Market Overview:

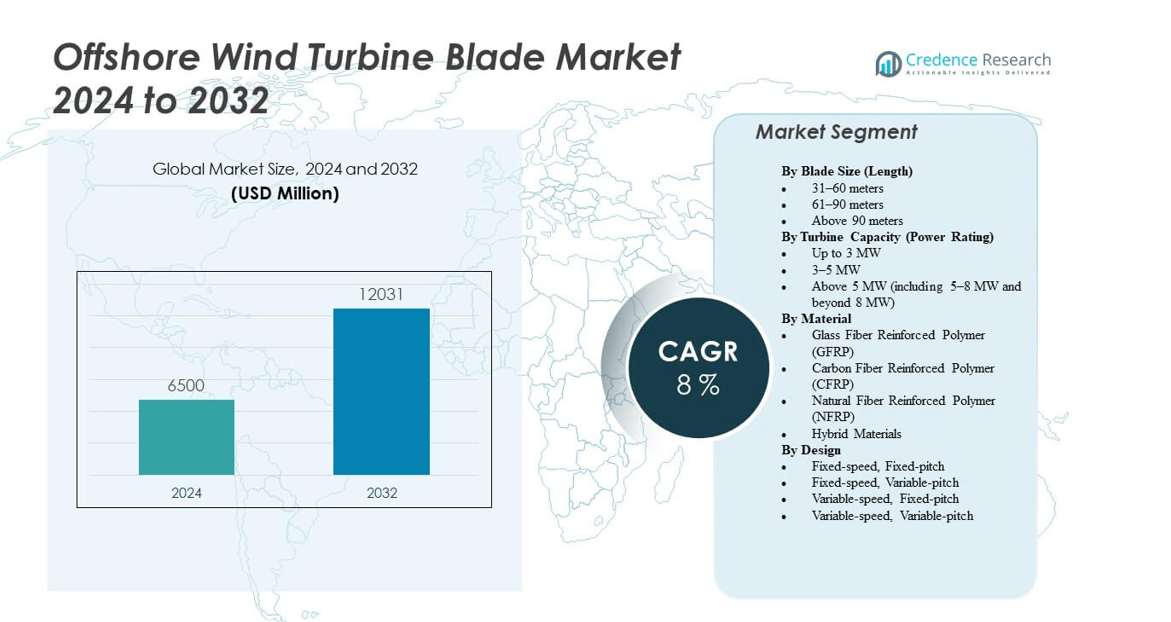

The Offshore Wind Turbine Blade Market is projected to grow from USD 6,500 million in 2024 to an estimated USD 12,031 million by 2032, with a compound annual growth rate (CAGR) of 8% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Offshore Wind Turbine Blade Market Size 2024 |

USD 6,500 million |

| Offshore Wind Turbine Blade Market, CAGR |

8% |

| Offshore Wind Turbine Blade Market Size 2032 |

USD 12,031 million |

The market growth is strongly driven by rising investments in renewable energy, favorable government policies, and decarbonization initiatives. Growing offshore wind farm installations are fueling the demand for larger and more durable turbine blades. Technological innovations, such as advanced composite materials and aerodynamic designs, enhance efficiency and performance, encouraging broader adoption. Increasing private sector participation and public funding further strengthen the industry’s long-term growth outlook.

Europe leads the offshore wind turbine blade market due to strong government support, established offshore infrastructure, and significant deployment across the UK, Germany, and Denmark. Asia Pacific is emerging as a high-growth region, with China leading large-scale offshore wind projects and nations like Japan, South Korea, and Taiwan investing heavily in offshore wind expansion. North America is gradually advancing, driven by U.S. offshore wind projects supported by clean energy policies.

Market Insights:

- The Offshore Wind Turbine Blade Market is projected to grow from USD 6,500 million in 2024 to USD 12,031 million by 2032, at a CAGR of 8%.

- Strong government policies and renewable energy targets are accelerating offshore wind farm expansion globally.

- Technological advancements in blade design and materials improve efficiency and durability in harsh offshore conditions.

- High manufacturing and installation costs remain a restraint, limiting adoption in price-sensitive regions.

