Market Overview:

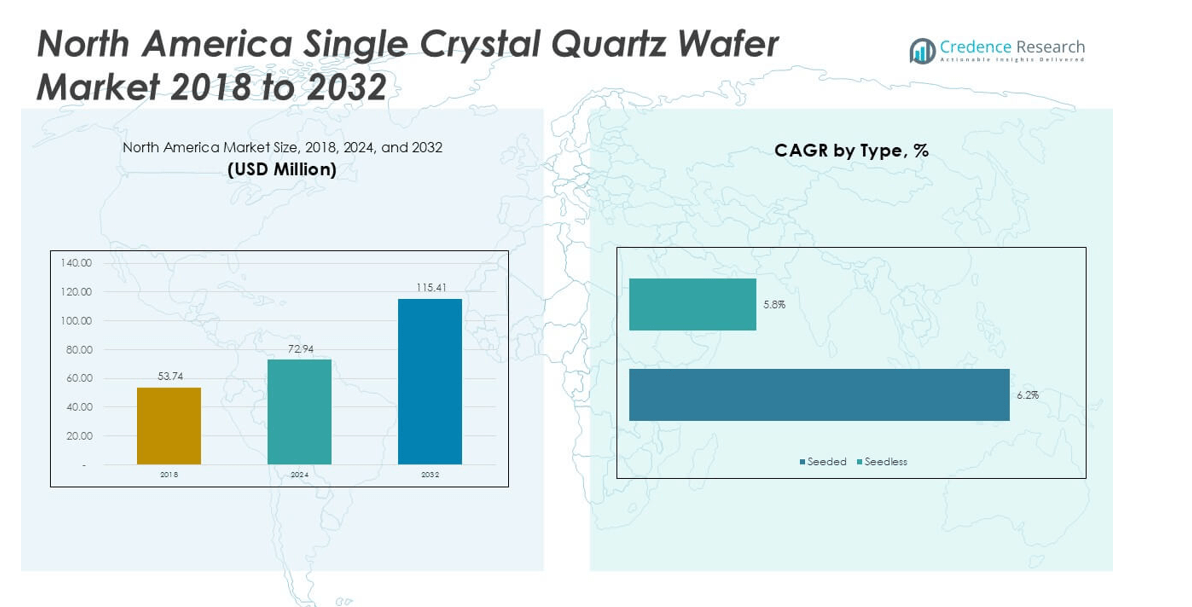

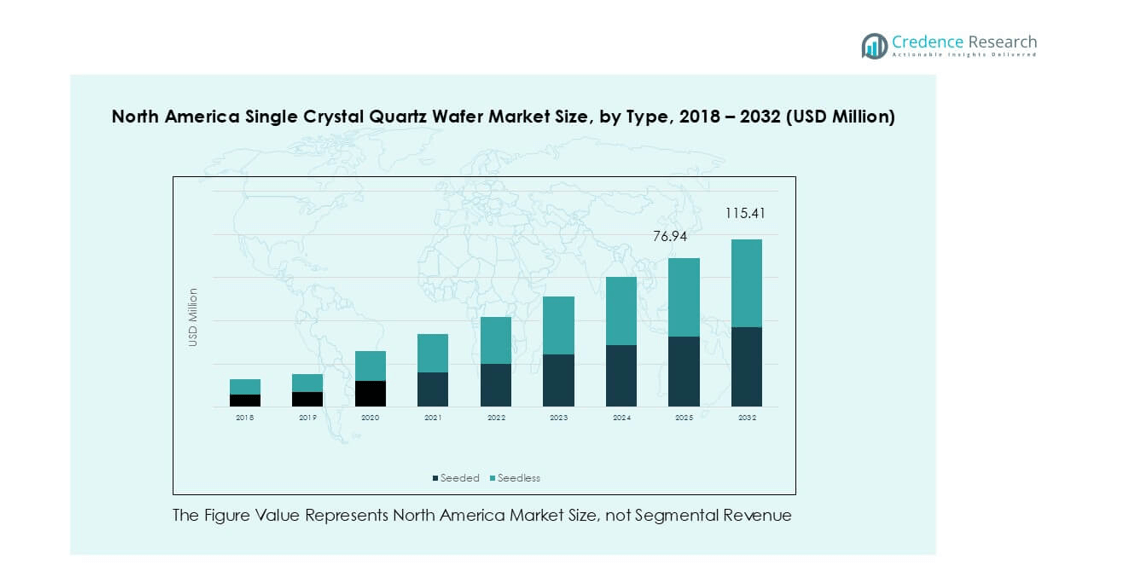

North America Single Crystal Quartz Wafer market size was valued at USD 53.74 million in 2018, increased to USD 72.94 million in 2024, and is anticipated to reach USD 115.41 million by 2032, at a CAGR of 6.0% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| North America Single Crystal Quartz Wafer Market Size 2024 |

USD 72.94 million |

| North America Single Crystal Quartz Wafer Market , CAGR |

6% |

| North America Single Crystal Quartz Wafer Market Size 2032 |

USD 115.41 million |

The North America single crystal quartz wafer market is led by key players including Corning Incorporated, Noah Chemicals, Semiconductor Wafer, Inc., MTI Corporation, and University Wafer, Inc., alongside international participants such as NIHON DEMPA KOGYO CO., LTD., Xiamen Powerway, and MicroChemicals GmbH. Corning Incorporated holds a strong position due to its advanced material technologies and large-scale production capabilities, while Noah Chemicals and Semiconductor Wafer, Inc. focus on specialized wafer solutions for electronics and semiconductor applications. MTI Corporation and UniversityWafer, Inc. cater to research-driven and niche demand segments. Regionally, the United States dominates the market with over 70% share in 2024, driven by its robust semiconductor manufacturing base, government-backed chip production initiatives, and growing MEMS and biotechnology applications. Canada and Mexico follow, each contributing around 15% share, supported by advancements in healthcare technologies and electronics assembly, respectively, strengthening the region’s overall market ecosystem.

Market Insights

- The North America single crystal quartz wafer market was valued at USD 72.94 million in 2024 and is projected to reach USD 115.41 million by 2032, growing at a CAGR of 6.0% during the forecast period.

- Market growth is driven by rising semiconductor manufacturing, increasing MEMS adoption in electronics, and expanding use of quartz wafers in biotechnology and IC packaging applications.

- Key trends include a shift toward larger-diameter wafers above 8 inches and growing integration of quartz wafers into IoT, 5G, and smart devices to ensure precision and reliability.

- The competitive landscape features leading players such as Corning Incorporated, Noah Chemicals, Semiconductor Wafer, Inc., and NIHON DEMPA KOGYO CO., LTD., with companies focusing on R&D, capacity expansions, and strategic collaborations to maintain market presence.

- Regionally, the United States holds over 70% share, followed by Canada and Mexico at around 15% each; by segment, 5–8 inch wafers account for more than 50% share in 2024

