Market Overview:

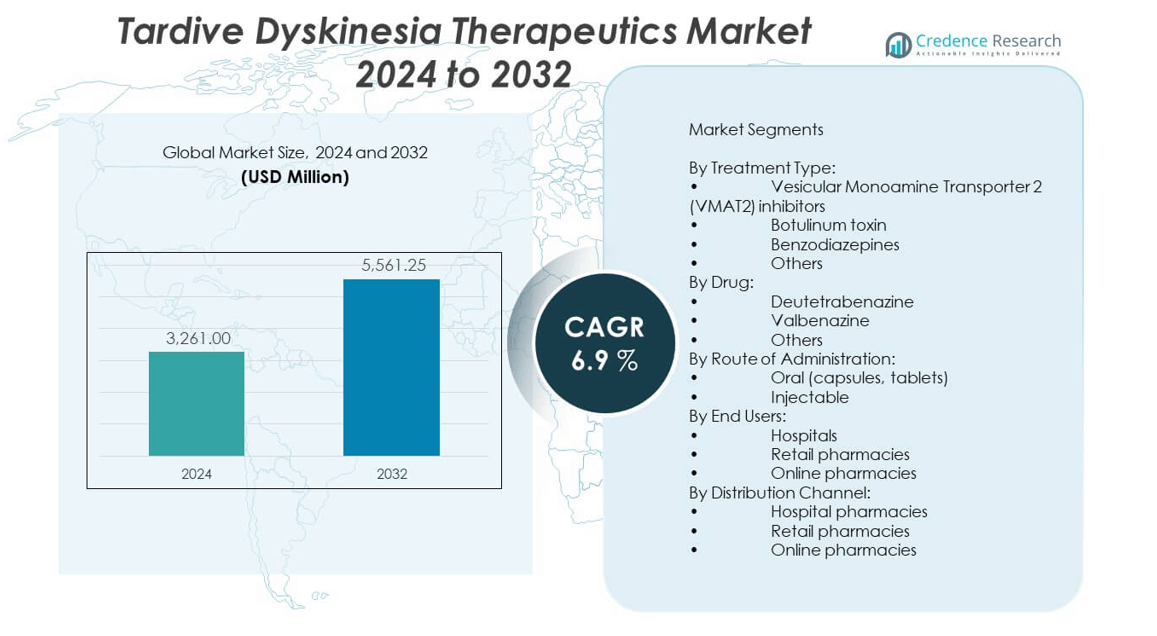

The tardive dyskinesia therapeutics market is projected to grow from USD 3,261 million in 2024 to an estimated USD 5,561.25 million by 2032, with a compound annual growth rate (CAGR) of 6.9% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Tardive Dyskinesia Therapeutics Market Size 2024 |

USD 3,261 million |

| Tardive Dyskinesia Therapeutics Market, CAGR |

6.9% |

| Tardive Dyskinesia Therapeutics Market Size 2032 |

USD 5,561.25 million |

The market growth is fueled by an increasing prevalence of schizophrenia, bipolar disorder, and other psychiatric conditions that require long-term antipsychotic therapy, which heightens the risk of tardive dyskinesia. Rising patient awareness, improved diagnostic capabilities, and proactive screening practices are boosting early intervention rates. Pharmaceutical companies are intensifying research into novel drug formulations, combination therapies, and extended-release options, enhancing treatment effectiveness while minimizing side effects, thereby expanding the market potential.

North America leads the tardive dyskinesia therapeutics market, supported by advanced healthcare infrastructure, high awareness levels, and strong availability of approved treatment options. Europe follows closely, driven by government-backed mental health programs and increased psychiatric care accessibility. The Asia-Pacific region is emerging as a high-potential market due to growing healthcare investments, rising mental health awareness, and expanding access to modern psychiatric treatments in countries such as China and India. Latin America and the Middle East & Africa are gradually adopting advanced therapies, driven by healthcare modernization and the presence of international pharmaceutical companies.

Market Insights:

- The tardive dyskinesia therapeutics market was valued at USD 3,261 million in 2024 and is projected to reach USD 5,561.25 million by 2032, growing at a CAGR of 6.9% during the forecast period.

- Rising prevalence of psychiatric disorders such as schizophrenia and bipolar disorder, requiring long-term antipsychotic use, is increasing the risk and diagnosis rates of tardive dyskinesia.

- Advancements in drug development, particularly VMAT2 inhibitors, are enhancing treatment efficacy, improving patient quality of life, and driving adoption across healthcare systems.