- Europe leads the market with 43% share, supported by advanced infrastructure and favorable policy frameworks.

- Asia Pacific holds 35% share and is the fastest-growing region, driven by large-scale projects in China, Japan, and South Korea.

- North America captures 15% share, while Latin America and Middle East & Africa together account for 7%, showing early but expanding opportunities.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Government Policies, Renewable Targets, and Energy Transition Goals

Governments worldwide are setting ambitious renewable energy targets, which push demand for offshore wind. Supportive policies, subsidies, and favorable auctions encourage developers to expand wind farms in deeper waters. The Offshore Wind Turbine Blade Market benefits from tax incentives, carbon neutrality goals, and stricter emission controls. It gains momentum as national energy security concerns accelerate the transition from fossil fuels. International agreements on clean energy commitments provide strong backing for offshore infrastructure investments. Long-term power purchase agreements reduce financial risks for operators. Public-private partnerships create an enabling environment for large-scale adoption. Increased policy clarity drives higher investor confidence.

- For instance, Ørsted has leveraged U.K. government Contracts for Difference (CfD) schemes to expand its Hornsea offshore projects, with Hornsea 2 alone deploying 165 turbines generating 1.3 GW capacity, ensuring policy-backed offshore adoption.

Technological Advancements and Efficiency Gains in Blade Design

Technological innovation is a critical factor driving demand for offshore turbine blades. The Offshore Wind Turbine Blade Market expands as composite materials improve strength-to-weight ratios in blades. It benefits from lighter, more durable structures that withstand harsher offshore conditions. Advanced manufacturing methods, including automated production, enhance cost efficiency and precision. Larger blades with improved aerodynamics increase energy capture from low wind speeds. Research efforts focus on boosting operational reliability and extending lifecycle performance. Collaboration between manufacturers and research institutes strengthens blade testing and standardization. Digital tools for predictive maintenance reduce downtime and improve output. These advancements accelerate adoption worldwide.

Rising Global Investments and Private Sector Involvement

Global investments in offshore wind projects have increased, driven by financial institutions, governments, and energy firms. The Offshore Wind Turbine Blade Market grows with rising capital flows into sustainable energy infrastructure. It benefits from investor confidence in long-term profitability and lower cost of offshore power. Large-scale financing from green bonds and institutional funds ensures faster project execution. Utility companies partner with blade manufacturers to expand turbine capacity across diverse geographies. Insurance firms design risk solutions tailored to offshore challenges, reducing financial uncertainties. Growing interest from oil and gas firms entering offshore wind strengthens competition. The investment ecosystem supports consistent demand.

Rising Energy Demand and Decarbonization Pressure in Industrial Sectors

Industrial sectors face increasing pressure to decarbonize operations and reduce carbon footprints. The Offshore Wind Turbine Blade Market benefits from rising electricity demand supported by renewables. It addresses needs of industries shifting away from fossil-fuel based power sources. Offshore wind provides scalable capacity to supply high-consumption users in steel, chemicals, and transport. Electricity from offshore wind also complements electrification in mobility and smart infrastructure. Corporations adopt offshore power purchase agreements to meet sustainability goals. Growth in data centers accelerates offshore demand due to their heavy energy use. Industrial partnerships with wind developers ensure long-term utilization. This demand cycle strengthens blade adoption.

- For instance, Amazon signed a 10-year corporate power purchase agreement with Ørsted for 250 MW of capacity from the 900 MW Borkum Riffgrund 3 offshore wind farm in Germany, marking one of the largest offshore wind-based corporate PPAs in Europe.

Market Trends:

Expansion of Floating Offshore Wind and Deepwater Installations

Floating wind technology is reshaping the offshore segment by unlocking deepwater opportunities. The Offshore Wind Turbine Blade Market benefits from blade designs optimized for larger floating platforms. It responds to demand from regions with deeper coastlines, where fixed-bottom foundations are not viable. Floating turbines expand geographic reach beyond traditional shallow waters. Manufacturers innovate blade materials to endure dynamic ocean conditions. Early pilot projects in Europe and Asia validate commercial scalability. Governments fund floating projects to diversify renewable portfolios. Collaboration between shipbuilders and energy firms supports the growth of this trend.