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

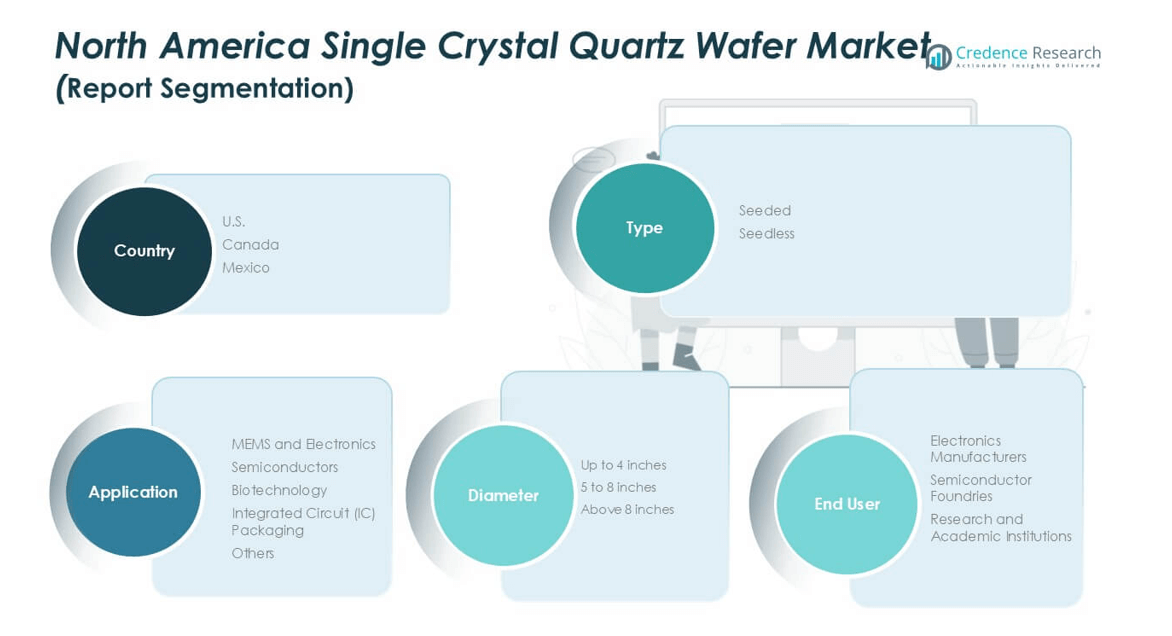

Market Segmentation Analysis:

By Type

The seeded segment dominated the North America single crystal quartz wafer market in 2024, holding over 60% share. Seeded wafers are preferred for their superior crystalline uniformity, stability, and consistency in performance, which are crucial for high-end electronics and semiconductor applications. Their ability to meet stringent specifications in microelectronics and precision optics drives their dominance. Seedless wafers, while gaining traction for cost-sensitive applications, remain limited due to challenges in ensuring consistent structural quality. Rising demand for advanced electronic devices ensures steady growth for seeded wafers across industries.

- For instance, Shin-Etsu Chemical produces ultra-high-purity synthetic quartz substrates (like VIOSIL) for advanced photomask blanks, which require extremely low defect densities for use in semiconductor lithography.

By Diameter

The 5 to 8 inches diameter segment led the market in 2024, accounting for more than 50% share. These wafers offer an optimal balance of scalability and performance, making them highly suitable for semiconductor and MEMS applications. Manufacturers favor this size range due to efficient production yields and compatibility with existing fabrication infrastructure. The up to 4 inches segment retains importance in research and specialty applications, while above 8 inches wafers are gradually emerging in advanced semiconductor production. Strong adoption in integrated circuits and electronics sustains the leadership of the 5 to 8 inches category.

- For instance, GlobalWafers Co. expanded its 200 mm (8-inch) wafer production capacity by 150,000 wafers per month at its Taisil facility in 2023, strengthening supply for power devices and analog ICs.

By Application

MEMS and electronics applications represented the dominant segment in 2024, capturing over 40% share of the market. The widespread use of quartz wafers in sensors, resonators, and frequency control devices underpins this leadership. Increasing deployment of MEMS in smartphones, automotive systems, and IoT devices continues to drive demand. Semiconductors also contribute significantly, driven by the rising need for high-performance computing and data storage solutions. Biotechnology and IC packaging segments are expanding steadily with innovations in medical devices and miniaturized electronics, but MEMS and electronics remain the primary driver of wafer consumption in North America.

Key Growth Drivers

Rising Demand from Semiconductor Manufacturing

The expansion of the semiconductor industry in North America acts as a primary driver for single crystal quartz wafer adoption. With the region being home to major semiconductor fabrication plants, the need for high-performance substrates that deliver precision and reliability is increasing. Quartz wafers play a vital role in photolithography, etching, and deposition processes due to their thermal stability and low impurity levels. The growth of advanced nodes in semiconductor manufacturing, particularly in the U.S., further strengthens this demand. Government incentives to boost domestic chip production under initiatives such as the CHIPS and Science Act also enhance wafer requirements. As semiconductor companies scale production capacity to meet global demand, the consumption of quartz wafers is expected to rise steadily, ensuring their role as a critical enabler of technology advancement in integrated circuits and electronic components.

- For instance, Intel announced in 2023 a $20 billion investment in two new fabs in Ohio, designed to support 7 nm and below process nodes requiring precise quartz wafer-based photomasks.