- High treatment costs and limited access in low- and middle-income countries remain key restraints, restricting adoption despite growing awareness.

- North America dominates the market, supported by advanced healthcare infrastructure, early adoption of innovative drugs, and strong reimbursement frameworks.

- Europe maintains steady growth through structured mental health programs, favorable reimbursement, and widespread availability of specialized treatment centers.

- Asia-Pacific is the fastest-growing region, fueled by expanding psychiatric care infrastructure, rising mental health awareness, and increased investments in healthcare access.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Prevalence of Psychiatric Disorders Increasing Tardive Dyskinesia Risk:

The tardive dyskinesia therapeutics market is strongly driven by the growing incidence of schizophrenia, bipolar disorder, and other chronic psychiatric conditions that require long-term antipsychotic therapy. Increased reliance on first- and second-generation antipsychotics elevates the risk of developing tardive dyskinesia among patients, thereby driving demand for effective treatments. Greater public and clinical awareness of the condition has led to earlier diagnosis and timely intervention. Improved access to psychiatric care in both developed and emerging markets is expanding the patient pool eligible for therapy. Efforts to integrate tardive dyskinesia screening into routine psychiatric care have enhanced detection rates. Hospitals and specialized mental health clinics are increasingly adopting standardized diagnostic protocols. Expansion of healthcare infrastructure is enabling better management of neurological side effects. The market is further strengthened by government initiatives promoting mental health awareness.

Advancements in Drug Development Enhancing Treatment Options:

Innovation in the pharmaceutical sector is accelerating the growth of the tardive dyskinesia therapeutics market. The introduction of VMAT2 inhibitors has significantly improved symptom control compared to older treatment methods. Drug developers are focusing on extended-release formulations to ensure sustained therapeutic effects and improved patient compliance. Companies are also investing in combination therapies that target both motor symptoms and underlying psychiatric conditions. Clinical trials are increasingly exploring new molecular targets, expanding the pipeline of potential therapeutics. Regulatory agencies are prioritizing the approval of novel drugs that demonstrate both efficacy and safety in reducing tardive dyskinesia symptoms. The rising number of industry collaborations and licensing agreements is fostering innovation. Strategic partnerships between biotech firms and large pharmaceutical companies are streamlining drug development and commercialization processes.

- For instance, Clinical pipelines are diversifying to include agents targeting neurotransmitter modulation, synaptic plasticity, and anti-inflammatory pathways, with advanced modalities such as biologics and gene therapies under investigation.

Expanding Healthcare Access and Insurance Coverage Supporting Market Growth:

Wider healthcare access is a key driver for the tardive dyskinesia therapeutics market, particularly in emerging economies where psychiatric care is becoming more accessible. Expansion of insurance coverage for mental health services ensures that more patients can afford long-term treatment. Reimbursement policies in developed nations are increasingly recognizing tardive dyskinesia as a distinct condition warranting specialized care. Telemedicine adoption is helping extend neurological consultation services to rural and underserved areas. Governments and non-profits are launching awareness campaigns that highlight the importance of early treatment. Expansion of psychiatric hospital networks is providing more points of care for affected individuals. Integration of tardive dyskinesia treatment protocols into general neurology practices is also boosting patient reach. Growing collaboration between private and public healthcare systems is improving therapy accessibility.

Growing Clinical Awareness Among Healthcare Professionals:

Increased clinical training and education are fueling growth in the tardive dyskinesia therapeutics market. Healthcare professionals are now better equipped to differentiate tardive dyskinesia from other movement disorders, leading to accurate diagnosis. Medical associations are issuing updated guidelines for antipsychotic use and tardive dyskinesia monitoring. The availability of diagnostic scales such as the Abnormal Involuntary Movement Scale (AIMS) is enabling structured assessments. Continuing medical education (CME) programs are spreading knowledge about emerging treatment options. Hospitals are integrating tardive dyskinesia screening into standard psychiatric evaluations. Pharmaceutical companies are conducting targeted physician outreach to improve therapy adoption. Cross-specialty collaboration between psychiatrists, neurologists, and primary care physicians is enhancing patient outcomes. The expansion of academic research is driving evidence-based clinical practices.

Market Trends:

Rising Integration of Digital Health Tools in Treatment Pathways:

The tardive dyskinesia therapeutics market is witnessing increased adoption of digital health solutions for patient monitoring and therapy optimization. Wearable devices and mobile health apps are enabling real-time tracking of involuntary movements, allowing clinicians to adjust treatment plans promptly. Teleconsultation platforms are reducing barriers to specialist care for patients in remote areas. AI-powered diagnostic tools are emerging to assist in early detection and progression tracking. Cloud-based patient records are enhancing coordination between psychiatric and neurological care teams. Pharmaceutical companies are partnering with digital health firms to create patient engagement platforms. Data analytics is being applied to identify treatment response patterns and improve clinical decision-making. Virtual clinical trials are accelerating drug development timelines.

