Market Overview:

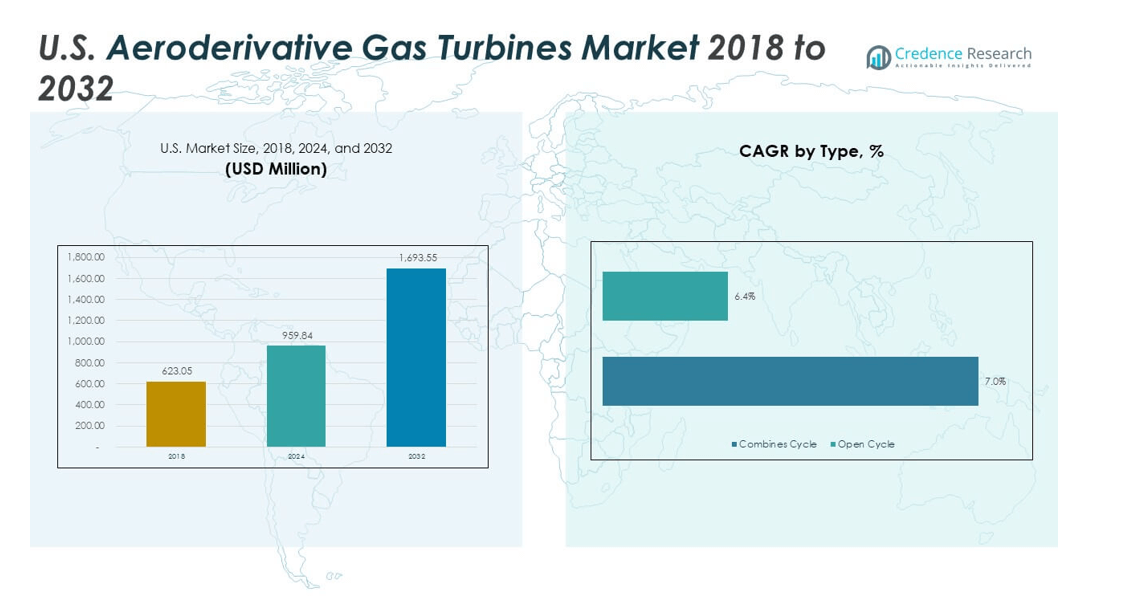

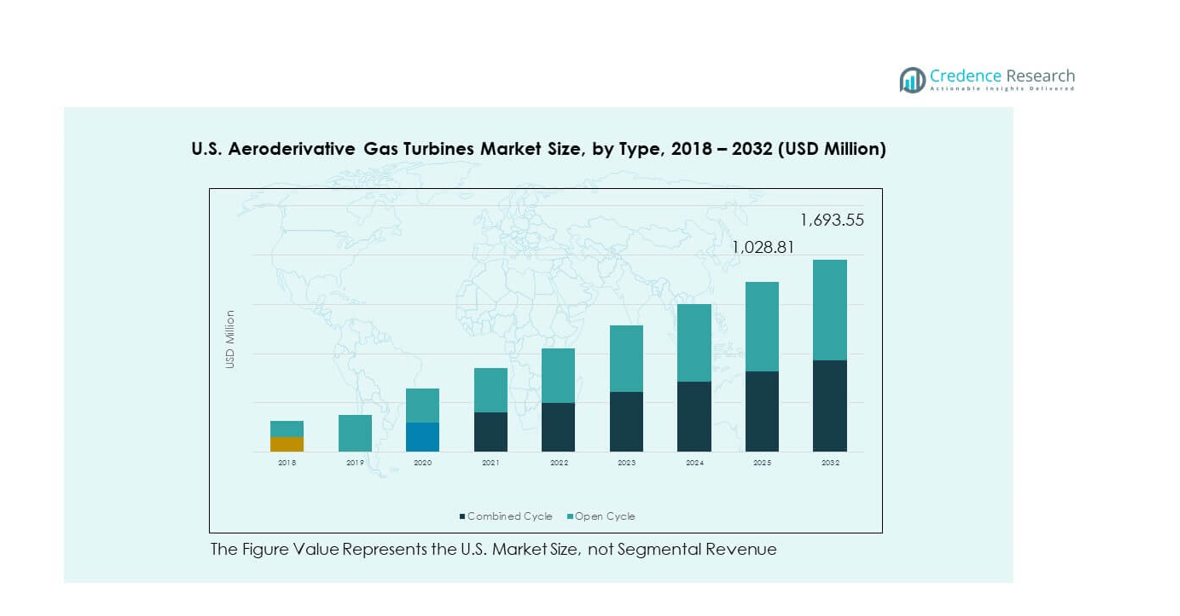

The U.S. Aeroderivative Gas Turbines Market size was valued at USD 623.05 million in 2018 to USD 959.84 million in 2024 and is anticipated to reach USD 1,693.55 million by 2032, at a CAGR of 7.30% during the forecast period. The market reflects strong momentum, supported by rising demand for efficient and flexible energy solutions across industries and utilities. Growth is further shaped by the increasing role of natural gas in the country’s energy transition strategies.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| U.S. Aeroderivative Gas Turbines Market Size 2024 |

USD 959.84 million |

| U.S. Aeroderivative Gas Turbines Market, CAGR |

7.30% |

| U.S. Aeroderivative Gas Turbines Market Size 2032 |

USD 1,693.55 million |

Market drivers include rising adoption of distributed power systems, a growing shift toward cleaner energy, and demand for rapid-response solutions in industrial and utility operations. The U.S. is witnessing an increased focus on reducing carbon emissions, making aeroderivative turbines favorable due to their lower environmental impact compared to heavy-duty turbines. Their ability to start quickly, provide backup for renewable power, and deliver efficient energy in remote or offshore areas enhances market expansion. Ongoing investments in modernization of energy infrastructure also accelerate adoption across multiple sectors.

Regionally, the U.S. Aeroderivative Gas Turbines Market benefits from strong industrial adoption in regions with extensive oil and gas operations, such as Texas and the Gulf Coast, where reliable power and mechanical drive systems are critical. Emerging opportunities are seen in renewable-integrated grids across western states, where turbine flexibility helps balance intermittent solar and wind resources. The northeastern U.S. also shows promising adoption, driven by regulatory focus on decarbonization and grid reliability. This diverse geographic adoption underscores the turbine’s adaptability to varied regional energy needs.

Market Insights:

- The U.S. Aeroderivative Gas Turbines Market was valued at USD 623.05 million in 2018, reached USD 959.84 million in 2024, and is projected to hit USD 1,693.55 million by 2032, growing at a CAGR of 7.30%.