- For example, Siemens Gamesa supplied 60 units of its SG 14‑222 DD offshore wind turbine for the Moray West project in Scotland. Each turbine uses three 108‑meter-long IntegralBlades the longest serially produced in the UK built at the Hull factory. This marked the first commercial deployment of the SG 14‑222 DD, with serial installation beginning in 2024.

Digital Integration, Smart Monitoring, and Predictive Analytics

Digital tools are transforming the way offshore turbine blades are monitored and maintained. The Offshore Wind Turbine Blade Market gains from predictive maintenance software that prevents costly breakdowns. It uses AI and IoT-enabled sensors to track blade performance in real time. Drones and robotics improve inspection efficiency and safety for offshore installations. Smart analytics extend blade lifespan by enabling proactive repair decisions. Digital twins allow simulation of operational scenarios to optimize reliability. Cloud-based platforms provide operators with accurate blade health data. This shift reduces operational costs and supports more efficient asset management.

Growing Sustainability Efforts and Recycling Innovations in Blade Materials

Sustainability initiatives influence material use in blade production across global markets. The Offshore Wind Turbine Blade Market adapts by developing recyclable and bio-based composites. It reduces landfill waste from decommissioned blades by promoting circular economy models. Research explores thermoplastic resins and modular blade designs for easier recycling. Industry players invest in blade repurposing programs for infrastructure and construction applications. Governments impose stricter recycling mandates to manage wind power’s environmental impact. Companies collaborate on closed-loop recycling solutions to enhance green credentials. Sustainability certifications increase adoption by environmentally conscious investors and operators.

- For instance, LM Wind Power has produced the world’s first 62-meter wind turbine blade made entirely from thermoplastic resin (Elium) at its Ponferrada facility in Spain, jointly developed with partners in the ZEBRA project; the blade is fully recyclable, setting a new standard for circular economy innovation in offshore wind systems.

Expansion of Supply Chain Networks and Global Collaboration

Supply chain networks are evolving to meet rising offshore wind demand. The Offshore Wind Turbine Blade Market benefits from regional blade manufacturing hubs near key projects. It reduces logistics costs and strengthens reliability for project execution. Joint ventures between global blade producers and local firms expand regional capacity. Standardization across blade sizes improves cross-border collaboration for component supply. Local workforce training programs support the growth of specialized manufacturing skills. Governments encourage domestic production to reduce import dependency. International partnerships ensure technology transfer and broader market penetration. The expanding supply chain enables faster scaling of offshore projects.

Market Challenges Analysis:

High Costs, Supply Risks, and Infrastructure Barriers

Cost pressures remain a central challenge in offshore blade manufacturing. The Offshore Wind Turbine Blade Market faces high expenses for composite materials and advanced fabrication. It struggles with fluctuations in raw material availability, especially carbon fiber and epoxy resins. Transportation and installation costs add further strain, particularly in deepwater projects. Limited port facilities and specialized vessels restrict deployment in some regions. Supply chain disruptions caused by geopolitical tensions or natural disasters create risks. Delays in grid infrastructure connections slow integration of offshore power. These combined factors restrain market growth and raise financial risks for developers.

Technical Reliability and Environmental Constraints in Offshore Deployment

Reliability issues challenge turbine blades due to extreme offshore weather and operational demands. The Offshore Wind Turbine Blade Market contends with erosion, fatigue, and material degradation over time. It requires frequent maintenance, increasing operational costs for developers. Certification and compliance with strict safety standards delay project timelines. Environmental concerns related to marine ecosystems complicate permitting processes. Local opposition to offshore wind development impacts project approvals in some regions. Limited availability of skilled labor slows innovation in blade production. These issues highlight the operational complexity and technical risks in offshore expansion.

Market Opportunities:

Rising Adoption of Floating Wind and Emerging Coastal Markets

Emerging coastal economies present new growth opportunities for offshore blade producers. The Offshore Wind Turbine Blade Market benefits from floating wind platforms that expand to deeper waters. It opens access to markets in Japan, South Korea, and the U.S. West Coast. Governments in these regions support floating technology with dedicated funding. Blade manufacturers can develop specialized designs tailored for floating stability. Expansion into non-traditional markets diversifies revenue streams for producers. Collaboration with local developers strengthens market entry strategies. The increasing pipeline of deepwater projects secures long-term opportunities for blade demand.