- For instance, the TD treatment landscape incorporates digital health innovations. Pharmaceutical companies are collaborating with technology firms to leverage wearable devices and mobile apps for continuous, real-time monitoring of involuntary movements, enabling timely treatment adjustments. AI-powered diagnostic tools and cloud-based patient record systems facilitate early detection, progression tracking, and multidisciplinary care coordination among psychiatric and neurological specialists.

Increasing Pipeline Diversification and Target Expansion:

The drug development pipeline for the tardive dyskinesia therapeutics market is expanding beyond VMAT2 inhibitors to include new classes of compounds. Research is targeting neurotransmitter modulation, synaptic plasticity enhancement, and anti-inflammatory mechanisms. Companies are exploring multi-action drugs that address both motor dysfunction and psychiatric comorbidities. Biologics and gene therapies are under investigation as potential long-term solutions. Orphan drug designations are being sought to incentivize innovation in this specialized therapeutic area. Global collaboration between research institutions is accelerating the sharing of clinical data. Fast-track regulatory designations are shortening approval timelines for promising candidates. The diversification of therapeutic targets is expected to create a more competitive market landscape.

- For instance, AI-powered diagnostic tools and cloud-based patient record systems facilitate early detection, progression tracking, and multidisciplinary care coordination among psychiatric and neurological specialists. These digital solutions improve patient engagement and drive precision medicine approaches, while virtual clinical trials accelerate drug development cycles.

Growing Patient Advocacy and Awareness Campaigns:

Patient advocacy groups are becoming influential in shaping the tardive dyskinesia therapeutics market. Campaigns are increasing public understanding of the condition and reducing stigma associated with movement disorders. Advocacy organizations are lobbying for broader insurance coverage and faster drug approvals. Educational webinars and patient-led forums are empowering individuals to seek timely treatment. Collaboration between advocacy groups and pharmaceutical companies is producing patient-friendly informational materials. Social media outreach is amplifying awareness messages to a global audience. Fundraising initiatives are supporting research into novel therapeutic approaches. Community-based events are fostering local support networks for affected individuals.

Expansion of Real-World Evidence Studies to Support Clinical Practice:

The use of real-world evidence (RWE) is gaining momentum in the tardive dyskinesia therapeutics market. Post-marketing surveillance studies are providing long-term safety and efficacy data for approved drugs. Registries are being developed to track treatment outcomes across diverse patient populations. RWE is helping identify subgroups of patients who respond best to specific therapies. Health economics studies are demonstrating the cost-effectiveness of early intervention. Data from routine clinical practice is being used to refine dosing protocols and treatment algorithms. Payers are increasingly requiring RWE to support reimbursement decisions. Academic journals are publishing more RWE-based studies, reinforcing clinical confidence in approved treatments. Collaborative RWE projects between healthcare providers and pharmaceutical companies are expanding the knowledge base.

Market Challenges Analysis:

High Treatment Costs and Limited Accessibility in Certain Regions:

The tardive dyskinesia therapeutics market faces significant barriers due to the high cost of advanced therapies, particularly VMAT2 inhibitors. For many patients in low- and middle-income countries, these treatments remain unaffordable without insurance or government subsidies. Even in developed markets, out-of-pocket expenses can limit patient adherence. Limited availability of specialized neurological care in rural and underserved areas further restricts access. Delays in reimbursement approvals hinder timely treatment initiation. Patients often experience financial strain due to the need for long-term medication. Generic options remain scarce, keeping prices elevated. Pharmaceutical companies face challenges balancing profitability with affordability. Lack of local manufacturing in emerging economies adds to cost burdens.

Underdiagnosis and Delayed Intervention Affecting Outcomes:

The tardive dyskinesia therapeutics market also struggles with widespread underdiagnosis, as symptoms can be mistaken for other movement disorders. Many healthcare professionals in general practice settings lack specific training to recognize early signs. Stigma associated with psychiatric conditions may discourage patients from reporting symptoms. Delayed diagnosis often results in advanced disease progression, reducing treatment efficacy. Awareness gaps in community healthcare settings contribute to missed intervention opportunities. The lack of standardized screening protocols in many countries prolongs the time between symptom onset and treatment initiation. Inadequate patient education limits self-reporting of early symptoms. This diagnostic lag directly impacts long-term patient quality of life and market potential.

