Market Overview:

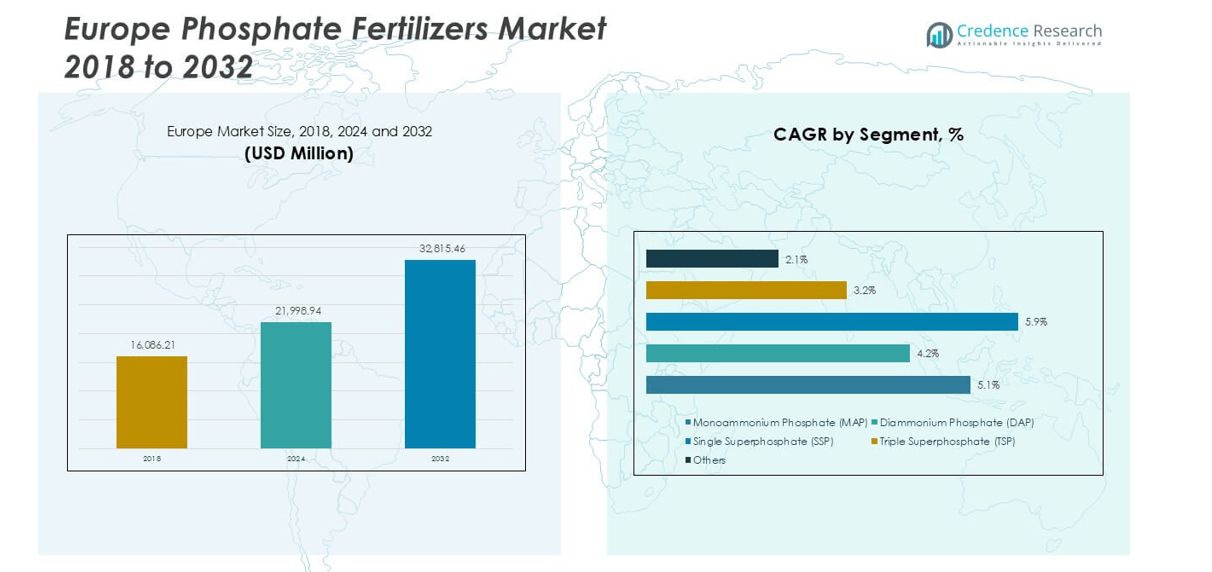

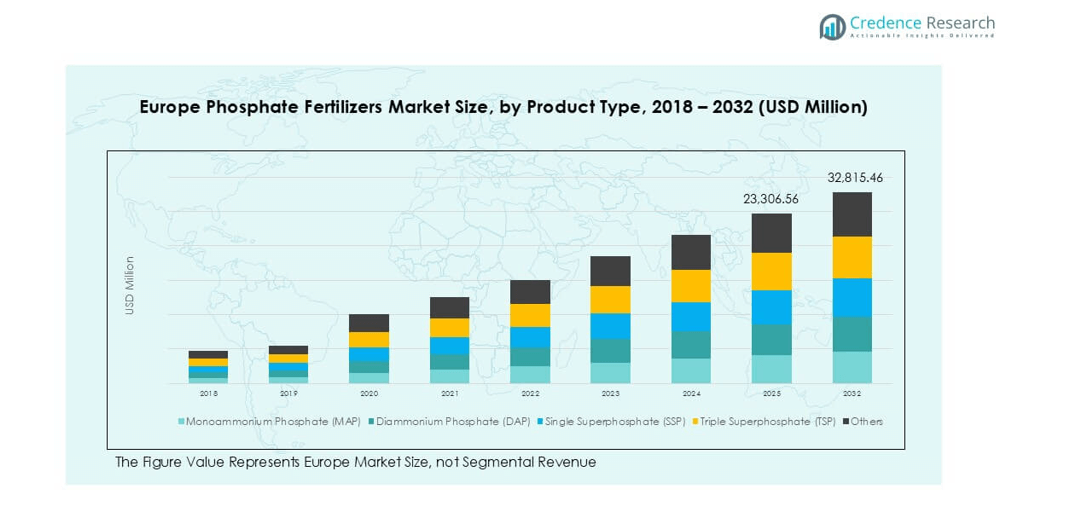

Europe Phosphate Fertilizers market size was valued at USD 16,086.21 million in 2018, reached USD 21,998.94 million in 2024, and is anticipated to reach USD 32,815.46 million by 2032, at a CAGR of 5.01% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Europe Phosphate Fertilizers Market Size 2024 |

