Market Overview:

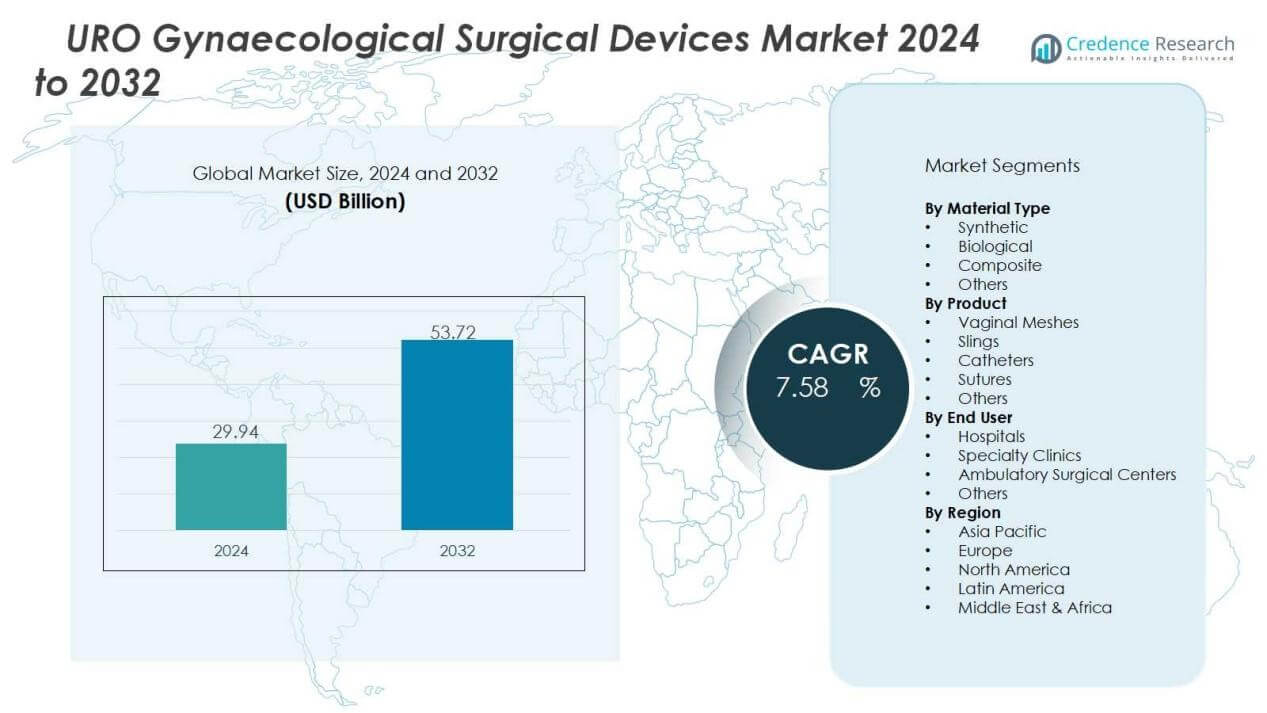

The uro gynaecological surgical devices market size was valued at USD 29.94 billion in 2024 and is anticipated to reach USD 53.72 billion by 2032, at a CAGR of 7.58% during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| URO Gynaecological Surgical Devices Market Size 2024 |

USD 29.94 Billion |

| URO Gynaecological Surgical Devices Market, CAGR |

7.58% |

| URO Gynaecological Surgical Devices Market Size 2032 |

USD 53.72 Billion |

Key market drivers include the aging female population, greater awareness of women’s health issues, and technological innovations in surgical devices. Demand is further reinforced by growing preference for minimally invasive and robotic-assisted procedures that reduce recovery time and improve patient outcomes. Healthcare providers are also investing in advanced solutions to reduce surgical complications and enhance long-term treatment effectiveness. These factors collectively support ongoing expansion of the market.

Regionally, North America dominates the uro gynaecological surgical devices market due to high healthcare expenditure, early adoption of innovative surgical technologies, and established reimbursement frameworks. Europe follows with significant growth, supported by strong clinical infrastructure and government health initiatives. Asia-Pacific is emerging as the fastest-growing region, fueled by increasing healthcare access, rising awareness of urogynecological conditions, and expanding investments in women’s health across China, India, and Southeast Asia.