Integration of Circular Economy and Advanced Recycling Solutions

Recycling innovation offers significant opportunities for blade manufacturers and operators. The Offshore Wind Turbine Blade Market embraces advanced recycling techniques that enhance environmental performance. It creates value through repurposed blades for construction, transport, or material recovery. Circular economy models reduce waste disposal costs for operators and increase sustainability appeal. Governments offer incentives for companies adopting green recycling practices. Research partnerships accelerate commercialization of recyclable blade technologies. Certification for green manufacturing improves investor confidence and customer trust. This opportunity supports a more sustainable offshore wind ecosystem while creating competitive advantages.

Market Segmentation Analysis:

By blade size, the Offshore Wind Turbine Blade Market is dominated by the 61–90-meter category, which remains the preferred option for most offshore projects due to its balance of efficiency and manufacturing feasibility. It benefits from strong adoption in large offshore wind farms in Europe and Asia. The above 90 meters’ segment is gaining momentum, driven by demand for ultra-large turbines suited for deepwater installations and floating platforms. The 31–60-meter category continues to serve smaller capacity projects and replacement markets but holds a smaller share.

- For instance, LM Wind Power produced the LM 107.0 P blade (107 meters) for GE’s Haliade-X turbine, successfully deployed and tested in the U.K. to enable next-generation deepwater projects.

By turbine capacity, the 3–5 MW segment has been widely deployed across existing offshore farms, but the above 5 MW category is expanding rapidly with the adoption of turbines up to 15 MW. It represents the future growth area as developers pursue higher output per installation. The up to 3 MW segment is gradually declining due to limited scalability in modern offshore projects.

- For instance, Siemens Gamesa’s SG 3.6-132 turbine, rated at 3.465 MW, has been installed across multiple European onshore wind farms, demonstrating proven long-term performance.

By material, glass fiber reinforced polymer (GFRP) remains the most widely used due to cost efficiency and reliable performance. The Offshore Wind Turbine Blade Market is shifting toward carbon fiber reinforced polymer (CFRP), offering superior strength-to-weight ratios needed for ultra-long blades. Hybrid materials and natural fiber reinforced composites are emerging segments, driven by sustainability goals and recycling initiatives.

By design, variable-speed, variable-pitch systems lead adoption, offering maximum efficiency in fluctuating offshore conditions. Fixed-speed configurations are declining in relevance, while variable-pitch alternatives maintain utility in specific project designs. It reflects the transition toward smarter, adaptable blade technologies.

Segmentation:

By Blade Size (Length)

- 31–60 meters

- 61–90 meters

- Above 90 meters

By Turbine Capacity (Power Rating)

- Up to 3 MW

- 3–5 MW

- Above 5 MW (including 5–8 MW and beyond 8 MW)

By Material

- Glass Fiber Reinforced Polymer (GFRP)

- Carbon Fiber Reinforced Polymer (CFRP)

- Natural Fiber Reinforced Polymer (NFRP)

- Hybrid Materials

By Design

- Fixed-speed, Fixed-pitch

- Fixed-speed, Variable-pitch

- Variable-speed, Fixed-pitch

- Variable-speed, Variable-pitch

By Region

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis:

Europe holds the largest share of the Offshore Wind Turbine Blade Market, accounting for 43% of global revenue. Strong policy frameworks, advanced offshore infrastructure, and aggressive renewable energy targets drive growth in countries such as the United Kingdom, Germany, and Denmark. It benefits from extensive government subsidies and early adoption of offshore wind technologies. The presence of leading turbine and blade manufacturers further strengthens the region’s position. Cross-border energy projects within the European Union enhance collaboration and deployment. Continuous investment in deepwater and floating wind projects expands long-term opportunities.