Expanding MEMS and Electronics Applications

Microelectromechanical systems (MEMS) and electronics applications represent another strong growth driver. Quartz wafers are widely used in resonators, oscillators, and frequency control devices that form the backbone of electronic communication, automotive systems, and consumer devices. The rising adoption of MEMS in smartphones, wearables, and automotive sensors has accelerated wafer demand across North America. Additionally, IoT-enabled applications in smart homes, connected vehicles, and industrial automation rely heavily on MEMS-based solutions. Quartz wafers offer high accuracy and reliability, making them indispensable in such applications. The push toward miniaturization of devices while maintaining performance standards further increases reliance on quartz substrates. As electronics manufacturers continue to innovate with compact, multifunctional devices, the MEMS and electronics segment will remain a key catalyst for market growth, expanding wafer applications into both consumer and industrial ecosystems.

- For instance, Broadcom supplied a large volume of Film Bulk Acoustic Resonator (FBAR) RF filters for 5G smartphones in 2023. These filters, a type of Bulk Acoustic Wave (BAW) technology, typically rely on silicon wafer substrates rather than quartz.

Advancements in Biotechnology and Healthcare Devices

The growing use of single crystal quartz wafers in biotechnology and healthcare further drives market growth. Quartz wafers serve as substrates for biosensors, lab-on-chip devices, and microfluidic platforms, enabling precise detection and diagnosis in medical applications. With North America leading global innovation in life sciences, demand for wafers in biomedical research and diagnostic tools is rapidly expanding. Increasing healthcare investments and emphasis on advanced diagnostic systems foster steady uptake in this sector. Additionally, the rise of personalized medicine and point-of-care testing accelerates adoption of biosensor technologies based on quartz substrates. Their superior optical and piezoelectric properties make them suitable for sensitive detection in genomics, proteomics, and immunoassays. As biotechnology companies and research institutes continue to advance diagnostic and therapeutic innovations, quartz wafers will remain a critical component supporting accuracy and efficiency in healthcare solutions.

Key Trends & Opportunities

Shift Toward Larger-Diameter Wafers

One of the emerging trends in the North America single crystal quartz wafer market is the gradual shift toward larger-diameter wafers, particularly those above 8 inches. Larger wafers enable higher productivity by allowing more devices to be fabricated per substrate, reducing costs for semiconductor and electronics manufacturers. Although adoption is currently limited by fabrication compatibility and higher production costs, investments in advanced wafer processing facilities are expanding opportunities. This shift is particularly relevant for integrated circuit packaging and advanced semiconductor applications where efficiency and scale are critical. Companies investing in technology upgrades to accommodate larger wafers are well-positioned to capture a competitive advantage in the market. Over the forecast period, this transition is expected to gain momentum as manufacturers seek cost-effective solutions while meeting the rising demand for high-performance devices.

- For instance, in June 2022, GlobalWafers announced plans to build a new facility in Sherman, Texas, to manufacture 300 mm (12-inch) wafers. While the initial investment was approximately $3.5 billion, the company announced an additional $4 billion in May 2025, bringing its total investment in the U.S. to $7.5 billion.

Integration with IoT and Smart Devices

The rapid growth of IoT and smart devices presents a significant opportunity for quartz wafer manufacturers. Quartz wafers form the foundation of oscillators and timing devices essential for reliable communication and synchronization in connected systems. The proliferation of smart homes, autonomous vehicles, and industrial IoT platforms has driven exponential demand for precise timing components. In North America, the adoption of 5G networks further amplifies the role of quartz wafers in enabling stable frequency control. Manufacturers that align their offerings with the expanding IoT ecosystem will benefit from increased application diversity. Beyond consumer electronics, the integration of quartz wafers into mission-critical systems like defense, aerospace, and healthcare devices opens long-term growth opportunities. This trend positions quartz wafers as a cornerstone material supporting the digital transformation across multiple industries in the region.

Key Challenges

High Manufacturing Costs and Supply Constraints

The production of single crystal quartz wafers involves highly specialized processes that require precision and advanced equipment, making manufacturing costs considerably high. North America faces challenges in scaling local supply, as much of the raw quartz and processing capabilities remain concentrated in other regions. This reliance on global supply chains increases vulnerability to disruptions, price fluctuations, and geopolitical tensions. Additionally, the cost burden limits adoption in cost-sensitive applications, slowing the penetration of quartz wafers beyond premium electronics and semiconductors. Manufacturers must invest heavily in R&D and processing innovation to lower costs while ensuring consistent quality. Without significant cost optimization and diversification of supply sources, this challenge could restrict market expansion despite strong demand from end-use industries.

