Market Overview:

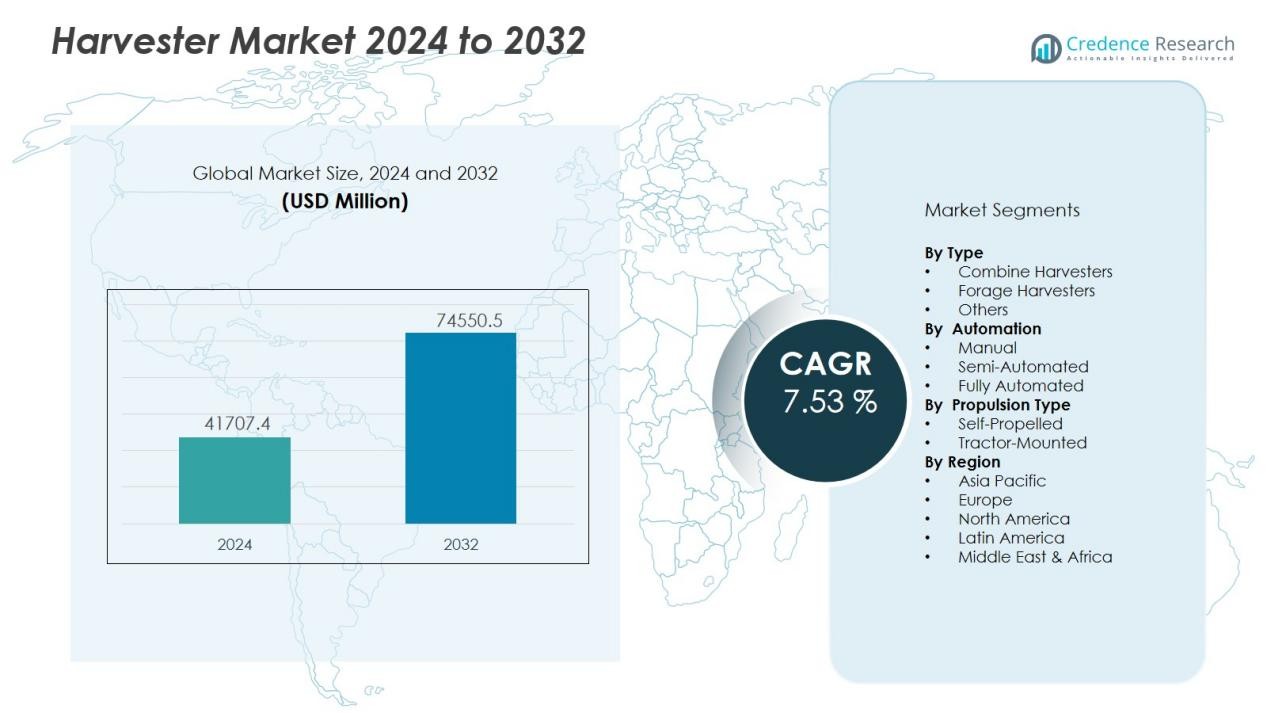

The harvester market size was valued at USD 41707.4 million in 2024 and is anticipated to reach USD 74550.5 million by 2032, at a CAGR of 7.53 % during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Harvester Market Size 2024 |

USD 41707.4 Million |

| Harvester Market, CAGR |

7.53 % |

| Harvester Market Size 2032 |

USD 74550.5 Million |

Growth in the harvester market is fueled by factors such as labor shortages in the agricultural sector, rising farm sizes, and government initiatives promoting farm mechanization. The integration of precision agriculture technologies, GPS guidance, IoT connectivity, and AI-enabled analytics is enhancing machine performance and reducing operational costs. In addition, the trend toward sustainable farming practices is prompting manufacturers to develop energy-efficient, low-emission harvesters that align with environmental regulations and farmers’ cost-saving goals.

Regionally, North America and Europe maintain strong market positions due to high technology adoption rates, advanced farming infrastructure, and supportive subsidy programs. The Asia-Pacific region is expected to record the fastest growth, driven by increasing agricultural investments in China, India, and Southeast Asia, where growing populations and food security concerns are accelerating the shift toward modern harvesting equipment. Latin America is also emerging as a promising market, supported by expanding commercial farming operations.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The harvester market was valued at USD 41,707.4 million in 2024 and is projected to reach USD 74,550.5 million by 2032, growing at a CAGR of 7.53% from 2024 to 2032.

- Labor shortages, expanding farm sizes, and supportive government mechanization programs are driving adoption of modern harvesting machinery.

- Precision agriculture integration, GPS guidance, IoT connectivity, and AI-enabled analytics are enhancing operational efficiency and reducing costs.