USD 21,998.94 million |

| Europe Phosphate Fertilizers Market, CAGR |

5.01% |

| Europe Phosphate Fertilizers Market Size 2032 |

USD 32,815.46 million |

The Europe phosphate fertilizers market is led by Yara International, EuroChem Group, ICL Group Ltd, BASF SE, and Nutrien Ltd, which together hold a significant share through strong distribution networks and advanced product portfolios. These players focus on high-efficiency MAP and DAP fertilizers and invest in sustainable, water-soluble solutions to meet EU environmental goals. Western Europe dominates with over 40% market share in 2024, driven by extensive wheat and barley cultivation in France and Germany. Eastern Europe follows with around 25% share, supported by growing acreage and modernization of farming practices.

Market Insights

- Europe phosphate fertilizers market was valued at USD 21,998.94 million in 2024 and is projected to reach USD 32,815.46 million by 2032, growing at a CAGR of 5.01%.

- Demand is driven by rising cereal and oilseed production, precision farming adoption, and EU policies supporting balanced nutrient management and soil fertility improvement.

- Key trends include growing use of water-soluble fertilizers, micronutrient-enriched phosphate blends, and digital farming solutions for optimized nutrient application.

- The market is moderately consolidated, with leading players like Yara International, EuroChem, ICL Group, BASF SE, and Nutrien focusing on sustainable production and expansion in high-demand regions.

- Western Europe leads with over 40% share, followed by Eastern Europe with 25%; by product, MAP dominates with 35% share, followed by DAP and SSP used widely across cereals & grains (50% of demand).

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Product Type

Monoammonium Phosphate (MAP) dominates the Europe phosphate fertilizers market, accounting for over 35% share in 2024. MAP is preferred due to its high phosphorus concentration and water solubility, making it ideal for precision farming and fertigation. Diammonium Phosphate (DAP) follows closely, driven by its dual nitrogen-phosphorus benefits that support rapid crop growth. Single Superphosphate (SSP) and Triple Superphosphate (TSP) remain important for cost-sensitive farming regions, while niche demand for specialty and blended fertilizers supports the “Others” category. MAP growth is fueled by rising adoption of high-yield cereal crop cultivation and sustainable farming practices.

- For instance, MAP (Monoammonium Phosphate) is a highly water-soluble fertilizer with a high phosphorus concentration. These properties make it a preferred choice for modern agricultural applications like precision farming and fertigation, allowing for the precise and efficient delivery of nutrients to crops.

By Application

Cereals & grains represent the largest application segment, contributing over 50% of total demand in 2024. The dominance is supported by Europe’s extensive wheat, barley, and maize production, which require consistent phosphate input to maintain soil fertility and maximize yield. Oilseeds, including rapeseed and sunflower, form the second-largest segment, driven by growing demand for edible oils and biofuel production. Fruits & vegetables show strong growth potential due to increasing consumer demand for nutrient-rich and organic produce. Controlled phosphate application enhances root development and crop quality, supporting greenhouse and open-field farming. This segment benefits from precision agriculture adoption and rising horticulture exports from Spain, Italy, and the Netherlands. The “Others” category includes pulses, forage, and turf applications, which see steady but smaller contributions to overall demand.

- For instance, the EU harvested about 270 million tonnes of cereals in 2023, with wheat & maize applications likely consuming more than 1.2 million tonnes of phosphate fertilizers.

Market Overview

Supportive EU Agricultural Policies

EU Common Agricultural Policy (CAP) reforms encourage sustainable fertilizer usage and better nutrient efficiency. Incentives for precision agriculture and controlled-release fertilizers push adoption of phosphate-based products. Programs promoting reduced nutrient losses and circular economy practices help farmers optimize phosphorus use. Subsidies and training initiatives further encourage small and medium farms to adopt modern fertilization techniques. This policy support is critical in maintaining long-term demand for phosphate fertilizers, while aligning with EU climate targets and water framework directives for responsible nutrient management.

- For instance, EU farmers applied an estimated 4.1 million tonnes of mineral phosphate (P) fertilizers between 2021 and 2023 across an average of approximately 157 million hectares of utilized agricultural area.

Growth in Biofuel and Oilseed Cultivation

The European biodiesel industry drives phosphate demand through increased oilseed production, particularly rapeseed and sunflower. Rising demand for biofuels to meet renewable energy targets creates strong consumption growth for phosphate fertilizers in oilseed farming. Fertilizers help improve seed quality and oil yield, making them vital for meeting EU blending mandates. Expansion of biofuel refining capacity across countries such as France, Germany, and the Netherlands further stimulates phosphate use. This trend strengthens long-term market growth prospects and enhances farmer investment in soil fertility management.