Market Opportunities:

Expansion of Therapeutic Options Through Pipeline Innovation:

The tardive dyskinesia therapeutics market holds strong potential for growth through the development of next-generation therapies. Companies are advancing research into novel drug classes targeting multiple neurological pathways. Opportunities exist for biologics and neuroprotective agents that offer longer-term benefits. Smaller biotech firms are leveraging partnerships with major pharmaceutical companies to accelerate commercialization. Expedited regulatory pathways for breakthrough therapies can shorten market entry timelines. Drug repurposing strategies could introduce cost-effective alternatives. The growing use of precision medicine opens avenues for individualized treatment approaches.

Growing Penetration in Emerging Healthcare Markets:

Rising healthcare investments in Asia-Pacific, Latin America, and the Middle East present significant opportunities for the tardive dyskinesia therapeutics market. Expansion of psychiatric care infrastructure in countries like India, China, and Brazil is enabling earlier diagnosis. Government health programs are gradually expanding coverage for neurological and psychiatric conditions. Training initiatives for healthcare professionals are improving diagnostic accuracy. Partnerships with local distributors can strengthen market penetration. Increasing patient advocacy in these regions is fostering demand for advanced treatment options. Affordable drug versions could secure a competitive edge in these price-sensitive markets.

Market Segmentation Analysis:

By Treatment Type

In the tardive dyskinesia therapeutics market, Vesicular Monoamine Transporter 2 (VMAT2) inhibitors hold the dominant share due to their proven efficacy and favorable safety profile in managing involuntary movements. Botulinum toxin serves as an alternative for targeted symptom control, while benzodiazepines are generally prescribed as adjunct therapies to manage anxiety or muscle tension. The “others” category includes off-label drugs and emerging options catering to specific patient needs or treatment-resistant cases.

- For instance, VMAT2 inhibitors dominate the market, followed by alternatives like botulinum toxin for localized symptom control and benzodiazepines used adjunctively for anxiety and muscle tension management.

By Drug

Valbenazine leads in both revenue and usage, supported by strong clinical adoption and extensive physician familiarity. Deutetrabenazine holds a significant position, offering a viable alternative with differentiated dosing benefits. Other drugs, such as amantadine, tetrabenazine, and clonazepam, are used in niche or off-label applications, contributing to therapeutic diversity and expanding patient management options.

- For instance, Industry trends include strategic partnerships between biotech firms and large pharmaceutical companies to streamline drug development and commercialization pathways, emphasizing patient-centered outcomes and regulatory compliance.

By Route of Administration

Oral formulations, including capsules and tablets, represent the largest segment, driven by patient convenience, ease of dosing, and better adherence rates. Injectable options, while less common, are utilized in cases requiring targeted delivery or specialized clinical intervention.

By End Users

Hospitals dominate the end-user segment due to the availability of specialist care, diagnostic facilities, and comprehensive management plans. Retail pharmacies play a key role in dispensing maintenance medications, while online pharmacies are gaining traction for their convenience and home delivery services.

By Distribution Channel

Hospital pharmacies hold the largest share, reflecting their role in initiating and managing specialist-driven therapies. Retail pharmacies support continuity of care in community settings, and online pharmacies are expanding access, particularly for chronic therapy management.

Segmentation:

By Treatment Type:

- Vesicular Monoamine Transporter 2 (VMAT2) inhibitors

- Botulinum toxin

- Benzodiazepines

- Others

By Drug:

- Deutetrabenazine

- Valbenazine

- Others

By Route of Administration:

- Oral (capsules, tablets)

- Injectable

By End Users:

- Hospitals

- Retail pharmacies

- Online pharmacies

By Distribution Channel:

- Hospital pharmacies

- Retail pharmacies

- Online pharmacies

By Region:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America Holding a Dominant Share Through Strong Infrastructure

North America leads the tardive dyskinesia therapeutics market, holding the largest market share due to its advanced healthcare infrastructure and high awareness among healthcare professionals. The region benefits from early adoption of novel drug therapies, strong insurance coverage, and active patient advocacy. The United States, in particular, drives growth with a large diagnosed patient base and robust pharmaceutical R&D activity. The presence of key market players ensures continuous product availability. Public health campaigns and continuing medical education programs maintain high detection rates.