- Sustainability trends are prompting demand for fuel-efficient, low-emission, and recyclable harvester models aligned with environmental regulations.

- North America holds 32% market share and Europe 28%, supported by advanced infrastructure, high technology adoption, and subsidy programs.

- Asia-Pacific holds 25% market share and is the fastest-growing region, fueled by agricultural investments, subsidy initiatives, and rising food security concerns.

- Latin America holds 9% market share and the Middle East & Africa 6%, with growth supported by agribusiness expansion, export-oriented production, and modernization initiatives.

Market Drivers:

Rising Global Demand for Food Production Driving Mechanization:

The harvester market is expanding due to the growing need to increase agricultural output to meet the food requirements of a rising global population. Farmers are adopting modern harvesting machinery to improve yield efficiency and reduce post-harvest losses. It enables faster operations compared to manual labor, allowing timely harvesting of crops in peak seasons. This shift toward mechanization is critical in regions facing labor shortages, where machines ensure consistent productivity. The demand for high-capacity harvesters is particularly strong in commercial farming sectors.

Technological Advancements Enhancing Operational Efficiency:

Innovations in harvester design and technology are transforming the market landscape. Manufacturers are integrating GPS guidance, precision farming tools, and IoT-enabled monitoring systems to optimize harvesting processes. It improves operational accuracy, reduces fuel consumption, and minimizes waste. These advancements also allow farmers to track performance metrics in real time, enabling informed decision-making. The incorporation of automation and AI capabilities is further enhancing efficiency in large-scale agricultural operations.

- For instance, John Deere’s S700 Series combines utilize the JDLink system, providing farmers with real-time machine data and enabling remote diagnostics for over 150 machine parameters.

Government Support and Subsidy Programs Encouraging Adoption:

Government initiatives promoting farm mechanization are a major growth driver for the harvester market. Subsidies, tax incentives, and low-interest financing options are helping farmers invest in modern equipment. It supports agricultural modernization and boosts rural economic development. In emerging economies, these programs are bridging the gap between traditional practices and advanced farming methods. The policy focus on food security is accelerating the replacement of outdated machinery with advanced harvesters.

Shift Toward Sustainable and Cost-Efficient Farming Solutions:

Sustainability concerns are shaping equipment preferences in the harvester market. Farmers are increasingly selecting fuel-efficient, low-emission models that meet environmental regulations and reduce operating costs. It aligns with global efforts to minimize the carbon footprint of agriculture. Manufacturers are responding by developing harvesters with alternative power sources and recyclable components. This focus on sustainable solutions is fostering long-term adoption and market growth.

- For instance, CLAAS’s LEXION 8900 Terra Trac model reduces ground compaction by 20 percent while maintaining throughput, thanks to its full-body rubber track system.

Market Trends:

Integration of Precision Agriculture and Smart Technologies:

The harvester market is witnessing a strong shift toward precision agriculture, with advanced sensors, GPS guidance, and data analytics becoming standard features. Farmers are leveraging these tools to monitor crop health, optimize harvesting schedules, and reduce waste. It enables more accurate operations, improving yield quality and minimizing resource use. The adoption of IoT-enabled harvesters allows real-time performance tracking, predictive maintenance, and remote diagnostics. Automation and AI integration are enhancing machine adaptability to varying field conditions, increasing efficiency in large-scale farming. Manufacturers are focusing on user-friendly interfaces and compatibility with farm management software to streamline operations.

- For instance, John Deere’s 8R Series combines equipped with the StarFire 6000 GPS receiver achieve repeatable accuracy of 2.5 cm, enabling pinpoint field positioning.

Growing Demand for Sustainable and Multi-Crop Harvesting Solutions:

Sustainability is shaping design trends, with manufacturers prioritizing fuel-efficient engines, hybrid power systems, and recyclable components. The harvester market is moving toward models that can handle multiple crop types, reducing the need for separate machinery and lowering operational costs. It addresses the needs of farmers managing diverse crop rotations and varying seasonal demands. The demand for compact and versatile harvesters is also increasing in small and medium-sized farms, especially in emerging economies. Manufacturers are responding with modular designs that allow customization based on crop and terrain requirements. These trends are positioning advanced, eco-friendly, and adaptable harvesters as key drivers of the next growth phase in the market.