- For instance, ance produced approximately 3.83 million tonnes of rapeseed on a harvested area of 1.16 million hectares. This was a higher yield than the previous year due to improved weather conditions.

Rising Demand for High-Yield Crops

Europe’s phosphate fertilizer market benefits from growing demand for high-yield cereal, oilseed, and vegetable production. Farmers are adopting balanced phosphorus application to increase productivity and address soil nutrient depletion. Government-backed initiatives promoting food security and precision farming further strengthen demand. Expanding wheat and barley cultivation in France, Germany, and Poland continues to drive phosphate consumption. Sustainable farming practices, such as integrated nutrient management, are gaining traction, supporting the consistent use of phosphate fertilizers for improved soil health and crop output.

Key Trends & Opportunities

Shift Toward Specialty and Water-Soluble Fertilizers

European farmers increasingly adopt water-soluble phosphate fertilizers and fertigation-compatible solutions to support precision agriculture. These fertilizers allow targeted nutrient delivery, improving uptake efficiency and reducing runoff. This trend supports sustainable farming initiatives and helps meet EU nutrient reduction targets. Specialty products such as micronutrient-enriched phosphates present growth opportunities for manufacturers. The market is also seeing demand for customized blends tailored for specific crops and soil types, creating a lucrative niche for companies offering innovative, high-efficiency formulations.

- For instance, Lifosa operates a crystalline MAP plant with an annual production capacity of 30,000 tonnes of fully water-soluble fertilizer for fertigation systems.

Adoption of Digital Farming Solutions

Digital agriculture platforms and soil testing technologies are transforming phosphate fertilizer use across Europe. Farmers use data-driven insights to determine optimal application rates and timings, reducing waste and boosting crop performance. This precision approach aligns with environmental regulations and lowers input costs. Agritech collaborations and IoT-enabled nutrient monitoring solutions are creating new market opportunities. Suppliers integrating decision-support tools with fertilizer products gain a competitive edge, promoting efficient phosphorus usage and strengthening long-term relationships with farmers and cooperatives.

- For instance, the European Union has allocated hundreds of millions of euros for digital farming tools through various official programs, including Horizon Europe and the Common Agricultural Policy (CAP), with funding available from 2022–2024 and beyond.

Key Challenges

Stringent Environmental Regulations

The market faces pressure from strict EU regulations targeting phosphate runoff and eutrophication in water bodies. Policies limiting phosphorus application rates challenge fertilizer consumption growth, particularly in environmentally sensitive areas. Farmers must comply with nutrient management plans, adding compliance costs and limiting over-application. This regulatory environment pushes producers to innovate low-impact and slow-release phosphate solutions, but compliance complexity may slow adoption rates among small-scale farmers lacking access to advanced agronomic support systems.

Volatility in Raw Material Supply and Prices

Fluctuating prices of phosphate rock and rising energy costs impact production economics for European fertilizer manufacturers. Dependence on imports from Morocco and Russia exposes the market to geopolitical risks and supply chain disruptions. Price instability affects farmer purchasing decisions and can delay application schedules. This challenge pushes manufacturers to secure long-term supply contracts and explore recycling of phosphorus from wastewater as an alternative source. However, large-scale adoption of recycled phosphorus solutions is still limited and requires further investment.

Regional Analysis

Western Europe

Western Europe leads the Europe phosphate fertilizers market with over 40% market share in 2024. Countries such as France, Germany, and the UK drive demand due to extensive cereal and oilseed cultivation. Strong adoption of precision farming techniques, favorable CAP subsidies, and investment in sustainable agriculture support steady growth. France dominates the region, with high phosphate usage in wheat and barley farming. The presence of advanced distribution networks and major fertilizer producers enhances supply reliability. Western Europe is expected to maintain its lead as farmers adopt balanced nutrient management programs and water-soluble phosphate solutions.

Eastern Europe

Eastern Europe accounts for around 25% of the market share in 2024, led by Poland, Ukraine, and Romania. Expanding agricultural acreage and cost-effective phosphate availability support strong consumption. Farmers increasingly invest in modern fertilizers to boost productivity and export competitiveness. Growing oilseed and corn production also drives demand, supported by government-backed agricultural modernization programs. Despite price sensitivity, this region sees rising adoption of MAP and DAP fertilizers for high-yield crop cultivation. Eastern Europe shows significant growth potential as regional governments focus on soil fertility restoration and rural development initiatives, particularly post-harvest recovery in Ukraine.