Europe Maintaining Steady Growth Through Policy Support

Europe holds the second-largest market share, supported by structured mental health programs and favorable reimbursement frameworks. Countries such as Germany, the UK, and France are at the forefront due to their comprehensive healthcare systems. Widespread availability of VMAT2 inhibitors and specialized neurological clinics supports treatment uptake. Government-backed awareness initiatives and integration of tardive dyskinesia screening into psychiatric care contribute to market expansion. Cross-border clinical collaborations and EU regulatory harmonization foster innovation. Eastern European nations are gradually increasing access through healthcare modernization.

Asia-Pacific Emerging as a High-Growth Market

Asia-Pacific is the fastest-growing regional segment of the tardive dyskinesia therapeutics market, driven by expanding healthcare infrastructure and rising mental health awareness. China, Japan, and India are leading the growth with significant investments in psychiatric care services. Government health reforms are improving access to advanced neurological treatments. Rising disposable incomes enable more patients to seek specialized care. Partnerships between multinational pharmaceutical firms and local companies are enhancing drug availability. Training programs for healthcare workers are improving diagnostic accuracy. This growth potential is attracting new entrants and investments in the region.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Neurocrine Biosciences, Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Lundbeck A/S (Denmark)

- AbbVie Inc. (U.S.)

- Otsuka Holdings Co., Ltd. (Japan)

- Astellas Pharma Inc. (Japan)

- Bausch Health Companies Inc. (Canada)

- Sumitomo Pharma America, Inc. (U.S.)

- Reviva Pharmaceuticals Holdings, Inc. (U.S.)

- Acadia Pharmaceuticals Inc. (U.S.)

Competitive Analysis:

The tardive dyskinesia therapeutics market is highly competitive, with major players focusing on innovation, strategic collaborations, and geographic expansion. Companies are prioritizing the development of advanced VMAT2 inhibitors and exploring novel therapeutic targets to maintain competitive advantage. The presence of established pharmaceutical firms ensures robust product pipelines and continuous clinical research. Partnerships with healthcare providers, advocacy groups, and research institutions enhance market reach and patient engagement. Competition is further shaped by regulatory approvals, pricing strategies, and reimbursement frameworks. Smaller biotech firms are leveraging niche innovations to capture market segments, while larger companies maintain dominance through brand recognition and global distribution networks.

Recent Developments:

- In 2025, Neurocrine Biosciences announced new data from a Phase 4 randomized withdrawal study demonstrating that continued treatment with INGREZZA® (valbenazine) significantly improves health-related quality of life and functional status in adults aged 65 and older with tardive dyskinesia. This data was presented at the American Association of Nurse Practitioners National Conference in June 2025, highlighting the durable benefits of INGREZZA beyond symptom control.

- In May 2025, Neurocrine Biosciences presented positive Phase 2 study results for NBI-1117568, an investigational oral selective muscarinic M4 receptor agonist being developed for schizophrenia treatment. The study showed significant symptom improvement and favorable safety and tolerability profiles. This advancement marks a potential next-generation therapy linked to neuropsychiatric conditions associated with tardive dyskinesia, with a registrational Phase 3 program planned.

- In May 2025, Neurocrine also launched the “ConnectING with Carnie” campaign featuring mental health advocate Carnie Wilson to reduce stigma, raise awareness, and promote early screening and treatment for tardive dyskinesia, enhancing patient engagement and education.

Market Concentration & Characteristics:

The tardive dyskinesia therapeutics market is moderately concentrated, with a few leading pharmaceutical companies holding substantial market shares through patented products and established distribution networks. It is characterized by high barriers to entry due to stringent regulatory requirements, significant R&D investments, and the need for strong clinical evidence. The market’s growth trajectory is shaped by innovation cycles, with VMAT2 inhibitors currently dominating treatment protocols. Strategic partnerships, mergers, and acquisitions are common as companies seek to expand portfolios and geographic reach.

Report Coverage:

The research report offers an in-depth analysis based on treatment types, drug classes, routes of administration, end users, and distribution channels. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Expansion of next-generation VMAT2 inhibitors with enhanced safety profiles.

- Increased market penetration in emerging economies through affordability programs.

- Greater integration of AI-assisted diagnosis into clinical workflows.

- Development of combination therapies addressing psychiatric comorbidities.

- Stronger patient advocacy influencing reimbursement policies.

- Growth in telemedicine-based neurology consultations.

- Diversification of drug pipeline beyond VMAT2 mechanisms.

- Rising adoption of extended-release formulations for improved compliance.

- Increased use of real-world evidence to guide treatment protocols.

- Entry of biosimilars once key patents expire.