Market Insights:

Market Insights:

- The uro gynaecological surgical devices market was valued at USD 29.94 billion in 2024 and is projected to reach USD 53.72 billion by 2032, growing at a CAGR of 7.58%.

- Rising prevalence of pelvic organ prolapse and urinary incontinence continues to drive surgical demand.

- Technological innovations, including robotic-assisted and minimally invasive devices, are enhancing patient outcomes.

- Increasing healthcare spending and infrastructure development worldwide support wider adoption of advanced devices.

- High device costs and limited reimbursement coverage restrict access in low- and middle-income regions.

- North America led with 38% market share in 2024, while Europe followed with 29% share.

- Asia-Pacific held 22% market share in 2024 and is expected to grow at the fastest rate.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Prevalence of Urogynecological Disorders Driving Surgical Demand:

The increasing incidence of pelvic organ prolapse, urinary incontinence, and other urogynecological conditions is a major driver for this market. Women in aging populations are at higher risk, which accelerates the need for surgical solutions. Early diagnosis and rising awareness of women’s health issues also contribute to demand. The uro gynaecological surgical devices market benefits from this sustained clinical need and continues to expand.

- For instance, Coloplast’s Restorelle Y mesh demonstrated an 89 percent anatomical success rate at 12 months and a 94 percent clinical cure rate with zero mesh-related complications in a prospective study of 120 patients undergoing robotic sacrocolpopexy.

Technological Advancements Enhancing Surgical Outcomes:

Innovations in surgical technology, including minimally invasive devices and robotic-assisted systems, have strengthened treatment effectiveness. These advancements enable shorter recovery times, fewer complications, and improved patient satisfaction. Hospitals and surgical centers are adopting new systems to deliver better outcomes. It has created an environment where device manufacturers are investing in R&D to maintain competitiveness.

- For instance, Intuitive Surgical’s da Vinci robotic systems have performed over 17 million procedures with more than 99% system uptime, demonstrating reliability and widespread adoption.

Growing Healthcare Spending and Infrastructure Development:

Increased healthcare expenditure and expanding clinical infrastructure worldwide are supporting higher adoption of advanced surgical devices. Emerging economies are investing in better surgical facilities and skilled professionals to address women’s health concerns. Governments and private players are working to improve healthcare access, further encouraging demand. It ensures consistent growth opportunities for device suppliers across multiple regions.

Shift Toward Minimally Invasive and Patient-Centric Care:

Patients and providers prefer minimally invasive procedures that reduce hospital stays and recovery periods. Rising acceptance of laparoscopy and robotic platforms reflects this shift. Insurers and healthcare systems also support technologies that lower complications and long-term treatment costs. It continues to shape the uro gynaecological surgical devices market, aligning innovations with patient-centered care priorities.

Market Trends:

Integration of Robotic and Minimally Invasive Surgical Technologies:

Robotic and minimally invasive platforms are becoming central trends in urogynecological surgeries. Surgeons are increasingly using robotic-assisted devices to perform precise and less invasive procedures. These technologies reduce complications, shorten recovery periods, and improve surgical accuracy. Hospitals are prioritizing the adoption of advanced tools to meet patient demand for safer and faster recovery. Training programs are expanding to equip surgeons with necessary skills, further driving adoption. The uro gynaecological surgical devices market is witnessing strong momentum as device manufacturers innovate to improve usability and clinical efficiency.

- For instance, Medtronic’s Hugo™ robotic-assisted surgery system with the LigaSure™ RAS vessel-sealing technology, CE-marked in July 2025, seals vessels up to 7 mm in diameter securely in approximately 2 second

Focus on Patient-Centric Solutions and Customized Implants:

There is a growing emphasis on patient-specific treatment approaches supported by customized implants and meshes. Manufacturers are investing in biocompatible and lightweight materials to enhance safety and comfort. Rising patient awareness of treatment choices has increased demand for tailored devices. Healthcare providers are responding with solutions designed to reduce post-surgical complications and improve quality of life. It has shifted market dynamics toward more personalized and outcome-driven solutions. The uro gynaecological surgical devices market continues to evolve with innovations that align with these patient-centered expectations.