- The Global Aeroderivative Gas Turbines Market size was valued at USD 2,288.5 million in 2018 to USD 3,617.3 million in 2024 and is anticipated to reach USD 6,608.2 million by 2032, at a CAGR of 7.85% during the forecast period.

- The Western U.S. held 34% share due to renewable integration, the Southern U.S. secured 29% driven by oil and gas operations, and the Northeast accounted for 21% supported by regulatory focus on emissions and grid reliability.

- The Midwest, with 16% share, is the fastest-growing subregion, fueled by industrial adoption and microgrid development enhancing energy resilience.

- By type, combined cycle turbines accounted for nearly 61% of market share in 2024, reflecting strong adoption in continuous power generation and efficiency-driven applications.

- Open cycle turbines held about 39% share, gaining importance for peaking roles, rapid deployment, and backup power requirements across industrial and utility sectors.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Demand for Flexible and Efficient Energy Generation

The U.S. Aeroderivative Gas Turbines Market is propelled by increasing demand for flexible energy solutions across industrial and utility sectors. These turbines are preferred for their rapid start-up times, high efficiency, and adaptability in peak load conditions. They support utilities in balancing grid fluctuations and responding quickly to demand surges. Growing reliance on distributed power generation further strengthens adoption, as turbines enable reliable supply in off-grid and remote areas. Their compact design and mobility make them suitable for diverse applications, including defense and offshore oil fields. It supports the transition toward cleaner energy, with lower emissions compared to heavy-duty turbines. Modernization of power infrastructure also drives replacement of outdated equipment. This consistent demand reinforces the market’s steady growth outlook.

- For instance, General Electric’s LM6000 aeroderivative gas turbine is designed to deliver up to 50 MW output, with a ramp rate capability of 50 MW per minute and start times of under 10 minutes, making it well suited for peaking operations, grid balancing, and data center backup applications.