- For instance, John Deere’s X9 1100 combine achieved a throughput of 115 tonnes per hour during independent PAMI benchmark testing, demonstrating both high capacity and fuel efficiency without compromise

Market Challenges Analysis:

High Initial Investment and Maintenance Costs Limiting Adoption:

The harvester market faces challenges due to the high purchase price and ongoing maintenance expenses of advanced machinery. Many small and medium-scale farmers in developing regions struggle to justify the investment without substantial financial support. It requires periodic servicing, replacement parts, and skilled operators, which add to operational costs. Fluctuations in agricultural commodity prices can further delay equipment purchases. Limited access to affordable financing options restricts modernization in rural areas. These cost-related barriers slow down the pace of mechanization in certain markets.

Seasonal Usage and Operational Constraints Affecting Efficiency:

Harvesters are typically used during specific crop seasons, leading to long idle periods and underutilization of assets. The harvester market also faces challenges from diverse terrain and crop conditions that require specialized models, increasing complexity for farmers managing multiple crops. It can be difficult to transport large machinery across rural regions with inadequate infrastructure. Weather variability and unpredictable climate patterns can shorten harvesting windows, reducing machine efficiency. In emerging economies, limited availability of trained operators impacts optimal usage. These operational constraints influence purchase decisions and affect market penetration rates.

Market Opportunities:

Expansion Potential in Emerging Agricultural Economies:

The harvester market holds significant growth potential in developing regions where mechanization rates remain low. Rising farm incomes, government subsidies, and infrastructure development are creating favorable conditions for adoption. It is expected to benefit from large-scale agricultural investments in countries such as India, Brazil, and parts of Africa. The transition from manual harvesting to modern machinery can substantially improve productivity and reduce labor dependency. Increasing demand for food security solutions will drive adoption in both commercial and smallholder farming. Manufacturers can capture market share by offering cost-effective, durable, and region-specific models.

Technological Innovation Creating New Revenue Streams:

Advancements in automation, connectivity, and sustainable engineering are opening new opportunities in the harvester market. The development of electric and hybrid-powered harvesters aligns with global emission reduction goals and appeals to environmentally conscious farmers. It offers scope for aftermarket services, predictive maintenance, and software-based upgrades to enhance equipment lifespan. Demand for multi-crop and modular designs is rising, allowing farmers to optimize machinery for diverse agricultural needs. Integration with precision farming systems will create value-added solutions, strengthening brand loyalty. These innovations can help manufacturers differentiate themselves and expand into untapped segments.

Market Segmentation Analysis:

By Type:

The harvester market is segmented into combine harvesters, forage harvesters, and others. Combine harvesters hold the dominant share due to their ability to perform multiple operations, including reaping, threshing, and winnowing, in a single process. Forage harvesters are witnessing steady growth in livestock-focused regions, driven by demand for high-quality silage. It is also seeing interest in specialized harvesters for crops such as sugarcane and root vegetables, particularly in markets with crop-specific farming. Manufacturers are focusing on enhancing versatility to cater to diverse agricultural needs.

- For instance, CLAAS JAGUAR 960 forage harvester achieved throughputs of up to 236 tonnes of fresh mash per hour during testing, with specific fuel consumption rates as low as 0.47 litres per tonne of harvested material.

By Automation:

The market is divided into manual, semi-automated, and fully automated harvesters. Fully automated models are gaining traction due to labor shortages, precision agriculture integration, and higher productivity benefits. Semi-automated systems remain popular among mid-scale farmers seeking cost efficiency with partial automation features. Manual harvesters still hold relevance in smaller farms with limited budgets or fragmented landholdings. It reflects a clear shift toward smart, sensor-enabled solutions in developed regions.

- For instance, AGCO’s Ideal combine range employs 52 mass acoustic-detection sensors for real-time crop flow adjustments via its IdealHarvest system.

By Propulsion Type;

The harvester market includes self-propelled and tractor-mounted segments. Self-propelled harvesters lead the segment due to their high efficiency, independence from external tractors, and suitability for large-scale farming. Tractor-mounted units remain in demand among small and medium farms for their lower cost and adaptability to existing machinery. It is expected that hybrid propulsion systems may emerge as a niche, aligning with sustainability goals and fuel efficiency requirements. This diversification is enabling manufacturers to cater to varying operational scales and budgets.

Segmentations:

By Type:

- Combine Harvesters

- Forage Harvesters

- Others

By Automation:

- Manual

- Semi-Automated

- Fully Automated

By Propulsion Type:

- Self-Propelled

- Tractor-Mounted

By Region:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America and Europe :

North America holds 32% market share, supported by advanced farming infrastructure, high adoption of precision agriculture, and favorable financing programs for farm equipment. Europe accounts for 28% market share, driven by strong agricultural mechanization policies, strict environmental standards, and continuous innovation in harvesting technologies. The harvester market in these regions benefits from established commercial farming operations and a strong presence of global manufacturers. It is further strengthened by research initiatives that focus on improving fuel efficiency and sustainability. Government subsidies and training programs accelerate adoption among both large and mid-sized farms. Seasonal demand remains stable due to diverse crop patterns, ensuring consistent equipment utilization.