Competition from Alternative Materials

The market also faces growing competition from alternative materials such as silicon, sapphire, and synthetic substitutes that can serve as cost-effective or application-specific replacements. For instance, silicon wafers are widely used in semiconductor applications due to their established supply chain and lower production costs. Sapphire substrates are gaining traction in optical and high-frequency applications, challenging quartz in select niches. As end-users explore alternatives to balance cost and performance, quartz wafer adoption may experience pressure. The challenge lies in demonstrating superior functional benefits such as higher purity, thermal stability, and piezoelectric properties that alternatives cannot match. Continuous innovation and differentiation will be critical for quartz wafer manufacturers to maintain competitiveness against these substitutes in the evolving North American technology landscape.

Market Segmentations:

By Type

By Diameter

- Up to 4 inches

- 5 to 8 inches

- Above 8 inches

By Application

- MEMS and Electronics

- Semiconductors

- Biotechnology

- Integrated Circuit (IC) Packaging

- Others

By End User

- Electronics Manufacturers

- Semiconductor Foundries

- Research and Academic Institutions

By Geography

Competitive Landscape

The North America single crystal quartz wafer market is moderately consolidated, with a mix of established multinational corporations and specialized regional suppliers competing for market share. Leading players such as Corning Incorporated, Noah Chemicals, and Semiconductor Wafer, Inc. dominate through strong product portfolios, advanced manufacturing capabilities, and strategic partnerships with semiconductor and electronics companies. Firms like MTI Corporation and University Wafer, Inc. focus on niche applications and research-oriented demand, while international players such as NIHON DEMPA KOGYO CO., LTD. and Xiamen Powerway strengthen competition by expanding their presence in the region. Companies are investing heavily in R&D to develop larger-diameter wafers, improve crystalline quality, and lower production costs to meet the rising demand from semiconductors, MEMS, and biotechnology applications. Strategic moves including acquisitions, capacity expansions, and collaborations with research institutes remain common, highlighting a competitive environment where innovation and supply reliability are key differentiators.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Noah Chemicals

- Semiconductor Wafer, Inc.

- MTI Corporation

- Corning Incorporated

- Vritra Technologies

- Xiamen Powerway

- MicroChemicals GmbH

- NIHON DEMPA KOGYO CO., LTD.

- INSACO, Inc.

- University Wafer, Inc.

- Other Key Players

Recent Developments

- In July 2025, Xiamen Powerway (PAM-XIAMEN) remains an active supplier of single crystal quartz wafers, specializing in X-cut, Y-cut, Z-cut, and ST-cut orientations up to 3-inch diameters.

- In July 2025, NDK highlighted its advancement in mass-producing high-uniformity quartz crystals using proprietary technologies. Their latest offering includes synthetic quartz wafers with AT-cut and tuning fork wafers, and a development plan for larger 6-inch wafers to cater to growing SAW device demand and frequency control in next-gen electronics.

- In August 2024, NDK (NIHON DEMPA KOGYO CO., LTD.) showcased its synthetic quartz crystals and quartz wafers for timing and optical applications at electronica India 2024, participating through a distributor’s booth at the trade fair.

Report Coverage

The research report offers an in-depth analysis based on Type, Diameter, Application, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand steadily with strong demand from semiconductor manufacturing.

- MEMS and electronics applications will remain the largest consumers of quartz wafers.

- Biotechnology and healthcare will offer new growth opportunities through biosensors and diagnostic devices.

- Larger-diameter wafers above 8 inches will gain higher adoption in advanced applications.

- The United States will continue to dominate the regional market with the highest share.

- Canada will strengthen its role in biotechnology-driven applications and research use.

- Mexico will grow as a key hub for electronics and automotive-related wafer demand.

- Companies will invest in R&D to improve wafer quality and lower production costs.

- Competition from alternative materials will drive manufacturers to differentiate on performance.

- Strategic collaborations and capacity expansions will shape the competitive landscape in the region.