Integration with Renewable Energy Infrastructure

Demand for aeroderivative turbines is driven by their compatibility with renewable integration strategies in the U.S. Utilities face rising challenges from intermittent solar and wind energy, and turbines provide fast-response backup solutions. Their ability to stabilize power grids makes them vital in states with strong renewable commitments. Investment in flexible power technologies creates opportunities for deployment in hybrid energy systems. Their design allows efficient operation at partial loads, aligning with fluctuating renewable supply. The U.S. Aeroderivative Gas Turbines Market benefits from policies promoting cleaner power and grid reliability. Their low start-up times and lower emissions strengthen their adoption for peaking and backup roles. Industrial players also adopt them for cogeneration systems, enhancing overall efficiency. It highlights their role in enabling a reliable low-carbon energy framework.

Expansion of Oil and Gas Applications

The oil and gas industry remains a critical driver of turbine demand, with growing applications in mechanical drive systems. Aeroderivative turbines power compressors and pumps in offshore and onshore operations, ensuring uninterrupted flow of hydrocarbons. Their high efficiency and compact footprint provide advantages in energy-intensive oil and gas environments. The market gains further traction in regions such as the Gulf Coast, where extensive exploration and refining activities continue. Rising investments in LNG facilities also accelerate turbine adoption for mechanical and power generation needs. The U.S. Aeroderivative Gas Turbines Market supports the industry’s demand for reliable and mobile energy sources. It helps reduce operational downtime and enhances safety through quick deployment. This synergy between energy infrastructure and oil and gas drives sustained market demand.

Government Policies and Infrastructure Modernization

Policy support and infrastructure modernization initiatives are major drivers shaping the U.S. turbine market. Federal and state-level programs emphasize emission reduction and energy efficiency, encouraging adoption of advanced gas turbines. Infrastructure spending focuses on modernizing aging power plants and upgrading transmission and distribution systems. These initiatives boost opportunities for turbine replacement and new installations. It aligns with national goals of reducing carbon intensity and ensuring energy security. Industries and utilities are supported with incentives for adopting flexible and efficient power technologies. The U.S. Aeroderivative Gas Turbines Market responds strongly to these measures by aligning with policy priorities. Modern grid infrastructure requires dynamic solutions, and aeroderivative turbines meet this demand effectively. The resulting synergy between policy and technology drives long-term market expansion.

- For instance, Siemens Energy developed the SGT-A45 TR aeroderivative turbine, capable of generating up to 44 MW with start-up times under 9 minutes. It features a dry low emissions system designed to achieve NOx as low as 25 ppm and CO near 10 ppm at full load, supporting cleaner and more flexible power generation.

Market Trends

Adoption of Hybrid Power Systems

Hybrid power solutions combining turbines with battery storage are gaining momentum in the U.S. market. These systems allow rapid load balancing and improved efficiency, addressing renewable variability. Aeroderivative turbines complement storage by providing instant power during extended demand periods. Utilities are adopting such hybrid models to maintain grid stability while integrating large renewable capacities. It reflects the shift toward advanced power ecosystems that balance cost, sustainability, and reliability. The U.S. Aeroderivative Gas Turbines Market benefits from this growing interest in hybrid energy solutions. Investments in smart energy grids accelerate adoption of hybrid turbine systems. This trend highlights the importance of flexible gas turbines in modern energy networks.

Increased Focus on Digitalization and Predictive Maintenance

Digital transformation is shaping turbine performance and maintenance in the U.S. market. Operators deploy advanced monitoring systems and predictive analytics to improve reliability and reduce downtime. These tools enable continuous performance optimization and real-time fault detection. It enhances turbine lifespan and reduces lifecycle costs for utilities and industrial users. Integration with industrial IoT and cloud-based platforms provides improved efficiency insights. The U.S. Aeroderivative Gas Turbines Market shows a clear trend toward smart operations and automation. Predictive maintenance reduces unplanned outages and strengthens supply security. This technological shift supports both cost efficiency and operational resilience.

- For instance, Siemens Energyimplemented its Omnivise monitoring platform, enabling real-time data analysis from over 1,500 sensors per turbine, resulting in a reported 30% reduction in unplanned downtime at monitored facilities.

Growing Role in Decentralized Energy Systems

Decentralized energy generation is emerging as a key trend across U.S. industries and communities. Aeroderivative turbines are well-suited for distributed energy plants due to their modularity and compact size. It allows flexible deployment in smaller grids, remote areas, and industrial parks. The technology aligns with rising demand for energy independence and resilience. Microgrids integrating turbines ensure reliable supply during disruptions and grid instability. The U.S. Aeroderivative Gas Turbines Market gains traction from these decentralized deployments. Utilities and local governments support microgrid projects to improve community resilience. This shift to localized energy generation strengthens the role of turbines in future energy models.