Asia-Pacific :

Asia-Pacific holds 25% market share and is projected to record the highest growth rate during the forecast period. Rising agricultural investments in China, India, and Southeast Asia are fueling mechanization and expanding demand for harvesters. The harvester market in this region is benefiting from government-led subsidy programs, rural infrastructure improvements, and growing commercial farming. It is also influenced by the need to improve productivity in densely populated nations facing food security challenges. The adoption of compact and cost-effective models is gaining momentum in smallholder farms. Expanding local manufacturing capabilities is reducing equipment costs and strengthening distribution networks.

Latin America and Middle East & Africa :

Latin America holds 9% market share, supported by expanding agribusiness investments in Brazil and Argentina, while the Middle East & Africa accounts for 6% market share driven by increasing agricultural modernization. The harvester market in these regions is supported by export-oriented crop production and favorable trade policies. It is gaining momentum through partnerships between international manufacturers and regional distributors. Seasonal crops such as sugarcane, coffee, and cereals create specialized demand for tailored harvester models. Government-backed agricultural transformation initiatives are accelerating technology adoption. Localized training and service networks are becoming critical to support long-term growth in these developing markets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- AGCO Corporation

- CNH Industrial N.V.

- Caterpillar Inc.

- CLAAS KGaA mbH

- Deere & Company

- Dasmesh Group

- KUBOTA Corporation

- Mahindra&Mahindra Ltd.

- Linttas Electric Company.

- SDF

Competitive Analysis:

The harvester market is highly competitive, with global leaders and regional manufacturers competing on technology, product range, and service capabilities. Key players include AGCO Corporation, CNH Industrial N.V., Caterpillar Inc., CLAAS KGaA mbH, Deere & Company, Dasmesh Group, and KUBOTA Corporation. It is characterized by continuous innovation in automation, precision agriculture integration, and sustainable design to meet evolving farming demands. Leading companies focus on expanding their product portfolios with high-efficiency, multi-crop, and low-emission models. Strategic partnerships, mergers, and localized manufacturing strengthen their market reach and cost competitiveness. Strong dealer networks, financing options, and aftersales services are critical factors in customer retention. The market structure favors players with the capacity to offer both technologically advanced solutions and region-specific, cost-effective equipment.

Recent Developments:

- In August 2025, AGCO Corporation launched the MF 8S Xtra series under its Massey Ferguson brand, introducing innovative enhancements in comfort and efficiency for agricultural machinery users.

- In August 2025, CLAAS KGaA mbH launched the new JAGUAR 1000 series forage harvesters, designed to increase efficiency and throughput for commercial users.

- In September 2024, Kubota North America expanded its precision agriculture portfolio by acquiring Bloomfield Robotics, integrating advanced crop analytics into its machinery line for enhanced yield management.

Market Concentration & Characteristics:

The harvester market demonstrates a moderately concentrated structure, with a mix of global leaders and strong regional manufacturers competing through technology innovation, product diversification, and aftersales service networks. It is characterized by high entry barriers due to significant capital investment, advanced engineering requirements, and the need for established distribution channels. Leading players focus on precision agriculture integration, sustainability features, and multi-crop adaptability to strengthen market positioning. Regional manufacturers often compete by offering cost-effective models tailored to local farming conditions. The market shows steady demand cycles aligned with seasonal agricultural patterns and replacement needs. Strong brand reputation, dealer support, and financing options play a crucial role in influencing purchase decisions.

Report Coverage:

The research report offers an in-depth analysis based on Type, Automation, Propulsion Type and Region. It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- Rising global food demand will continue to drive the adoption of advanced harvesting machinery across developed and emerging markets.

- Increasing integration of AI, IoT, and precision agriculture tools will enhance operational efficiency and yield optimization.

- Sustainable harvester models with low emissions and energy-efficient engines will gain stronger market traction.

- Multi-crop and modular designs will become more prevalent, offering flexibility for diverse farming needs.

- Expansion of subsidy programs and rural financing initiatives will improve access to modern equipment in developing regions.

- Growth in commercial farming operations will create higher demand for high-capacity and automated harvesters.

- Seasonal and climate-resilient designs will gain importance to address unpredictable weather patterns.

- Localized manufacturing in emerging economies will reduce equipment costs and strengthen distribution networks.

- Strategic partnerships between global manufacturers and regional dealers will improve market penetration and aftersales support.

- Continuous innovation in harvester technology will position advanced models as a standard requirement for large-scale farming operations.