Southern Europe

Southern Europe holds approximately 20% market share in 2024, driven by high phosphate demand for fruit, vegetable, and vineyard cultivation. Spain and Italy dominate this region due to intensive horticulture, greenhouse farming, and export-oriented production. Controlled phosphate application helps improve crop quality, taste, and shelf life. Adoption of drip irrigation systems and fertigation enhances fertilizer efficiency. Southern Europe benefits from strong government support for sustainable farming and climate-smart agriculture. Market growth is further supported by rising consumer preference for high-value crops and export-driven production of Mediterranean fruits, vegetables, and wine grapes.

Northern & Other Europe

Northern and other European countries collectively account for 15% of market share in 2024. The region includes Scandinavia, the Baltics, and smaller agricultural nations. Phosphate fertilizer demand is driven by cereal and forage production, especially in Denmark and Finland. Cold climate conditions limit growing seasons, but greenhouse farming and precision fertilizer application help optimize yields. Strict environmental regulations push adoption of slow-release and low-runoff phosphate solutions. While overall consumption is lower compared to other regions, strong focus on sustainable farming practices and government-backed nutrient management programs provide steady demand growth over the forecast period.

Market Segmentations:

By Product Type:

- Monoammonium Phosphate (MAP)

- Diammonium Phosphate (DAP)

- Single Superphosphate (SSP)

- Triple Superphosphate (TSP)

- Others

By Application:

- Cereals & Grains

- Oilseeds

- Fruits & Vegetables

- Others

By Geography:

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Rest of Europe

Competitive Landscape

The Europe phosphate fertilizers market is moderately consolidated, with leading players focusing on capacity expansion, product innovation, and sustainable solutions. Yara International, EuroChem Group, ICL Group Ltd, BASF SE, and Nutrien Ltd hold significant market presence, offering a wide portfolio of MAP, DAP, SSP, and customized phosphate blends. Companies invest in water-soluble and micronutrient-enriched fertilizers to meet the growing demand for precision farming and sustainable nutrient management. Strategic mergers, acquisitions, and partnerships strengthen supply networks across key agricultural regions. For instance, EuroChem has expanded production capacities in Lithuania and Belgium to enhance regional availability. Sustainability initiatives, such as BASF’s focus on reducing carbon footprint in fertilizer production, are gaining importance. Players also emphasize digital advisory services and soil testing solutions, providing integrated crop nutrition support to farmers. Competition is expected to intensify as regional and global manufacturers align with EU Green Deal targets and launch low-impact phosphate solutions.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Recent Developments

- In December 2023, Yara announced that it is acquiring the organic-based fertilizer business of Agribios, a company in Italy. The acquisition includes a production facility in Ronco all’Adige, focused on sustainable farming solutions through organic-based and organo-mineral fertilizers. This deal aligns with Yara’s strategy to expand its offerings in regenerative agriculture, complementing its current mineral fertilizer portfolio.

- In May 2022, Coromandel International, a fertilizer manufacturer, plans to buy a 45% stake in Baobab Mining and Chemicals Corporation (BMCC), a rock phosphate mining firm based in Senegal Africa, for $19.6 million (approximately $150 crore).

- In May 2022, Indian Potash Ltd signed a five-year agreement with Israel Chemical Ltd to import 0.6-0.65 million tonnes of potash muriate annually.

- In February 2022, EuroChem Group (hereafter referred to as “EuroChem” or “the Group”), a leading global producer of fertilizer, recently announced that it had completed the acquisition of the Serra do Salitre phosphate project in Brazil.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Market will see steady growth supported by rising demand for high-yield crop production.

- Precision farming adoption will boost use of water-soluble and controlled-release phosphate fertilizers.

- EU policies will push manufacturers to innovate low-runoff and environmentally safe formulations.

- Demand for MAP and DAP will remain dominant due to balanced nutrient content and efficiency.

- Digital soil monitoring and advisory tools will drive optimized fertilizer application rates.

- Oilseed production for biofuel will continue to expand, supporting phosphate consumption.

- Greenhouse and horticulture sectors will increase use of soluble phosphate products.

- Investment in local production will rise to reduce import dependence and price volatility.

- Companies will focus on sustainability, reducing carbon footprint in production processes.

- Competition will intensify with new product launches targeting EU Green Deal compliance.