- For instance, Medtronic plc demonstrated the clinical safety and effectiveness of its Hugo robotic-assisted surgery system in a 137-patient multi-center IDE study presented in April 2025, underscoring its role in enhancing precision and personalized surgical care in urologic procedures.

Market Challenges Analysis:

High Costs and Limited Access to Advanced Surgical Devices:

The adoption of advanced surgical devices is often restricted by high costs and limited reimbursement coverage. Hospitals in low- and middle-income countries face budget constraints that slow technology penetration. Patients in these regions may not afford advanced procedures, reducing overall adoption rates. The uro gynaecological surgical devices market faces challenges in balancing innovation with affordability. It creates pressure on manufacturers to introduce cost-effective solutions without compromising quality. Unequal access to advanced care continues to limit the global growth potential of this market.

Regulatory Hurdles and Risk of Post-Surgical Complications:

Stringent regulatory requirements delay the approval of new devices, impacting market entry timelines. Compliance with safety and performance standards often increases development costs for manufacturers. Concerns about complications related to surgical meshes and implants also create hesitation among patients and providers. Negative publicity from product recalls and litigation further influences device adoption. The uro gynaecological surgical devices market must address these concerns through stronger clinical validation and transparent communication. It underscores the need for innovation that prioritizes patient safety and regulatory alignment.

Market Opportunities:

Rising Demand in Emerging Economies with Expanding Healthcare Infrastructure:

Emerging economies present significant opportunities due to growing healthcare investments and improving access to specialized care. Governments and private providers are expanding hospital infrastructure and surgical facilities, enabling wider adoption of advanced devices. Rising awareness of women’s health issues is encouraging more patients to seek treatment for urogynecological conditions. The uro gynaecological surgical devices market can capitalize on these trends by offering affordable yet innovative solutions. It creates a strong pathway for manufacturers to penetrate untapped regions and expand their global footprint. Local partnerships and training initiatives further enhance adoption prospects.

Innovation in Biocompatible Materials and Digital Surgical Solutions:

Advances in biocompatible materials and patient-specific implants offer opportunities for safer and more effective surgeries. Manufacturers are focusing on lightweight, durable, and customized meshes and implants to improve patient outcomes. Integration of digital technologies such as AI-assisted navigation and data-driven surgical planning is also gaining traction. Healthcare systems are increasingly open to adopting tools that reduce complications and optimize recovery. It allows the uro gynaecological surgical devices market to align with the global shift toward precision and personalized care. Continuous innovation in these areas positions the industry for sustainable growth and differentiation.

Market Segmentation Analysis:

By Product:

The uro gynaecological surgical devices market includes products such as vaginal meshes, slings, catheters, and sutures. Vaginal meshes and slings dominate due to their effectiveness in treating pelvic organ prolapse and urinary incontinence. Catheters and sutures maintain steady demand, supported by their role in post-surgical care. It continues to see innovation in product design aimed at reducing complications and improving patient comfort. Hospitals and clinics favor devices that combine safety with ease of use.

- For instance, Boston Scientific’s Advantage Fit mid-urethral sling achieved a 92% continence success rate at 12-month follow-up in a multicenter clinical trial.

By Material:

Materials used in these devices include synthetic, biological, and composite variants. Synthetic materials, such as polypropylene, hold a significant share due to durability and cost-effectiveness. Biological materials are gaining traction for their biocompatibility and reduced risk of rejection. Composite materials provide a balance between strength and flexibility, supporting broader adoption. The uro gynaecological surgical devices market benefits from ongoing research into advanced biomaterials designed to improve surgical outcomes.

- For instance, Caldera Medical’s Vertessa™ Lite Y-Mesh polypropylene implant features a macroporous monofilament structure with a pore size of 1500 µm, enhancing tissue integration while maintaining durability.

By End User:

Key end users include hospitals, specialty clinics, and ambulatory surgical centers. Hospitals dominate due to advanced infrastructure and higher patient inflow for urogynecological surgeries. Specialty clinics are expanding with focused expertise and adoption of minimally invasive procedures. Ambulatory centers are growing rapidly, driven by demand for day-care surgeries and shorter recovery times. It highlights the shift toward patient-centered care across different healthcare settings.