Asia Pacific represents 35% of the Offshore Wind Turbine Blade Market, making it the fastest-growing regional segment. China dominates installations with large-scale projects supported by state-led initiatives. It gains traction in Japan, South Korea, and Taiwan, where coastal resources and policy incentives align to support offshore expansion. Rapid industrialization and rising electricity demand fuel adoption in emerging economies. Local manufacturing hubs lower costs and improve supply chain resilience. Government-backed floating wind demonstration projects increase market potential in deeper waters. This region is positioned as a critical growth engine for the industry.

North America accounts for 15% of the Offshore Wind Turbine Blade Market, with the United States leading regional demand. It receives support from clean energy policies and state-level renewable portfolio standards. Growing offshore wind projects along the East Coast provide momentum, while ports and supply chain investments strengthen deployment capacity. Canada and Mexico are at early stages but exploring opportunities to diversify their energy mix. Latin America holds a 4% share, with Brazil and Chile showing interest in offshore wind to strengthen renewable energy portfolios. The Middle East & Africa capture 3%, driven by early-stage projects in South Africa and emerging interest in Gulf nations.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

Competitive Analysis:

The Offshore Wind Turbine Blade Market is highly competitive with the presence of established global players and emerging regional firms. Leading companies such as Siemens Gamesa, Vestas, GE Vernova, LM Wind Power, and Nordex dominate with extensive product portfolios and strong offshore project pipelines. It gains strength from technological leadership, strategic partnerships, and advanced manufacturing facilities close to major offshore hubs. Smaller firms focus on niche innovations, including recyclable blades and hybrid materials, to capture specialized demand. Competition intensifies with increasing investments in floating wind platforms, which require larger and more durable blades. Global players expand capacity through joint ventures and localized production to reduce costs and strengthen supply chains. Competitive advantage depends on scale, cost efficiency, and technological innovation. The market remains dynamic, with collaborations between energy developers, material suppliers, and blade manufacturers shaping future growth trajectories.

Recent Developments:

- In August 2025, RWE, in partnership with Siemens Gamesa, launched the large-scale use of recyclable wind turbine blades at the Sofia offshore wind farm in the UK. This marks a notable shift toward sustainability by deploying blades designed for full-material recovery, setting new standards in environmental stewardship for offshore wind projects.

- In January 2025, MingYang Smart Energy secured £60 million in funding from the Scottish government to establish its first turbine blade factory outside China. The Offshore Wind Turbine Blade Market gained significance from this investment, which supports North Sea offshore wind expansions under the ScotWind initiative.

- In December 2024, Russia’s state nuclear corporation Rosatom reopened a wind turbine blade factory in Ulyanovsk, replacing the former Vestas facility. The Offshore Wind Turbine Blade Market saw renewed domestic production capacity in Russia, with the plant expected to produce up to 450 blades annually and potentially export to projects in Kyrgyzstan. This move reflects Russia’s push to replace Western renewable equipment suppliers.

Report Coverage:

The research report offers an in-depth analysis based on Blade Size (Length), Turbine Capacity (Power Rating), Material and Design. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Offshore blade designs will expand toward ultra-long formats, supporting turbines with greater capacity and improved power efficiency across varying wind conditions.

- Floating wind platforms will generate strong demand for specialized blades, enabling installations in deepwater regions previously inaccessible to fixed-bottom foundations.

- Advanced composites and hybrid materials will dominate development, offering enhanced durability, reduced weight, and improved resistance against offshore environmental stress.

- Digital twin technology will become central to blade lifecycle management, allowing operators to simulate scenarios and adopt predictive maintenance strategies.

- Recycling and repurposing of decommissioned blades will gain momentum, aligning the market with global sustainability and circular economy objectives.

- Regional blade manufacturing hubs will scale, reducing transportation costs while strengthening supply resilience and localized workforce capabilities.

- Strategic alliances between energy developers and blade producers will encourage faster innovation and accelerate deployment of next-generation offshore turbines.

- Policy-driven expansion across emerging coastal economies will diversify adoption and strengthen the global deployment footprint.

- Growing private and institutional investment will accelerate R&D into lightweight blade designs with longer lifespans.

- Integration of automation and robotics in blade production will streamline efficiency, enhance precision, and reduce project delivery timelines.