- For instance, General Electric’s LM2500 aeroderivative gas turbine family has over 2,500 units sold worldwide, amassing more than 97 million operating hours. The LM2500 can deliver between 22 and 34 megawatts (MW) of power output, with start-up times as low as five minutes, making it suitable for decentralized power generation and microgrid applications in the U.S. and globally.

Increasing Use in Military and Defense Applications

Defense applications are shaping new growth areas for aeroderivative turbines in the U.S. Military facilities require mobile, efficient, and secure power systems to support critical operations. Turbines provide rapid deployment, mobility, and reliability for remote and temporary sites. It ensures operational continuity during emergencies and military exercises. Their design supports both stationary and mobile platforms for defense use. The U.S. Aeroderivative Gas Turbines Market is experiencing rising demand from defense programs seeking flexible energy systems. Strategic investments are being directed toward energy independence for military bases. This adoption underscores the turbines’ role in national security strategies. It expands their scope beyond commercial and utility applications into specialized sectors.

Market Challenges Analysis

High Capital Costs and Competitive Pressures

One of the key challenges for the U.S. Aeroderivative Gas Turbines Market is high capital costs. The initial investment required for purchasing and installing turbines can deter smaller utilities and industries. It limits widespread adoption despite clear operational benefits. Intense competition from alternative technologies, such as renewable energy and heavy-duty turbines, also pressures the market. Renewable energy, in particular, offers cost advantages with falling prices for solar and wind power. The financial burden of integrating turbines into existing infrastructure adds complexity. Industrial buyers often weigh capital expenditure against long-term operational savings. Limited budgets in certain sectors further restrict adoption rates. This financial barrier remains a persistent challenge for market penetration.

Environmental Regulations and Fuel Price Volatility

The market also faces challenges from strict environmental regulations and volatile fuel prices. Regulatory authorities emphasize emission reduction targets, increasing compliance costs for turbine operators. Fuel price fluctuations impact operational expenses, making turbines less attractive compared to renewables. It creates uncertainty in long-term planning and investment decisions. Advances in alternative technologies such as battery storage and hydrogen fuel add competitive pressure. The U.S. Aeroderivative Gas Turbines Market must adapt to evolving policies and sustainability benchmarks. Utilities are under pressure to adopt cleaner energy solutions, which sometimes conflict with turbine adoption. These external factors create significant challenges for market growth and stability.

Market Opportunities

Expansion into Renewable Integration and Hybrid Solutions

Significant opportunities exist in renewable integration, where turbines support grid stability and reliability. They provide critical backup for intermittent solar and wind resources. The U.S. Aeroderivative Gas Turbines Market can expand by offering hybrid systems that combine turbines with storage. Utilities seek reliable solutions to manage demand fluctuations while ensuring energy security. It allows operators to balance environmental goals with practical supply needs. Increased investment in clean power frameworks creates strong growth avenues for turbine applications. Their adaptability and rapid deployment support evolving energy landscapes. This positioning offers long-term expansion opportunities for market players.

Growth Potential in Industrial and Defense Applications

Opportunities are emerging in industrial and defense sectors seeking reliable and mobile energy solutions. Industries require turbines for cogeneration, offshore operations, and mechanical drives, supporting productivity and efficiency. The U.S. Aeroderivative Gas Turbines Market benefits from military adoption, where rapid deployment and resilience are vital. Defense facilities invest in turbines to achieve energy independence and secure operations. It strengthens demand beyond conventional utility markets, opening new revenue streams. Industrial modernization and expansion projects further support turbine adoption. These factors highlight untapped growth opportunities in specialized applications. Market players focusing on these segments can gain a competitive edge.

Market Segmentation Analysis:

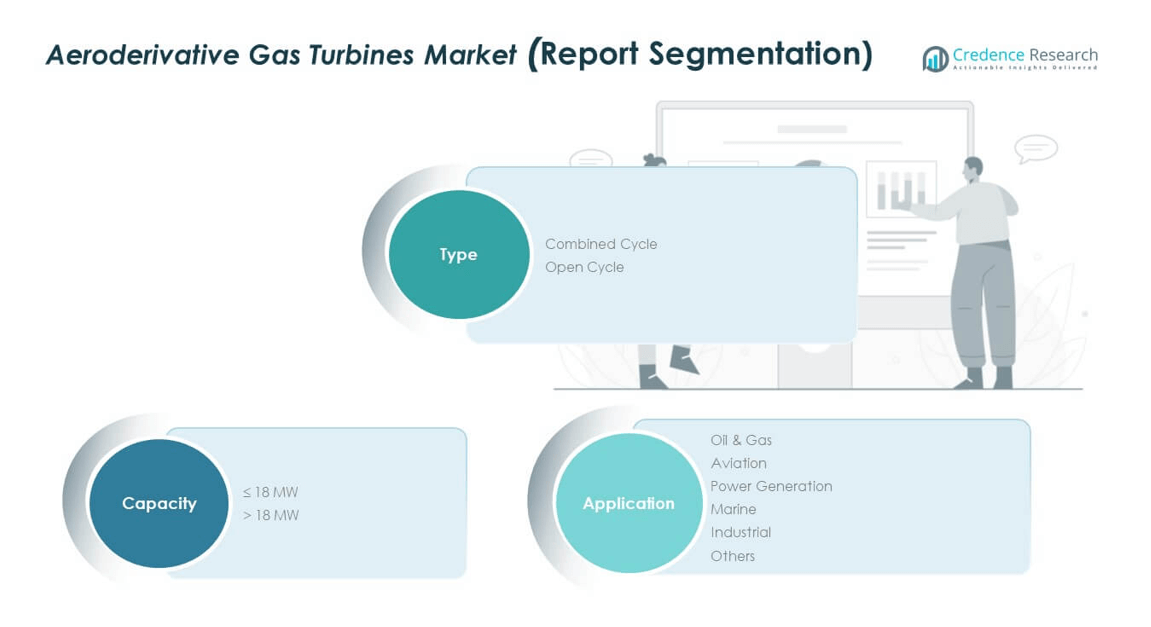

By type, the U.S. Aeroderivative Gas Turbines Market is divided into combined cycle and open cycle systems. Combined cycle turbines hold strong adoption due to higher efficiency and suitability for continuous power generation. Open cycle systems remain vital for applications requiring fast start-up and flexible deployment, such as emergency power or peak load management. The choice between these types depends on operational priorities, grid requirements, and cost efficiency. It creates balanced demand across both categories, with utilities and industries leveraging specific benefits.

By capacity, the market is segmented into ≤18 MW and >18 MW turbines. Units in the ≤18 MW range find use in distributed energy, offshore operations, and industrial plants where compactness and mobility are critical. Turbines above 18 MW dominate large-scale power generation, aviation support infrastructure, and oil and gas facilities requiring high output. The diversity of applications across both capacity brackets strengthens demand, with buyers prioritizing efficiency, reliability, and operational adaptability. It reinforces the role of turbines across multiple end-use sectors.

- For instance, Mitsubishi Power’s FT8® MOBILEPAC® offers 30 MW in portable form, successfully used for disaster recovery and remote industrial sites.

By application, the U.S. Aeroderivative Gas Turbines Market spans oil and gas, aviation, power generation, marine, industrial, and other sectors. Oil and gas remain leading users, supported by widespread adoption in mechanical drives and LNG facilities. Aviation uses turbines for ground power and auxiliary systems, while marine operators deploy them for propulsion and onboard energy. Power generation drives consistent demand for backup and peaking roles. Industrial sectors adopt turbines for cogeneration, enhancing efficiency. It highlights broad versatility across critical national industries.

- For instance, Siemens’ SGT-A35 RB aeroderivative turbine, derived from the RB211, delivers up to 38 MW of output with high power density. It has been widely deployed worldwide across oil and gas operations, including offshore platforms, where compact, efficient turbines are essential for reliable power generation.

Segmentation:

By Type

- Combined Cycle

- Open Cycle

By Capacity

By Application

- Oil & Gas

- Aviation

- Power Generation

- Marine

- Industrial

- Others

Regional Analysis:

Western United States

The Western United States holds a market share of 34% in the U.S. Aeroderivative Gas Turbines Market. This subregion benefits from extensive renewable energy integration, where turbines provide fast-response backup to stabilize solar and wind generation. California and neighboring states prioritize flexible and low-emission energy systems, supporting turbine demand in hybrid and peaking roles. Industrial users also invest in turbines for cogeneration, improving energy efficiency in high-demand sectors. Offshore projects and distributed energy installations strengthen adoption in coastal areas. It demonstrates the region’s commitment to balancing environmental goals with reliable power supply.