Segmentations:

By Product:

- Vaginal Meshes

- Slings

- Catheters

- Sutures

- Others

By Material:

- Synthetic

- Biological

- Composite

- Others

By End User:

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Others

By Region:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East

- GCC Countries

- Israel

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

Regional Analysis:

North America and Europe:

North America accounted for 38% market share in 2024, while Europe held 29% market share in the same year. Both regions dominate due to advanced healthcare infrastructure and early adoption of innovative surgical technologies. Strong reimbursement systems and high awareness of women’s health support widespread use of minimally invasive devices. The uro gynaecological surgical devices market in these regions is strengthened by continuous clinical research and product development. It benefits from well-established training programs that enhance surgeon expertise. Government initiatives in women’s health also contribute to maintaining leadership positions in these markets.

Asia-Pacific:

Asia-Pacific represented 22% market share in 2024 and is projected to expand at the highest CAGR during the forecast period. Rapid urbanization and rising healthcare investments are fueling adoption of advanced surgical devices. Increasing patient awareness of treatment options and growing prevalence of urogynecological disorders drive regional demand. It benefits from expanding hospital networks in China, India, and Southeast Asia. Governments are actively improving access to specialized surgical care. Partnerships with international device manufacturers further accelerate regional market expansion.

Latin America and Middle East & Africa:

Latin America captured 6% market share in 2024, while the Middle East & Africa accounted for 5% market share. Growth in these regions is supported by improving healthcare infrastructure and gradual adoption of minimally invasive procedures. Private sector investments and medical tourism are helping strengthen device availability. The uro gynaecological surgical devices market here faces challenges with affordability and limited specialist access. It still holds potential due to rising awareness of women’s health and ongoing infrastructure development. International collaborations are expected to support steady growth across these regions.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Aesculap

- Johnson and Johnson

- Integra LifeSciences

- Ethicon

- Smith and Nephew

- Teleflex

- Baxter International

- R. Bard

- Cook Medical

- Stryker

- Boston Scientific

Competitive Analysis:

The uro gynaecological surgical devices market is highly competitive with strong participation from global healthcare companies. Leading players include Aesculap, Johnson & Johnson, Integra LifeSciences, Ethicon, Smith & Nephew, Teleflex, Baxter International, R. Bard, and Cook Medical. These companies compete on product innovation, global reach, and clinical reliability to secure strong positions in hospitals and specialty clinics. It benefits from continuous investment in advanced materials, minimally invasive devices, and robotic-assisted solutions that improve patient outcomes. Companies are expanding portfolios through mergers, acquisitions, and collaborations with healthcare providers to strengthen distribution and training. Regional expansion into emerging markets remains a core strategy, supported by rising demand for advanced surgical care. Competitive intensity is expected to increase as new entrants and local manufacturers introduce cost-effective alternatives, creating pressure on pricing and differentiation.

Recent Developments:

- In May 2025, Aesculap extended its strategic partnership with Ascendco Health for another 10 years to expand surgical instrument tracking across U.S. health systems.

- In July 2025, Johnson & Johnson reported strong Q2 2025 financial results with multiple new product launches including daily disposable multifocal toric contact lenses and the VOLT™ wrist and proximal humerus plating systems in the U.S.

Report Coverage:

The research report offers an in-depth analysis based on Product, Material, End User and Region. It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- Demand for minimally invasive and robotic-assisted procedures will continue to accelerate global adoption.

- Manufacturers will invest in biocompatible materials and patient-specific implants to improve safety and comfort.

- Digital integration, including AI-driven surgical planning and navigation, will gain wider acceptance.

- Healthcare systems will prioritize solutions that reduce complications and lower long-term treatment costs.

- Emerging economies will become critical growth hubs due to rising healthcare infrastructure and awareness.

- Collaborations between device makers and hospitals will expand training programs for advanced surgical techniques.

- Regulatory alignment and stronger clinical validation will remain priorities to ensure patient trust.

- Personalized treatment solutions will shape device design and enhance long-term patient outcomes.

- Telemedicine and digital health platforms will indirectly support pre- and post-surgical care in urogynecology.

- The uro gynaecological surgical devices market will experience steady growth, driven by innovation and global demand for women’s health solutions.