Material Type, Packaging Type, Product type and Application, It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Demand for bioplastics in flexible and rigid packaging formats will continue to grow across food, beverage, and personal care industries.

- Regulatory support and plastic bans will accelerate the shift toward biodegradable and compostable packaging materials.

- Innovation in high-barrier and thermal-resistant bioplastics will expand application in frozen foods and pharmaceuticals.

- E-commerce packaging will emerge as a key growth area for lightweight and compostable bioplastic solutions.

- Asia Pacific will witness the fastest adoption due to rising consumer demand and expanding manufacturing capacity.

- Circular economy models will influence packaging design, collection systems, and end-of-life strategies.

- Strategic alliances between biopolymer producers and FMCG brands will increase to ensure product scalability.

- Investment in industrial composting and recycling infrastructure will support broader bioplastics adoption.

- Premium and luxury brands will drive demand for customized, bio-based packaging with aesthetic appeal.

- Government funding and R&D initiatives will focus on developing next-generation bio-based polymers.