Southern United States

The Southern United States accounts for 29% of the market share, driven by robust oil and gas operations across Texas and the Gulf Coast. Aeroderivative turbines are widely deployed for mechanical drives in LNG terminals, refineries, and offshore platforms. The region’s high energy demand and industrial base create steady opportunities for power generation and cogeneration. Utilities rely on open cycle systems to manage peak loads, while industrial players adopt turbines for continuous supply. The U.S. Aeroderivative Gas Turbines Market benefits from strong investment in energy infrastructure across this subregion. It continues to lead in applications linked to hydrocarbons and heavy industry.

Northeastern and Midwestern United States

The Northeastern United States secures 21% of the market, supported by regulatory focus on emissions and reliability of grid systems. States with dense populations and older infrastructure adopt turbines to modernize energy supply. Demand is strong in peaking power and backup applications. The Midwestern United States contributes 16% market share, driven by industrial operations and localized energy needs. Utilities in the Midwest integrate turbines within microgrids to enhance resilience against disruptions. It strengthens adoption in sectors where stability and efficiency are critical. Together, these subregions highlight the geographic diversity of turbine deployment.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

Competitive Analysis:

The U.S. Aeroderivative Gas Turbines Market is characterized by the presence of global leaders and specialized manufacturers competing on technology, performance, and service capabilities. General Electric, Siemens, Pratt & Whitney, Mitsubishi Heavy Industries, Baker Hughes, and Solar Turbines dominate through strong portfolios and established client bases. These companies focus on expanding product reliability, fuel flexibility, and efficiency to secure long-term contracts with utilities and industrial operators. Regional and niche players strengthen competition by offering tailored solutions and aftermarket services to localized industries. It creates a dynamic environment where innovation and service differentiation remain critical success factors. Market participants actively pursue mergers, acquisitions, and strategic alliances to enhance technical expertise and broaden their customer reach. Companies emphasize hybrid integration, digital monitoring, and predictive maintenance platforms to support evolving customer demands. Service agreements and lifecycle support models contribute to stable revenue streams and improve brand loyalty. The U.S. Aeroderivative Gas Turbines Market reflects intense competition, where players compete not only on equipment performance but also on operational efficiency and sustainability credentials.

Recent Developments:

- In July 2025, GE Vernova announced a major delivery agreement with Crusoe, a leading AI infrastructure provider, to supply 29 LM2500XPRESS aeroderivative gas turbine packages for Crusoe’s data centers, targeting rapid AI-driven energy demand and emissions mitigation.

- In April 2025, Duke Energy entered a notable partnership with GE Vernova to procure up to eleven American-produced GE Vernova natural gas turbines. This partnership aims to fulfill Duke Energy’s growing demands driven by economic development and the rise of data center power needs.

- In March 2024, TRS Services, a key provider specializing in maintenance, repair, and overhaul of component parts for industrial gas turbines, announced its acquisition by Battle Investment Group. The acquisition is designed to strengthen TRS’s operations and expand strategic growth, particularly in servicing aeroderivative gas turbines used across remote, mobile, and off-grid power solutions, crucial for distributed energy needs in North America

- In November 2024, Wärtsilä joined a research consortium led by the University of Vaasa and funded by Business Finland to scale up a hydrogen-argon power cycle for net-zero power generation. The approach replaces air with recycled argon and oxygen in combustion engines and uses hydrogen as fuel, resulting in only water and inert argon as byproducts.

- In December 2024, Siemens Energy entered a strategic partnership with UK power giant SSE on the “Mission H2 Power” project, focused on developing combustion systems for the SGT5-9000HL gas turbine to operate 100% on hydrogen, supporting full decarbonization of SSE’s Keadby 2 Power Station.

Report Coverage:

The research report offers an in-depth analysis based on Type, Capacity and Application. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- The U.S. Aeroderivative Gas Turbines Market will expand with increasing demand for flexible energy systems.

- Integration with renewable energy grids will strengthen, as turbines provide rapid-response backup solutions.

- Growth will be supported by oil and gas operations that require reliable mechanical drive applications.

- Hybrid models combining turbines with storage technologies will gain adoption across utilities and industries.

- Investments in digital monitoring and predictive maintenance will improve operational efficiency and reliability.

- Industrial sectors will increasingly adopt turbines for cogeneration, driving efficiency and energy independence.

- Defense and military programs will continue to use turbines for mobile and resilient power systems.

- Modernization of existing power infrastructure will encourage replacement demand for outdated turbine systems.

- Regional diversification will expand, with strong adoption in the South, West, and industrial Midwest.

- Continuous innovation in design and fuel flexibility will enhance long-term competitiveness in the market.